Dead cat bounce or does the equity market have what it takes to reverse that negative bear market stigma? As we highlighted over the last few weekly notes, we suspected the equity markets would bounce. However now, we feel that the euphoria has hit some technical levels that should put to test the veracity of this rally. We like to take a longer-term approach in times like this as everyone is all goosed up about the rebound, because fundamentally nothing has really changed. In fact, one can argue where fundamentals are concerned, the backdrop continues to weaken, global instability continues to gain, and the US government furlough seems to be foolishly overlooked.

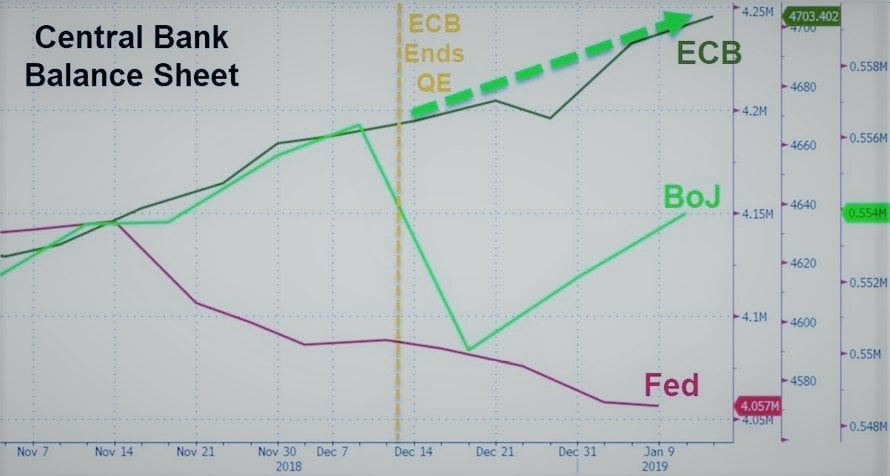

The French yellow vest movement continues unabated and western media continues to shun coverage. Brexit once again continues with uncertainty and we can’t figure out for the life of us what that even entails in the larger scheme of things, other than it sets a precedent for others to follow. Speaking of Europe, we can’t help but notice Draghi and his alleged balance sheet reduction as the ECB continues to take on assets. As Zhedge posted today, the balance sheets of the ECB and BOJ continue to grow. We suppose the latter couldn’t help themselves considering the Nikkei weakness to take down just a few more shares! Anyway, here is their chart, which perhaps, points to a single rationale for equity outperformance early on in 2019:

Q3 hedge fund letters, conference, scoops etc

No matter, you all know our mantra “QE4EVR” and it’s obvious here even the smallest equity pullback sends cold water shivers down the spines of these weak central bankers. DeutBank this week cut the EU growth forecast 30% down to 1%. So, the test is on for these central bankers, are they willing to let asset prices fall and balance sheets shrink, or will it be business as usual?

No matter which they choose two outcomes are certain, debt piles will continue to grow exponentially, and market signals will continue to be heavily distorted by this endless artificial central bank support. They aren’t fooling us, we know the truth, fiat and debt, they are the same things and to value an asset based on them is a function of continued QE. Without QE asset prices fall, defaults occur, economies contract and central banks assert further control. Whether or not the people like it, doesn’t matter, unless the entire system changes this is all we have.

So, with all that said, we are still going to say Powell stays the course and hikes in March to get the Fed Funds toward the upward bound of 2.75%. His history, his opinions, the fact that he is not an economist, gives us hope that he will continue what he started. It’s not because we want a prolonged contraction or a recession to be induced. Rather, it is because we know that the natural course of things is inevitable, not preventable. The longer we allow this charade to continue the harder the punishment will be in the long run and it’s not financial ruin we are concerned with as so much the drubbing civil society will take when eventuality does reach its due course.

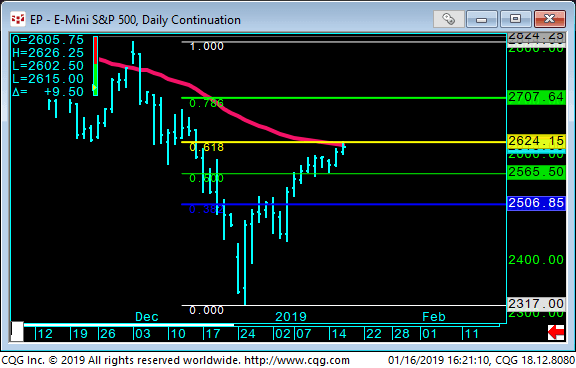

Technically, let’s look at how the week transpired. This chart of the SP500 future gives a great technical glimpse at the resistance from both the fib. 61.8% as well as the 50 period Vwap. The 2625 level is the bull’s hurdle and the bears level to defend:

