There are many stocks that are beloved by income focused investors, one group of those are the so called Dividend Aristocrats — companies that have raised their payout for at least 25 years in a row. An even more elite group of companies are the Dividend Kings, companies that have raised their dividend for at least 50 years in a row. You can see the full list of all 25 Dividend Kings here.

[REITs]Q1 hedge fund letters, conference, scoops etc

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Click here to download my Dividend Kings Excel Spreadsheet now. Keep reading this article to learn more.

There aren’t many of those companies with a five-decade dividend growth track record, but those that exist are worthy of a closer look. In this article, we will take a closer look at healthcare giant Johnson & Johnson (JNJ).

Business Overview

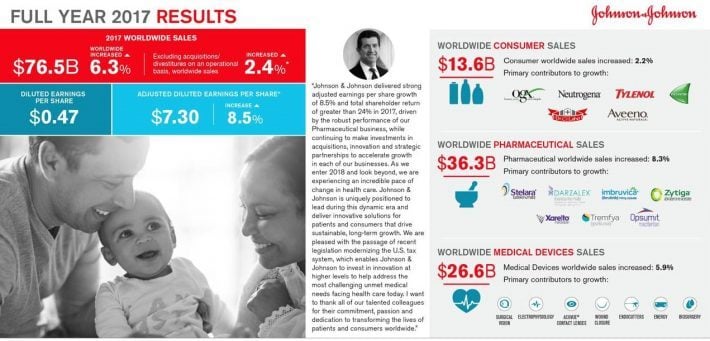

Johnson & Johnson operates in three separate industries: Consumer health products, medical devices, and pharmaceuticals. This business model means that Johnson & Johnson’s revenue stream is well diversified. The company is not too dependent on a positive growth outlook in one of its segments, as good results from one business can balance out weaker results in another segment.

None of the industries Johnson & Johnson operates in are cyclical: The consumer goods segment sells products that people require for their everyday life, the medical devices and pharma products are necessary to keep people healthy.

Source: JNJ presentation, page 1

Johnson & Johnson’s pharmaceuticals segment is the most important one, strong growth in this area over the last couple of years has made it grow to about half of the company’s sales. A good performance of the other business units was still needed for Johnson & Johnson’s stellar long term track record.

The company has increased its sales consistently through the last decades, although the growth momentum has slowed down a bit in the 2010s. This is not surprising though, as a 10% growth rate gets harder to achieve from a higher base.

Currency rates (i.e. a very strong dollar) also adversely impacted Johnson & Johnson’s dollar denominated top line in the last couple of years. Since the dollar has gotten weaker again, this should not hurt the company going forward, though. During the most recent quarter Johnson & Johnson’s top line grew by an impressive 12%, which shows that the company can still grow at a very attractive pace.

Growth Prospects

In the last couple of years the main growth driver was Johnson & Johnson’s pharmaceuticals division, and that will likely remain true going forward as well.

Source: JNJ presentation, page 12

The company is ramping up sales from new drugs, such as Darzalex, which has resulted in a very compelling 18% revenue growth rate during the most recent quarter. Johnson & Johnson’s oncology portfolio has developed into the second biggest pharma unit, and with its high growth momentum it is likely that it will at one point be the main revenue contributor for Johnson & Johnson’s pharmaceuticals division.

That would be a positive, as the global oncology market is poised for long-lasting growth: During the 2014 to 2020 period the global oncology drug market is poised to grow by more than 7% annually. Johnson & Johnson’s young drug portfolio with potent products such as Imbruvica, in cooperation with AbbVie (ABBV), will likely continue to grow faster than the market as a whole. Double digit annual sales increases for Johnson & Johnson’s oncology drug unit thus look quite likely.

Unsurprisingly oncology is also a key area for Johnson & Johnson’s R&D efforts: The company has 17 phase III studies running in order to get new oncology drugs to the market or in order to get new indications for its existing drugs. Thanks to the fact that some new approvals are likely due to so many phase III studies being underway, the growth from Imbruvica and Darzalex is poised to continue in the coming years.

The growth momentum for Johnson & Johnson’s other units is less outstanding, but the company will see rising sales there as well. The global medical device market will continue to grow due to advancements in healthcare provisions in developing countries and due to an aging population in industrial nations. A more senior population will mean that there is a growing need for orthopaedics (hips, knees, etc.) and for cardiovascular medtech products. Those are areas where Johnson & Johnson is well positioned, thus the medical devices segment is poised for further growth as well.

