My site is read by readers from all walks of life. We have those with no experience investing, to those who have been through the ups and downs of the past half a century (and even longer). We also have a variety of readers, who are interested in the concept of dividend growth investing, but who do not have the time to go through the painful process of screening, monitoring, and assembling portfolios of individual companies.

One of the most frequently asked questions I receive comes from busy investors, who are short on time right now, but want to be able to generate rising dividend income for life. Most of those investors are looking for the best dividend ETF out there. In general I have not been a big fan of dividend ETFs, but I have somewhat reluctantly relaxed my attitude about it. After all, not everyone wants to be like me ( go figure).

What should a busy investor do with their money? How should they invest their hard earned money for their life goals (retirement, kids education etc)?

After thinking out loud for a few years, I have come out with one or two funds for busy dividend investors.

The catch: they are not marketed as dividend growth funds.

When evaluating the dividend ETF I am going to share with you today, I looked for the following traits:

1) A history of dividend increases

2) Low costs

3) Low portfolio turnover

4) A long history of real world performance

The fund I came up with is based on the Standard & Poor’s 500 index. I am going to focus on this index, because S&P 500 funds are available in the 401 (k) plans of most employers.

This S&P 500 index is based on the market capitalization of 500 large US based companies. It was started in 1957, so it has had a track record of 60 years’ worth of history. This includes a long dividend record as well. The index has also been reconstructed and backtested to include information from 1871 to 1957.

This index covers 75% – 80% of the market capitalization for the Total US Stock Market. It is used as a proxy for how the stock market does. I see this index as one large dividend growth stock with 500 subsidiaries. The subsidiaries change over time, similar to the way large dividend kings such as Johnson & Johnson (JNJ) or Procter & Gamble (PG) regularly buy new companies, start new subsidiaries and exit certain businesses.

The index is diversified, as it has exposure to 11 different sectors. Those sectors include:

I wanted to add a few words for clarification as well. While I have exclusively discussed the S&P 500 index, I wanted to mention that a slightly better and more inclusive ETF would be the Total Stock Market index. The latter covers almost all publicly traded US stocks, and includes large caps, mid-caps and small caps. The long-term results have been very similar over the past 25 years, but I do not have as much data for the Total Market Index as I do for S&P 500. In addition, the Total Market Index is more inclusive, has low costs, and low turnover. I believe that the record for the Total Market Index will be similar to that of S&P 500, but I do not have the data to prove it.

That being said, if given the choice between S&P 500 or the Total Stock Market Index, I would choose the latter (TMI). This is mostly because the total stock market index includes several thousand companies and has exposure to smaller capitalization companies that have historically delivered better results in some environments. Again, as I mentioned in the article above, I focused on S&P 500 because I have a lot of data for its real world performance, it has similar returns to that of the Total Market, and because it is widely available in most employer defined benefit plans I am aware of.

So how does it stack against the criteria I outlined above?

1) A history of dividend increases

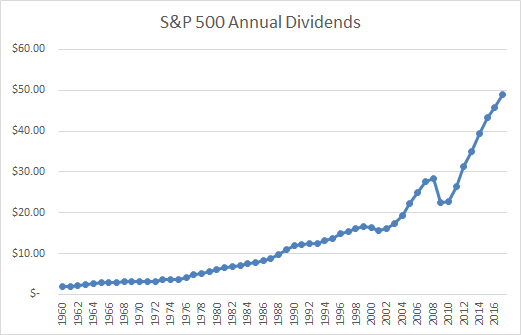

From the charts below, you can see a steep upwards trend in dividends per share over the past 60 years. The only major interruption was during the Financial Crisis in 2008. I would think that a dividend portfolio with exposure to different sectors would have had some dividend cuts in 2008 as well. Since 2009, S&P 500 has managed to grow annual dividends for 8 years in a row. Given the expectations for tax cuts and tax incentives for repatriating foreign profits to the US, I would expect that dividend growth continues in 2018 and 2019. This would bring the track record of annual dividend increases for the S&P 500 into dividend achiever status.

The most interesting observation is that roughly 419 companies in it pay dividends, while the rest do not. The number of non-dividend paying companies increased from the 1980s to the early 2000s, before reversing course. Despite this “handicap”, the index still managed to register higher dividends per share for decades. This should not be surprising however.

Most US corporations tend to have the habit of rewarding shareholders with a dividend increase over time, using their excess cashflows. A successful corporation, similar to a frugal individual, generates more money than it knows what to do with. This excess cashflow is usually distributed to investors in the form of a dividend. Most successful US corporations tend to follow the policy of gradually raising their dividends per share over time. Our experience shows that successful corporations generate a predictable stream of excess cash, which leaves a trail of regular dividend increases. When a company starts to lose its competitive position, its profitability deteriorates to the point where it cannot support its previously established dividend policy.

