Startup ecosystem rankings and insights from the world’s most comprehensive, quality-controlled dataset

SAN FRANCISCO, Calif. — June 15, 2023 — The Global Startup Ecosystem Report 2023 (GSER 2023) by Startup Genome and the Global Entrepreneurship Network (GEN) was launched today at The Next Web Conference in Amsterdam, presented by JF Gauthier, Founder and CEO of Startup Genome. The GSER is powered by the world’s most comprehensive and quality-controlled dataset on startup ecosystems.

Informed by data on 3.5 million startups across 290+ global ecosystems, the report provides compelling new insights and deep knowledge about startup trends including the impact of inflation, AI regulation, talent attraction, trends in global VC funding, and sub-sector analyses.

Contributions from expert thought leaders and local key players further enrich the report’s extensive, evidence-based findings, which are the product of over a decade of Startup Genome’s independent research and policy work.

Key Findings From The Global Startup Ecosystem Report

Global key findings from the #GSER2023 include:

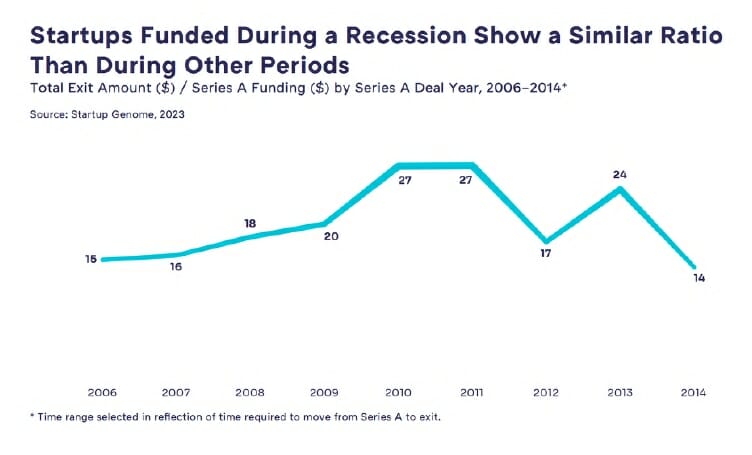

A recession is a good time to invest in startups — high interest rates can benefit startups, concentrating capital and talent into ventures that create value. Startups funded during the Great Recession had slightly higher exit multiples over total money invested than those funded during economic expansions.

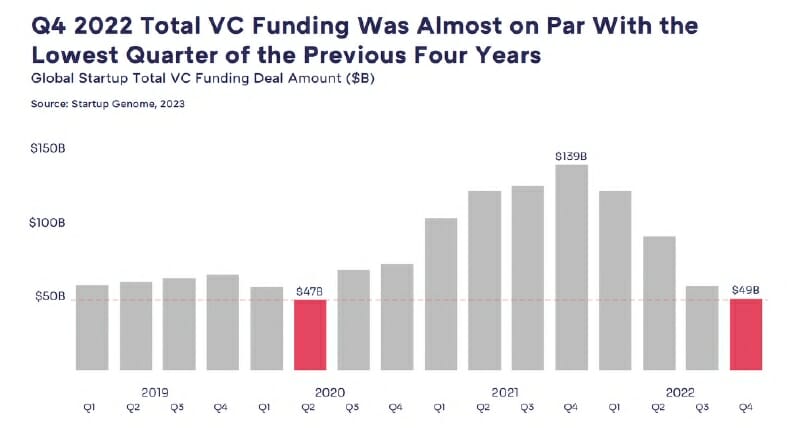

VC funding globally began its downward trend in the first quarter of 2022, dropping 13% in amount raised from Q4 2021. Overall, 2022 declined by 35% from 2021.

Although fewer startups were funded in 2022 globally, they received larger sums. There was an 18% decline in the number of deals, but a 17% decline in deal amount, meaning that the average deal size grew 2%.

