I’ve long said that at this point in the cycle higher rates would be beneficial to the overall economy. Housing is being held back by the low rates and lending would expand if rates rose (note: this is not an instantaneous process). The MBA’s “mortgage availability” index seems to back that view. While many “fear the taper”, to the contrary I feel the Fed’s reduction in activity would further boost economic activity in one of the if not the largest US industry, housing. Far from being a negative, tapering would in my opinion give the economy the boost continued QE has failed to do.

What short term effects would it have on the stock market? Who knows? Maybe by the time they finally get around to doing it more folks will have come around to this line of thinking? Maybe there us a “taper tantrum” like we saw last time? One thing for sure is we cannot judge the efficacy of Fed policy by the immediate market reaction to it or a few months data post decision. People will be hyperventilating at every gyration post decision and that simply is wasted energy. I know that if we do sell off I’ll view it as a temporary issue and be looking to be a buyer.

Has housing made huge strides since the crash yes? But as strong as it has been is remains well below historical levels (even if we exclude bubble years data) and I maintain QE and its effect on lending rates is a significant culprit. For instance if we look at the homebuilder activity after the last housing downturn we see that single family starts recovered from the drop and returned to historic levels in just over two years. Granted the drop was far less severe than what we just witnessed but we are now 5 years since the trough in housing starts/sentiment and only in the past year have those indexes begun to turn positive on a sustained basis. Some may take that as an indication QE is working but I have another reason for the rebound. Demand….every year we still have ~1M household formations and they need a place to live. For the past 5 years building simply has not kept pace with that growth. This is why the dreaded “shadow inventory” proved to only be a ghost, not a reality as it was soaked up by the market as it became available. Even with the recent surge in building to the August number of 682k starts, that number still does not keep up with household demand and is just over half of what is needed (this is the reason since 2011 I have been very bullish on everything housing related).

But now the low hanging fruit is disappearing. The dirt cheap homes are a thing of the past for the vast majority of the US and since there has been zero to minimal building, supply is the largest issue (for the overall economy, not if you are a homebuilder). If you doubt that talk to a realtor. I have several I talk to regularly and all saw the same thing, “If I don’t have a solid offer in 7 days I’m shocked”. ”why” when I ask, “no supply” they all say. Because of that we have seen the dramatic price increases of the past few years. Builders, while they have significantly upped production are reluctant to really put the pedal to the floor because while demand is strong and supply limited, the demand is not broad based due to still very restrictive lending from banks. This is due to the artificially low rates QE has produced. Is that going to “kill” the housing recovery? No. Far too many people still want to own homes and there just are not enough of them now. What it IS going to do is dampen the overall effect of what additional buyers would be doing for the housing market and then the overall economy and GDP. If we look at what is being built now it is geared to higher income folks (not “rich”, say “upper middle” and up) because those are the folks who can get mortgages. There is a whole demographic not now being served. Opening credit to these folks would take a strong housing recovery (from a building and GDP effect perspective) and make it spectacular. This would not necessarily force home prices higher because building more starter homes has limited effect on the $50ok neighborhood’s pricing…totally different buyers. It would have a tremendous effect on economic activity though (more jobs, building supplies bought, transaction income etc etc).

More realistic lending from banks (spurred by higher interest rates) would take an economy growing 2%-3% and boost that to 3%-4% (or more).

On a side note, this housing meme IMO has years ahead of it. Delete the word housing and make it food or anything else people must have (they do need shelter) and then look at the supply that item being produced below the growth of the population that needs it for over a half decade now and what do you think the fundamentals of that item would be going forward? Me too….

“Davidson” submits:

