CorMedix Inc. (CRMD): Strong Sell On Partner Failure, Misleading Data And Paid Stock Promotion. -91.4% Downside by Pump Stopper

Also we are NOT an investment advisor but see some of our earlier articles on CRMD

Summary

- CRMD’s 1970s-era chemical acquired for <$1m cash from bankruptcy after 2+ failed sale attempts. Bankruptcy documents show Fresenius passed on CRMD even at <$2m value while Gambro deemed Taurolidine worthless.

- German corporate records show Tauropharm is ~$1.3-2.5m failure, indicating CRMD market claims are inaccurate. German court transcripts show CRMD patent based on “outdated” prior art view, so CRMD patent worthless.

- CRMD uses misleading clinical-data as in-depth industry research shows Neutrolin/Taurolidine is a failure while “40% benefit!” versus industry standards is inaccurate. CRMD now spends more on insider compensation than R&D.

- CRMD’s failed shell financially engineered by biotech wipeout artist Rosenwald, associated with fraud allegations and disasters, CRMD also partnered with John Carris who was expelled by FINRA for fraud charges.

- Despite 8+ years of “imminent” Phase3 trials and strategic partner claims, with paid stock promotion and failed company sale process, CRMD stock has temporarily pumped to an unsustainable 224m+ valuation.

I believe CorMedix is one of the most brazen, worthless biotech shells of insider enrichment I have ever seen. Bankruptcy documents show Cormedix (NYSEMKT:CRMD) is based on a 1970s-era catheter product acquired for <$1m cash the last time this company went bankrupt, apparently after at least two failed sales processes. Global catheter companies apparently passed on CRMD when given the option to purchase CRMD for almost nothing out of bankruptcy while Gambro evaluated the product and abandoned it.

After failing on all other prospects (given abandonment of these other compounds), CRMD was left with Neutrolin. Then, with just 5 full time employees and this antiqueted product derived from Taurine (yes, the antioxidant in RedBull), CRMD was financially re-engineered into a public shell by famous biotech wipeout-artist Lindsay Rosenwald while also partnering with John Carris, who was expelled by FINRA for fraud charges involving an ilegitimate tattoo and gun shopping spree with stock manipulation.

Picture credit CorMedix and me

German corporate records show Tauropharm (selling a product identical to CorMedix ’s for 15 years) is at best a $3-4m per year business that is not growing and marginally profitable, indicating CRMD’s market size claims are wildly inaccurate. Why does CRMD management seem to me to pretend Tauropharm financial data is not available when asked on CRMD investor calls?

Furthermore, direct German court transcripts indicate German injunction courts believe CRMD’s patent appears to have been mistakenly granted based on outdated “prior art” concepts now viewed as doubtful, making CRMD’s patent “not valid”. While this lawsuit will likely drag on for years before CRMD loses, these direct German court transcripts seem to me contradictory to the message given by CRMD and in my view make future CRMD patent failure inevitable.

Now, CRMD seems to have “pulled out all the stops” with paid stock promotion and endlessly touting misleading clinical data along with a (NYSE:NOW) failed company strategic review process retail shareholders mistakenly believe will result in company sale. As a result, CRMD stock has become temporarily pumped to an unsustainable $224m+ valuation as CRMD has “seized the moment” to dump millions of dollars in stock while apparently specifically targeting the most unsophisticated retail shareholders possible.

Using the most optimistic Neutrolin estimates possible AND assuming CRMD management are honest, CRMD fair value is a maximum of $0.44 per share for -91.04% near term downside, with most of that value made up from the cash CRMD just raised, which insiders will likely burn and pay out as excessive compensation. I expect as CRMD burns through their cash they will go bankrupt (again). Insider and company stock sales further support this view.

With CRMD stock imploding as this failure continues to unravel, I think it is an opportune time to review what happened and how this was an easily preventable financial disaster for so many retail share (bag) holders. CorMedix is a stock I have been involved with for a while now and my hope is to use this report as an “Op Ed” template to help explain to retail shareholders how to avoid getting bagged in the future in worthless biotech shells of insider enrichment. For many shareholders, it is already too late to avoid capital losses in CRMD, but you can cut your losses short and learn from your mistakes by reading the rest of this report.

As a result this report is unusually long. I encourage you to pour a tall glass of gin and focus though, as what you read will shock you.

CorMedix History: Failed Company Sale Attempts, Bankruptcy and Repeated Wrong Press Releases

In order to truly understand what is going on behind the scenes at CRMD, historical context is critical and I highly recommend you at least read this article for interesting background. CorMedix ’s sole product Neutrolin is a simple mix of old compounds which CRMD claims can be injected into a catheter to try and treat infections in a procedure known as “Catheter Lock”. Catheter Lock protocol is where a dialysis catheter is closed on each end and filled with an intense cleaning solution to address infection risk. The only chemical CRMD has any unique claim to is a compound called Taurolidine which is a Taurine amino acid derivative originally discovered and experimented with back in the 1970s which, similar to aspartame, seems to metabolizes into formaldehyde. After apparently failing on all their other prospects, CRMD was left primarily with this Neutrolin/Taurolidine product.

CRMD was originally known as Biolink, supported by Spinnaker Capital LLC, and truly began back in 2001 when the first IDE (#G0102000) for Neutrolin was filed and approved with the FDA. At that time Fresenius put up $1.5m to help fund Neutrolin and Fresenius had the option to buy CRMD/Neutrolin for US and Canada for $80m, an option which was never exercised.

However, all that apparently failed swiftly as CRMD went bankrupt in 2003. Prior to formally filing bankruptcy it is typical for a company to try and sell itself in order to avoid seeing the business cease to exist. We can deduce presumably this first sale process failed and that likely CRMD was put up for sale to not only Fresenius but also Fresenius’s competitors in order to try and force Fresenius hand and avoid getting wiped out. Tellingly, no buyers of any kind stepped in to avert bankruptcy.

Once in bankruptcy, CorMedix was put up to auction. Remember Fresenius already had involvement with CRMD and knew it well. Pharma/Biotech is an intensely competitive and public space so I would be shocked if other global dialysis companies competing with Fresenius weren’t aware of CRMD’s bankruptcy auction as well.

Question: If the CRMD asset had any value, why wouldn’t a competitor try to steal it away from Fresenius out of bankruptcy? Why wouldn’t Fresnius buy it? The questions answer themselves, in my view.

In the end, the only one willing to own CorMedix/Neutrolin was an affiliate of current investors that were still owed $941k from CRMD: Spinnaker Capital. They were allowed to “credit bid” their $941k debt and put up ~$1m in cash to own CRMD outright. In these same bankruptcy documents we learn Fresenius bid as well but was not the winning bid, indicating Fresenius put in a bid lower than Spinnaker Capital’s $1-1.9m bid. When the only people interested in owning your failed and bankrupt company are the current investors throwing good money after bad, that seems like an obvious failure.

I believe the catheter industry has spoken and the verdict is clear: CorMedix is worth, at most, $1.9m, which is ~$0.06 per share.

The failed company seems to have languished dormant for years until 2008 when Spinnaker Capital have formed “ND Partners LLC”,apparently run out of an apartment in Boston.

Neutrolin Owner “ND Partners” HQ Is a Boston Apartment?

Google Earth

They then took ND Partners and joined forces with notorious biotech wipeout master Lindsay Rosenwald to “re-boot” this failed company into a public company shell. ND Partners received $325k and some stock and Rosenwald took a huge piece of the company through a brutal convertible debt offering.

Even back in 2008, CorMedix was touting they would enter their pivotal trial “soon” and with a product on the market in 2011 or sooner. In line with CRMD’s years of failure though, apparently no credible private healthcare investors would fund this thing and the latest investors also presumably couldn’t sell the company outright for a profit, so no trials ever happened. Instead CorMedix decided the best way to get money would be to raise it in America’s public markets with a largely retail shareholder base. The shareholder base remains largely confused and uninformed retail investors who I believe are falling victim to this mess.

Who will financially “prime the process” on this worthless failure? Who will step into promote this worthless shell where insiders get rich? How will insiders salvage their broken investment no one else wanted to buy out of bankruptcy court? Read on!

So with Rosenwald’s help as escrow agent and financial partner, CRMD went to the public markets in 2011 with the story now that their pivotal study would start in 2011 and Neutrolin would be on the market in 2013 while CorMedix would file their IND with the FDA (sound familiar?). This hopeless team somehow managed to raise $12.5m on the back of this story and the claim their imminent Phase3 trial would cost just $10m, which they claimed they had cash for. They also claimed European revenues would be coming in 2011 time frame. None of this seems to have happened and CRMD kept the money.

CRMD’s Lindsay Rosenwald: Involved in Multiple Fraud Lawsuits, Master of Biotech Wipeout

Lindsay Rosenwald: Biotech Wipeout Artist – pic credit Rosenwald

You can read on your own all about Lindsay who I think is perhaps the most impressive Master of Biotech Wipeout in the entire stock market. Basic google research will help you find interesting background about Rosenwald and his ties to DH Blair, indicted on 173 counts and described as “massive scheme of securities fraud”, or the apparent jail time and probation of associates with securities issues, or just the uncanny “pattern” of basically everything he touches to get wiped out, over and over again. You may also find it interesting to read up on the multiple biotech disasters he has been involved in that “coincidentally” get sued for fraud, like Interneuron or Ventrus (where Elliot got wiped out too).