We are seeing some successful companies today that have never paid a dividend. Examples include Google’s parent Alphabet (GOOG) and Facebook (FB). However, it is quite possible that at some point in time, they will initiate a dividend. For example, Microsoft did not pay a dividend between 1986 and 2003. At that point the company was generating more money than it knew what to do with, which is why it initiated a dividend that it has been growing ever since. Apple (AAPL) is another successful company that initiated a dividend in 2012, after a 15 year hiatus. It has been growing that dividend ever since. I would think that Facebook, Google and even Amazon will one day initiate a dividend for their shareholders. Again, as a holder of S&P 500, I view those three companies as subsidiaries that are still growing. However, at some point they will start paying dividends.

2) Low Costs

Cost is one of the few tools within the control of the individual investor. That is because the lower the investment cost, the higher the amount of profits that you can keep as an individual investor. This fund is available in ETF or mutual fund form through Vanguard (VOO, VFIAX), and costs 0.04%. It is also available through iShares (IVV) at a cost of .04% and through a mutual fund at Fidelity (FUSVX) for 0.035%. At Schwab,(SWPPX) the fund costs 0.03% too. As we all know, when your investment costs are low, this means you get to keep more of the dividends and capital gains, without having to feed an expensive mutual fund manager and/or an expensive financial advisor. As long as you do not pay massively more than 20 times forward earnings for this ETF, it should deliver a decently satisfactory return over an investing lifetime.

3) Low Turnover

The nice fact about S&P 500 and the Total Market Index is that they both have a low amount of turnover. Roughly 3% – 5% of companies leave the fund due to mergers and acquisitions, failure or no longer meeting eligibility requirements. The reason why I would prefer the Total Market Index to the S&P 500 is that it is more inclusive and more passive. It is less likely to take out companies due to market capitalization falling behind a certain threshold and is less likely to make major overhauls on the portfolio composition. The S&P 500 has historically made some notable changes to its composition, such as the addition of financial companies in 1976 to the index. Another change occurred in 1999, when it added more technology companies during the dot-com bubble. That doesn’t mean that either index is not immune to changes in composition and adjusting weights based on free float.

While turnover is low, there is always the possibility that this can trigger capital gains on sales of shares within the ETF/mutual fund portfolio. This is a low probability event, which is still possible nevertheless. This is why it may be preferable to hold those funds in a tax-sheltered account such as a 401 (k) or a Roth IRA.

In conclusion, I believe that ETF’s on the S&P 500 index or the Total Market Index can be good ETF’s for busy dividend investors in the accumulation phase. Unfortunately, their current yields are pretty low around 2% as we speak.

Some investors believe that they can take that 2% dividend yield, and then sell 1% – 2% of their stock holdings every year. I do not recommend having to sell shares to fund retirement. Selling shares can increase the risk of running out of money in retirement, due to sequence of return risk. If you have to sell when prices are low during the next bear market, you may have to sell a lot more shares, and increase your chance of running out of shares to sell. As your number of shares declines, you are increasingly betting that a rising tide will bail you out. While stocks usually go up over long periods of time, they have also gone nowhere for extended periods of time too. If you have to sell shares while prices are low, you are depleting your asset base. This is speculative behavior, and not how an investor should operate.

For retired dividend investors, who are not interested in selecting their own investments, I believe that two good choices today include the Schwab Strategic Dividend Equity ETF (SCHD) and the Vanguard High Dividend Yield ETF (VYM). Both yield close to 3% today, or have at least reached those yields fairly recently. They are decently diversified, and have long histories of real money performance. The retired investor could swap their plain vanilla index fund for one that is focused on current income. This is easily done in a retirement account. However, it will be more difficult and costly to implement in a taxable account, because such a transaction could trigger costly capital gains. Hence, if you are interested in investing in funds,be advised that a retirement account is the best account type for such investments.

Assuming you want to get more enterprising as an investor, you can create your own dividend fund by utilizing an entry criteria to help you reach your goals. You can maintain equal weights, make sure you are not overpaying for companies and you can also check to see if your dividends are secure.

In essence, this I am somewhat of a hybrid investor, because I own index funds in my retirement accounts, and individual dividend holdings in my taxable accounts. When I retire for good, I will likely convert those funds in retirement accounts either into dividend funds and/or build a portfolio consisting of individual dividend payers to complement my retirement income stream.

Relevant Articles:

- The Best Dividend ETF to Consider

- Dividend ETF’s Are Bad for Investors: Here is Why

- How many individual stocks do I need to consider myself diversified?

- My Bet With Warren Buffett

- How to properly weight dividend portfolio holdings

- The Benefits of Automatic Investing

Article by Dividend Growth Investor