The biggest tech exit of the year was Miami-based MSP Recovery’s $32.6 billion IPO, which pales in comparison to 2021’s biggest exit, which was nearly five times larger (Beijing-based Kuaishou’s $150 billion IPO).

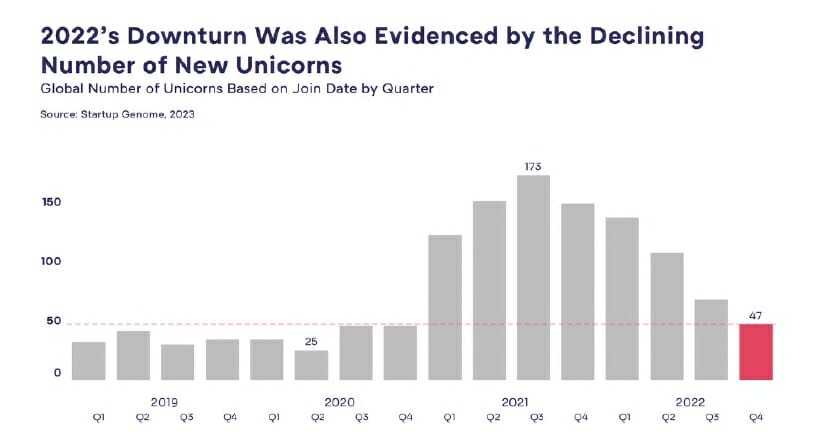

2022 showed a slowdown in the number of unicorns, a global decline of 40% from 2021’s 595 to 359. However, seven ecosystems produced their first tech unicorn in 2022.

Reflecting AI’s increasing use and intersection with other sub-sectors, AI & Big Data is the sub-sector with the highest count of total VC deals, making up 28% of the global share in 2022. It also has the highest growth in number of exits, at 74%, from 2017–2018 to 2021–2022.

As Deep Tech innovations become more integrated into the startup world, Deep Tech’s exit amount has grown faster than non-Deep Tech technologies from 2017–2018 to 2021–2022, at 326% vs. 225%.

Overall VC funding in Asia dropped by 31% from 2021, from $102 billion to $70 billion. However, Asia was the least impacted global region in terms of early-stage funding amount, dropping just a single percentage point from 2021 to 2022.

In 2022, the amount of early-stage funding in Europe was down 15% from 2021, but the average early-stage deal amount was up by 7% due to a significant reduction in the number of early-stage deals, just 75% of 2021’s number.

Latin America declined 72% in Series B+ funding amount from 2021 to 2022. The Series B+ deal count declined 54%. Over 2018–2022, Latin America experienced a 65% increase in Series B+ deal count and a 143% increase in Series B+ amount.

In 2022, MENA experienced a decline of 19% in Series B+ deal amount and 14% in total VC funding. Over 2018–2022, MENA saw a 96% rise in early-stage funding amount, a 28% growth in Series B+ deal count, and a 113% increase in Series B+ deal amount.

In 2022 Oceania experienced a 31% year-on-year decline in Series B+ deal amount, a 10% decline in the number of Series B+ deals, and a 13.6% decline in early-stage funding amount. However, Oceania experienced a 60.7% increase in early-stage funding amount over 2018–2022, the highest of any global region for this period.

In sub-Saharan Africa, early-stage funding declined 5.9% and early-stage funding amount by 6.7% from 2021 to 2022. Looking at 2018–2022, the region was up 227% in early-stage funding amount and up 43.8% in early-stage deal count.

North America’s early-stage funding dropped 26% and Series A deal count 25% from 2021 to 2022. Regardless, North America is still the world’s leading startup nation, making up 50% of the top 30 plus runners-up ranking.

The top three ecosystems have maintained their ranking positions from 2020, with Silicon Valley at the top, followed by New York City and London tied at #2. Silicon Valley continues to dominate despite having a reduced market share, with Series A deal amount contracting by 75% and Series B+ by 73% from 2021 to 2022.

