For weekend reading, Gary Alexander, senior writer at Navellier & Associates, offers the following commentary:

Jackson Hole, Wyoming, is a nice fishing spot, and former Fed Chairman Paul Volcker loved to fish.

The first Fed conference sponsored by the Kansas City district was held in 1978 and was titled, “World Agricultural Trade,” since Kansas City is situated in America’s breadbasket, with some prime farmland.

Q2 2022 hedge fund letters, conferences and more

It was a pretty dull affair until 1982, when the market was just beginning to rise after Fed Chair Paul Volcker wrestled hyper-inflation to the mat by raising rates up to 20% from 1979 to 1982, so to lure their 6’7” MVP to the meeting, the Kansas City Fed decided to hold their 1982 annual meeting near a fishing spot Volcker liked in Jackson Hole – in the remote Northwestern corner of the Kansas City Fed’s district.

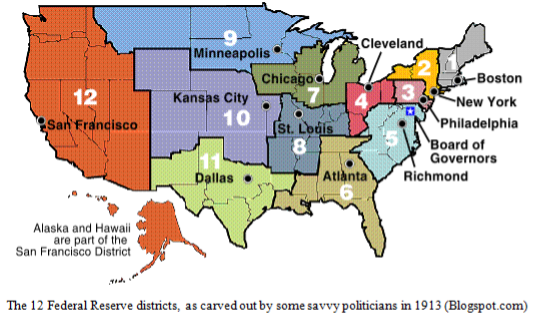

As it turns out, Missouri is headquarters for two of the Fed’s 12 districts, with my favorite District, St. Louis, holding down the eastern half of the state. They specialize in monetarist studies and historical charts with their FRED database. The Kansas City district is more of a bucolic, farm-oriented district.

How did Missouri capture two of the 12 Fed district capitals? Elementary, my dear Wilson. When the Fed was born in 1913, the first year of Democratic President Woodrow Wilson (serving 1913-1921), the Speaker of the House was Champ Clark, a Democrat from Missouri. The Federal Reserve System was opposed by James Reed, a powerful Democratic Missouri Senator from Kansas City who served on the Senate Banking Committee, so Wilson’s Secretary of Agriculture – David F. Houston, from St. Louis, and one of the three members of the Federal Reserve Bank Organization Committee – and Clark held out the plum of a Federal Reserve District for St. Louis AND Kansas City, making Reed and Houston happy.

For the last 40 years, Paul Volcker’s fishing haven has become an annual getaway for central bankers, with some of the most beautiful scenery (above), usually causing some reflection and thought about the future of central banking, rather than some 8-minute rant about fixing the problems bankers have caused.

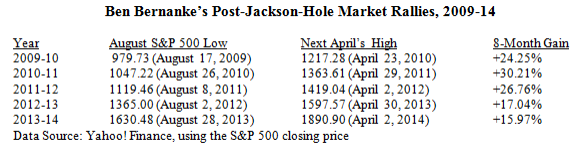

Be that as it may, this late August confab has become an annual rallying point for the stock market over the last 15 years, since the world fell apart in 2007-09, but this year was an exception. Usually, this pre-Labor Day meeting in the Rockies provided a boost the market needed, especially under Ben Bernanke:

Ben Bernanke Made History with His QE (“Helicopter Money”) Pronouncements in Wyoming

- The 2010 Jackson Hole conference was held August 26-28. In his August 27 talk, Mr. Bernanke said that the pace of economic growth had been “less vigorous” than the Fed was expecting, and the pace of the U.S. job growth was “painfully” slow. He also acknowledged that the Fed was surprised by the “sharp deterioration” in the U.S. trade balance. His solution was to revive the Fed’s late-2008 “quantitative easing” (QE) scheme. The market loved this QE2: The S&P rose from 1040 on the day of Bernanke’s Jackson Hole talk to 1363 the following April, up over 30%.

- The 2011 Jackson Hole conference was held August 25-27, during an especially volatile month in market history. Gold was soaring. Stocks were sagging. At Jackson Hole, Chairman Bernanke laid out the groundwork for another new Fed monetary strategy called “Operation Twist.” The details weren’t announced until September 21, but then various Fed governors hit the road to explain and defend their $400 billion operation to artificially flatten the yield curve. The stock market loved Operation Twist. The S&P 500 rose over 26% from August 2011 to April of 2012.

