Black Bear Value Fund letter to investors for the second quarter ended June 30, 2019.

“Sometimes I wish I could boldly go where no man’s gone before, but I’ll probably stay in Aurora.” – Garth Algar

Q2 hedge fund letters, conference, scoops etc

To My Partners and Friends:

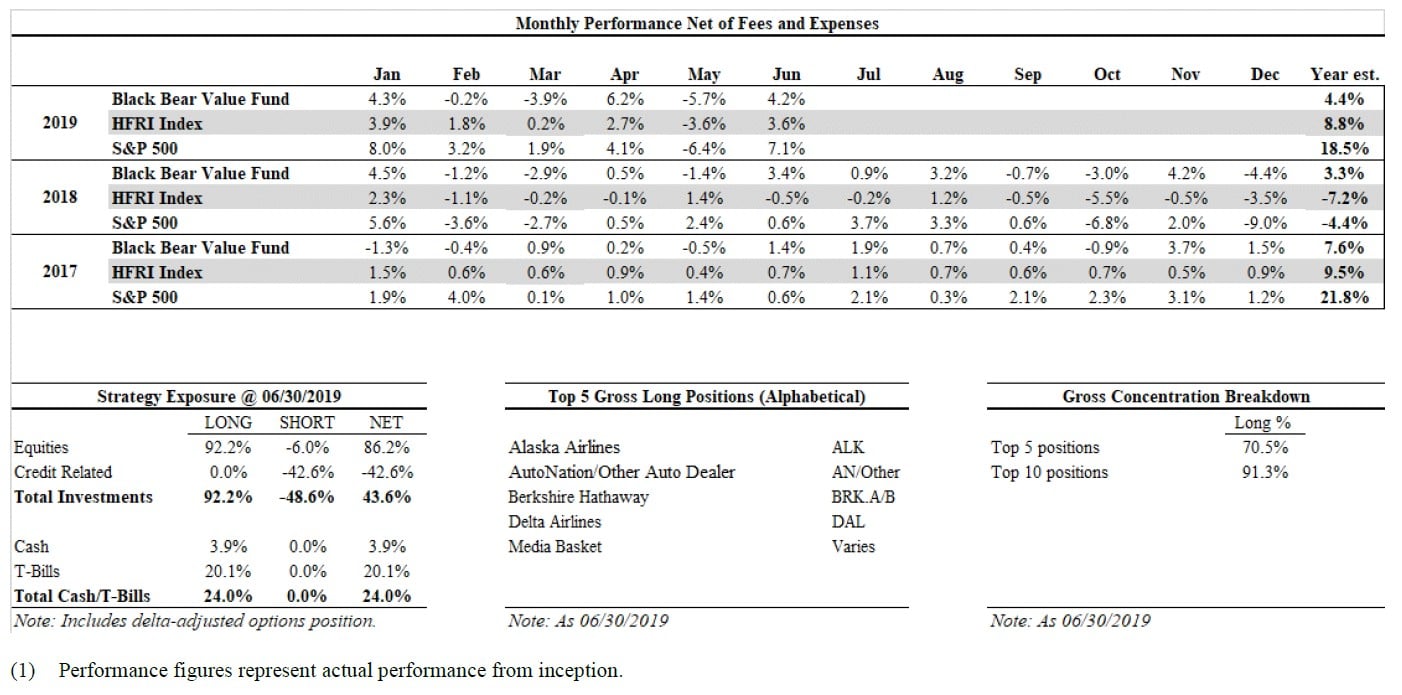

- Black Bear Value Fund, LP (the “Fund”) returned +4.7% in the 2nd quarter and 4.4% YTD.

- The S&P 500 returned +4.8% in the quarter and +18.5% YTD.

- The HFRI index returned +2.7% in the quarter and +8.8% YTD.

- We do not seek to mimic the returns of the S&P 500 and there will be variances in our performance.

Each investors’ return will vary depending on the timing of the investment. I would caution those reading that our portfolio is shown at a point in time and can change for a variety of reasons.

Performance Summary

Top 5 Businesses We Own (Alphabetical)

Below you will find positions by name and others by theme. Our main goal is to communicate the central portfolio themes. At times a theme would be top 5 in total, but not on an individual company basis (Media content is a great example). I will strive to maintain consistency in this style of reporting, but it could vary from quarter to quarter.

