Europe has continued to surpass the U.S. when it comes to economic performance in recent years, and that trend looks set to continue through 2019, according to European Commission forecasts. In this opinion piece, Kalin Anev Janse, secretary general and a member of the management board of the European Stability Mechanism (ESM), the eurozone’s lender of last resort, suggests a “Euroboom” is underway, thanks to global investors. He goes on to sketch out critical new steps Europe is taking that he believes will add to the growth numbers. His comments are adapted from his speech at the recent Bloomberg Investment Summit 2018 in Luxembourg.

[REITs]Wow — what a difference a year makes! A year ago, Europe woke up to a big shock. Trump had been elected president of the United States. The polls hadn’t seen it coming. They hadn’t seen Brexit coming, either. Would populism and protectionism win in Europe as well? Was this the end of globalization? What would happen to everything the European Union stood for?

Many feared that the populist wave would spread to Europe: the Netherlands, France and Germany. This would have meant a real revolution in 21st century Europe. But I did not believe that. In January 2017, I stuck my neck out. I said I did not think Europe would see a populist uprising. In an op-ed for Knowledge@Wharton, I explained why.

A Europe from the Mind and Heart

Part of the explanation came from the mind: The three countries holding elections have created more wealth for their citizens over the past 60 years than the U.S. or the UK. Income inequality is also much better in those countries, and in Europe in general, than elsewhere.

And last but not least, the EU has brought citizens of close to 30 countries together like never before. Europe has now seen 70 years of peace — which is unprecedented in its history.

Another part of the explanation came from the heart: I am a Dutchman and a Bulgarian, living in Luxembourg. And I just did not get the feeling a populist surge was about to happen. Speaking to my colleagues, friends or family — no one believed it. What we built up in Europe was too precious to give up.

Luxembourg, where the ESM is based, is a great example. Almost half of the workforce in Luxembourg crosses the borders from Germany, France and Belgium every day. That’s 180,000 people! And the monuments of the terrible world wars are only an hour’s drive away. There is hardly a place where European integration is more tangible, and more visible.

A Spectacular 2017 for Europe’s Economy

Luckily, I was proven right. While the start of 2017 wasn’t easy, it has now emerged as a very strong year for Europe.

The election results were pro-European and Europe’s economy started to perform really well. The EU outperformed the U.S. in terms of GDP growth in 2016. It looks like this will be the case again in 2017 once the numbers are in. That is two years in a row.

But what is even more important is per-capita growth. This shows the share of each European citizen in growth. So, it is what people feel in their pocket. And here, things look even better.

This month, the autumn forecasts from the European Commission came out. They predict that the European Union will outpace the U.S. this year, and in 2018 and 2019. It was already the case in 2016. So four consecutive years!

A #Euroboom from Global Investors

This year I met almost 150 investors around the world. Their feedback was bullish. They see Europe as a safe haven. There is lot of uncertainty about what the new U.S. administration can deliver. And the U.K. is struggling with how to deal with Brexit. Investors simply don’t like such uncertainty.

