In a note this week, UBS echoed its earlier assessment that gold has indeed “entered a new bull run,” as I shared with you last month. The precious metal had a spectacular first half of the year, with total global demand reaching 2,335 tonnes, the second-highest on record, according to the World Gold Council (WGC).

Despite this, gold is still under-owned, accounting for only 3 percent of total ETF assets under management, UBS writes. The group adds there is room for new or returning market participants who might have cleared out their gold positions during the recent bear market.

Driving the bull run, according to the group, are “a prolonged period of depressed real yields” and “elevated macro uncertainty.” These are themes I’ve returned to many times in the past six months, with global government bond yields continuing to drop below zero and economic and geopolitical unrest advancing following the Brexit referendumand ahead of the U.S. presidential election this November.

Confidence in monetary policy and appetite for government debt continues to erode. According to Zero Hedge, foreign central banks dumped a record $335 billion in U.S. Treasuries during the last year. The top seller in June was China, which cleared $28 billion in Treasuries off its balance sheet. Over the same period, the world’s second-largest economy added to its official gold reserves—500,000 ounces in June alone—in an effort to diversify its holdings.

Investors should take heed of the fact that even central banks have become net buyers of gold. It’s always been my recommendation to maintain a 10 percent weighting in your portfolio—5 percent in gold bullion, another 5 percent in gold stocks.

A Superior Way to Gain Exposure to Gold

One of the best ways to play gold, I believe, is royalty and streaming companies. As a reminder, these companies serve as specialized financiers to explorers and producers. In return for upfront financing, they can receive one of two different types of payments. In one way, they can receive a royalty, or percentage, on whatever future sales the debtor company makes during the life of the mine.

In another way, they can buy a stream of precious metals at a low, fixed price. Discounts on gold, for instance, could be as much as 75 percent. This has typically been the preferred method for paying back the royalty company.

Some of our favorite names in this space include Franco-Nevada Mining, Silver Wheaton, Royal Gold and Sandstorm Gold, all of which have outperformed underlying gold for the 12-month period. Click the hyperlinks to read my special reports on Franco-Nevada and Silver Wheaton.

Better Allocators of Capital

Royalty and streaming companies show great opportunity on the upside but avoid many of the risks and operating expenses that explorers and producers must deal with.

Interestingly, they all employ a small group of technically skilled mining geologists, engineers, metallurgists and financial mining executives to analyze and monitor their investments.

Because they’re not responsible for buying mining machinery and building, operating and maintaining mines, they have a much lower total cash cost per ounce of gold than miners do. (In this context, cash cost refers to operational expenses that are paid using cash, rather than credit.) Their overhead is kept at a minimum, and they have some of the highest sales per employee in the world. As you can see below, their debt per share is much lower than senior miners Newmont Mining and Barrick Gold—the Army to royalty companies’ more agile and tactical Navy SEALs. Last year, Barrick cut $3.1 billion in debt last year and is on track to pay down an additional $2 billion this year.

Their margins have typically been much larger than traditional explorers and producers, allowing them to remain profitable even during gold bear markets.

Take Sandstorm, one of the younger royalty companies. Its second-quarter cash cost per ounce of gold was a mere $261, giving it operating margins of $994 per ounce.

Compare this to Barrick, the world’s largest gold producer. Barrick reported cash costs of $578 per ounce, nearly double that of Sandstorm—and Barrick has some of the lowest costs compared to other miners, according to Motley Fool.

| Mining Companies | Royalty Companies | |

|---|---|---|

| Precious metals price upside | X | X |

| Exploration upside | X | X |

| Production rate upside | X | X |

| No sustaining costs | X | |

| No exploration costs | X | |

| No capital expense overruns | X | |

| Fixed cash costs | X |

Investors like royalty companies because they’re a skilled team of former miners and mining executives who generate substantially greater gross margins and have materially fewer employees, with less general and administrative expense.

Further, they offer spectacular optionality. They often buy an asset with a payload over 10 years. However, these deposits often extend for 30 years, so they have potential for a much bigger payback. If the mining company expands production, it’s free additional cash flow, and if they make a large discovery near the producing mine, the royalties have free upside growth.

For further reading, one of the strongest overviews of royalty companies is Streetwise Reports’ “Precious Metal Royalties: The New Landscape.”

A New Entrant

Just as there still might be ample scope for gold investors to participate in the market, one CEO is betting there’s still room for another entrant into the precious metals royalty company space. Long-time precious metals commentator David Morgan recently helped found Lemuria Royalties, which reported in June that it had acquired its first silver royalty from a Peruvian mine operated by a subsidiary of Fortuna Silver Mines.

In January of this year, Morgan summed up his reasoning for establishing a new royalty company: “We favor the streaming and royalty companies a great deal because the risk is very low relative to, let’s say, an exploration company or even a producing company.”

