Selling cash-secured puts on stocks an investor is happy to take ownership of is a great way to generate some extra income.

Q3 2021 hedge fund letters, conferences and more

A cash-secured put involves writing an at-the-money or out-of-the-money put option and simultaneously setting aside enough cash to buy the stock.

The goal is to either have the put expire worthless and keep the premium, or to be assigned and acquire the stock below the current price.

It’s important that anyone selling puts understands that they may be assigned 100 shares at the strike price.

Why Trade Cash Secured Puts?

Selling cash secured puts is a bullish trade. However, it’s slightly less bullish than outright stock ownership.

If the investor was strongly bullish, they would prefer to look at strategies like a long call, a bull call spread, or a poor man’s covered call.

Investors would sell a put on a stock they think will stay flat, rise slightly, or at worst not drop too much.

Cash secured put sellers set aside enough capital to purchase the shares and are happy to take ownership of the stock if called upon to do so by the put buyer.

Naked put sellers, on the other hand, have no intention of taking ownership of the stock and are purely looking to generate premium from option selling strategies.

The more bullish the cash secure put investor is, the closer they should sell the put to the current stock price.

This will generate the most amount of premium and also increase the chances of the put being assigned.

Selling deep-out-of-the-money puts generates the smallest amount of premium and is less likely to see the put assigned.

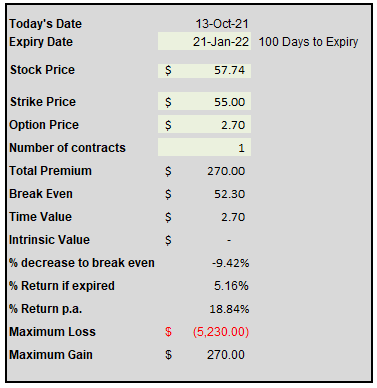

DOW Cash Secure Put Example

Yesterday, with Dow Inc (NYSE:DOW) trading around $57, the January 2022 put option with a strike price of 55 was trading around $2.70.

Traders selling this put would receive $270 in option premium.

In return for receiving this premium, they have an obligation to buy 100 shares of DOW for $55. By January next year, if DOW is trading for $50, or $40, or even $10, the put seller still has to buy 100 shares at $55.

But, If DOW is trading above $55, the put option expired worthless, and the trader keeps the $270 option premium.

The net capital at risk is equal to the strike price of 55, less the $2.70 in option premium. So, if assigned, the net cost basis will be 52.30. That’s not bad for a stock currently trading at $57.74.

That’s a 9.42% discount from the price it was trading yesterday.

If DOW stays above $55, the return on capital is:

$270 / $5,230 = 5.16% in 100 days, which works out to 18.84% annualized.

Either the put seller achieves an 18.84% annualized return, or gets to buy a high-yielding, blue-chip stock for a 9% discount.

You can use this handy calculator to run the numbers and make sure you are happy with the different scenarios.

Summary

While this type of strategy requires a lot of capital, it is a great way to generate an income from stocks you want to own.

If you end up being assigned, you can sit back and collect the fat 4.81% dividend on offer from DOW.

You can do this on other stocks as well, but remember to start small until you understand a bit more about how this all works.

If you have any questions, feel free to reach out to me by email or on Twitter.

*Disclosure: On the date of publication, Gavin McMaster did have (either directly or indirectly) positions in the securities mentioned in this article. All information and data in this article is solely for informational purposes. The information herein is based solely on my personal opinion and experience. All investments hold inherent risk, and the information provided should not be interpreted as any kind of guidance, recommendation, offer, advice, or suggestion. Any ideas and strategies discussed on this channel should not be implemented without first considering your financial and personal circumstances or without consulting a financial professional.

Article By Gavin McMaster, The Financially Independent Millennial