In today’s social media language, you would say: #EUROBOOM

In today’s social media language, you would say: #EUROBOOM

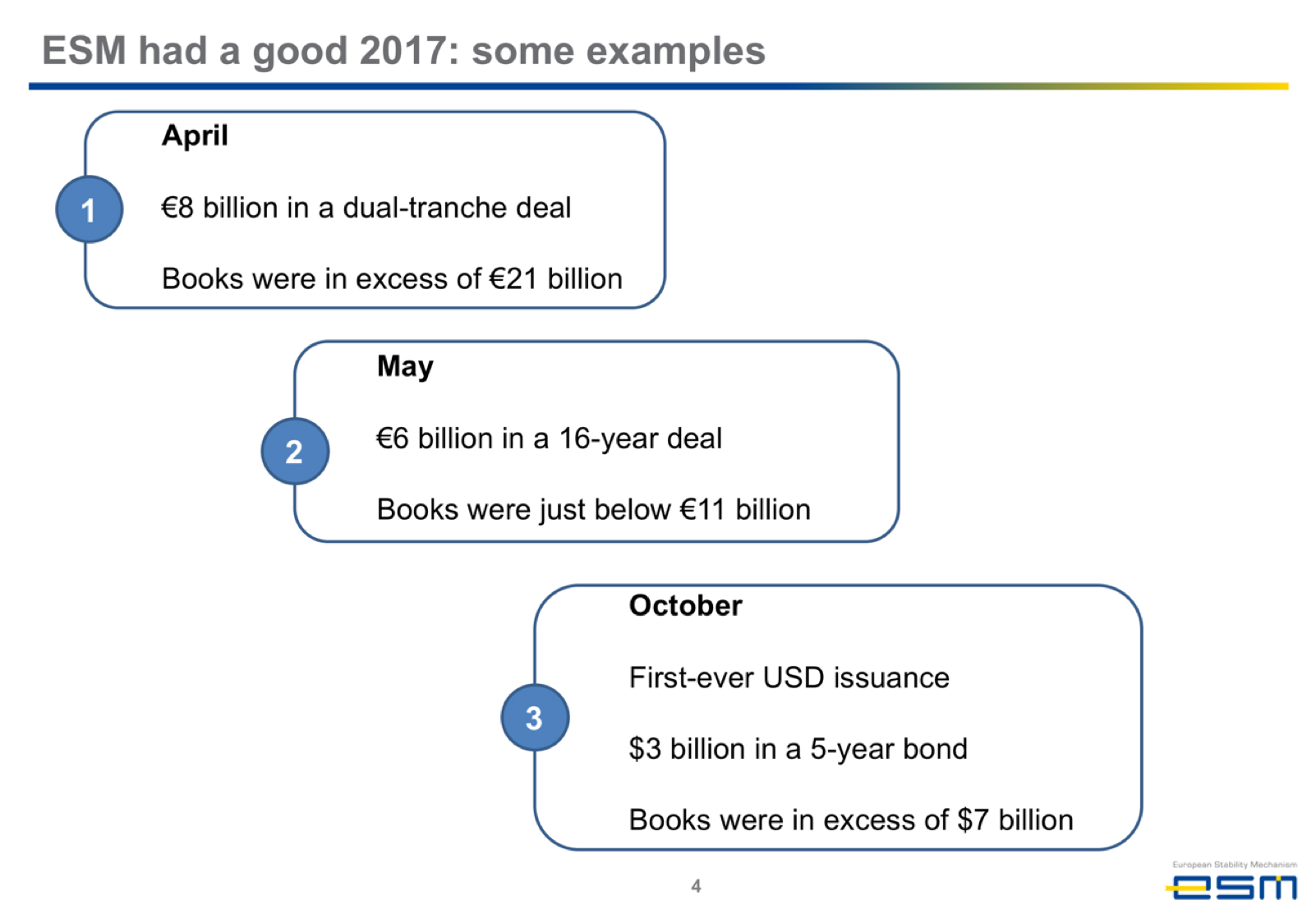

This made my job a bit easier. Just after the French election, we saw that investors had started to recognize Europe’s success. In April, we raised €8 billion in a dual-tranche deal. Books were in excess of €21 billion. In May, on a 16-year deal, we raised €6 billion, with books just below €11 billion.

Our debut in the dollar market last month was also very successful. We sold $3 billion of a 5-year bond, and orders were at $7 billion.

From my investor meetings, I drew three conclusions:

1. Investors have recognized that Europe is doing well.

2. They are putting their money where their mouth is.

3. They want to know what’s next for the euro area.

Next Five Big Ideas for Europe’s Economy

There are a lot of ideas about the future of the euro area — from think tanks, politicians and European institutions. But as a large market player, I want to hear from investors what is needed. A common response is that markets need to become more integrated, that we need a more competitive financial sector, and that we need to deepen economic collaboration.

Fortunately, a lot of the steps that are on the political agenda are already heading in that direction. There is real political movement in Europe’s capitals towards these changes. Reform momentum hasn’t been as good as it is now in a long time. European citizens support it as well.

The popularity of the euro is at record highs. Almost three-quarters of the people in the euro area are in favor of the euro. This gives politicians a mandate to continue to build the monetary union.

Let me walk you through the five big ideas that should “secure Europe’s future.”

First, we need to complete Banking Union. Europe already did a massive amount of work in this area. In record time, we established a single supervisor for the 130 largest banks. And we set up a single resolution fund to wind down banks.

With these two institutions, Europe’s system of banking supervision is comparable to that of the U.S. And what took the U.S. decades, even centuries to set up, we did in a few years. Think about it!

But it’s not complete yet. The SRF [Single Resolution Fund] is slowly filling its coffers. But it needs to be ready at all times, for any eventuality. And therefore, there needs to be a backstop for the SRF. A backstop would make the SRF more credible in the eyes of the markets. In the States, the Treasury can backstop the FDIC if needed. In Europe, the ESM is considered as a likely candidate to play this role of a financial backstop for the SRF.

The second thing we need to add to the Banking Union is a common deposit insurance in Europe. If all of Europe’s banks would guarantee deposits together, it would reduce the risk of a bank run in any country. At the moment, depositors know that ultimately, the buck stops with their government. To know that all of Europe is behind the guarantee would be a big reassurance. And so, once you put it in place, you will hardly ever use a common deposit insurance.

But it’s not that easy to implement. You need to clean up legacy problems with banks in certain countries. Otherwise, healthy banks might end up paying for mistakes made in the past by their competitors in other countries. So this may take a few years. And in general, cross-border European banks are positive about this move, to complete Banking Union.

Fostering Financial Integration

Once you put these two steps in place, you have a pretty complete framework to foster financial integration. And that is needed, because the home bias of banks has risen massively during the crisis. That’s not helpful for a number of reasons. For one thing, it means banks cannot benefit from the economies of scale that cross-border banking brings. So European banks are less profitable. They are unlikely to retrieve the cost of capital for the foreseeable future, which is a situation that cannot last.