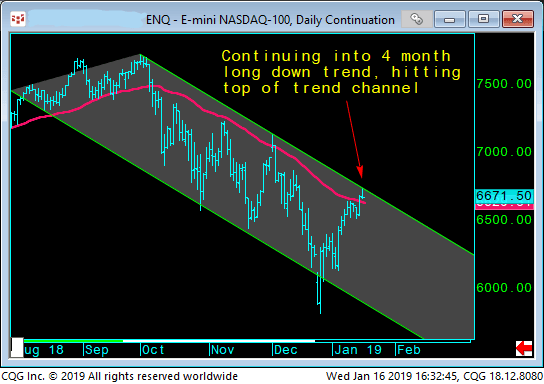

The Nasdaq future is situated at the top of our 4-month long trend channel as 6675/90 area seems to be logical resistance:

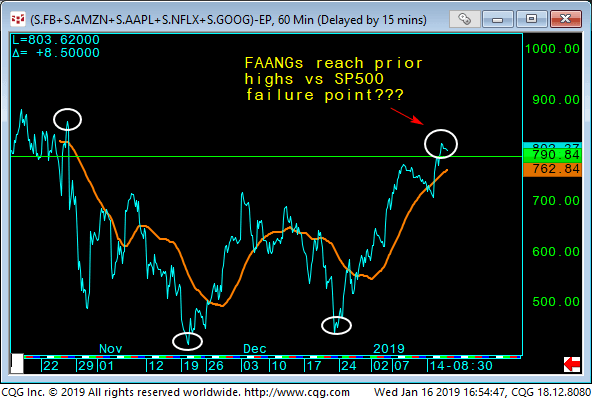

The tech heavy Nasdaq when viewed vs the SP500 has hit near the prior highs from late November. We know FAANGs continue to be the favorite, but we are thinking the boat is full and if the tide does turn again, life jackets will be far and few between:

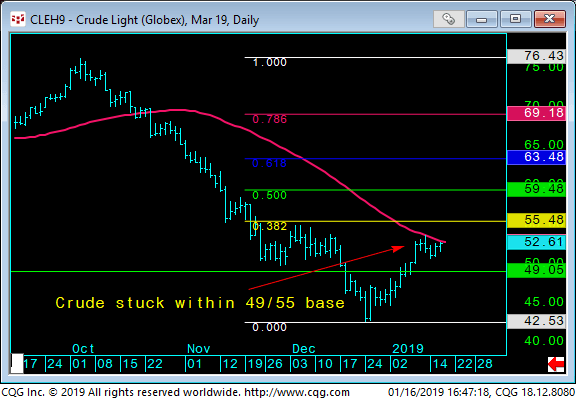

When we look at March Crude Oil, we can see that it too peaked last October and since putting in a nice low at $42, we are back forming a base between $49 and $55 with clear resistance from the Vwap continuing to pressure the bull’s case here:

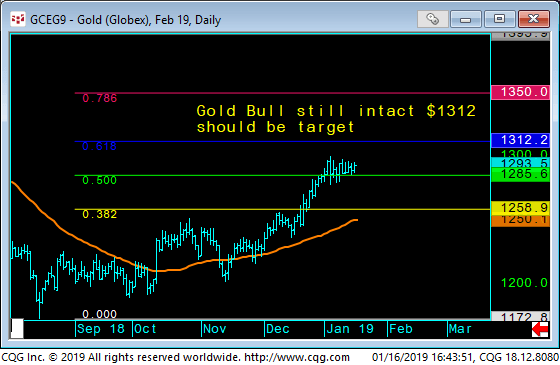

Our final chart is Feb Gold, which continues to shine, and we feel a break of $1295 points nicely up to $1312 and ultimately up toward $1350:

