Hidden Value Stocks issue for the fourth quarter ended December 31, 2022, featuring an update from GrizzlyRock Capital pitching their thesis on Ardagh Metal Packaging (NASDAQ:AMBP).

GrizzlyRock On Ardagh Metal Packaging

Back in July 2017, GrizzlyRock Capital pitched Resource Capital and Vishay Precision Group as the firm’s two favorite undervalued small caps.

Q4 2022 hedge fund letters, conferences and more

Both have produced positive returns over the past five years, but Vishay Precision is the standout performer. The stock more than doubled between July 2017 and August 2018.

Over the past five years and 10 years, the stock has returned 8.6% and 11.7% annualized, respectively.

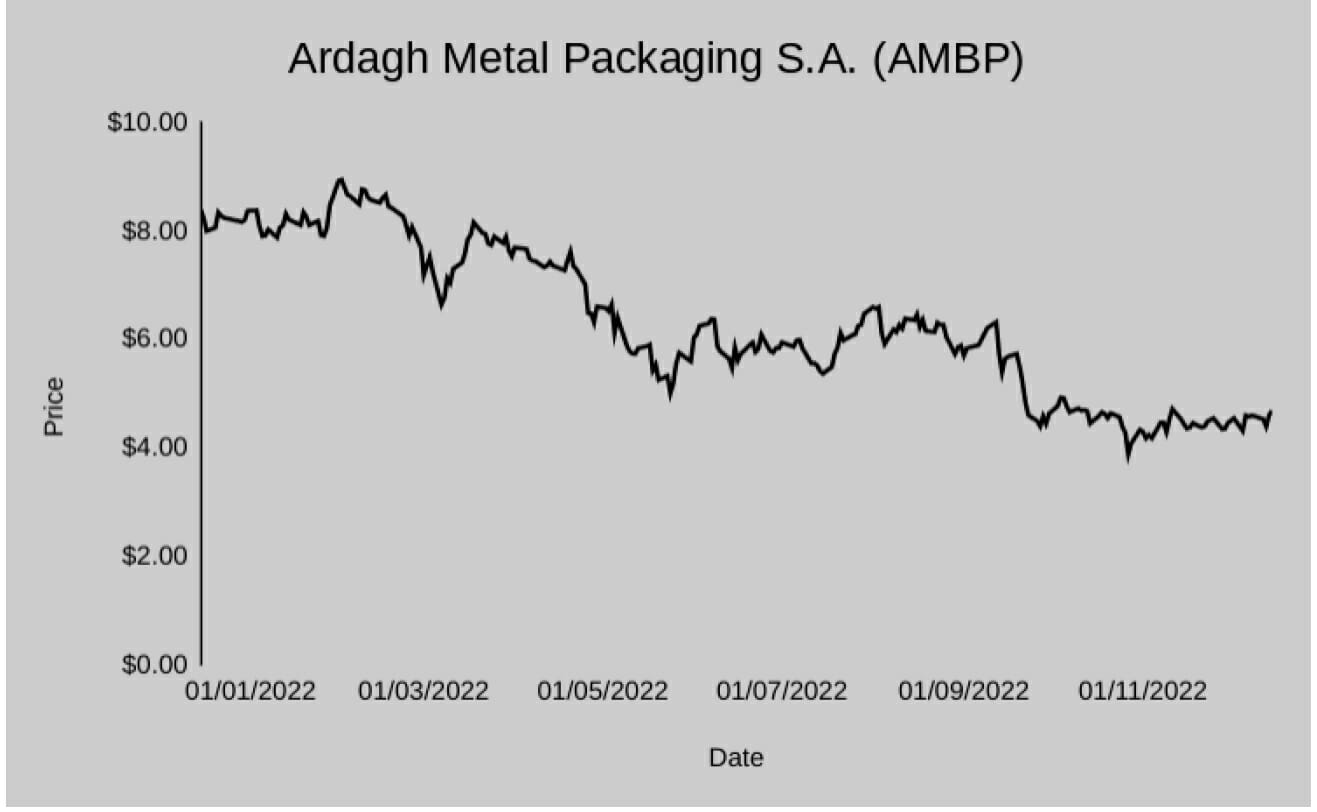

One of the fund's latest ideas is Ardagh Metal Packaging (NASDAQ:AMBP), a company that listed publicly via a SPAC and has since struggled to gain investor attention. GrizzlyRock believes the market isn't giving the business the attention it deserves:

Ardagh Metal Packaging is the #2 or #3 producer of metal beverage cans in North America, Europe, and Brazil.

The business was created when legacy glass manufacturer Ardagh Group (privately held) purchased a consortium of high-quality assets being forcibly divested during the 2016 Ball Corp and Rexam merger. Managed by reputable industry veteran Oliver Graham, Ardagh Metal listed publicly in 2021 via SPAC to provide growth capital for the current growth cycle.

Not only economically stable, demand for the simple beverage can is surging due to aluminum’s sustainable attributes. According to Wall Street Research, 75% of all aluminum ever produced remains in use.

Aluminum cans are infinitely recyclable which achieves many CPG firm’s circularity goals, have the highest recycling rate of any beverage packaging substrate, and include (by far) the highest amount of recycled content.

This supply-demand imbalance is so severe that bottlers are importing billions of cans into the US and Europe despite incurring the significant cost of “shipping air” (moving empty cans around the globe). In response to growing demand, the industry is adding a tremendous amount of capacity.

Ardagh is now onshoring supply to meet demand in each geography they serve. In return for this capacity, CPG customers are signing 4 to 5 year contracts (historically contract norm was 3 years) at terms which provide ~20% unlevered IRRs for the can producer. With industry standard financial leverage, return on equity capital is far higher.

The bear case is that during the current rush to expand capacity, the players are going to overbuild. This would crush historically exceptional unit economics as firms would be forced to lower price to fill unused capacity.

Despite the rapid growth, each beverage can producer has also delayed announced expansion and/or shuttered high-cost assets. Just this year, Ball Corporation announced North American facility closures and Ardagh has quietly pushed back a greenfield expansion plan in Phoenix, Arizona by about a year -evidence that the industry remains rational during this period of significant growth.

To assess via free cash flow, EBITDA of ~$954 million would generate ~$600 million of free cash flow after interest, taxes, and maintenance CapEx. Valuing these earnings at a 9% yield would imply shares are worth $11.2 (131% return).

Using an 8% yield shares would be worth $12.6 for a 159% return. These returns are prior to the $0.40 annual dividend which adds 8.3% per annum at the current price."