FORECASTS & TRENDS E-LETTER

by Gary D. Halbert

February 14, 2023

IN THIS ISSUE:

- Inflation Soared To A 40-Year High In 2022, Up Over 9%

- Why Precious Metals Failed To Perform As Inflation Hedges

- SPECIAL REPORT – Is It Time To Move On From Precious Metals?

- U.S. Credit Card Debt Jumps 18.5% To Record $930.6 Billion

- Major Banks Make Huge Profits Off Rising Credit Card Debt

Q4 2022 hedge fund letters, conferences and more

Inflation Soared To A 40-Year High In 2022, Up Over 9%

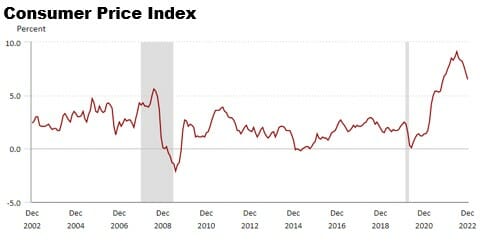

Inflation as measured by the Consumer Price Index (CPI) soared to a 40-year high last year to the surprise of almost everyone. Prices on just about everything we consume – from food to energy to housing and just about everything we buy – soared last year.

The CPI, which had remained fairly tame over the last couple of decades, exploded to 9.1% last year, the highest level since the 1970s. While the CPI has come down some in recent months, it remains at the highest level in decades.

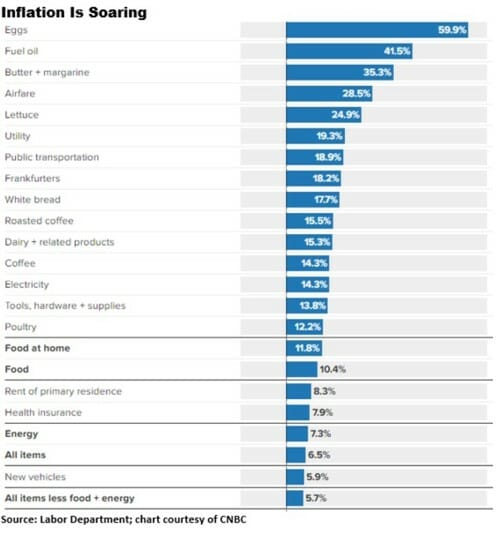

Here’s a look at how much prices have gone up the last couple of years for many things we consume. As a result, consumers are feeling a pinch in their pocketbooks, because wages have not increased as much as inflation, and most families are having to make adjustments to what they buy.

Most consumers never saw this coming. Ditto for most investors. Even if most investors had seen it coming, the traditional inflation hedges they usually look to in times of rising prices didn’t help out much. Take precious metals for example.

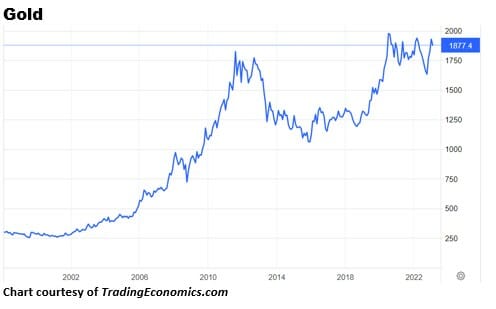

Gold prices actually went down modestly in 2021 and 2022 at a time you would have expected it to be shooting through the roof, what with inflation soaring to a 40-year high. Even gold bugs are scratching their heads and wondering why the yellow metal didn’t perform as traditionally expected.

Silver prices didn’t fare well either and most would argue performed even worse than gold over the last two years as inflation soared. Silver has been a dreadful investment over the last decade, losing over 50% of its value since 2011. Gold at least went up modestly over the last decade, while silver has been a dog.

Why Precious Metals Failed To Perform As Inflation Hedges

There are numerous theories as to why precious metals didn’t perform much better over the last couple of years as inflation soared to a 40-year high. Gold has long been regarded as one of the most effective investments for protecting one’s wealth from various possible adverse financial effects.

A plummeting stock market or an increase in inflation are two examples of these hazards. We had both in 2022. Most investors would have expected gold to rally significantly in this environment. Yet gold decreased about 10% last year.

Gold has been seen as a hedge against inflation throughout time. As a result, it is the asset of choice for many investors who want to ensure that their money will continue to have the same buying power in the future while minimizing the amount of risk they are exposed to.

Gold has also long been considered a hedge against political, economic and military crises around the world. In fact, gold did hit a new all-time high near $2,000 per ounce in the spring of last year when Russia invaded Ukraine. But as you can see in the chart above, gold fell significantly in the months which followed, although it did rebound somewhat late last year.

Another theory why gold didn’t perform better the last couple of years is the fact that more and more Baby Boomers are retiring and restructuring their portfolios to be less aggressive. Think about it: Most of us Baby Boomers were taught all our adult lives that precious metals were a good hedge against inflation. So, we bought and held gold and silver for years.

The next generation: Not so much. Generation X, the next generation after the Baby Boomers, did not have precious metals as inflation hedges pounded into their heads because, simply put, inflation was not a major concern for the last two decades – until the last couple of years, as shown above.