Competitive Advantages & Recession Performance

The healthcare industry is very sizeable and holds many major players. None of them combine the excellent diversification and great balance sheet that Johnson & Johnson possesses, though. The company’s AAA-rated balance sheet is a major positive in a rising rates environment, as Johnson & Johnson will not be negatively impacted by higher interest expenses.

The fortress balance sheet also provides Johnson & Johnson with the ability to engage in M&A activities wherever and whenever the company pleases: In a less fortunate economic environment Johnson & Johnson would not get into problems and could acquire targets for a cheap price.

The low cyclicality of the markets the company targets, combined with great diversification not only across products, but also geographically, makes Johnson & Johnson recession-proof. The company’s performance during the Great Recession is below:

- 2007 earnings-per-share of $4.15

- 2008 earnings-per-share of $4.57 (10% increase)

- 2009 earnings-per-share of $4.63 (1% increase)

- 2010 earnings-per-share of $4.76 (3% increase)

In 2010 Johnson & Johnson already earned more than in 2008, the financial crisis thus put just a small dent into the company’s great results.

Valuation & Expected Returns

Johnson & Johnson expects earnings-per-share of $8.10, at the midpoint of 2018 guidance. As a result, the stock currently trades for a price-to-earnings ratio of 16.4. This is a reasonable valuation, especially for such a high-quality company. The stock has held an average price-to-earnings ratio of 15.7 in the past 10 years.

Source: Value Line

The valuation may not expand further beyond current levels, but the stock can still generate healthy returns, from earnings growth and dividends. A potential breakdown of future returns is as follows:

- 6%-8% earnings growth

- 2.5% dividend yield

When it comes to expected returns, one way to make an estimate for the future is to combine the dividend yield and the dividend growth rate. In Johnson & Johnson’s case this gets us to ~ 9%. This easy calculation assumes that the dividend growth rate stays at the same level it has been in the past and that the company’s shares continue to trade at a yield of 2.5%. It would, however, be possible for the yield to increase (share prices don’t grow as fast as the dividend) or for the yield to decline (share prices grow faster than the dividend).

Analysts are currently forecasting a 7.8% EPS growth rate over the coming years — due to the company’s strong growth outlook, that does not seem unrealistic. We can look at a scenario analysis to see where Johnson & Johnson’s shares could trade in five years:

Assumption: EPS of $8.10 in 2018, 7.8% annual growth through 2023, which means EPS of $11.80 in 2023.

We see that Johnson & Johnson would produce mid-single digits annual returns even if its PE ratio plummets to a 13 times multiple (from a current level of 18.4). If the valuation remains at the current level the company’s investors would get double-digit annual total returns. If the valuation declines somewhat, investors would see high single digit annual returns over the coming six years.

It is impossible to know which valuation Johnson & Johnson’s shares will trade at a couple of years down the road, but the scenario analysis gives us a glimpse: Even if things go south the returns investors will receive are not bad at all. Multiple expansion would lead to very high returns, if the multiple declines to a 17 or 16 times PE ratio, returns would still be quite attractive.

For income investors, a key argument for buying Johnson & Johnson’s shares is the dividend, which yields 2.5% right now. The company has made four dividend payments at the $0.84 per share level, thus it is very likely that the next dividend announcement (end of April) will feature another dividend increase.

Johnson & Johnson’s dividend has grown very smoothly over the years, the dividend growth rate averaged 6% to 7% over the last couple of years. Johnson & Johnson has increased its dividend for 55 years in a row already, something investors find only seldom, therefore Johnson & Johnson is a member of the exclusive Dividend Kings.

Shares of Johnson & Johnson are not extremely cheap right here, but they are not overly expensive either. For a high-quality company like Johnson & Johnson the current price looks quite fair, and the current price will allow for compelling total returns with a high likelihood.

Final Thoughts

Johnson & Johnson is the epitome of a safe investment: Great diversification across industries and geographic markets, a fortress balance sheet, a dividend growth history spanning decades and products that are not cyclical at all. Even during the last financial crisis the company continued to make billions and continued to share this wealth with investors.

The growth outlook is good and Johnson & Johnson will provide attractive total returns over the coming years — at least with a very high likelihood. This Dividend King hence looks like a great core holding for income-focused investors who want to build a sleep-well-at-night portfolio.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

Article by Sure Dividend

{kind=link}