In this article I present the dividend safety analysis of Chico’s FAS Inc (NYSE:CHS). The company is a retailer of women’s clothing and accessories. The main interest for some investors is the high forward yield of ~8.7%. Despite CHS’ current challenges, the company is Dividend Challenger having grown the dividend for nine consecutive years. However, the raises since 2014 have only been one penny per share. The high yield is attractive, but investors should be wary since the dividend is not covered by earnings or free cash flow. This places the dividend at risk for a freeze or even worse, a cut. Chico’s FAS is a turnaround story and not suited for most investors focused on dividend growth or even income.

Before I present the dividend safety analysis, let’s first discuss Chico’s FAS’ businesses. The company operates under three brands: CHS, White House Black Market, and Soma. The Chico’s brand primarily sells private branded clothing focusing on women 45 and older. The White House Black Market brand sells private branded clothing and accessories. The Soma brand sells private branded lingerie and sleepwear.

Retail story

As of November 2, 2019, Chico’s FAS operated 1,373 stores in the U.S. and Canada. The company also sells through 89 international franchise locations in Mexico and two franchise locations in U.S. airports. The company also sells merchandise through its websites and catalog.

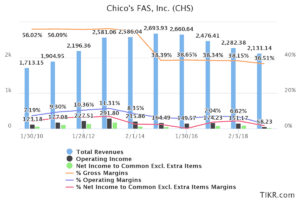

CHS’ top line has been declining since 2015. In turn this has pressured margins as cost cuts have not kept up with the decline in sales. But with that said, only two of the three brands are deformingly poorly with negative organic sales growth. At the Chico’s brand, sales continue to decline. However, there has been sequential improvement in comparable sales in the most recent quarter as the company tries to right the ship through better product, better inventory management, and improved marketing. At the White House Black Market brand, the company is also trying to turn around sales declines.

The bright spot for Chico’s FAS is the Soma brand, which showed an acceleration in sequential sales growth with two quarters in a row of double-digit sales growth. The market has punished Chico’s FAS’ stock price, which is down ~75% in the past three years due to the company’s challenges.

Chico’s FAS is clearly a turn around story. The company is making efforts to improve merchandise, marketing and customer engagement, clear old inventory, make omnichannel investments, and drive greater efficiencies. That said, this will take some time perhaps a few years. Furthermore, the competition is not standing still. In addition, recent tariffs on imports from China will likely cause headwinds to the turnaround effort.

CHS Dividend Safety

Let’s now examine the dividend safety of Chico’s FAS. From the perspective of earnings, the dividend is not covered. Consensus FY 2019 EPS is ($0.14) and the annual dividend is $0.35 per share. This means that Chico’s FAS will need to use cash on hand or add debt to pay the dividend. This presents higher risk to the dividend when combined with the decline in top line.

The dividend is not covered by free cash flow either. At end of Q3 FY 2019, operating cash flow was ($13.81M) and capital expenditures were $8.05M giving free cash flow of ($21.86M). The dividend required $10.36M. Even on an annual basis, the dividend is not well covered by free cash flow after stock repurchases are factored in.

In fiscal 2018, operating cash flow was $158.1M and capital expenditures were $54.2M giving free cash flow of $103.9M. The company bought back $84.8M in stock leaving only $19.1M for the dividend, which required $43.2M. The company had to pay the remainder of the dividend with cash on hand.

Net debt is a bright spot right now since the company has a net cash position. The company has long-term debt of only $46.3M at end of Q3 FY 2019. This is offset by $70.19M in cash and equivalents, and $57.25M in marketable securities on hand. But cash and equivalents have been facing a slow decline from a peak of $193.6M at end of Q1 FY 2018 to less than half that now. Debt doesn’t currently place the dividend at risk but the declining cash position is of concern.

The risk here is that Chico’s FAS may need to preserve cash for operations and capital expenditures since it has negative earnings and operating income. The simplest way to do that is to stop the stock buybacks and freeze or even cut the dividend. In fact, Chico’s FAS has reduced stock buybacks quite a bit in the past two quarters. But historically buybacks have been lumpy meaning that they are conducted periodically during the year and not a fixed amount each quarter.

There is still about $55M left in the existing repurchase authorization so it is possible that the Chico’s FAS will buyback more shares this year or in fiscal 2020. The company also has not signaled that they are reducing the dividend at this point. From this context, the balance sheet can buy some time in the short-term but if the turnaround does not gain traction the risk to the dividend obviously rises.

Final Thoughts On CHS

CHS’ dividend yield may be enticing but there is risk here. The company is currently a turnaround story and it is not clear if the turnaround will take hold. Chico’s FAS faces intense competition from bricks-and-mortar stores and e-commerce channels. In addition, tariffs and trade friction are also providing headwinds.

The dividend is currently not covered by earnings or free cash flow. But the balance sheet will buy a little bit of time here for the turn around to take hold. However, if the top line and margins do not stabilize and earnings and cash flow decline further then the risk to the dividend will rise. Hence, at this time I do not view the dividend as safe.

BIO

Dividend Power is a blogger on dividend growth stocks and personal finance. He also works as a part-time independent equity research analyst with a leading newsletter on dividend stocks. Dividend Power also provides analyses on Seeking Alpha. He is currently is in the top 10% out of over 7,000 financial bloggers as tracked by TipRanks (an independent analyst tracking site).