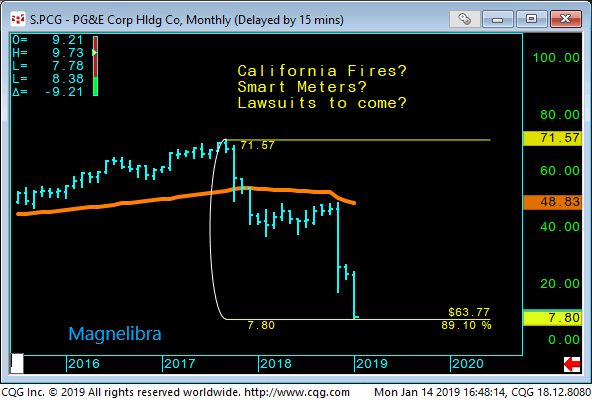

We have a follow up to our ongoing PG&E saga, which we first mentioned in our November 14th weekly letter. Well with bankruptcy almost certain and despite the rating agencies ineptitude to downgrade them sooner, it looks as if they will become the third largest IG default in history with $17.5bln of index eligible debt. (Zhedge) Here is a chart we posted back in November:

What else have we learned this week? The WSJ put out a nice piece on the hackers of the SEC EDGAR filing system and outlined to perfection their scheme to profit from the information. We can’t help but think that this will continue to be an issue in the electronic global market place. An issue that will continue to plague our digital lives, especially considering IBM is going to put their new quantum computer in the cloud. If you don’t know what this means for old encryption and security, well you better read up, things are about to get truly interesting. Sort of makes me wish we could go back to the good old paper trail pit trading days where everything was done with a physical order.

We also read a quant piece on Rep. Ocasio’s plan for a 70% tax rate, the numbers are in and that would raise some $300bn over 10 years…this is nearly half the amount claimed. It will be interesting to watch the polarization between the political left and right in this country unfold, one thing is certain, these politicians can claim that they are the beacons of hope for their constituents, when they are nothing more than mouthpieces for the highest bidders.

Finally, on a sadder note, Vanguard found Jack Bogle died today. The financial industry titan single handedly paved the way for passive index fund investing and turned Vanguard into a behemoth with more than $5 trillion in assets, what a legend! Ok that does it cheers!

Sign up for our weekly newsletter here:

http://info.capitaltradinggroup.com/ctgs-weekly-unique-insights-newsletter-0-1-0

Finally, we will decidedly end our notes with our reaffirmation of the growing need for alternative strategies. We would like to think that our alternative view on markets is consistent with our preference for alternative risk and alpha driven strategies. Alternatives offer the investor a unique opportunity at non correlated returns and overall risk diversification. We believe combining traditional strategies with an alternative solution gives an investor a well-rounded approach to managing their long term portfolio. With the growing concentration of risk involved in passive index funds, with newly created artificial intelligence led investing and overall market illiquidity in times of market stress, alternatives can offset some of these risks.

It is our goal to keep you abreast of all the growing market risks as well as keep you aligned with potential alternative strategies to combat such risks. We hope you stay the course with us, ask more questions and become accustomed to looking at the markets from the same scope we do. Feel free to point out any inconsistencies, any questions that relate to the topics we talk about or even suggest certain markets that you may want more color upon.

Capital Trading Group, LLLP (“CTG“) is an investment firm that believes safety and trust are the two most sought after attributes among investors and money managers alike. For over 30 years we have built our business and reputation in efforts to mitigate risk through diversification. We forge long-term relationships with both investors and money managers otherwise known as Commodity Trading Advisors (CTAs).

We are a firm with an important distinction: It is our belief that building strong relationships require more than offering a well-rounded set of investment vehicles; a first-hand understanding of the instruments and the organization behind those instruments is needed as well.

Futures trading is speculative and involves the potential loss of investment. Past results are not necessarily indicative of future results. Futures trading is not suitable for all investors.

Nell Sloane, Capital Trading Group, LLLP is not affiliated with nor do they endorse, sponsor, or recommend any product or service advertised herein, unless otherwise specifically noted.

This newsletter is published by Capital Trading Group, LLLP and Nell Sloane is the editor of this publication. The information contained herein was taken from financial information sources deemed to be reliable and accurate at the time it was published, but changes in the marketplace may cause this information to become out dated and obsolete. It should be noted that Capital Trading Group, LLLP nor Nell Sloane has verified the completeness of the information contained herein. Statements of opinion and recommendations, will be introduced as such, and generally reflect the judgment and opinions of Nell Sloane, these opinions may change at any time without written notice, and Capital Trading Group, LLLP assumes no duty or responsibility to update you regarding any changes. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Any references to products offered by Capital Trading Group, LLLP are not a solicitation for any investment. Readers are urged to contact your account representative for more information about the unique risks associated with futures trading and we encourage you to review all disclosures before making any decision to invest. This electronic newsletter does not constitute an offer of sales of any securities. Nell Sloane, Capital Trading Group, LLLP and their officers, directors, and/or employees may or may not have investments in markets or programs mentioned herein.

{kind=link}