The Rosenwald Pattern, as it is known in the biotech investment community, seems pretty simple and recurring to me. Take a financially unviable, apparently failed compound acquired for nearly free, which may be selling minimal amounts in some foreign market (or not), then promote it, typically with lots of unsophisticated retail investors, then collect huge compensation or sell stock before the stock price implodes. Rinse, wash, repeat until you’re filthy rich with a $90m NYC penthouse. What do non-insider shareholders get? Brutal wipeouts.

Invest in Rosenwald biotechs and this could be you!

Picture credit

Now that we understand CRMD is another re-booted public shell making Rosenwald and insiders rich, how do these Rosenwald disasters typically end?

The Amarin (AMRN) “Fish Oil Wipeout”: Sued For Fraud Allegations

(click to enlarge)

Fortress Biotech (NASDAQ:FBIO)

(click to enlarge)

Avax Technologies

(click to enlarge)

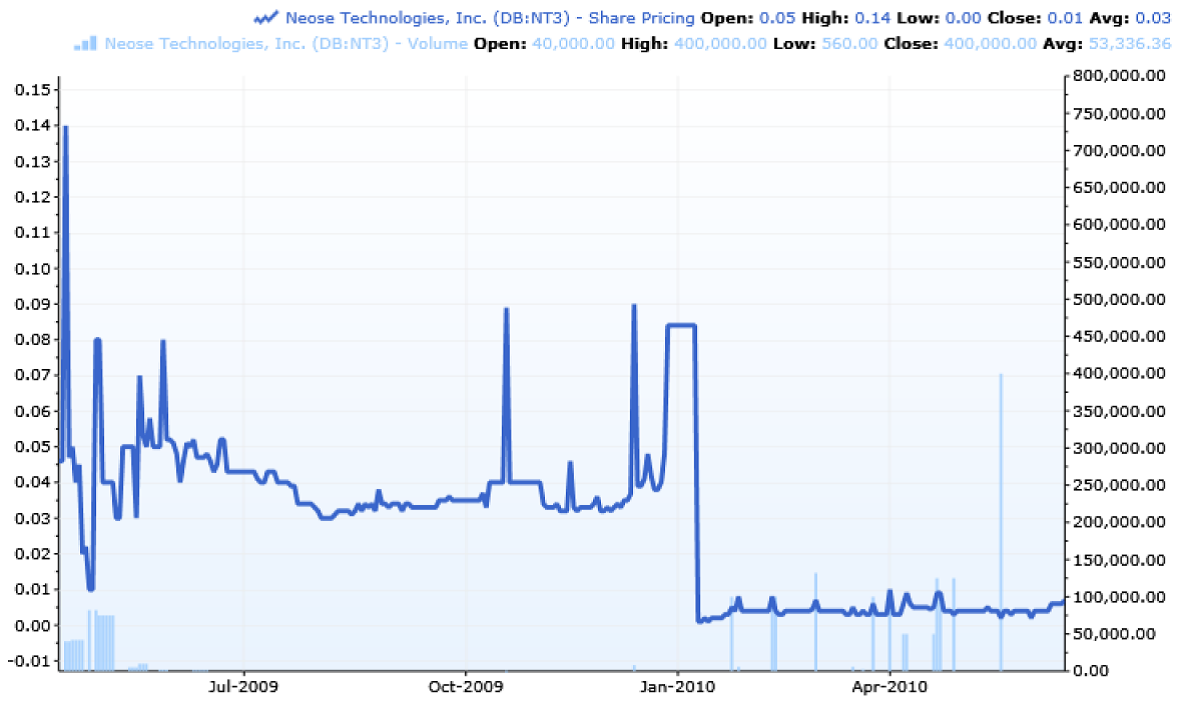

Neose Technologies

(click to enlarge)

Assembley Biosciences (NASDAQ:ASMB)

(click to enlarge)

Genta Incorporated: Sued for “false and misleading statements that had the effect of artificially inflating the market price of company’s securities” and went bankrupt.

(click to enlarge)

All charts from CapIQ

CRMD Partner With John Carris: Expelled by FINRA for Fraud Charges Involving a Gun & Tattoo Shopping Spree with Stock Manipulation

In 2012 CRMD was facing bankruptcy again with the stock decaying near $0.14 per share and CRMD’s total valuation of ~$25m. Again, where are the real healthcare investors? Where are the legitimate healthcare companies who have known about Taurolidine/Neutrolin since the 1970s?

Pic credit to John Carris

Instead of choosing to work with anyone credible, CRMD partnered with“John Carris Investments”. John Carris was charged with fraud by FINRA and later expelled from the investment industry. John Carris CEO George Carris allegedly issued false documents, when in fact $600k was spent by CEO George Carris on a massive shopping spree of guns, motorcycle gear and tattoos. Among many issues, FINRA also alleged Carris fraudulently sold stock and manipulated stock through strange pre-arranged trading and block orders.

What kind of company chooses to partner with people like this?

CorMedix’s 10+ Year Graveyard of Broken Promises

This is not the first time CorMedix has announced partnership discussions and imminent Phase3 trials, as it seems to me CRMD has 8-10+ straight years of breaking their own promises. I don’t have enough time to go through all of CRMD’s moved goalposts and broken promises as that would likely take months or years but to look at a few “interesting” recent examples we can note CorMedix has been touting “discussions underway with global pharmaceutical and medical device companies” for the last 18 months straight. When CRMD again raised money in 2013 they stated:

“we expect that our cash position is sufficient to reach profitability…we would be able to be at an operating break-even run rate by the end of 2014… we certainly have the flexibility to get to where we want to be without having to raise any additional capital”

At the time CRMD was guiding investors to a strong European launch given their years of effort and strong marketing push there, but of course all of this turned out to be wrong. CRMD also has been stating since at least 2013 they planned to partner in the US. If nobody will partner with CRMD who will possibly want to own this previously bankrupt failure?

CRMD has been guiding to imminent phase3 trial with near term market launch since 2008 also. The company rehashed this tired promise again in 2010 and is still using this tired story in 2013 until today. In 2014 CRMD stated:

“want a Phase III program before the end of the year… be ready to launch in the U.S. either later 2016 or early 2017?

Yet again though the goal posts are moved and presumably after partnership discussion failure, CRMD drops the early 2014 bomb of:

“we may decide to establish our own commercial organization in the United States….We have ongoing discussions with a number of companies….we think that the negotiations with some of these companies will accelerate”

Or how about telling investors on the Q2 2014 call:

“Starting the trial in or before the first quarter 2015….the level of interest increased I would say maybe dramatically….We’re talking to companies that both on the pharma side and the device side.”

Or the tired story from just 6 months ago of CorMedix having enough cash:

“we believe that our cash resources as of December 31, 2014 will be sufficient to enable us to fund our projected operating requirements into the third quarter of 2015?

And just on the Q1 2015 call:

“John Marcel – XG Capital: A follow up question. Do you expect to register more shares in the coming six months?Randy Milby – CEO At this point, no”

Which we know is wrong given CorMedix is siphoning millions of dollars of cash out of retail shareholders accounts via their ATM. From what I can tell it seems CRMD has basically done nothing but tell stories, break investor promises, and raise tens of millions of dollars largely from retail investors. How can you possibly trust anything these people say?

Just Stop Already CRMD

Picture of me credit to me

We know multiple global catheter companies have shown no interest in Neutrolin despite established relationships. We know CRMD has repeatedly partnered with people sued for fraud and we know CorMedix seems to endlessly postpone ever actually running their study to get Neutrolin on the market, even when CRMD has plenty of cash. If CRMD and Neutrolin were really an amazing opportunity, how can all of these things possibly be true? Why has CRMD been postponing the study endlessly for 7 years (for now, next year it will probably be 8 years!)? Why can’t CRMD find any credible partners? Why won’t they just hire a dang CRO and get this study done? How could this many broken promises and failures possibly be a coincidence?

We know if CRMD’s Taurolidine/Neutrolin truly had gazillion dollar market potential, then catheter giant Gambro would never have dropped it as they did with Geistlich manufactured “TauroSept” (2% Taurolidine blend) in Europe a few years back and instead offers coated catheters now. Fresenius had a partnership with CRMD as far back as 2003 and could have purchased CorMedix outright for <$2m but chose not to. Tauropharm has been selling a product identical to Neutrolin in Europe since at least 2003 and yet Tauropharm has never been acquired by a big dialysis company and flounders along as a tiny failure? Doctors have been experimenting with Taurolidine flushes for at least ~15 years and yet it has never caught on, why?

Obviously Gambro, Fresenius and these global dialysis companies know more about catheter issues and CRBIs then CRMD ever will (or you or me). So why have global dialysis companies deemed CRMD’s product worthless? How is this possible when CorMedix management told you it’s worth gazillion dollars?!? Let me explain…

Why CRMD’s Product Is Financially Unviable and Worthless

Unfortunately most retail investors don’t have the resources, tools and experience to properly evaluate most biotech/pharma companies and instead rely on message board touts (who in my view are likely dumping their stock given CorMedix stock price implosion) along with company management, which as we see above has been disastrous. As you see what the research actually shows I think you will begin to comprehend what CRMD’s true purpose is and what is going on with your money.

