We have talked at length on the sinking Dollar and at Davos the “Mnuch” stated that “the weak dollar is good for the U.S. as it relates to trade and opportunities.” Gee thanks Mr. Secretary , but what do you guys really mean? We will tell you what it means…it means that the FED cannot have its cake and eat it too. It cannot on one hand raise rates and on the other have sit- idly by with an ever sinking U.S. Dollar.

Now all econ fundamentals aside, one should be asking, why is the dollar moving lower when our rates are moving higher. Shouldn’t that make our debt more attractive on yield a level vs another countries debt? One would think but in a central bank, in a globally coordinated central bank world you have to realize that the central banks are not working independently but in unison. We will dig deeper into that at another time, but the crux of the statement is every nation cannot be an exporter and when countries go to war with their currencies; the outcomes globally are usually disastrous and swift. Are we there yet? Yes we tend to think we are and how long the markets will continue to ignore this is anyone’s guess. Anyway the problem with the FED raising rates coupled with the U.S. fiscal support, means a whole bunch of debt is going to have to be swallowed and higher rates have to attract such unwilling participants.

The last decade will go down in the history books as the decade the central banks hijacked global financial systems and decided that it’s in everyone’s best interest to work together. That is, obviously until it is not. Who will be the first to balk? Our guess is the Chinese. They have the most to lose, domestically and internationally and it’s why they have been so reticent in shoring up their gold reserves and trying to internationalize their financial exchanges. However their underlying distrustful fiscal policies and their too good to be true WMPs, no not WMDs of the good ole Bush era, but potentially a synonymous acronym none the less as these WMPs will be like economic weapons of mass destruction. WMPs are Wealth Management Products, which basically package deposits and attract buyers with higher rates of interest, we hate to say it, but they sure do look a bit Ponzi in nature. Then again, isn’t the entire leveraged, rehypothecated, fractional reserve system, exactly just that? So let’s get to some other market news this past week:

- Starbucks was out this week saying it’s going to spend $250m on new employee benefits.

- Credit Suisse was out stating the Pension Funds sector should be a natural seller when it rebalances this month. No doubt equity outflows will benefit bond inflows, but in realty how big of a dent will this be?

JPM commented upon this and gave us this nice chart below. When we looked at this chart what stood out to us as odd was that the Pension Funds have flat lined their bond purchases, seems a bit odd considering the fixed payment obligations they have. This made us think pensions have been overreaching for yield for decades and in return receiving massive convexity risk. none the less we feel that if Pensions decide that equity risk is too much, we could see some massive reallocation into bonds and lower yields would beckon and equities will have a few less fools, anywhere here is the chart:

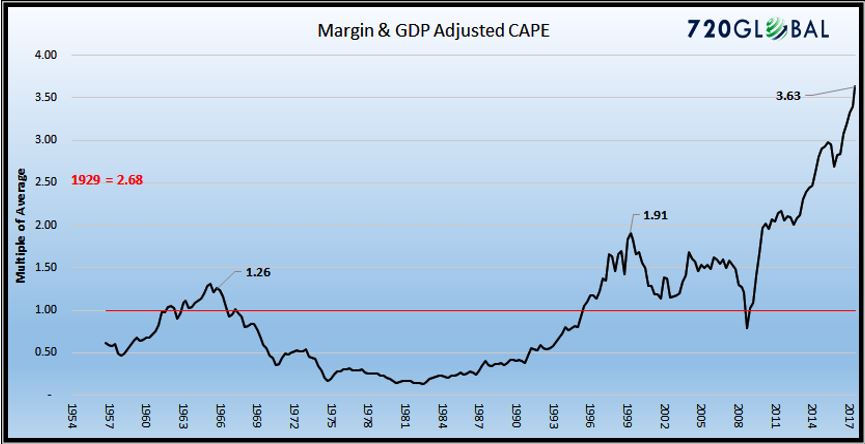

- 720Global was out this week with some charts of their own fitting Margin, GDP and Schillers CAPE, we think the following chart is shocking and from a value perspective in owning equities here, if you’re scared of Bitcoin, well Caveat Emptor:

- Goldman out with an economic report which covered the equities growth and its relationship to increasing GDP. The report focused upon a sharp correction where stocks fall 20% in Q1, hmm some interesting timing considering the rebalancing coming up. Also of note we noticed Goldman’s year end SP500 level is 2850 a level that is lower than Friday’s settlement price.