A decline of China’s dominance and continued growth of India — eight Chinese ecosystems have fallen in the rankings from last year, including the leading hubs of Beijing, Shanghai, and Shenzhen, while seven Indian ecosystems moved up, including Delhi and Bengaluru-Karnataka in the top 30 and Mumbai tied at #31.

Boston and Beijing have both slipped out of the top five to #6 and #7 respectively, losing two positions each. This has paved the way for Los Angeles to rise to #4 and Tel Aviv to #5, both gaining two spots.

Singapore has entered the top 10 for the first time, moving up an impressive 10 places to #8 from #18 in the GSER 2022, the biggest improvement in the rankings.

Melbourne has moved up an impressive six places from last year, to reach #33. The Australian ecosystem grew 43% in Ecosystem Value from the GSER 2022.

The top 100 Emerging Ecosystems are collectively worth over $1.5 trillion in Ecosystem Value, a 50% increase from the GSER 2022.

Istanbul takes the #1 spot in the new Strong Starters ranking, which identifies the top 25 Emerging Ecosystems where early-stage funding activity is most robust.

“We continue to serve as expert advisors for accelerating entrepreneurial performance and growth in ecosystems worldwide, and the GSER, as the most comprehensive and data-driven analysis of the subject published each year, remains a significant cornerstone of our mission,” shares JF Gauthier, Founder & CEO of Startup Genome.

“Despite current economic challenges, we are confident that, equipped with the right knowledge, entrepreneurs, policymakers, and community leaders everywhere can leverage opportunities to come together and show how innovative technologies can not only continue to drive growth and job creation, but simultaneously help save the planet and ensure a better future for everyone. This essential mission cannot be put on hold while we wait out rocky economic times.”

The GSER 2023 ranks the top 30 global ecosystems and10 runners-up, as well as ranking the top 100 emerging ecosystems. It also highlights startup communities from a regional perspective, separately ranking ecosystems in Asia, Europe, Latin America, MENA, North America, Oceania, and sub-Saharan Africa.

“Given that over half the companies on the 2009 Fortune 500 list launched during a recession or bear market, we know that lean economic times can produce high-performing startups,” said Jonathan Ortmans, Founder and President of the Global Entrepreneurship Network.

“Despite recent downturns in investment, this report foreshadows where we might see the world’s most disruptive and solution-driven companies emerge in the years to come — and provides unparalleled insights that policymakers and community leaders need to build resilient startup ecosystems.”

The GSER 2023 is created in partnership with the Global Entrepreneurship Network, Dealroom, and Crunchbase. The GSER 2023 provides invaluable insights and guidance on how to promote thriving startup communities — the #1 engine of job creation and economic growth. Discover how 140 entrepreneurial ecosystems compare and view the full report here: https://startupgenome.com/report/gser2023.

About Startup Genome

Startup Genome’s data-driven insights provide innovation policy leaders with clarity, momentum, and strategy to help them define and execute growth-focused actions. Working side-by-side with 300 partner organizations across six continents in 50+ countries to date, Startup Genome’s frameworks and methodologies are instrumental in building foundations for startup ecosystems to grow.

Many of the world’s leading governments and innovation-focused organizations have joined our knowledge network to cut through the complexities of startup ecosystem development. Startup Genome identifies key gaps in these ecosystems and prioritizes actions to fuel sustained economic growth. Find out more by contacting Adam Bregu at [email protected] or visiting startupgenome.com and LinkedIn.

About The Global Entrepreneurship Network

The Global Entrepreneurship Network (GEN) operates programs in 200 countries aimed at making it easier for anyone, anywhere to start and scale a business. By fostering deeper cross-border collaboration and initiatives between entrepreneurs, investors, researchers, policymakers and entrepreneurial support organizations, GEN fuels healthier start and scale ecosystems that create more jobs, provide education, accelerate innovation, and strengthen economic growth. Learn more about GEN at genglobal.org and by following us on Twitter, Facebook, Instagram and LinkedIn.