A secondary goal of this type of disclosure is to protect our intellectual capital. We have had 3 sources of growing assets under management. We made some money in 2018 and have modestly grown from 2019 performance. Another source of growth has been from existing investors (that includes me) adding capital to Black Bear in 2019. Additionally, we have welcomed several new investors over the course of the year. Finding ideas can require turning over a lot of rocks and I would like to continue buying the businesses we like at cheap prices as our partnership grows. Further discussion on idea sharing follows at the end of the letter.

Please note our media content section is largely similar as last quarter. Others have been updated.

These positions comprise ~71% of the portfolio at quarter-end.

Airlines: Alaska and Delta

Past discussions have centered on Alaska Airlines, which remains a core position. We also own Delta, which benefits from similar dynamics as Alaska though each story has its nuances. The capital-light credit card business is undervalued, and we could be getting an airline for near-free. Healthy balance sheets, a respect for capacity growth, wise capital allocation and rational decision-making result in a much different industry than in prior decades. Each business is independently a top 5 position on its own.

Please refer to past presentations and/or letters which discuss the thesis on the airlines. These can be found on our website behind a password protected wall. These are only intended for accredited investors.

Auto Dealers

We have owned AutoNation for several years and now own another auto dealer. The thesis for both is similar though not identical. A lot of attention is being paid to New Car selling rates (SAAR) and less attention is being paid to the growing car park and opportunities in parts and service. The new dealership we purchased has a great management team, is smaller (maybe an M&A target?) and is cheap.

Selling new cars has long been a lower-margin business and gets more attention than is deserved. Car dealerships have resilience with car buyers migrating to used vehicles (higher-margin). Historically, the new car customers received more of the focus both on the sale and the subsequent warranty and service work. Over the coming years, the business should generate meaningful cashflow from the used business as well as the parts/service segment (both for new and used cars).

Berkshire Hathaway

Berkshire Hathaway remains in our top 5. We have owned it continuously since the inception of our Partnership in varying sizes. The combination of a fortress balance sheet, a relatively cheap equity portfolio and healthy/growing operating businesses with sustainable moats allows me to sleep at night. Berkshire has recently been buying back their stock and has allocated capital in a thoughtful manner since inception. If we encounter any periods of distress in the marketplace, Berkshire can capitalize.

In May, my family travelled to Omaha for the annual meeting. We would highly recommend this to anyone with kids. It’s a very natural way to show kids businesses in a tangible way. Now when we pass a See’s Candy or GEICO billboard my girls will often yell out something Berkshire related. I want to extend my thanks to Berkshire for a great weekend as well as the fund managers/fellow shareholders who came up to say hi. My kids got a real thrill and we plan on making this an annual family tradition.

After we spent the weekend in Omaha my wife asked me why we owned so much of the stock and how I value it. I’ve also gotten this question from current LP’s, so I figured I’d give you the napkin version of why I think it’s cheap. I would warn that what follows is NOT a math proof but a rough valuation.

#1 Public stock holdings

- ~$140k per class A share (vs. a 6/30 price of ~$318,000).

- Apple ~24%, Financials ~34% (American Express, Bank of America, Wells Fargo etc.). Coca Cola ~9% and Kraft ~5%.

- Somewhere between kind of cheap to fairly priced

- Assume a range between $130k-$180k with $150k at the midpoint.

#2 Operating businesses

- Examples: GEICO, BNSF railroad, McLane, Precision Castparts etc.

- Should generate $13-15k in pre-tax cashflow on average in a given year for the next few years.

- Assume 8/10/12x multiple which equates to ~6-9% FCF yield.

- A historical market multiple to a discounted market multiple.

- This gets to a value of $104k-$180k per Class A ($13k x 8 for the lower bound of $104k).

#3 Cash on balance sheet

- War chest of cash that is equivalent to $70k per class A share.

- What’s the value of cash?

- Current book value = $70K per share

- Maybe positive option value from that cash? In PV terms maybe it’s worth $75k/$80k? More?

- Perhaps in the latter stages of the Buffett/Munger Opus they mirror one of their investment heroes, Henry Singleton from Teledyne (known for very opportune buybacks) and buy back a lot of Berkshire stock.

Total

- Add up #1, #2 and #3 and you get to a price of ~$304k-$430k assuming no premium from the cash vs. $318K at quarter end.

- If we presume some premium for the cash, we arrive at a stock price far above where it is trading today with a lot of safety.

- This position gives me no heartburn and as I am writing this I wonder why I don’t own even more.

- Big up…small down.