- ECB meeting produced some interesting developments as Draghi was calling out the U.S. for currency manipulation rhetoric…see the wars have already begun…anyway here are the headlines from the ECB and Draghi:

- VERY FEW CHANCES OF A RATE HIKE THIS YEAR

- SOMEONE ELSE’S FX TALK DOESN’T COMPLY WITH AGREED TERMS

- SAYS STRUCTURAL REFORMS MUST BE STEPPED UP SUBSTANTIALLY

- URGES OTHER POLICY ACTORS TO CONTRIBUTE MORE DECISIVELY

The results of such rhetoric, well a surging Euro of course:

As for German 10 year yields seems as if 60 basis points some 212 basis points lower than corresponding 10 year U.S. yields is the line in the sand, here’s the chart:

So an astute observer asked, why not just buy U.S. and sell German 10 years? Well good point and if we were the likes of G&G (Gross & Gundlach) we most likely are, but we can’t telegraph it right. Anyway there are other forces at play, most notably the currency risks and a whole host of short term basis funding issues, not only with the Euro but the Yen as well. But hey at least some are thinking astutely! So we simply replied to their question with this, “Cross basis currency swaps are expensive meaning dollar funding is expensive and there is no compensation for yield pickup for foreign investors and the flip side to QE is dollar weakness which should continue and if they don’t get ahold of the short rate from rising to far too fast, the dollar will get smoked and U.S. 10s will be plus 3%.

We also believe the crypto space is pulling some real capital out of leveraged markets and into the global economy, so money is being funneled out of the U.S. and who knows where it goes from there…so if this continues than leverage has to fall because the banking system is being drained of cash, so it will be interesting to see how raising rates into a cash shortage moves markets…our assumption would then be the dollar falls vs all other fiats…this would be the natural progression and of course U.S. equities would be the next likely culprit to tumble, they will lose 30% by summer is our guess if they continue to raise rates.

- BofAML put out their “Bull & Bear” indicator this week which has a 100% successful hit rate on its signals since 2002, with the average peak to trough of 12%. They warn that the SP500 has a potential pullback area of 2686 by March or some 10% lower from last week’s highs.

-We certainly won’t disagree with his thesis!

- Q4 GDP missed expectations of 3%, rising only 2.6% as imports surged. Overall 2017 was decent with a 2.3% rise in GDP on the heels of good consumer and business spending.

- The U.S. DOJ, CFTC and FBI worked together, and charged 3 European banks (DB, UBS & HSBC) and 8 individuals in an alleged “spoofing” case with total fines reaching $46.6 million. We kind of have to laugh at that considering the banks involved and the amount of money they made off of these trades. The penalty doesn’t fit the crime, that we are certain. Anyway it is good to see at least that some justice is being served, the markets in question were gold, silver, platinum or palladium futures, as well as in S&P E-mini futures.

- We read somewhere of a plan that Illinois wants to issue $103 Billion in bonds to pay for pensions…hmm well why not? I like the idea and in a world where a country like Greece is paying 1.27% I don’t blame the Democrat who came up with this idea…I would first call Draghi and make sure the ECB amends their monetary policy to enable for purchase, US Munis…Illinois must first remove the inherent structural problem of the state’s constitution however, which bans any reduction in worker retirement benefits, then again, nobody ever accused a congressman of too much logic.

