I recently wrote an article for Sure Dividend entitled “Consider Equity REITs for Your Next Investment“. In that article, I listed nine equity REITs (eREITs) for dividend investors to consider in light of the drubbing that eREIT valuations have recently taken due to fear of rising interest rates and to capitalize on the pass-through provision for REIT income included in the new tax legislation. Both of these topics are covered in some detail in the previous article. This article provides a more complete investment thesis for Chatham Lodging Trust (CLDT) one of the nine eREITs highlighted in the previous article.

[REITs]ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Chatham Lodging Trust

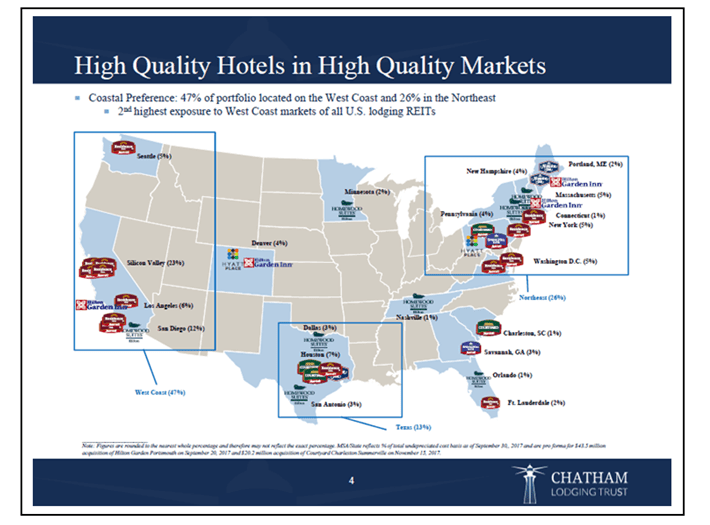

Chatham Lodging Trust is a select service and extended stay hotel eREIT with an enterprise value of roughly $1.6B. Chatham Lodging Trust owns 41 hotel properties primarily on the West (47%) and East (26%) coasts and in Texas (13%). The chart below shows the mapped locations of CLDT’s US properties.

Source: Chatham Lodging Trust Website

CLDT’s hotels are concentrated in prime business locations serving large metropolitan centers. The chart below shows a breakdown of CLDT’s hotel property types and the major markets served.

Source: Chatham Lodging Trust Website

One of the key metrics (maybe THE key metric) that measures a hotel’s ability to generate revenue and potential earnings is known as RevPAR or revenue per available room. Compared with CLTD’s select service hotel REIT peers, CLDT consistently has the highest RevPAR by a significant margin. The chart below shows CLDT’s RevPAR compared to its select service hotel peers.

Source: Chatham Lodging Trust Website

Chatham’s high RevPAR along with being a pure select services (i.e. limited service) with lower costs than full service hotels, allows CLDT to generate high EBITDA margins, the highest in the hotel REIT sector. The chart below shows CLDT’s EBITDA margins compared to its peers in select service hotels and compared to full service hotels.

Source: Chatham Lodging Trust Website

In addition to generating a consistently high stream of EBITDA, CLDT’s capitalization structure is conservative and healthy. The chart below summarizes CLDT’s capitalization structure and key debt metrics.

Source: Chatham Lodging Trust Website

Key metrics are CLDT’s low overall debt, it’s low cost of debt (4.6%), the fact that 87.6% of their outstanding debt is fixed rate and not immediately subject to rising interest rates. The only debt coming due before 2023 is the $75M on CLDT’s revolver facility in 2020 and a small $14M note in 2021. Chatham won’t have to consider refinancing any significant portion of its debt for 4-5 years.

Chatham Lodging Trust Recent Financial Performance

Chatham’s near term financial performance has been very solid as evidenced by its growth in funds from operations (FFO) and adjusted FFO (AFFO) and its dividend.

A short note here for investors not fully versed in eREIT financial metrics. Because eREITs have very high depreciation write-offs which are tax accounting entries that do not affect cash flow, the usual metrics of earnings per share (EPS) and price earnings ratios (P/E) are not meaningful for eREIT financial reporting. The accepted metric for eREIT financial reporting is FFO and AFFO which are cash flow metrics. The following charts show CLDT’s near term financial performance in those accepted metrics.

Source: Author

The charts above show CLDT’s AFFO/share and cash dividend payment growth over the last 6 and 7 years respectively. That growth has been steadily upward except for 2016 AFFO and the 2017 dividend. Double digit AFFO and dividend growth is very solid performance.

The dividend payout ratio is also presented for eREITs in terms of AFFO. The chart below shows CLDT’s payout ratio over the last 7 years.

Source: Author

For the last 6 years, CLDTs payout ratio has been 61% or less. For an eREIT, anything less than 90% payout ratio is acceptable and less than 80% is good. Chatham’s payout ratio of 61% is very conservative and certainly has room to allow for future dividend increases.

CLDT Investment Thesis

With the general market currently experiencing a mild correction and eREIT valuations suffering further from fear of rising interest rates, why would I be considering an investment in CLDT at this time?

Today, CLDT is on sale having fallen 10% in about the last 6 weeks. While the market has pushed eREIT valuations down over the last quarter, and particularly the past two weeks, due to fears of rising rates, history tells us that eREITs generally do well during periods of slowly rising rates and some eREITs will even beat the big market indexes under these conditions. This is particularly true for hotel REITs since the economic conditions that are causing the Fed to tighten monetary policy will also improve hotel occupancy and allow for room rate increases. For a more complete discussion of the impact of rising rates on REIT financial performance as well as a more detail on the new pass-through provision, readers should see my earlier article “Consider Equity REITs for Your Next Investment“.

Chatham continues to grow its property assets by acquiring quality properties. The last two CLDT acquisitions were the Hilton Garden Inn in Portsmouth, NH and Courtyard in Summerville, SC just north of Charleston. The Hilton Garden Inn is located in the center of downtown Portsmouth, is only 6 years old, recently renovated, and has a 2018 projected RevPAR of $167 making it CLDT’s highest revenue generator. The Courtyard is strategically located near the existing Boeing and Daimler facilities and, in addition, Volvo is building a new manufacturing facility very near the Courtyard location. Both of these recently acquired properties should payoff very nicely in the next few years and allow CLDT to increase its dividend.

Final Thoughts

Chatham is a well established and well run hotel REIT with a solid balance sheet and a history of growth. Recent investor jitters over rising interest rates has pushed CLDT’s stock price into bargain territory and its dividend yield up to 6.2%.

The partnership and REIT pass-through provision in the recently passed tax legislation will shield 20% of CLDT’s dividend from Federal income taxes. With the economy picking up steam and projected GDP growth between 3-4 percent combined with CLDT’s prime business locations and its high RevPAR and EBITDA margins, CLDT is well positioned to provide many years of healthy dividends and capital appreciation to today’s investors.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

Article by Dirk S. Leach, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

{kind=link}