This is precisely why we continue to find the royalty business model very attractive.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.13 percent. The S&P 500 Stock Index fell 0.01 percent, while the Nasdaq Composite climbed 0.10 percent. The Russell 2000 small capitalization index gained 0.57 percent this week.

- The Hang Seng Composite gained 0.87 percent this week; while Taiwan was down 1.27 percent and the KOSPI rose 0.28 percent.

- The 10-year Treasury bond yield rose 6 basis points to 1.58 percent.

Domestic Equity Market

Strengths

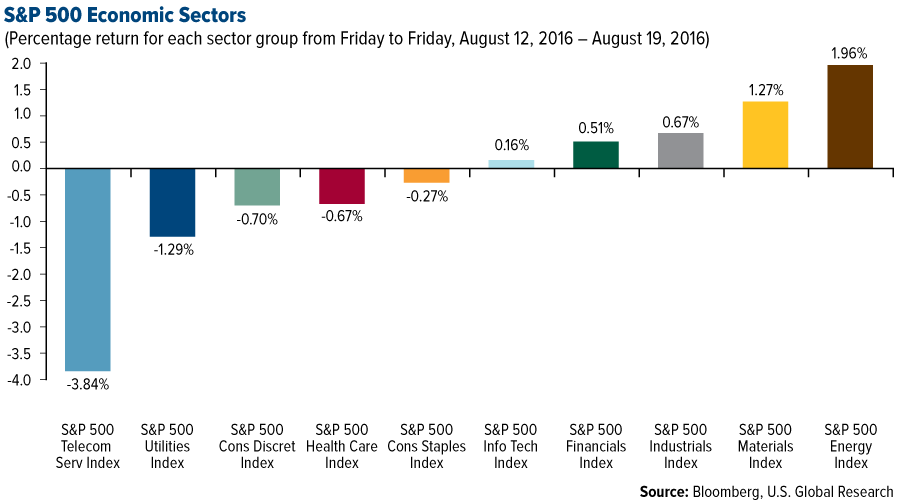

- Energy was the best performing sector for the week, increasing by 1.96 percent versus an overall decrease of -0.02 percent for the S&P 500.

- Urban Outfitters was the best performing stock for the week, increasing 23.36 percent. The company’s shares surged after its sales and earnings outpaced Wall Street estimates, helped by new fashions that resonated well with consumers.

- Netapp surged 22 percent during the week as the data management and storage company swung to a profit in the fiscal first quarter.

Weaknesses

- Telecommunications was the worst performing sector for the week, falling by -3.84 percent versus an overall decrease of -0.02 percent for the S&P 500.

- Verisign was the worst performing stock for the week, falling -9.85 percent.

- Prison stocks crashed this week. The Department of Justice is phasing out contracting to privately run prisons, according to a memo. After this news crossed, shares of Corrections Corporation of America, the largest publicly traded prison provider, fell in half, while Geo Group fell by more than 40 percent. Trading in both shares was halted for volatility. Private prisons are less secure than those run by the Federal Bureau of Prisons, the DOJ said.

Opportunities

- Walmart, the world’s number-one, brick-and-mortar retailer reported second-quarter adjusted earnings per share of $1.07 ($1.02 estimated), revenue of $120.9 billion ($120.3 billion estimated), and raised its outlook for full-year EPS. Sales at stores open for at least one year were positive for a seventh straight quarter.

- Home Depot reported second-quarter earnings that met and raised its full-year outlook amid a strong U.S. housing market.

- Urban Outfitters beat on the top and bottom lines. The retailer earned an adjusted $0.66 a share on revenue of $890.6 million, easily beating the $0.55 and $885.6 million that analysts were expecting. Comparable-store sales unexpectedly rose 1 percent, outpacing the 1.2 percent decline that was expected. “These results were driven by a positive retail segment ‘comp’ and substantial improvement in merchandise margins,” CEO Richard Hayne said in the earnings statement.

Threats

- Target struggled to sell electronics in the second quarter, especially Apple products. The retailer reported earnings that were stronger than expected, but it lowered its outlook for the rest of the year as it plans for a “challenging environment,” according to CEO Brian Cornell.

- T. Rowe Price is suing Valeant Pharmaceuticals, alleging fraud. The mutual fund, which invests in the company, alleges that Valeant is running a “fraudulent scheme” through its now shuttered pharmacy, Philidor.

- Volkswagen could face civil and criminal penalties because of its emissions scandal. The German automaker has been found liable for criminal wrongdoing by the U.S. Department of Justice, CNBC reports. Volkswagen may be forced to pay damages that exceed Toyota’s $1.2 billion settlement, the largest on record, for intentionally concealing acceleration problems.