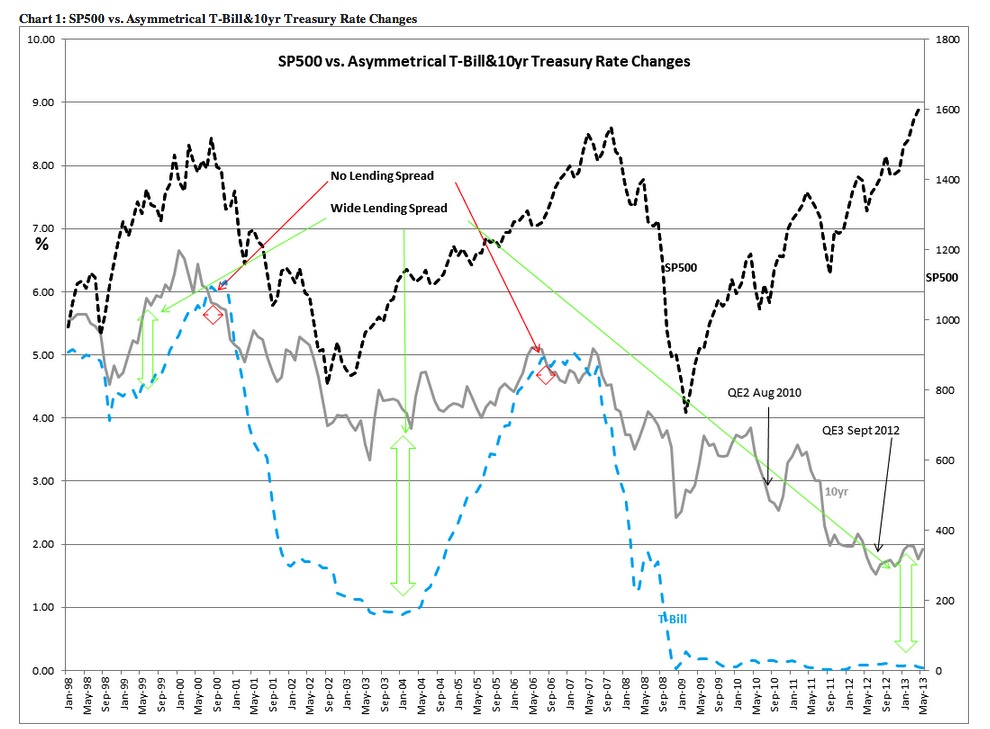

It is widely believed that the Federal Reserve is doing its best to stimulate the economy by its actions to lower longer term mortgage rates thru its QE2 & QE3 fixed income purchase programs. Chart 1: SP500 vs. Asymmetrical T-Bill&10yr Treasury Rate Changes shows that when QE2 &QE3 were announced the 10yr Treasury Rates fell from 3.85% in April 2010 to 1.53% in July 2012. On talk of a Fed “taper” 10yr Treas. rates rebounded May-July 2013 to the 2.75% range we see today. The Fed does have an impact on rates if it works hard enough!

That the Fed’s QE2 & QE3 actions have actually hurt mtg lending can be seen in a relatively new indicator by the Mortgage Bankers Association called Mortgage Credit Availability Index or MCAI as shown in Chart 2: MCAI. The link to this chart is: Mortgage Bankers MCAI. An explanation of the MCAI is found at: Mtg Bankers Assoc Presentation of MCAI. One can see that as 10yr Treasury rates fell sharply from 3.46% in April 2011 to 1.97% in Jan 2012, the MCAI fell from ~111 to ~97 in Jan 2012. Mortgage lending declined with a decline in 10yr Treasury rates. MCAI improved to the ~108 range in Jan 2013 and then improved to ~111 as 10yr Treasury rates rose May 2013-July 2013. Mortgage lending improved with the rise in 10yr Treasury rates!

Lower 10yr rates correlated to lower mtg lending! Higher 10yr rates correlated to higher mtg lending!(at this point in the credit cycle).

This looks and sounds more complicated than it is! Chart 1: SP500 vs. Asymmetrical T-Bill&10yr Treasury Rate Changes shows that long rates are rising faster than short rates which have remained flat the past several months. This widens credit spreads for lending institutions which borrow short and lend long. Wider credit spreads improve profits for lenders. This is reflected in the rise of the MCAI for June 2013-July 2013.

Wider credit spreads increase mortgage lending!