CRMD Claims to Address an Issue That Already Has Countless, Effective and Cheap Solutions in Use

Unsophisticated CorMedix shareholders mistakenly believe “There is nothing on the US market that addresses this grave problem” when in fact catheters have been in use for over 100 years, and infections have always been an issue the medical community has addressed. To think doctors around the world have just been sitting by idly while their patients die for 100+ years is obviously absurd.

The truth is there are literally countless solutions put in practice as standard protocol at hospitals around the world. These solutions are effective, easy to administer, safe and use a combination of common generic drugs that are so cheap as to be essentially free. Among these solutions are BOTH antibiotic and many non-antibiotic compounds proven to be effective and cheap. These are all recommended by CDC and other recognized disease protocol experts, and have been used effectively for many decades.

CRBIs Already Addressed With Dozens of Industry Protocols Effectively Deployed for Decades

Straight Heparin is not the standard protocol for infection prevention in catheter locks as antibiotic and anti-microbial locks are the recommended protocol and have been for decades. Don’t believe me? Ask the CD, ISDA and other protocol establishing medical foundations:

“Clinical practice guidelines recommend antibiotic lock therapy(NYSEARCA:ALT) for both prevention and treatment of catheter-related infections (NYSE:CRI)”

“Guidelines from the Infectious Diseases Society of America (NASDAQ:IDSA) for the diagnosis and management of CRIrecommend antibiotic locks “

“CVC removal remains first-line therapy for management of CRI, especially in cases of Staphylococcus aureus and resistant gram-negative pathogens, including Pseudomonas aeruginosa. “

The reason for this is that a simple and virtually free Gentamicin flush reduces infections by 92%, which is actually more than some of CorMedix ’s efficacy claims.

Pic credit

Despite what CRMD may claim, there are dozens of antibiotics hospitals have at their disposal should any one infection build resistance to any other antibiotic. This is why they these protocols have been effectively used for countless decades on tens of millions of people globally. Including aminoglycosides, beta-lactams, fluoroquinolones, folate antagonists, glycopeptides, glycylcyclines, lipopeptides, oxazolidinones, polymyxins, and tetracyclines, ethyledenediaminetetraacetic acid, citrate, isopropyl alcohol, hci acid, urokinase and countless other catheter lock protocols. To claim there is no solution available for CRBI is beyond absurd and even just 1 minute of google research proves that.

Clinical Studies Show CRMD Product Offers No Benefit vs. Current Industry Protocols

Unfortunately for CorMedix clinical studies show Taurolidine catheter locks are just not more effective than what is currently being used while both obviously show benefits vs heparin placebo:

“Gentamicin/heparin and taurolidine/citrate, used for locking UC, were similarly effective at preventing CRB and catheter thrombosis for up to 3 months, until a functional permanent vascular access became available. Both antimicrobial lock solutions were superior to heparin in CRB prevention with similar thrombosis rates.”

When CRMD’s Neutrolin is compared against the current industry standard it seems to obviously offer no benefit. Furthermore, there are special products which hospitals have had for years to address any unusual infection they come across:

“Several agents that may be used for resistant gram-positive infections including daptomycin, linezolid, and tigecycline have been studied”

If you still want to buy CorMedix, I have some magic beans to sell you (which haven’t gone bankrupt or partnered with fraudsters)

CRMD’s Misleading Neutrolin Presentations

As you now know, a simple heparin catheter lock is NOT the standard for infection treatment and CRMD’s comparison and proposed Phase3 trial against this irrelevant benchmark seems very misleading to me. In fact, multiple medical studies show Taurolidine lock is functionally identical to the currently established protocol and is absolutely NOT “40% better!” than what is currently in use. In light of the above, CRMD’s direct statement of “no approved catheter lock solution” seems blatantly incorrect to me. If CRMD’s Phase3 trial was properly constructed and CRMD forced to compare their worthless Taurolidine solution against what doctors actually use for catheter infections, medical studies show there would be essentially no advantage and CorMedix would fail.

First of all Heparin has no antimicrobial or anti-infection prevention, so using that as the baseline is like comparing Neutrolin to a placebo. With cancer trials we don’t test oncology products against Skittles or water, so why does that make sense here? Even more upsetting, putting trial patients at unnecessary risk of death when the opposing study arm should be receiving industry standard infection protocols seems irresponsible and dangerous in my view.

Pic credit to Cormedix

Since we know Heparin is NOT the industry standard for catheter infections, why would CRMD use these misleading presentation slides when pitching their stock to retail investors?

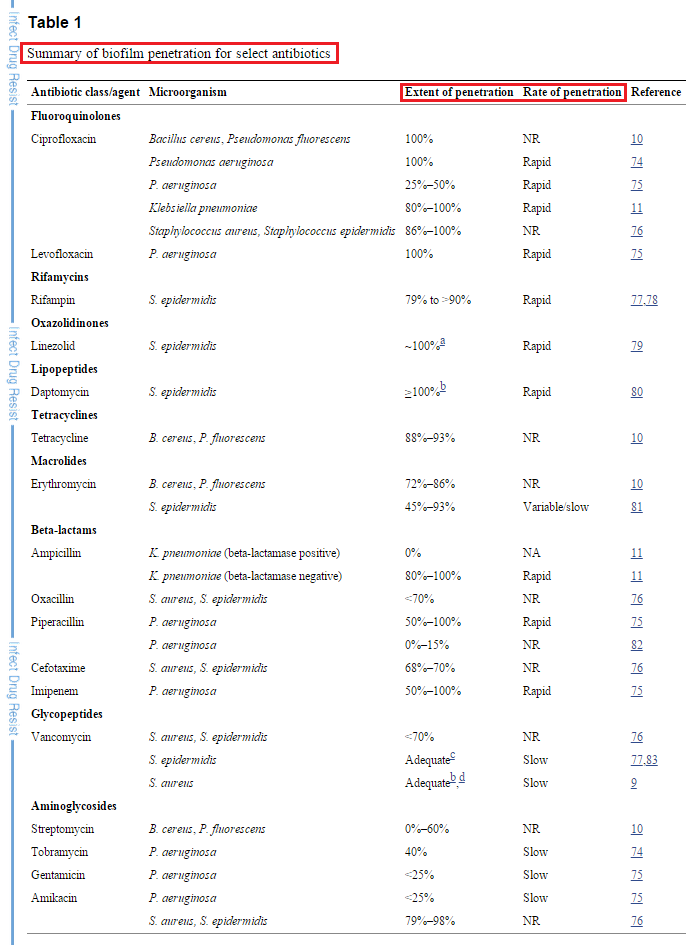

Current Catheter Lock Protocols Penetrate Biofilms “Rapidly” and “Completely”

The other bull case for CorMedix revolving around biofilms is equally absurd as the current, nearly-free and commonly used protocols already address this as well. As you can see below there are many compounds which rapidly penetrate biofilms by 100%, and this list is not even close to inclusive and also doesn’t even list the multitude of non-antibiotic protocols in use today.

(click to enlarge)

Picture credit

It’s not just the standard anti-biotics in use though that penetrate biofilms effectively as there is a multitude of other non-antibioticprotocols already in use for years which effectively deal with biofilms and simultaneously offer synergistic effects with the current antibiotic protocols as well:

“The antimicrobial effect of potential additives, such as ion chelators like ethylenediaminetetraacetic acid (OTCPK:EDTA) and citrate, should also be considered. Such agents have been shown to disrupt biofilm and exhibit synergistic activity with antibiotics.12,13“

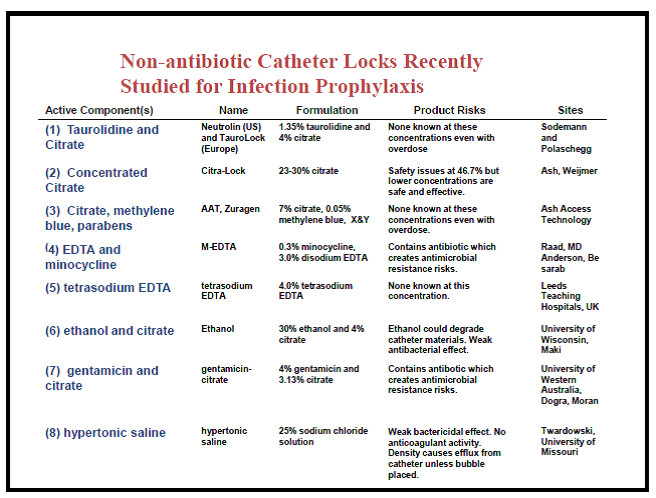

Many Cheap Non-Antibiotic Solutions are Superior to CorMedix as Well

CorMedix touts claim Neutrolin is unique in that it’s not an antibiotic but there are already many cheap non-antibiotic catheter lock protocols being used around the world that Neutrolin cannot compete with. This old list below is far from inclusive but is provided as example with sites listed so you can call these places and verify what I am saying.

