The bullish outlook has increased momentum in the stock which could propel it higher over Q1

Shares of cancer and disease focused biotech Zymeworks (NASDAQ:ZYME) strengthened 15.80% in trading on Friday as the market found out that the largest shareholder EcoR1 Capital bought more shares in the company which sparked a flurry of investor buying demand. The transaction was first seen in Fintel’s insider trading tracker on Thursday evening.

The latest spike of investor demand appetite has boosted ZYME’s total return above 115% from the stock’s annual low point in early September when the stock was sub $5. The stock has been charging higher in 2023 since Zymeworks management released a corporate update on the firm’s outlook last week.

Q4 2022 hedge fund letters, conferences and more

Despite the latest rally, Zyemworks shares continue to trade well below the pandemic highs which pushed the stock above $50.

In a form 4 filed with the SEC, Zymeworks shareholder EcoR1 Capital disclosed the purchase of 1,026,300 shares on market with an average cost per share of $7.67.

The latest transactions by the San Francisco based biotech hedge fund increased the funds total share ownership count to 8,594,873 shares or and boosted ownership in the float from around 12% up to 13.6%.

EcoR1 Capital is the largest shareholder on the register followed by Redmile Group.

The fund's newest investment followed a positive financial guidance update from management. In the update Zymeworks told investors the company exited 2022 with about $490 million in cash resources which excluded reimbursement payments incurred from the Jazz R&D agreement worth $30 million in Q4.

Zymeworks received a payment of $375 million from the collaboration agreement with Jazz which substantially improved the financial position of the company and reduced cash burn. Over 2023 and 2024, Zymeworks expects to earn more milestone payments under the existing agreements and possible new agreements that will be used towards to advance the current product pipeline.

Management has also reduced its rate of cash burn and believes it can keep costs in the order of $90 to $120 million over 2023 which includes Capex of $15 million.

The firm is forecasting that the current cash balance will fund its operations, research and development programs through 2026 and possibly further.

ZYME’s CFO Christ Astle stated to investors “We now have the balance sheet strength to both fund our current operating plans and be opportunistic in evaluating additional R&D opportunities internally and externally, while maintaining a strong financial position”

Additionally, in conjunction to the firm's internal re-organization, the groups Chief Medical Officer Neil Josephson will be departing the company.

Liquidity concerns around funding requirements have been overhanging the stock which was a primary driver of the falling share price. This update significantly de-risks the stock and will reduce the liquidity risk discount being factored into the valuation.

The $490 million cash balance stacks up well against the small $630 million market capitalization based on Friday’s closing price.

Another sign of bullish sentiment was sparked by the rating upgrade in late December from analysts at Jefferies investment bank. The institution upgraded the stock to a ‘buy’ call from ‘hold’ while increasing their target price from $7.70 to $11.

Analyst Akash Tewari is happy with the current valuation of ZYME as it is trading in a similar range to where it was when it completed the capital raise at the beginning of 2022. Tewari also thinks it's worth buying the stock before the release of GI ASCO data around the 19th or 20th of January.

Fintel’s consensus target price of $13.09 has risen from $12.55 in mid-December as analysts are becoming more positive on the medium-term outlook.

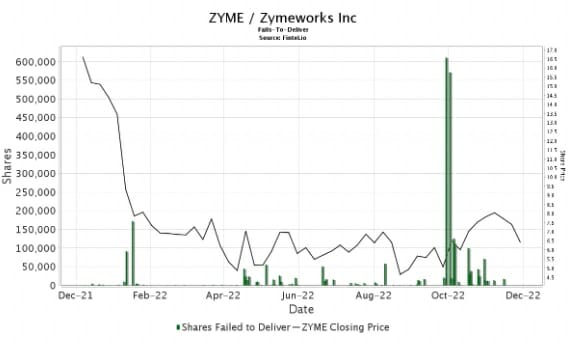

The sharp share price rise has pushed up the risk of a short squeeze in the stock. Fintel’s Short Squeeze Score of 89.10 ranks ZYME in the top 2% of companies that are likely to experience a short squeeze.

Zymeworks currently has 27.29% of its float currently shorted with 7.85 days to cover. The chart below shows the stock that failed to be delivered and the correlation with share price rallies over 2022.

Article by Ben Ward, Fintel