Media-Content Basket (Same note as last quarter)

Media-content companies (companies that produce the shows/events we watch on screens) have been out of favor. There is fear about cord-cutting, millennial apathy, increased penetration of Netflix, the destruction of the cable bundle and an increasing amount of direct-to-consumer video delivery. These fears are fair but are more than reflected in the stock prices which trade anywhere from 10-15% free-cash-flow yields. Our businesses produce unique content that has advertising value, consumer loyalty, and an engaged customer. Methods of media consumption will inevitably change over time. What will remain the same is a need for content to attract the consumers. The industry is ripe for consolidation and M&A (“mergers and acquisitions”) Who buys who and when? I’m not sure. We will clip meaningful cashflows from the businesses while we wait.

Shorts

We remain short credit in large size in the Fund. We have also added some equity shorts though they are small. I have discussed the short-credit thesis at length in previous letters. Please check out our past letters and/or presentations as our feelings have not changed.

If the Fed is concerned about the economy, I would presume the spread being charged to companies should widen as their fears of potential default rise. So far that presumption has been wrong and resulted in mark-to-market losses in our portfolio this year.

When one shorts an equity outright, the gains are limited to 100% (the company goes bankrupt) while the losses are unlimited (stocks can go up infinitely). This ratio does not suit me and while I am bearish on the prospects of our shorts, I lack the temperament that could rest easy with the potential for unlimited losses. Hence, they are structured with puts, so I know how much we can lose.

The equity short ideas come from work done on the long side and are companies which compete or are in the ecosystems of businesses we are familiar with. We have 2 shorts and think their prospects are misunderstood by their owners. The businesses are capital intensive, lose money, require more capital to grow, with gimmicky/misleading accounting and exceptionally promotional management. Promotional management can be quite convincing as well as the group-think/party associated with the investment.

I would like to say I’ve never fallen victim to smooth management but that would be wrong. It’s also a reason I am loathe to spend time with managements until I have done a lot of my own work. These companies remind me of a “greatest hits” version of some of my past investment mistakes. I would anticipate losing money on these in the short-term as optimism takes time to be tempered. When the genie is let out of the bottle, I presume it will be a fairly quick fall from grace. Short-selling can open one up to confrontations with management and a lot of wasted time. For that reason and others, I am not going to be disclosing the names of the stocks we are short but plan on discussing when we exit the positions.

As I watch many companies with money losing, quasi indecipherable businesses with “visionary” leaders move up in price I think of Dana Carvey in Wayne’s World saying, “Party on Wayne!”. When the party ends another line may be equally adept: “If you’re gonna spew, spew into this.”

Musings on Idea Sharing and Capital Allocation

Talking about what one owns can be both helpful and harmful. Sharing some names with our partners and some outside managers can help me think thru ideas and provide pushback. On the other hand, one can feel an attachment to an idea and the accompanied bias from defending it. This is something to be particularly mindful of. I am much more eager to hear the other side of an argument as it’s hard to learn from preaching to the choir. If we haven’t thought through thru a counterpoint or have the hubris to ignore it, we run the risk of losing money. As one gets older and has more experience, you ironically realize more of your potential for blind spots and feel no shame in saying “I don’t know” or seeking out counterpoints.

Onto buybacks…There is a misnomer, largely stemming from politicians who have decried stock buybacks as “bad”. Buybacks are neither good nor bad without knowing the price being paid and the intrinsic value of the business. A business generates cash and management has a choice to do something with it. They can hang onto it. They can reinvest in the business (new plants, raises for employees etc.). They can buy other companies with it. They can issue dividends to the owners. Lastly, they can buy back their own stock. If they pay too high a price it’s bad for shareholders. Alternatively, if they buy cheaply it’s great as we own more of the business at a discount. Most of the companies we own have high amounts of insider ownership and employee ownership so if management buys in stock cheaply we all benefit. I would encourage our elected officials to better understand the basic economics of how this works before painting broad brushstrokes. Hardworking employees who support their families should benefit as well as the owners of the business. A word that seems to have disappeared from our political discourse is balance. We would all benefit from a more balanced debate and understanding of this topic.

Cash

We had approximately 8% of our assets in cash/T-bills (ignoring the cash we get from our shorts). We do not target a cash balance.

General partnership business

We recently presented on the airlines at ValueX Vail. Vitaliy has organized a great event that I look forward to every year. It is a special group of smart, kind and collaborative people and I am lucky to be included. The presentation was recently sent out and can also be found on our website, www.blackbearfund.com.

Thank you for your trust and support. Have a great summer.

Black Bear Value Partners, LP

This article first appeared on ValueWalk Premium

{kind=link}