(click to enlarge)

Pic credit

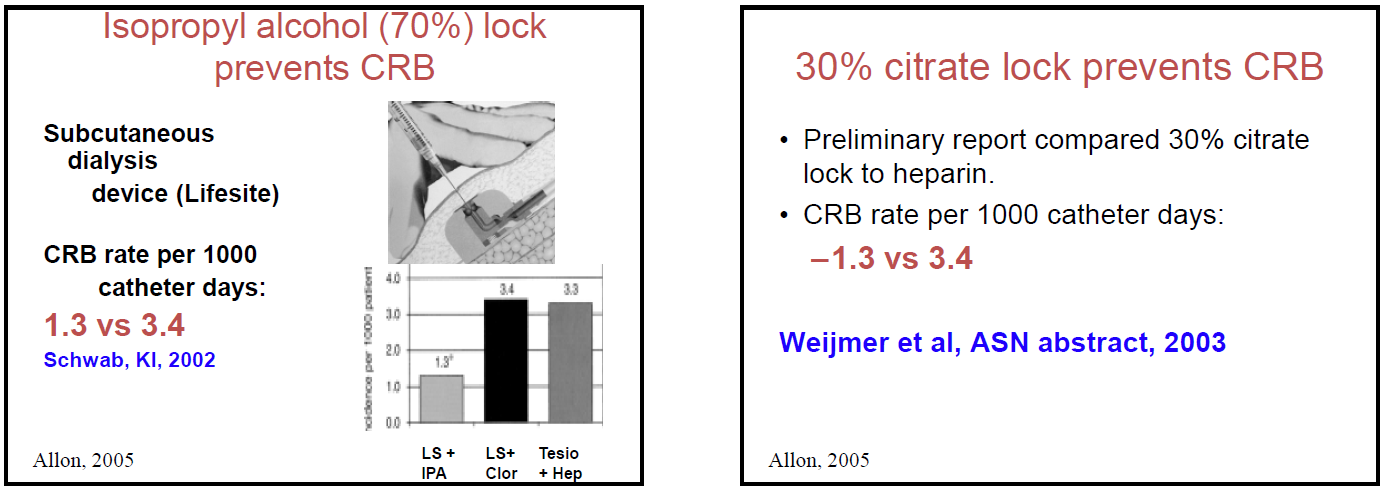

To expand on this, we can see this study found 1.1 infection episodes per 1000 catheter days and furthermore, generic Citrate alone or even simple Isopropyl alcohol locks cause 62% reduction in CRB rate vs. heparin. Based on this, it seems a simple iso-alcohol lock is similarly effective as CRMD’s claims!

(click to enlarge)

Pic credit

Or here where a simple 25% ethanol lock solution alone ELIMINATED CVC issues in this setting

(click to enlarge)

Pic credit

Pic credit

Some doctors even advocate a simply Hydrocholric acid lock as well, which is virtually free and:

“significantly reduced the need to remove and replace CVCs. The procedure is practical, appears to be safe, and may reduce the consumption of antibiotics”

While this very simple non-antibiotic also alternatively generated 70.7% lower catheter infection rates over a study including ~50k catheter days.

Clinical Studies on Taurolidine/Neutrolin Seemingly Contradict CRMD’s Efficacy Claims

To pretend medical consensus on Taurolidine is unanimous is misleading also. There are multiple clinical trials and medical though leaders who consider use of Taurolidine to be controversial and not beneficial. This adds an additional layer of risk and I believe is another reason, despite being around for 40 years, Taurolidine has never gained acceptance.

CRMD’s Product Metabolizes into Formaldehyde: Where are CorMedix’s Carcinogen Studies?

Leakage of catheter lock solution into the blood stream is inevitable. Considering this and the fact Taurolidine metabolizes into formaldehyde, why is CRMD not proposing Taurolidine carcinogen studies? The FDA has much higher standards than Europe and this whole fiasco reminds me of the Zuragen catheter lock failure, which initially showed compelling efficacy data before failing miserably.

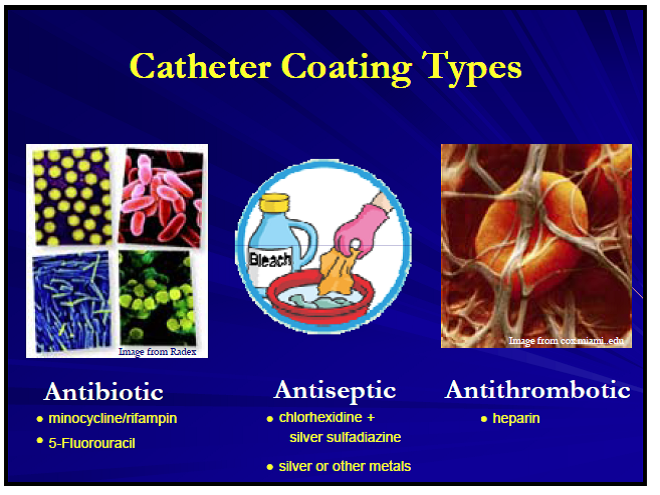

Catheter Lock To Become Obsolete Anyway; Coated Catheters the Future: Render CorMedix Obsolete Unfortunately these perpetual failure biotechs that never advance to trials (such as Provectus (PVCT)) frequently see their ancient compounds rendered obsolete by the rapid pace of innovation that occurs in real biotech and pharma companies. If you talk to anyone who works deeply in the catheter business they’ll all tell you the same thing: coated catheters are the future for infection and biofilm elimination when the situation justifies an increased cost over current protocol.

Technologies relentlessly evolving include anti-microbial coatings, antiseptic impregnations, ultrasmooth nano tech coatings, and pharma/biotech solutions.

(click to enlarge)

Pic credits

Biofilm and infection is not an unusual complication in medicine and the industry has innovated solutions for this in everything from stents, to pacemakers to contact lenses.

If you don’t believe me, simply look at all the patents recently filed relating to coated, and anti-microbial coatings, for catheters or the dozens of products already on the market addressing these issues. The current innovation in medical coatings is impressive and owning CRMD is inherently a huge bet that the relentless evolution of medical device coatings will never succeed: if you own CorMedix, you are implicitly short medical progress.

Pic credit

All of these trends make CorMedix a long-term zero even if you somehow think their product has value today. This is likely why dialysis giant Gambro dropped Taurolidine years ago but offers coated infection prevention catheters today. Owning CRMD is effectively a bet against nanotechnology and innovative coating technologies in healthcare, which is obviously a bad bet to make.

Neutrolin not even Vaguely Cost Effective vs. Currently Established Medical Protocols

Probably the most important reason CRMD’s old Taurolidine compound is not viable is because it will just never be cost competitive against what doctors are already using. Even if CorMedix somehow avoided bankruptcy, made it through all regulatory hurdles and was on the market, it would still be totally financially unviable and worthless.

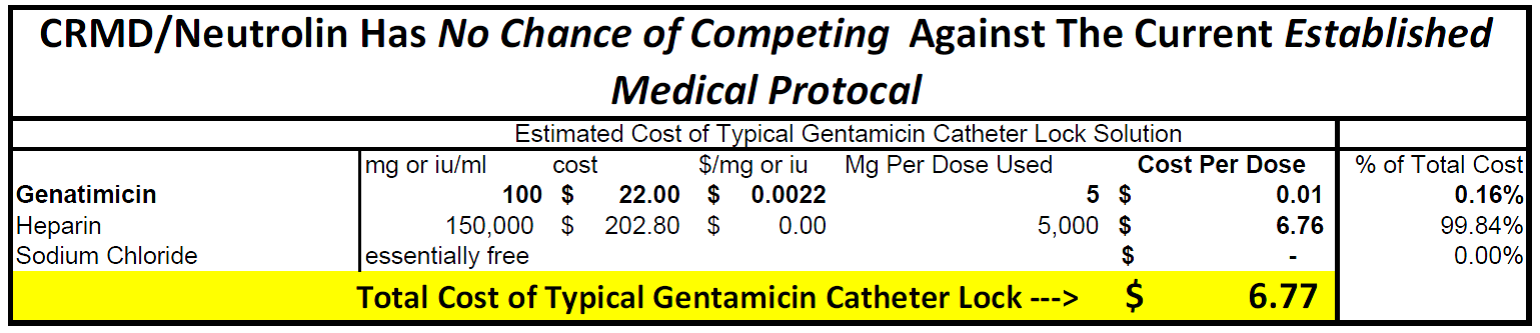

For example, a typical catheter lock solution will use 0.5ml of 20mg/ml Gentamicin, 5,000iu of Heparin and some sodium chloride (saline water). Gentamicin has been generic forever and so a typical 100mg/ml, 100ml bottle costs just ~$20. If you add up these ingredients you can see the typical catheter lock protocol costs a maximum of $6-7 and most likely much less.

(click to enlarge)

The numbers I’ve used here assume both unusually high heparin dosage and zero bulk purchase discount as well, which any hospital will certainly have. As evidence of the true cost of your average catheter lock infection prevention protocol check this Middle East quote stating $2.50 per lock is typical.

(click to enlarge)

Middle East dialysis presentation

All the ridiculous Roth, Griffin, etc. models using a $20-30+ price per lock application cost are clearly absurd and I think there is no chance CRMD could ever make any profit at these prices. The currently established medical protocols used generic compounds that are so cheap as to be essentially free and the bulk of the current cost is in the Heparin anyway, which CRMD’s Neutrolin has and therefore has no advantage. There is just no chance Taurolidine with all its risks, doctor perceived uncertainty and cost can ever hope to compete with what Doctors are currently doing when it is infinitely more expensive. Remember from above Taurolidine locks show are “similarly effective” at best to current protocols. To convince a cash strapped hospital or health insurance provider they need to increase their cost by 10,000% to solve a problem they already have countless solutions for is obviously unviable. In fact, it’s laughable.