Ok let’s move to some market moving technical charts shall we:

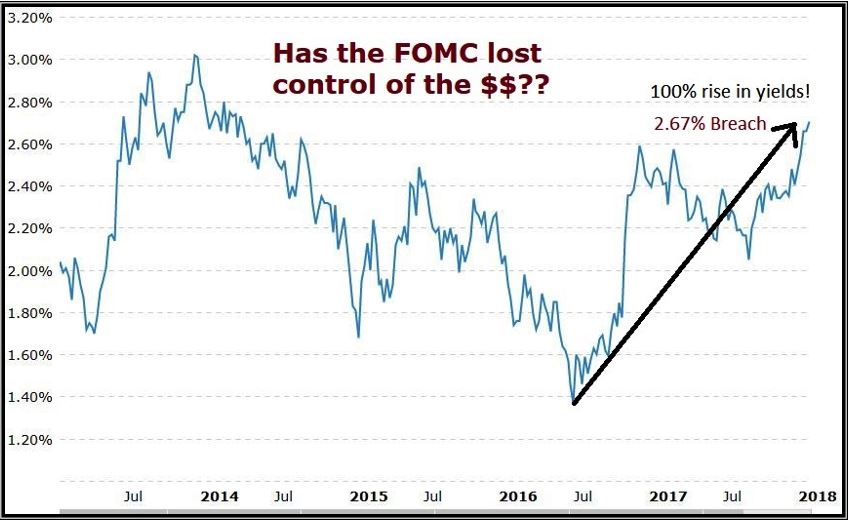

US 10yr yields have risen over 100% since mid-2016 and now are over 2.7%:

Updated chart from Keystone Charts on the US 10yr today with the Golden Cross:

Sticking with the US Treasuries, here is the 30yr pushing 3%:

We would tend to think that the 200 month moving average in this US 5yr yield chart will entice both pension funds and insurers alike; if not well, we would gladly replace your existing PMs and do their job for them:

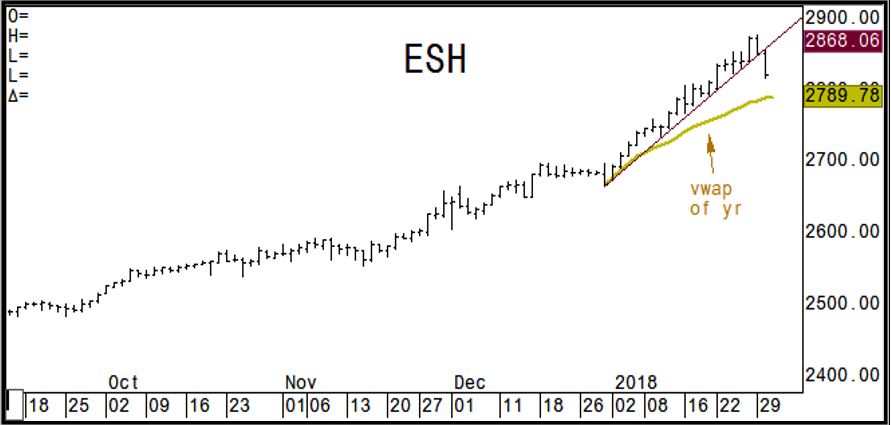

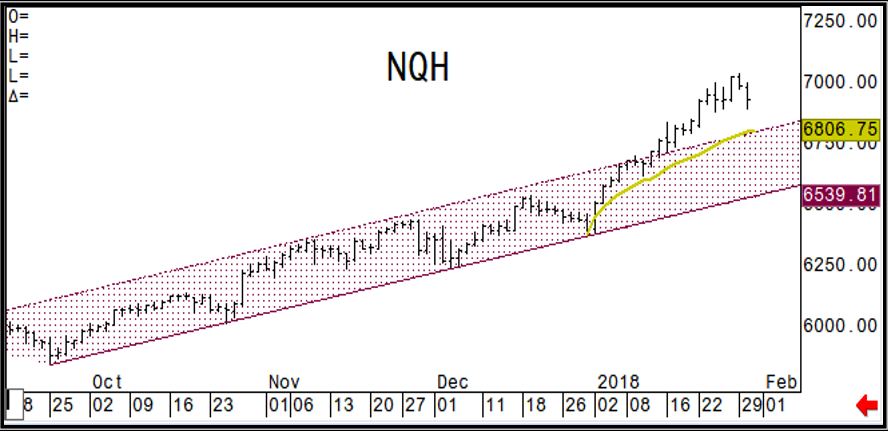

Moving over to US Equity Index land we can see both the SP500 and the NASDAQ had a rare 1% down day today as of this writing. We suppose the Spectre (Capitalized and spelled intentionally for those inquisitive minds) of inside intel at Davos, all the bearish Inv. Bank reports and portfolio rebalancing sent the MOMOs in sell mode, anyway here are the latest charts with VWAP supports:

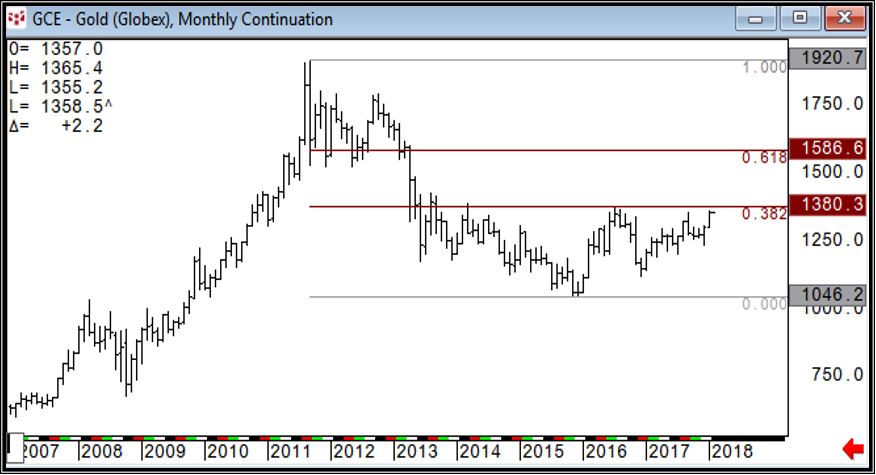

Moving to the metals, it seems Gold has run into some nice 38.2% resistance:

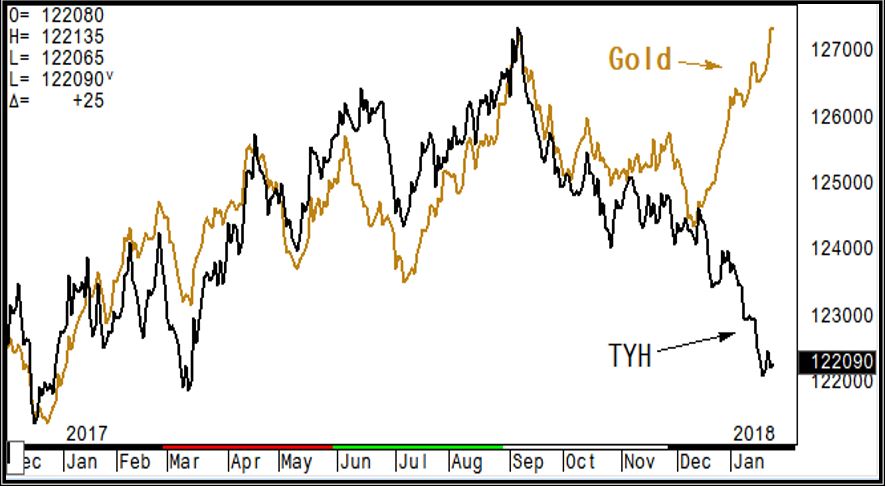

So much for the gold correlation with the US 10yr, risk parity what?