- The 2012 Jackson Hole conference, held August 30 to September 1, laid the groundwork for QE3, which was officially launched on September 13. Bernanke’s Jackson Hole remarks were more frank than usual. First, he said that the stagnant job market was of “grave concern” to the Fed. He also called current economic growth “far from satisfactory” and “tepid.” Because of this, Bernanke said that the Fed will “provide additional policy accommodation as needed.” This became QE3, which the market loved, as the S&P 500 rose over 17% from its August 2012 lows.

- The 2013 Jackson Hole conference was held August 22-24. By then, Chairman Bernanke was a lame duck, so he let his replacement (Janet Yellen) speak in his place. Strangely, she did not say much, except as part of a panel. Since the skies were smoky around Jackson Hole, due to all of the fires in Idaho, the inside joke was that Jackson Hole’s skies reflected the foggy future of the Fed, especially since Bernanke’s hints of “tapering” (uttered in May) were spooking the markets. In the end, tapering failed to faze the market, with the S&P 500 rising 16% in the next 7 months.

Bernanke’s time at the Fed expired in January 2014, but here’s his track record after the 2008-09 crash:

Janet Yellen (and Mario Draghi) Continued to Spread the Benjamins Around

Long after Benjamin Bernanke left the scene, the Benjamins kept pouring out of the Fed. Chairperson Janet Yellen took her turn at the helm, saying, “Our goal is to help Main Street, not Wall Street,” but she turned out helping both. By keeping rates super-low, she encouraged many businesses to borrow money at low rates, often to buy back more of their shares. Low rates also make home mortgages and vehicle loans more affordable, reviving the housing and auto markets. Low rates also put a damper on the debt service portion of the federal budget – even though low rates limit some fixed-income investors.

In all, Ben Bernanke and Janet Yellen kept the Federal Reserve’s key short-term interest rate – the Fed Funds Rate – near zero (officially, in a range of zero to 0.25%) for seven full years (seven of President Obama’s eight years in office), starting on December 16, 2008 and lasting until December 16, 2015, encompassing Bernanke’s final five Jackson Hole conferences, and Janet Yellen’s first two sessions there.

- More importantly, the 2014 Jackson Hole conference introduced Modern Monetary Theory (MMT) into the conversation when European Central Bank President Mario Draghi indicated that he was worried about inflation staying too low for too long. This laid the groundwork for Europe’s more virulent version of QE, including negative interest rates, starting in 2014.

Several rounds of Quantitative Easing (QE), seven years of ZIRP (Zero Interest Rate Policy), bolstered by Modern Monetary Theory (MMT), now popular in Washington DC, and “helicopter money” (Bernanke’s phrase) has been a bold experiment in avoiding a Greater Depression, and that sort of succeeded, but the central bankers waited too long to return to normal after 2008. Since the financial crisis of 2008, central bankers have bent over backward to be accommodating, fighting any remote chance of a 1930s rerun.

This fear of deflation has caused central bankers to fuel too much inflation for too long before belatedly fighting back, and that has put Jerome Powell in an obviously foul mood. Perhaps he is angry at himself and other central bankers – and justifiably so – but his Friday temper tantrum caused a Wall Street panic.

The stock market may not bottom this year until September or early October, if history is any guide, so we may have a rocky road ahead. This does NOT mean sell stocks. I may be wrong, and it’s better to weather any market panic, or switch sectors, than to sell all stocks.

The full weight of Quantitative Tightening (QT), or $95 billion per month taken out of circulation from the Fed’s balance sheet, could have the opposite effect of QE, i.e., radically lower inflation by year’s end, as I predicted at the start of 2022. This could put upward pressure on bond yields, which could test the resolve of international T-bond buyers. Is the U.S. still the global capital oasis? Yes, I think it still is.

So, as we celebrate the 40th anniversary of the first Jackson Hole meeting with a mini-replay of the first one – when Paul Volcker faced down runaway inflation with monster tightening – we should remember what happened next. August 1982 was also the birth of a monster bull market, rising 15-fold in 17 years.