CRMD Phase3 Trial: Far From Assured

Another demonstrably false claim by CorMedix touts is that somehow CRMD’s phase3 trial is a “sure thing”. As we have seen above, when CRMD Neutrolin is compared against current industry standard, it is demonstrably not superior as the medical community has already made these comparisons over decades. We also know CRMD does not appear to be proposing any carcinogen studies despite that known concern. There are countless drugs in use in Europe that are not allowed in the US and simply extrapolating European usage to mean US success is assured is clearly ridiculous.

I think all of the above along with the phase3 trial is why Elliot is desperately trying to jettison this failed investment now before the phase3 trial or product market failure become undeniable, otherwise why not wait for the theoretically huge upside? Clearly this question answers itself.

CRMD Market Claims Far Overstated: German Corporate Records Show Tauropharm ~$1.3m Business

Tauropharm was spun out of CorMedix predecessor Biolink and has been selling a product functionally identical to CRMD’s Neutrolin for 12 years into international markets. Tauropharm offers four Taurolidine products in the European market: two without Heparin and then in 2007 Tauropharm launched two more products with Heparin since some customers were adding their own Heparin independently.

Pic credit Tauropharm

Due to essentially identical products, we can use Tauropharm for a useful proxy for Taurolidine/CRMD’s International market opportunity. Furthermore, since CRMD has said the two markets are is similar in size, we can also use Tauropharm as an indication of how Neutrolin would do in the US. As you can see below Tauropharm is a tiny company and basically a failure despite a 15 year head start.

With so many questions about the size of the European markets and Tauropharm you’d think someone would just go and pull Tauropharm’s German corporate records, which is cheap and easy (it took me less than 30 minutes to cheaply find it here ). I did this and am happy to share the results with you to help you understand why CRMD repeatedly refuses to provide any discussion of Tauropharm’s financials on CorMedix investor calls: Because the results are abysmal.

Tauropharm has <10 employees (I estimate 3) and has been around for 15 years, yet their CUMULATIVE earnings are just ~$3.61m euros. That is not a typo.

(click to enlarge)

From German Corporate Records

2012 was a record year for Tauropharm, which took over a decade to build to, and yet Tauropharm generated <1m euro, while the previous year they made 57,000 euro (no, I didn’t forget any zeros)

From German Corporate Records

We can also look at Tauropharm’s balance sheet and see they are a tiny business. We know Tauropharm is the manufacturer of Taurolock bulk product and yet we see they have a tiny balance sheet with total working capital of <4m Euro. Not only that but we can see from the working capital line that Tauropharm’s business is, at best, flat lining but likely shrinking.

From German Corporate Records

Using typical pharma manufacturing balance sheet metrics from peer companies we can further corroborate what Tauropharm’s estimated annual revenue is as well. Ranbaxy for instance manufactures bulk pharma products and they carry ~258 days of inventory on hand. Mylan is more efficient and carries 160 days of inventory. If we just average the two of these since Tauropharm is small and likely not extremely efficient, we estimate Tauropharm carries 209 days of inventory.

(click to enlarge)

With the above balance sheet data we see Tauropharm has ~1.3m Euro of Inventory in 2013. With 209 days of inventory on hand that could only support ~2.3m Euros of revenue for that year. If we consider Tauropharm probably has ~40% gross margins (at best), with some opex and salary for their 3-4 employees that also roughly triangulates to the income statement numbers we have above.

Any way you cut it, despite 15 years of effort, Tauropharm isn’t a success. You should also note CRMD claims, in a best case outcome, it would only have a Maximum of 10 years of market exclusivity in the US so CorMedix’s results would likely be far weaker than what Taurpharm has experienced. If that is what CRMD bulls are hanging their hats on, they are severely mistaken.

Lastly, there is free Tauropharm data online regarding the size of their business. While the free data isn’t as precise, it clearly shows you Tauropharm is closer to 1-2m EUR per year.

Pic credit

Through four different analysis we repeatedly arrive at a <$4m per year business after ~15 years of effort and with four different products. I would also note that Tauropharm has been in the Middle East since at least 2007 so any CRMD touts claiming the Middle East will be a huge market for CRMD are clearly incorrect.

The reason for CorMedix and Tauropharm’s failure with Taurolidine catheter locks in Europe is that the European market is very similar to the US in that there are already countless proven solutions which are nearly free. Here we can see a German medical handbook outlining effective catheter lock solutions from as far back as 2004.

from this book

Germany is also perhaps one of the most cost conscious and efficient developed healthcare markets in the world. If Taurolidine was some miracle product with a compelling value proposition, it would not be failing there after 15 years of sales and marketing efforts generating just $3.5m cumulative of earnings. Given what we now know, how could the following CRMD management quote possibly be presentable?

“The potential market for Neutrolin, we stated it’s $500 million. It’s almost evenly split between the U.S. and EU.”

I also find it concerning CorMedix management has also repeatedly refused to provide any color on the possible size of Tauropharm on the investor calls. These records are easily available so I only see two possibilities here:

- Is CRMD management ignorant and incompetent so their “guidance” should be disregarded?

- Is CRMD management dishonest and self-enriching so their “guidance” should be disregarded?

CRMD International Launch Also a Failure

We don’t need to look at Tauropharm though, we can see from CRMD’s international market Neutrolin failure that Neutrolin/Taurolidine is just not financially viable. CRMD has now been selling Neutrolin in the international markets for 18 months including Italy, Malta, Austria, the Netherlands and other markets.

Despite “strong pre-commercial marketing efforts” CorMedix has failed miserably and while coming up on 2 years since launch, CRMD revenue last quarter was a measly $31k as losses actually accelerated badly. If this market were large and viable I think it is obvious CRMD would not be failing miserably across multiple countries and multiple sales forces with their “new! Amazing!” product.

Given everything we just learned I am not surprised CRMD is apparently not in a hurry to put their product on the market in the US. If they ever do put the product on the US market, it seems obvious that it would fail very badly very quickly. If the CorMedix “story” imploded, what would that mean for the “gravy train” of high insider compensation coupled with significant insider selling? Most likely the company would declare bankruptcy again and they’d all lose their jobs.

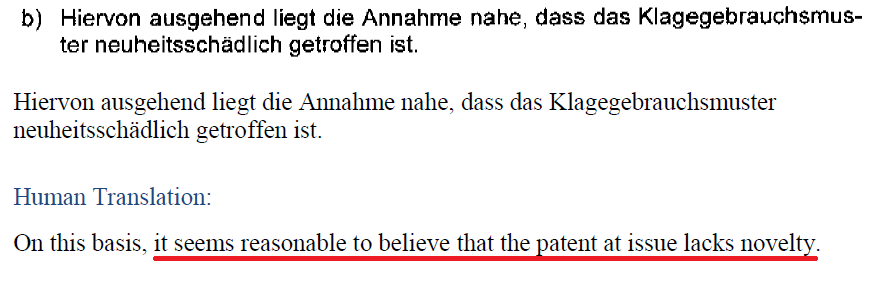

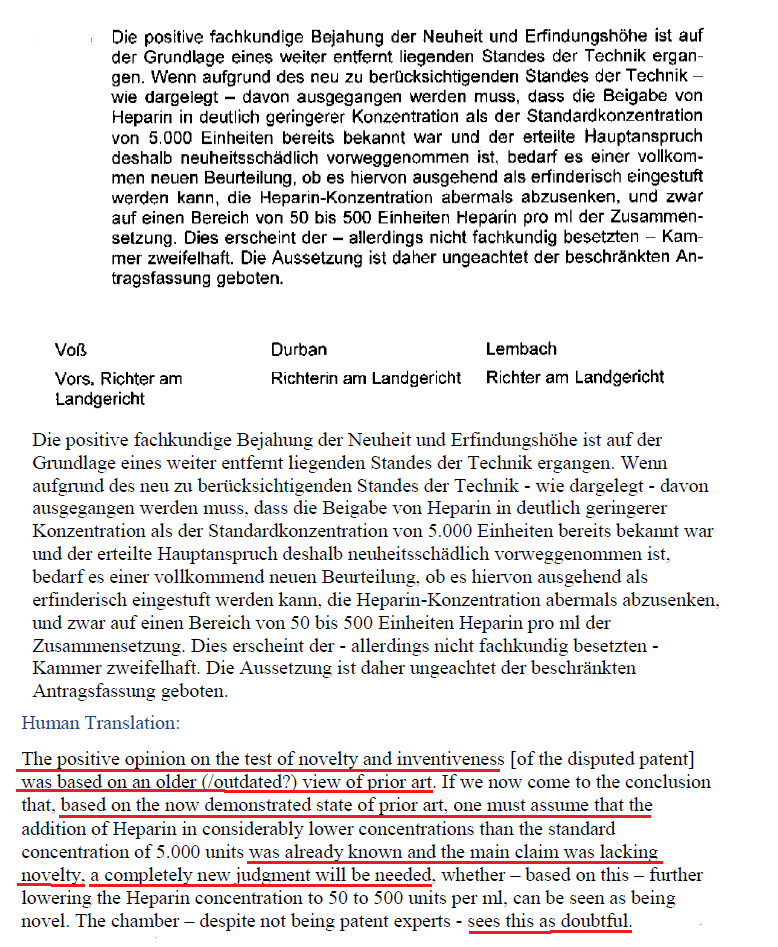

CRMD’s Recent German Patent Failure

I think it is clear when dealing with teams of people like CRMD insiders you, to put it nicely, should be skeptical. With that in mind I got the German legal transcript and it seems to bring up some very “questionable disclosure issues” I believe CRMD management need to address immediately as the German courts have spoken loud and clear and anyone can get these transcripts cheaply with a German lawyer.