But having fragmented banks also means fewer economic ties in the euro area. Having one single currency means converging to one banking sector. The banking sector is the gear stick for the economy. And you can’t drive a car with 19 different gear sticks.

Thirdly, Europe needs to harmonize financial markets. It needs to become much easier to invest from one country into the other. This is a wide-ranging project known as the Capital Markets Union.

At the moment, bankruptcy laws — for instance — vary massively between European countries, for reasons that sometimes date back centuries. The same differences exist in corporate law, and in tax law. If it would cost less time to figure out the laws in the country you want to invest in, surely this would open up investments abroad. It would help venture capital and the private equity market. And that’s good news for companies, because it would open up a new financing channel for them.

Now, let me address the question of whether Europe needs more fiscal tools to help the economy. That is my fourth point. You may have heard people talk about setting up a rainy day fund in Europe, and this is a related issue. Let me explain what is meant by that.

Poor European countries can get support from the EU budget. The EU budget is small, only 1% of the size of Europe’s economy. As a comparison, the U.S. Federal budget is 17% of GDP. But for the receiving European countries, the transfers can be large, up to 4% of their GDP. This system works well, and it is sufficient.

We also have a system in place for when the entire euro area is hit by a severe economic downturn. In that case, countries are allowed to spend more taxpayer money than is normally the case.

Normally, as you know, there is a cap on budget deficits of 3% of GDP. But during the euro debt crisis, countries simultaneously exceeded this — and this was a big help in stimulating the economy at a time when it was badly needed.

But what if a single country is hit by a crisis, and its neighbors aren’t? For instance, think of a case where Ireland is hurt if the Brexit negotiations fail to come up with a good solution? Then there is no fiscal leeway for the country. Economists call this an asymmetric shock. And it would be good to have a facility in the euro area to do something against such shocks. Of course, the ESM can already address problems in individual countries. But that’s when it is too late, when they have already lost market access. This new facility would be used to prevent such problems, and to prevent the ESM from having to act.

Different models are being discussed. One strict condition is that countries always need to repay any funds they receive. There will be no permanent transfers between countries, and there will be no jointly issued debt. That’s just a political reality … today. But this is possible, and if you want to know how it can work, you need to look at the United States. Most states in the U.S. have rainy day funds, which they can tap during a crisis. And later, when they have recovered, they need to simply repay the money.

There are also other models, which work on the basis of a complementary unemployment insurance. These models are being studied, and this looks like a realistic option now as well.

Further on the fiscal side, politicians are studying ways to simplify the fiscal rules. The rules under the Maastricht Treaty and the Stability and Growth Pact, which impose fiscal discipline in Europe, were made tougher after the crisis. But now, they have become too complex: hundreds of pages. They are very hard to understand, even for experts. Making them simpler would make them more credible.

‘A Lot More Europe’

But in some countries, people are scared that all this means “a lot more Europe.” That is not the case. We do not need a full fiscal union, with extra transfers between countries. And we certainly don’t need a full political union. If that were the case, we would be the United States of Europe. That is not something that has a lot of support these days.

Finally, regarding the European Monetary Fund — my fifth and last point. It is a reality that the role of the IMF, our global counterpart, in Europe has gradually become smaller. When the crisis first started, and Ireland and Greece needed financial support, the ESM did not have the expertise to do that. Nor did we have enough money at that time. But over time, the financial firepower of the ESM has grown, and so has our expertise. And the role of the IMF, at least financially, has become less prominent. In the current Greek program, they have so far not contributed any money.

I believe there is a consensus now that in any future crisis in Europe — I am not saying that there is one on the horizon, but it will occur at some stage — the IMF will probably no longer be involved in our programs.

So then, rather than having four creditors – IMF, ECB, ESM and the European Commission – you’d just have two. The ESM would do the programs together with the Commission. And exactly how we would divide the labor is now also being thought about.

I believe these are the big five policy topics to watch in Europe next year. The aim is to have a more stable and stronger euro area.

Let me return to the conclusions noted at the outset. Europe is a project of the mind, but also from the heart. It has been extremely successful in fighting the crisis. I think the economic data show that sufficiently. But it is now time to take the next steps to sustain that success.

These steps are no longer vague ideas that may or may not happen. They are concrete steps that are firmly on the political agenda. They all aim to make the markets stronger, to support the recovery of the financial sector, to make the monetary union more robust and the economy more resilient.

Yes — the plans are ambitious. But I am committed — my institution is committed — to make them happen.

Will 2018 be as good as 2017?

I began by saying Europe woke up with a shock a year ago. But, look at what happened in 2017.

In Europe, we live in a society where multilateralism is a tradition, where international cooperation is a habit, and where our neighbors have become good friends. In 2017, European citizens truly spoke with their minds and their hearts. And investors showed their strong trust in our continent.

I hope at the end of 2018, we can reflect on the year again and look back at the steps that Europe took to secure its future. To create more jobs for citizens, and more security. When we do that, I personally hope to be able to say again: “Wow, what a difference a year makes!”

Article by Knowledge@Wharton

{kind=link}