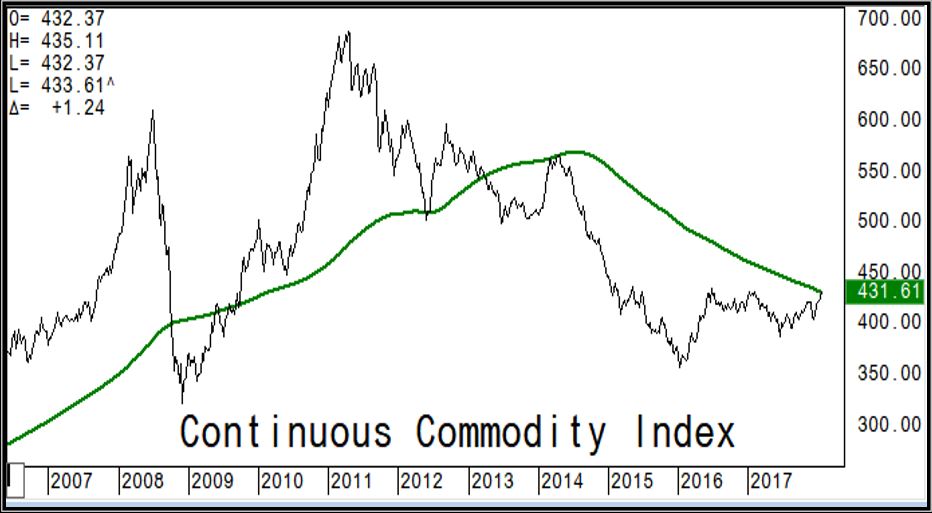

With all this bearishness abound where do we see some positive light, is there anywhere to hide? Well we present this chart:

* The Continuous Commodity Index (CCI) is a broad grouping of 17 different liquid commodity futures, which is a benchmark of performance for commodities as an investment. We thank Keystone Charts for pointing this out, we know where Jeff Gundlach stands on this area, so due your diligence.

Now moving to our section known as:

{CryptoCorner}

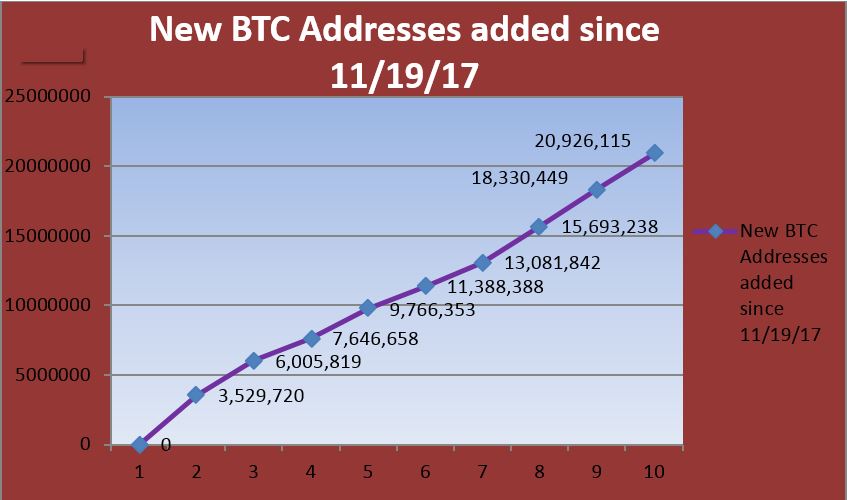

We continue to see a pullback in the crypto currency space. As always we like to keep things in context as the massive run up since last November is merely being walked back. We continue to see adoption in the space which can be displayed in the following chart which shows the cumulative growth in new BTC addresses since last November:

- As usual the likes of J. Stiglitz and various banks were bashing Crypto at Davos stating things like, Bitcoin is used for “secret use cases” & that fiat currency is superior. We wouldn’t expect anything less from old establishment style players.

- Hey Coinbase isn’t going to complain, it was reported this week that they are making nearly $2.7 million a day and $1 Billion in revenue last year! Coinbase has some 13.5 million years and continues to grow.

- Robert Shiller at Davos said cryptocurrency is a “really clever idea, I’m impressed by the technology, blockchain is important, but it’s not stable”

- Sweden’s Deputy Central Bank governor summed Bitcoin up best at Davos, “The fact that people keep talking today that bitcoin is below 10,000, it’s a disaster, or bitcoin is above 10,000 and that’s crazy. I think the fact that bitcoin is still alive, and attracting so much attention, the fact that we’re talking about bitcoin in Davos with a Nobel Prize winner, a central bank governor and a seasoned investor, I think that’s a powerful tool”

- Mnuchin of course took a negative tone and stated “My number-one focus on crypto currency is that we want to make sure it’s not used for illicit activity” –Hmm how about the U.S. Dollar Mr. Secretary?