I will share with you my own best-effort translations of some choice quotes but I strongly encourage you to go get and translate this whole transcript for yourself because it’s a doozy.

For background, CRMD recently sued Tauropharm over a new patent CorMedix filed regarding CRMD’s claims they over the addition of Heparin to a Catheter Lock, despite Tauropharm selling these products since 2003 without previous complaint. Now this is being decided across the German courts where CRMD will try and legally outspend a company that actually has profits and without CRMD’s egregious insider compensation costs. The latest German court decision to go against CRMD is in regards to CRMD’s overly aggressive claim of an injunction against Tauropharm.

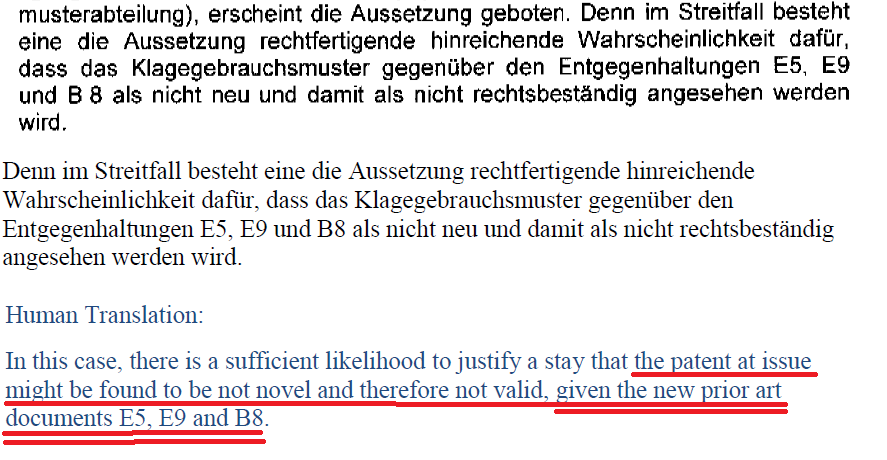

In response to this, the German court analyzed CRMD’s ridiculous patent to see if it was novel enough to merit ruling that Tauropharm was in violation and should be stopped. The German courts clearly ruled NO and the language they provided, which will surely be read and understood by the patent courts, seems loud and clear.

I’ll remind you CRMD management did not seem to me to properly disclose this initially, instead CorMedix seems to have filed the bare minimum 8k SEC filing as required by law, then forced CRMD shareholders to dial into a conference call. Even then it appears to me this issue was not fully disclosed in depth, so let me set the record straight.

I believe what you will find is this document clearly shows CRMD claim to any unique patentable product is a lost cause and waste of shareholder money.

(click to enlarge)

(click to enlarge)

(click to enlarge)

(go hire a German lawyer to verify these if you don’t believe me)

Clearly this whole patent debacle is desperate and absurd. CRMD never mentioned any IP infringement in any of their IPO documents and Tauropharm has been openly selling Taurolock since 2003. Why the sudden lawsuit claims if not to temporarily prop up CRMD stock? Is this just another “story” designed to support the stock price for the benefit of insiders?

Just looking at this patent mess and using common sense will help you. CRMD came out of nowhere and sued a German company, in Germany, for a product on sale for over 12 years, based on a recent patent focused on the addition of simple Heparin to a catheter lock. Everyone knows Heparin in catheter lock is essentially required and has been part of the standard protocol for decades, clearly the addition of Heparin in various dosages is not novel. This would be analogous to me filing a patent regarding water in KoolAid and then suing KoolAid co. Obviously adding water to KoolAid and Heparin to a catheter lock is not a novel concept.

Either way, this lawsuit is probably going to drag on for countless years and cost CorMedix many millions more. What seems clear is any CRMD touts claiming big payments from Tauropharm are misguided. More likely this gamble will backfire in CRMD’s face and I believe CRMD could very well eventually be liable for Tauropharm’s legal bills (and go bankrupt as a result?), as Germany is nowhere near as tolerant towards frivolous lawsuits as America.

If CRMD is obviously such a failure then what are CRMD insiders really doing with this worthless Product? What are they honestly doing with this failed public company shell?

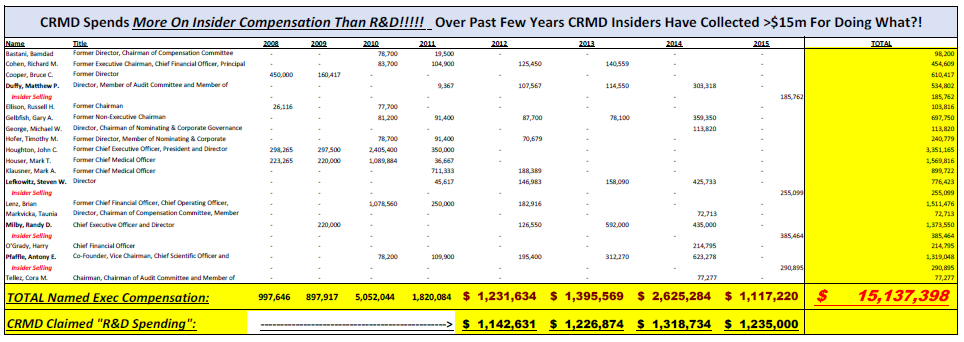

CRMD’s Public “Bagholder Machine”: CorMedix Insiders Pay Themselves More Than Is Spent on R&D!!!

(click to enlarge)

Chart built by me with public information from CapIQ

Just the ~5 named executives alone have removed over $15m in shareholder value from this shell over the past few years while, best I can tell, doing nothing but failing and endlessly publishing wildly promotional press releases which later turn out to be wrong. Even more offensive, over the past few years CRMD insider compensation has actually accelerated to the point CorMedix insiders are now siphoning off more money for themselves than they even spend on R&D!

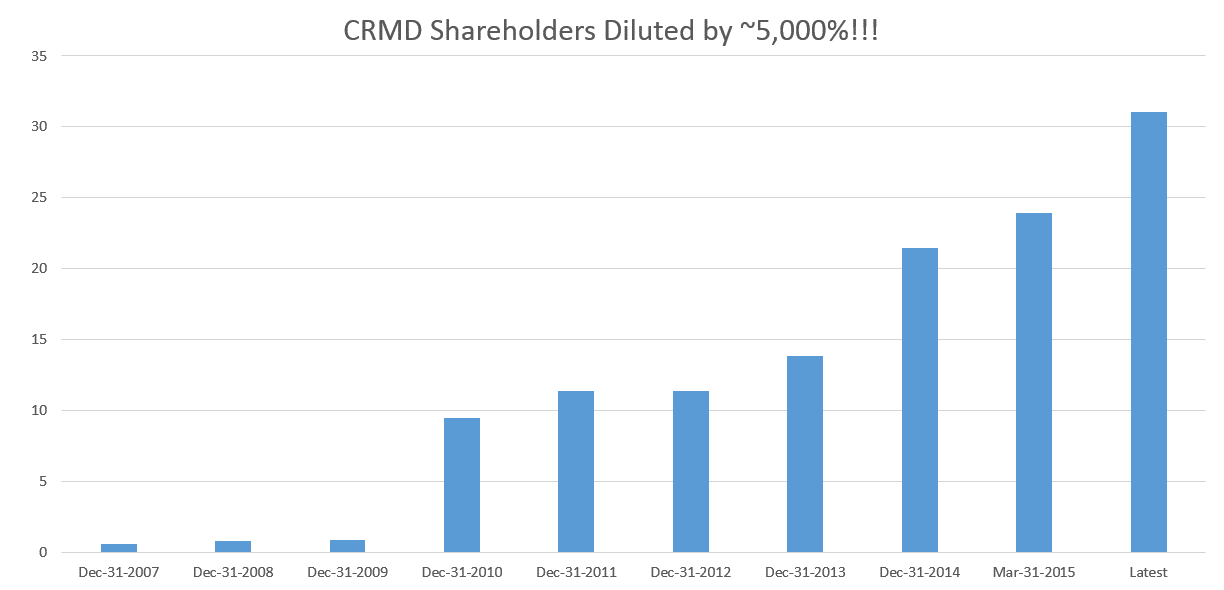

How Have CRMD Insiders Possibly Funded This Disaster?

(click to enlarge)

Chart built by me with CapIQ info

Lucky for CorMedix insiders, they have a publicly traded shell now which they can use to dump stock on retail shareholders so insiders can collect their millions of compensation for constantly failing to do what they say they will. Without this disgusting public shell, it seems obvious they’d all just go bankrupt (again) as happened when this was a private company (despite a temporary partnership with Fresenius back then too).