With inflation not a major concern, and with gold and silver not performing well, many younger investors felt no need to invest in precious metals which not only pay no dividends, but have to be stored at a cost if one wants to hold them physically.

The bottom line is the popularity of precious metals is just not what it used to be.

These reasons and others may explain why gold and silver prices have not performed better recently than they have in past decades. Still, I would have expected some kind of a bounce over the last two years.

SPECIAL REPORT – Is It Time To Move On From Precious Metals?

In the next few weeks, I’ll be sending you a new SPECIAL REPORT entitled Is It Time To Move On From Precious Metals? As I have discussed in today’s letter, there are reasons why precious metals have lost their luster in the last couple of years.

I’m not saying precious metals have lost their luster for good, but they could be out of favor for some time to come, especially with many younger investors paying them little attention. Maybe it’s time to consider an alternative for at least part of your precious metals allocation.

I believe I have an alternative for a portion of your portfolio, one which you can consider as a replacement for precious metals or simply an addition, which I will discuss in detail in my upcoming SPECIAL REPORT. So, be looking for my latest SPECIAL REPORT in the next few weeks.

U.S. Credit Card Debt Jumps 18.5% To Record $930.6 Billion

Americans’ total credit card debt reached a record $930.6 billion in the fourth quarter, up 18.5% from a year earlier, according to research and consulting firm TransUnion.

Inflation is driving people to put everyday expenses on their credit cards or to turn to subprime and personal loans, says Michele Raneri, vice president of TransUnion which tracks these trends.

“Whether it’s shopping for a new car or buying eggs in the grocery store, consumers continue to be impacted in ways big and small by both high inflation and the interest rate hikes by the Federal Reserve,” Raneri says.

Until inflation subsides to more historic norms, “We fully expect consumers to continue to look to credit products such as credit cards, HELOCs (home equity lines of credit) and unsecured personal loans to help make ends meet.”

Americans carry an average balance of $5,805 on their credit cards, most of which charge interest of nearly 20%.

Generation Z, those born between 1981 and 1996, has been hitting the plastic the most, with the number of credit cards they hold rising 19% in the past year and their balances ballooning 64%, according to TransUnion.

Overall, 2.26% of credit card holders were delinquent on payments in the fourth quarter of 2022, up from 1.48% a year earlier.

TransUnion cautions: “The increases in delinquencies is something to watch. If unemployment goes up, and we see a spike in delinquencies, then that indicates a longer-term problem.”

Americans opened up 202 million new credit accounts in the fourth quarter of 2022, bringing the total number of credit cards held by the 332 million people living in the United States to 518.4 million.

Bankrate estimates that, at a 20% interest rate, a person paying just the minimum on a $5,805 credit card balance and not making any additional purchases would pay an additional $8,213 in interest over 17 years before bringing their balance down to zero.

Major Banks Make Huge Profits Off Rising Credit Card Debt

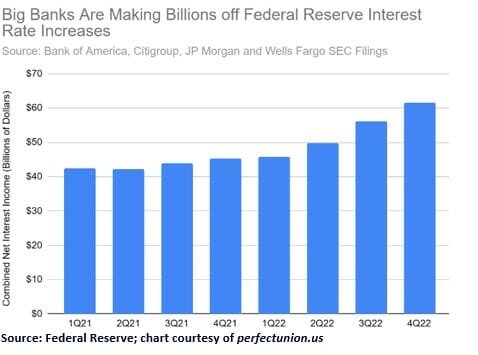

While it should come as no surprise to anyone reading this, major Wall Street banks are making billions from the Federal Reserve’s efforts to fight inflation, while American consumers are loading up on debt and falling behind to pay for necessities.

Bank of America, Citigroup, JP Morgan and Wells Fargo reported stellar earnings last quarter due in large part to the Federal Reserve’s interest rate hikes and ballooning credit card debt.

Combined, the Wall Street titans’ net interest income – a financial metric that measures the difference between what they paid on deposits and what they earned through loan interest – topped $61 billion for the quarter.

This means banks are extracting huge amounts from credit card interest while paying the bare minimum to those with savings accounts. Last quarter’s results amount to a 36% increase from the previous year.

Banks typically tie their credit cards’ interest rate to actions by the Federal Reserve. The Fed’s rate hikes over the last year have pushed the average credit card interest rate to over 23%, a 30% increase compared to pre-pandemic levels. This helped many of America’s largest banks blow past their own internal profitability goals last year.

In a competitive market, consumers should be seeing some benefit from the Fed’s actions in the form of higher returns on deposits in checking and savings accounts.

But so far consolidation in the banking industry has kept any benefits in check. Just six financial conglomerates control half of the US banking system. No wonder we’re not seeing the benefits we should be! I’ll have more to say about this in the near future.

Very best regards,

Gary D. Halbert

SPECIAL ARTICLES

Consumer Price Index Rose To 6.4% Annualized, Still Too High

U.S. Credit Card Debt Soars To Record $930.6 Billion In 2022

Gary’s Between the Lines column: Implications From Last Week’s Blockbuster Jobs Report