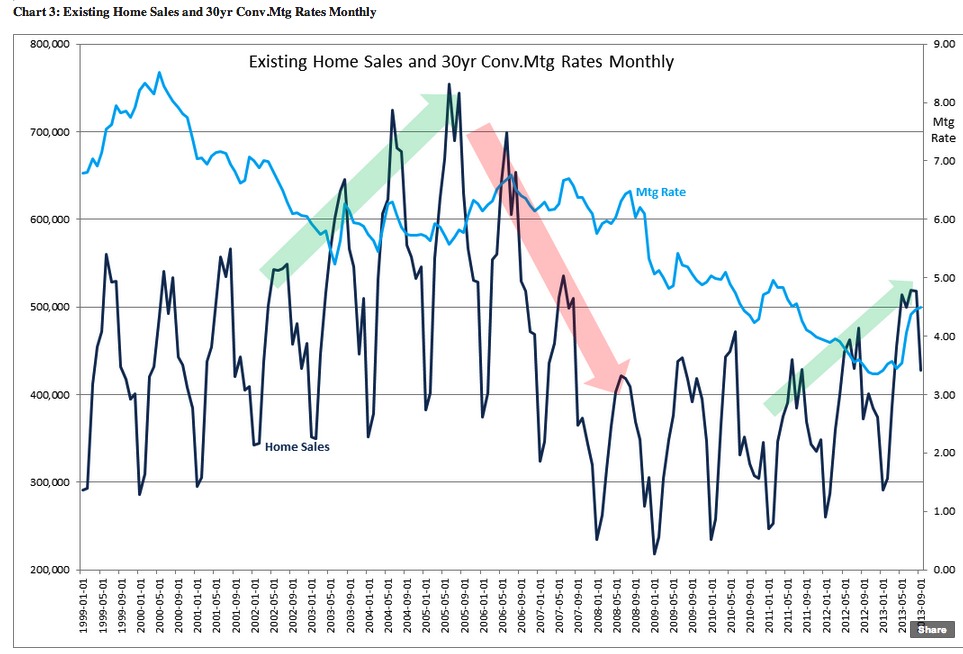

The Feds believe that lower long term rates would stimulate the economy. The opposite of what has actually occurred! Fortunately the writing is on the wall. Banks cannot make a better profit unless they move funds out of 10yr Treasuries at 2.7% and into mortgages which average ~4.4% for 30yr Conventional Mortgages-see Mortgagenewsdaily Rates. The evidence is in the MCAI and in various Single Family Home economic data that home sales are improving. Some of this can be difficult to see with home sales being highly seasonal, i.e. highest in the spring and lowest in December. Chart 3: Existing Home Sales and 30yr Conv.Mtg Rates Monthly provides a longer term picture of the seasonal patterns of home sales and mtg rates. This not perfectly correlated as mortgage rates are impacted by more than the simple supply/demand of home buyers, but the correlation can be seen just the same. We are in a period of housing market expansion and it is clear that since 2008 we have witnessed generally higher lows and higher highs. The economic data indicate that home sales should be higher this coming spring.

My fundamental point of view is that the desire of ~310million individuals to expand their and their family’s standard of living is a very powerful economic driver. One can read daily about individual triumphs to find/develop solutions to issues blocking pathways to better lives. Only if one is reading about these triumphs at the individual level can one get an understanding as to why we have rebounded from every financial collapse in our history. The solutions occur individually! We each have our own issues and develop our own solutions! Many of us would have it no other way!

It is our ‘Free Market’ which provides the base which permits each of us to create and then benefit individually from solutions to life’s problems. Some of us invent solutions that can be sold to others. Free Markets mean that inventors have the sole rights to the financial value of their inventions. One can read about this occurring at the individual level throughout our economic history. Through extensive reading of individual economic contributions, one comes to the realization as to how powerful are the economic forces which reside on the individual level. Those who only focus on macroeconomics do not see the dynamic strengths inherent in individual inventiveness. The Macro-Economists do not realize that millions of individuals left to find millions of unique individual solutions will actually find them! We have found solutions to issues at the individual level for centuries. Those who operate small businesses get this and it is one of the reasons we hear that small business owners often prefer that government to stay out of stimulating various parts of the economy. They want the economy to find its own way. Fortunately, even if government does something which impedes economic development through misguided and often politically inspired activity, the economy has always righted itself and moved forward.

Summary:

A new indicator from the Mortgage Bankers Association, the Mortgage Credit Availability Index(MCAI) shows that Fed stimulation through lower mortgage rates has impeded rather than fostered economic expansion. Nonetheless, we should expect mtg rates to rise at this point in our economic cycle and that this should stimulate additional mtg lending and further expand our economy. Every economic cycle has its nuances and the current cycle has seen Fed intervention well beyond what the Fed has historically considered doing. But, our economy continues to expand, if not exactly as it has in the past, it is within patterns which are historically familiar.

All signs continue to point to a traditional economic recovery and higher equity prices in spite of missteps by government at economic stimulation. Optimism continues to be warranted in my opinion with LgCap Domestic and International equities being the most favored (SPDR S&P 500 ETF Trust (NYSEARCA:SPY)). SmCap Domestic and International equities should continue to generally rise with other equity classes. The only asset classes which I have exited thus far in the current economic/investment cycle have been Fixed Income, REITs and EmgMkts

Via: valueplays

{kind=link}