Keep in mind an “At The Market Transaction Offering” (or ATM) literally entails the company selling you their stock directly in the market andkeeping the cash from your account. In the light of the retail shareholder base and everything we’ve seen above I find this direct “wealth transfer” to be offensive and disgusting.

Is CorMedix Targeting Retail Investors? CRMD’s Paid Stock Promotion and Gambling Conferences

When a previously-bankrupt company has over a decade of failure, with ties to people sued for fraud somehow reaches a temporary $250m+ valuation but is held almost exclusively by unsophisticated retail shareholders, this is a huge red flag. If this is “real”, where are the reputable healthcare investors?

(click to enlarge)

Chart built by me with Capiq info

So how exactly did CRMD end up with one of the most unsophisticated retail message-board based shareholder bases I’ve ever seen? Was this an accident?

Unsurprisingly (given Rosenwald’s involvement) CorMedix has a history of what seems to be paid stock promotion. For instance this wildly promotional “Life Sci” report appears made up to look like a real research report from a Wall Street bank. The fine print at the bottom ofpage 46 reveals the truth:

(click to enlarge)![]()

Or this comically bad “Griffin Securities” report which on the surface appears almost real but, yet again, careful analysis of disclosures reveals the truth, where Griffin is apparently so bullish they won’t even pay for the postage:

(click to enlarge)

Or how about CRMD’s CEO literally taking a shareholder-funded Vegas party trip to pitch worthless stock at a conference apparently aimed specifically at gamblers? This unbelievable conference includes such relevant topics as “Craps Lessons” and “Sports/Horse betting”. If CRMD was about to be imminently acquired why would the CEO have time to go to a Vegas gambling party?

CRMD’s Evercore Sale Process: Obviously Failed

Over 3 months ago CRMD started a “strategic review” process that CorMedix claimed would take a maximum of 6 months. Since then both CRMD insiders and through their company’s ATM, have dumped hundreds of thousands of shares and made many open market transactions. These were not 10b51 transactions which could potentially be protected from insider trading laws, these were straight up open market sell orders. Make no mistake, if CRMD had anything material and undisclosed going on, nobody would be making any open market transactions – or they would be violating federal securities laws and should be in jail, there is no middle ground. The CorMedix legal team would never allow it and they would be in jeopardy of horrific future lawsuits that would wipe them out personally. Furthermore, with the warrant exercises and cash on hand CRMD already had 12m+ months of cash on hand without the ATM shares. Clearly despite years of touting “partnership discussions” and even hiring Evercore, CRMD’s strategic review process to sell the company has obviously failed.

Picture Credit

With all of this now understood we can see the true pattern of CRMD and what is actually going on here.

(click to enlarge)

CRMD pattern chart built by me

CRMD has almost gone bankrupt several times and given a raging bull market for speculative biotech dreck, has seized the moment. Despite claiming the company is “in play” and with plenty of cash, CorMedix claimed they wouldn’t need to issue any stock but instead filed a huge ATM and immediately began dumping hundreds of thousands of shares of CRMD stock into the corresponding stock price rise largely created by confused retail shareholders. Literally taking the cash from unsophisticated retail shareholders and putting into their worthless public shell, where insiders it seems will collect yet another $15m of compensation and endlessly miss their own promises.

CRMD Must be a Sure Thing since Elliott Put 0.00396% of their Portfolio in CorMedix Years Ago, Right?

First of all, big name investors get hosed in frauds all the time like Paulson and SinoForest for example. I will point out three reasons investors are confused about the importance of Elliot’s involvement though.

- Elliot’s backstop of CRMD was SENIOR DEBT and only $3m (way to be bullish…) and carried both a 6% interest rate and hundreds of thousands of free warrants AND the loan terms carried insane “death spiral” terms. These “loan shark” terms in no way can be interpreted by any astute investor as a bullish indication while the total $3m value, huge amount of free warrants and high interest rate mean that in a worst case outcome if/when CRMD goes bankrupt Elliot could have ended up owning the whole company for $3m. Incidentally, this $3m cost is only slightly more than what CorMedix fetched in the last bankruptcy process when no real pharma company wanted to buy these worthless assets.

- The tiny amount of CRMD equity Elliot owns was purchased at average prices far below where the stock trades today.

- Elliot Management’s 1.8m shares of CorMedix may seem like a lot to you but this is approximately nothing compared to their $25+ BILLION in assets under management. CRMD represents less than 0.0396% of their portfolio or (as in 3.9 tenths of one percent) and was likely some random idea from an intern or junior analyst. Elliott isn’t even a healthcare fund anyway and I think they are clearly trapped in a failed investment, trying to do anything they can to salvage this failure. The fact Elliot made a mistake here doesn’t change reality.

- What would you do if Elliot began rapidly selling their stock? There is no margin of safety in CRMD and Elliot has no way out without destroying CRMD.

Elliot has been wiped out in Rosenwald disasters in the past as well. Elliot was a large bag holder of Ventrus which Lindasy Rosenwald actually founded himself. How did this other Rosenwald disaster, which also lured Elliot in, go for shareholders?

(click to enlarge)

Chart credit ycharts

Elliot/Rosenwald’s VTUS was a disaster and fell -95.7%, and the company was sued for “false and misleading statements” and misrepresenting FDA trial info and wiped everyone out. Not that it matters to Rosenwald though as he was paid $25k a month to Lindsays’ firm Paramount Corporate Dev. While you may get hosed, Rosenwald “somehow” always seems to do well on his stocks …

Pic credit Animal House

Following Elliot into Rosenwald biotechs is obviously a bad idea and once the Evercore company sale process formally fails, CRMD stock will implode like all his other biotech wipeouts.

Repeated CFO Turnover and CRMD Auditor found to have “Audit Deficiencies”

As if the huge mess of red flags above weren’t enough, CRMD has gone through 3 CFOs (so far) since just 2012, has “material weakness” regarding financial/accounting internal controls, and CRMD has faced repeated “going concern statements” expressing doubts CRMD can avoid insolvency.

Even more concerning however is CRMD’s curious and sudden “auditor shopping” resulting in changing auditors now to the questionable “Friedman LLP” who has faced repeated, failed audit inspections. In 2008 the PCAOB inspected Friedman and found “audit deficiencies” and “failure to perform sufficient audit procedures”. One would think after a disastrous failed inspection like that, Friedman would fix its issues immediately. In 2013’s PCAOB inspection Friedman actually seems to have gotten worse showing even more “audit deficiencies”. Furthermore there was failure to test controls related to revenue and cash as well as “failure by the firm to perform” … “certain necessary audit procedures”.

CRMD’s previous auditor CohnReznick was with CRMD for years and yet CorMedix changed auditors suddenly despite knowing the above public information about Friedman. Why would CRMD possibly decide to suddenly change auditors to this apparently low quality audit firm shown to have performed insufficient audit work with audit deficiencies??

Furthermore, CRMD only had five employees but somehow burns through $10-20m per year! Where exactly is all the money going?!

Given all these red flags it seems to me CorMedix is rotting from the inside out.

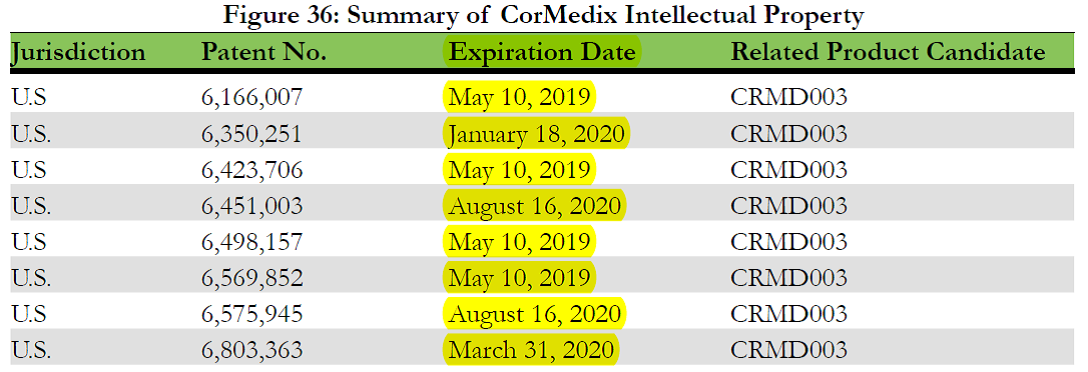

CRMD’s Extremely Weak “IP” Claims

The most absurd part of all the past biotech failures getting re-hyped in this crazy biotech market is they are based on ancient technology with corresponding expiring patents. Even in the ~0% chance a biotech “re-hype” does anything real and ever gets through regulatory hurdles AND ever make any money, any real generic pharma company like TEVA, Mylan (NASDAQ:MYL) or Ranbaxy (OTC:RBXLY) will obviously destroy these weak “follow on” patents and take drink the milkshake of these random biotechs.

In CRMD’s case we can see the majority of their patents expire about the same time CRMD managements (endlessly postponed) market launch date and their ridiculous follow on patents are weak and likely unenforceable if anyone ever cared to challenge them (they don’t).

(click to enlarge)

Chart credit Lifesci

CRMD Management Response:

I called CorMedix management repeatedly for weeks to try and get answers but I was unable to ever get anyone to pick up the phone. I’m not even convinced they come into the office and any company that can’t answer their phone for investors is a huge red flag in my view. I encourage you to immediately call CRMD and speak to the company YOU own as a shareholder to demand they clarify the multitude of issues raised here.