- Japan’s Coincheck exchange was hacked on January 26th, which saw a theft in the amount of $534 million in NEM coins. What is now known, and an apparently a major oversight by the exchange was the fact that the coins were stored on a single signature hot wallet. –How could they be this stupid??? Good news is that Coincheck plans on refunding in full all the users that were affected. This is in our opinion the essence of progress; we only wish Mt. Gox was so diligent. Further the development team at NEM announced its working on tracking the coins and tagging addresses that are involved.

-See we see this as good progress in an area that will continue to see constant threats, but it takes an ecosystem with the kind of players willing to right the wrongs, for it to grow organically and positively.

- Been reading a lot about EOS a platform being built by Dan Larimer of Block.one, we think our readers should look more into this. It seems as if it will compete directly with Ethereum. What is EOS? It is software that introduces a blockchain architecture designed to enable vertical and horizontal scaling of decentralized applications. It seems as if Mr. Larimer wants to solve the transaction support systems to handle massive volumes prior to jumping into running financial markets on blockchain. We admire their vision, so read further into what they are doing. His presentation can be viewed HERE

- Rapper 50 Cent’s move to accept bitcoin for his 2014 “Animal Ambition” album has resulted in a multi-million dollar windfall! –Sure if he hasn’t bailed by now!

- Mobius Network co-founder and CEO David Gobaud explains, why his startup ran its initial coin offering (ICO) on the Stellar network instead of Ethereum, the most popular blockchain for token sales. Noting Ethereum’s scaling challenges. “the company that makes transacting in crypto easy, the fastest, stands to recoup benefits with a long tail,” Gobaud said

- Chicago based DRW Holdings is hiring cryptocurrency experts at home and abroad. Its Cumberland Mining unit has been active since 2014, trading cryptocurrencies. DRW bought Bitcoin from the U.S. Government after the takedown of Silkroad, buying 27k BTC at the auction

- GDAX, the cryptocurrency exchange run by startup Coinbase, has partnered with trading software provider Trading Technologies to integrate spot bitcoin trading with futures on Bitcoin. –hmm latency front running anyone?

- Stock trading mobile app provider Robinhood plans to roll out Bitcoin and Ether trading services via its mobile apps next month, trades will be FREE! Robinhood has 3 million accounts. CEO Tenev said, “We envision a world where people can have your cryptos alongside your stocks, ETFs, and more” –Damn we applaud and fully support their effort!

Finally IMF managing director Christine Lagarde spoke briefly of the Bitcoin movement in Davos, she said the technology, and the distributed ledger technology is fascinating, has multiple uses like tracing transactions and in land ownership. She then said its anonymity is likely to facilitate money laundering, dark money. -Hmm so on one hand she says the technology is fascinating because of its ability to trace transactions and yet on the other hand they continue to push the illicit activities narrative. Well you can’t really have it both ways now can you? You can’t say the technology can trace transactions then turn around and complain that it’s a boon for illicit anonymous users now can you? This is the typical double speak misdirection, but we know better now don’t we.