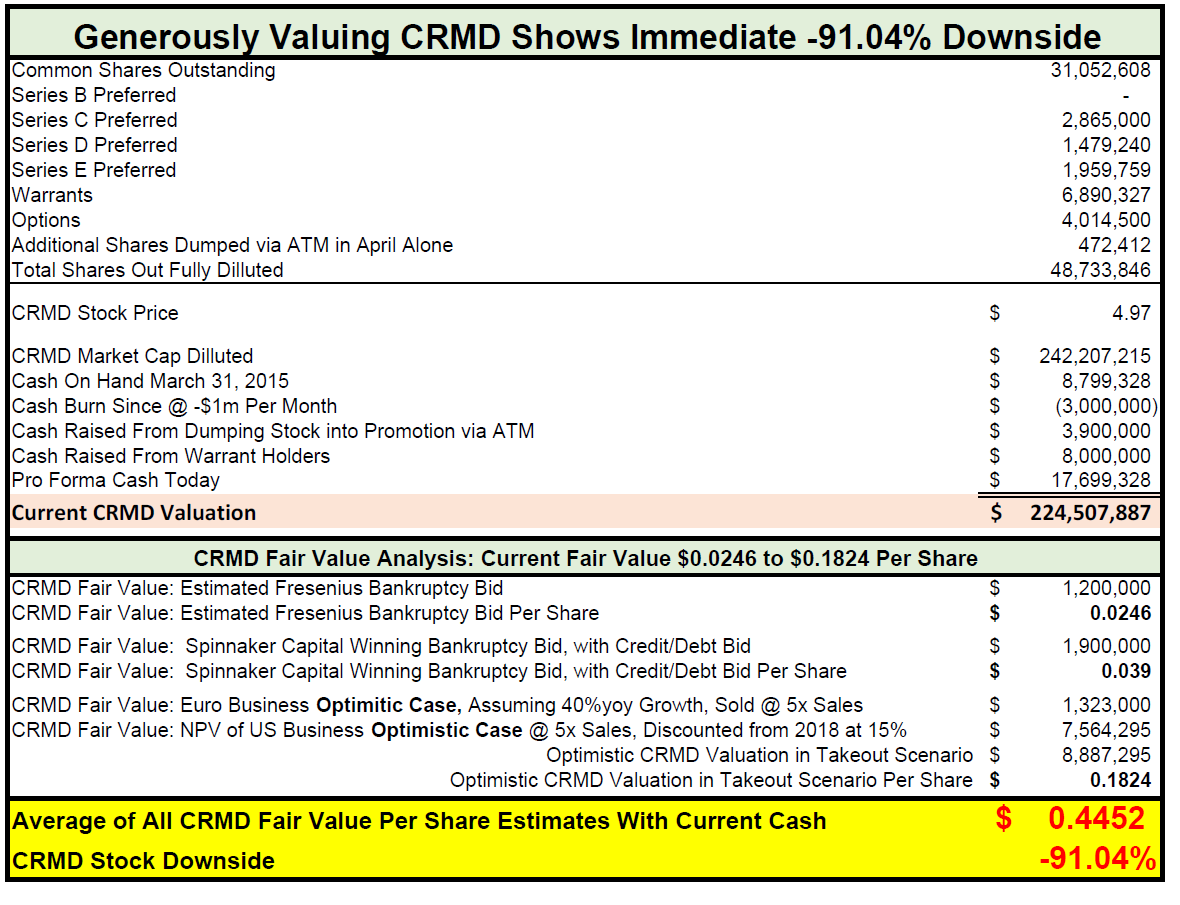

CRMD: True Fair Value: “Optimistic Case” Shows -91.04% Downside

Now that we understand CorMedix ’s sole product is not commercially viable, let’s be very generous and assume CRMD insiders don’t simply take whatever minimal value or shareholder cash is left for themselves and endlessly dilute everyone into oblivion. I will generously assume CRMD’s European business grows 40% next year (it won’t). I will also assume CRMD ever goes through with their comically delayed Phase3 AND gets approved AND launched AND produces sales 3x higher than Tauropharm AND this is all done according to CorMedix management’s notoriously unreliable timeline estimates.

(click to enlarge)

Even being optimistic and making all these obviously unrealistic assumptions STILL shows CRMD fair value per share of $0.445 per share for -91.04% downside, which is actually still 3x higher than where CRMD stock traded in just 2012. More realistically though, I think CRMD will just go bankrupt (again) eventually once their cash runs out and retail shareholders finally wake up and refuse to fund this insider enriching bagholder machine. A financially unviable product controlled by a team of people seemingly intent on self-enrichment is fundamentally worthless in my view, especially as foundational patents are expiring soon.

Note a full 81.6% of CorMedix fair value calculated above is made up of the cash CRMD just raised. I am convinced insiders will just keep this and burn it so this should likely be adjusted downward in value by some amount but remember I am trying to be as generous to CRMD as possible here.

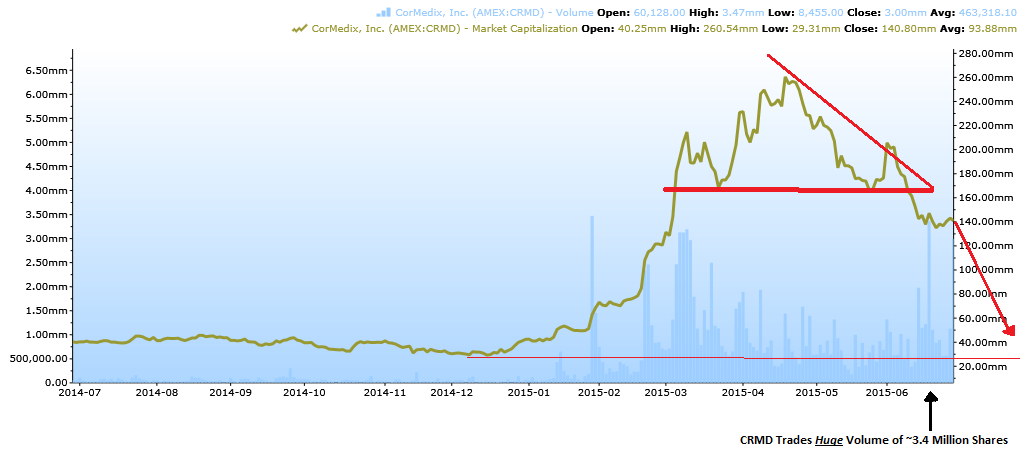

CRMD Stock Technically Breaking Down On Huge Volume: “Head and Shoulders” & Wedge Broken

The only thing worse than the fundamentals here is the short term technical chart. CorMedix has broken through a classic head and shoulderspattern, as well as breaking down through a large wedge pattern. As you can see in the chart below there is zero technical support for CorMedix stock until ~$1.32 per share, which would still give CRMD a $63.71m market cap, which as you can see based on the fundamentals above is still wildly overvalued. I don’t have to remind you CRMD was a $0.14 stock recently in 2012 so it may be interesting to think about the value of your investment as it round trips that price.

(click to enlarge)

Chart by me

I will also point out CRMD stock has been imploding on huge volume recently. You can trust InvstorVillage or Ihub all you want, but the reality is large holders are dumping CRMD stock in big volume while all you see on the message boards is wild, unjustified optimism. I think it is obvious someone is getting fooled, please make sure it isn’t you. Are message board touts promoting optimism while aggressively dumping their stock and warrants?

It honestly makes me sad to see so many retail shareholders get “bagged” over and over and over. I’m pleading with you guys, please pay attention and stop buying impossibly speculative longshots based on suspicious message board touts. Please. There are literally tens of thousands of investment opportunities globally in front of you, including thousands of healthcare companies, and I’m sure you can do better than this with even modest effort given all the great tools like SeekingAlpha at your disposal. There is no reason to invest in any company where insider compensation is more than R&D which has partnered with people involved in fraud allegations. None. Zero.

PumpStopper Makes His Call: “CorMedix Will Never Be Sold for $250m+, Actual Fair Value $0.000?

“To Plunge or Not to Plunge, That is the Question”

Picture by me

CRMD Conclusion: Don’t Fall For It

CRMD’s unsophisticated retail investors are expecting a dramatic, company-sale conclusion to CRMD’s “strategic review process” in 2h 2015, which is clearly never going to happen. The German patent lawsuits just blew up in CRMD’s face and Tauropharm corporate records show the Taurolidine catheter lock market is a tiny fraction of that which is portrayed by CRMD.

Every day that goes by is more confirmation the Evercore sale process has obviously failed. As retail investors understand this reality, while simultaneously the research showing CRMD’s sole product is unviable and worthless, I expect CorMedix stock to continue imploding eventually back to its previous lows of $0.14 per share on its way to another bankruptcy while Rosenwald and insiders collect another $15m of shareholder money based on endless failure and dilution.

Even if you ignore all of the above AND think CorMedix insiders are honest people with your best interests at heart, CRMD still has -91.04% downside in a “best case” scenario as the current valuation is impossibly inflated.

There are thousands of publicly traded healthcare opportunities out there and I see zero reason to risk my hard earned savings in something this messed up. Don’t fall for it.

Invest carefully.

{kind=link}