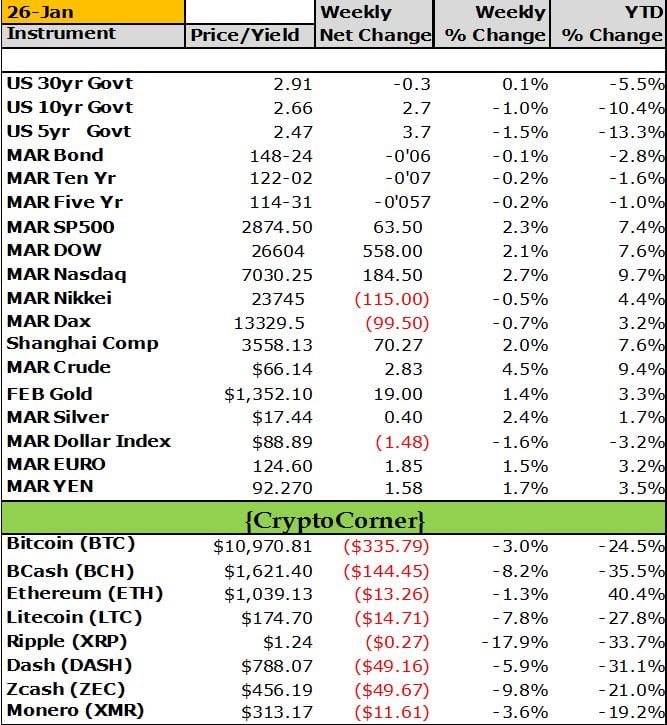

In conclusion, we look forward to the State of the Union speech and considering Trump’s demeanor, no doubt he will be speaking with a proud, boyish grin, the usual arrogance we have been accustomed to. Hell we don’t even mind anymore, it works and that’s why he was elected in a populist revolt, because the people want something that works. Some may not agree with everything he says, he does, nor the way he delivers it, but hey, we all know the great old adage: If you try pleasing everyone, you end up pleasing no one! Unfortunately there will always be sides, we just like being on the right side of things as opposed to the other alternative. Ok, we leave you with the weekly settles where you can see we have separated the traditional markets covered and added a new Crypto section. Cheers!

Weekly Settles for Friday January 26th 2018

Finally, we will decidedly end our notes with our reaffirmation of the growing need for alternative strategies. We would like to think that our alternative view on markets is consistent with our preference for alternative risk and alpha driven strategies. Alternatives offer the investor a unique opportunity at non correlated returns and overall risk diversification. We believe combining traditional strategies with an alternative solution gives an investor a well-rounded approach to managing their long term portfolio. With the growing concentration of risk involved in passive index funds, with newly created artificial intelligence led investing and overall market illiquidity in times of market stress, alternatives can offset some of these risks.

It is our goal to keep you abreast of all the growing market risks as well as keep you aligned with potential alternative strategies to combat such risks. We hope you stay the course with us, ask more questions and become accustomed to looking at the markets from the same scope we do. Feel free to point out any inconsistencies, any questions that relate to the topics we talk about or even suggest certain markets that you may want more color upon.

____________________________________________________________________________________

Capital Trading Group, LLLP (“CTG“) is an investment firm that believes safety and trust are the two most sought after attributes among investors and money managers alike. For over 30 years we have built our business and reputation in efforts to mitigate risk through diversification. We forge long-term relationships with both investors and money managers otherwise known as Commodity Trading Advisors (CTAs).

We are a firm with an important distinction: It is our belief that building strong relationships require more than offering a well-rounded set of investment vehicles; a first-hand understanding of the instruments and the organization behind those instruments is needed as well.

Futures trading is speculative and involves the potential loss of investment. Past results are not necessarily indicative of future results. Futures trading is not suitable for all investors.

Nell Sloane, Capital Trading Group, LLLP is not affiliated with nor do they endorse, sponsor, or recommend any product or service advertised herein, unless otherwise specifically noted.

This newsletter is published by Capital Trading Group, LLLP and Nell Sloane is the editor of this publication. The information contained herein was taken from financial information sources deemed to be reliable and accurate at the time it was published, but changes in the marketplace may cause this information to become out dated and obsolete. It should be noted that Capital Trading Group, LLLP nor Nell Sloane has verified the completeness of the information contained herein. Statements of opinion and recommendations, will be introduced as such, and generally reflect the judgment and opinions of Nell Sloane, these opinions may change at any time without written notice, and Capital Trading Group, LLLP assumes no duty or responsibility to update you regarding any changes. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Any references to products offered by Capital Trading Group, LLLP are not a solicitation for any investment. Readers are urged to contact your account representative for more information about the unique risks associated with futures trading and we encourage you to review all disclosures before making any decision to invest. This electronic newsletter does not constitute an offer of sales of any securities. Nell Sloane, Capital Trading Group, LLLP and their officers, directors, and/or employees may or may not have investments in markets or programs mentioned herein.