Stanphyl Capital January 2020 hedge fund letter to investors on why Tesla Inc. (NASDAQ:TSLA) is still a good short and going to be crushed by competition from the Audi e tron. Full letter can be found in PDF at the bottom of this post.

Friends and Fellow Investors:

……………

Despite our significantly reduced (in December) Tesla short position, that stock hurt us again this month as it was up another 56% in January, and roughly half of this month’s negative performance was due to a major hit we took on January 2021 TSLA $690 calls that I’d shorted in the $17s back in 2018 when the stock was in the low $300s. Coming into this month they comprised just under 5% of the hedge fund and were priced at $14, and when the stock rocketed in early January I stopped them out at $25 to $35 (they finished the month at $108!), and the bulk of this month’s damage was done. Now our only TSLA short position is straight equity that currently comprises around 5% of the fund.

I continually ask myself what I’ve learned from this disastrous Tesla experience, and how I’d handle it differently in the future. Let me first say that before I opened this fund I made many avoidable mistakes in the stock market; in fact, it was learning from a long litany of “the usual investing mistake suspects” (if you’ve been in the markets long enough, you’ve undoubtedly learned from many of them yourself), that gave me the confidence to open this fund in 2011.

That said, Tesla, unlike any other company I’ve ever seen, checks every box for a desirable short position: a fundamentally terrible business in a capital intensive, massively competitive industry with a bubble-stock valuation and a pathologically lying CEO committing (and so far getting away with) a multitude of fraud in plain daylight. In other words, you give me 1000 TSLAs and for 999 of them a short position will work fantastically.

Stanphyl is a concentrated fund (that’s why I won’t handle more than 10% of any outside value investor’s portfolio, although approximately 80% of my money is in the fund) that will sometimes run as much as 1/3 of the portfolio in a single equity position. When I see something that I believe would work 999 times out of 1000 I don’t size the position as if it has, say, “a 70% probability of working.” Instead I size it as if it not working would be the equivalent of getting hit by “a stock market meteor” (which admittedly has lower odds than getting hit by a real meteor).

You give me 1000 companies with the profile of Tesla to short and together we’ll have the largest and most successful fund in the history of investing, but unfortunately (or perhaps “fortunately”) there aren’t 1000 short candidates with the profile of Tesla—in fact, there aren’t even two. From a practical standpoint then, Tesla’s “rarity” means it’s extremely unlikely we’d ever again size a short position in a similar manner (our normal size for a short position is 2% to 5%)—not because “this one didn’t work,” but because we’ll likely never again see a company as crazy as Tesla.

As for Tesla, I’ll now leave it as a 5% position unless I learn before the market does (legally, of course!) that the feds finally slapped a pair of cuffs on Musk. Prior to stumbling across this company I had a long record of exceptional outperformance, and I want that record back.

In that vein, as you may recall from last month’s letter, in late December I took the fund back to its roots to focus primarily on finding deep-value microcap/nanocap long positions and (as I won’t alter our definition of “value stocks” to suit a worldwide asset bubble) holding more cash if necessary. I covered our nonTesla equity shorts for as long as the Fed is printing money; when the money-printing stops we’ll short other stocks again, but as I wrote last month, right now that’s like playing poker against a guy with a chipmaking machine on his lap—he can call every bet a short-seller makes and I don’t want to “play against the house.”

…………

And now for the fund’s positions…

……………..

As noted above, we remain short Tesla Inc. (TSLA), which I still consider to be the biggest single stock bubble in this whole bubble market. The core points of our Tesla short thesis are:

- Tesla has no “moat” of any kind; i.e., nothing meaningfully proprietary in terms of electric car technology, while existing automakers—unlike Tesla—have a decades-long “experience moat” of knowing how to mass-produce, distribute and service high-quality cars consistently and profitably, as well as the ability to subsidize losses on electric cars with profits from their conventional cars.

- By mid-to-late 2020 Tesla and its awful balance sheet will return to losing money.

- Tesla is now a “busted growth story”; Q4 revenue was roughly flat year-over-year while unit demand for its cars is only being maintained via continual price reductions and expiring tax incentives.

- Elon Musk is a securities fraud-committing pathological liar.

Tesla tax credits

In January Tesla reported $105 million in earnings for the fourth quarter of 2019 (entirely from the sale of regulatory emissions credits, not from a self-sustaining auto business), which was down 25% from Q4 2018, while revenue was up just 2% and the full-year loss was $862 million. If we compare the second half of 2019 to the second half of 2018, Tesla revenue fell 3% and net income fell 45%. Yet somewhere out there is a mass of idiots bidding this stock to the moon because they think it’s a “hypergrowth” company! Liam Denning at Bloomberg does an excellent job of pondering that absurdity.

Additionally, Tesla’s “earnings” are typically inflated by at least $200 million per quarter due its massive ongoing warranty fraud, so in reality the company likely lost money in Q4; here’s my Twitter thread explaining some of that and here’s an excellent Seeking Alpha article explaining the rest. Meanwhile we’ll have to see the 10-K in a few weeks to learn what other scammery Tesla pulled in the quarter; rest assured there was plenty.

Fraud at Tesla?

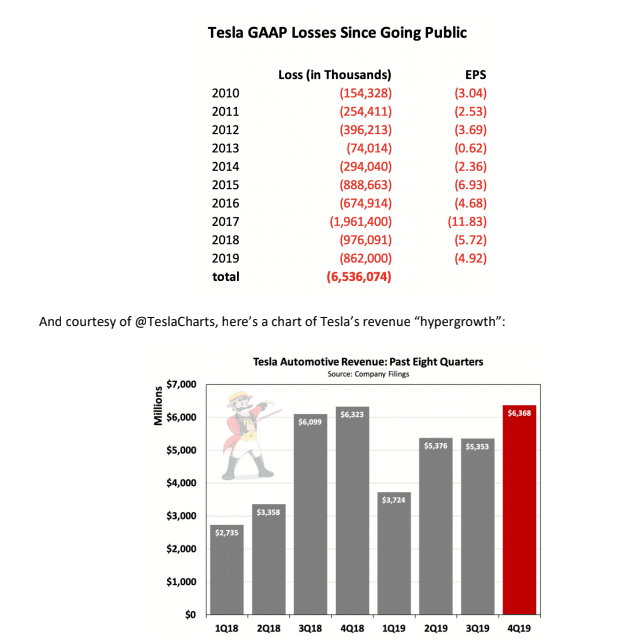

Yet even with all that fraud, here (courtesy of my friend @Montana_Skeptic) is a great historical chart of Tesla’s earnings track record despite billions of dollars in public subsidies:

And courtesy of @TeslaCharts, here’s a chart of Tesla’s revenue “hypergrowth”:

As for the nonsensical earnings conference call, this quote from Musk about when so-called “Autopilot” will be “feature complete” may have been the highlight:

“feature complete just means like it has some chance of going from your home to work let’s say with no interventions. So, that’s — it doesn’t mean the features are working well, but it means it has above zero chance. So I think that’s looking like maybe it’s going to be a couple of months from now.”

That insane statement prefaces Fraud-Boy’s desire to recognize approximately $500 million of non-cash (it’s already on the balance sheet) deferred revenue from its fraudulently named “Full Self-Driving” (the capabilities of which offer nothing of the kind), thereby turning a future money-losing quarter (likely Q2 2020) into one showing paper profits. Meanwhile, God only knows how many more people this monstrosity unleashed on public roads will kill.

Major competition from the Audi e-tron

For those of you looking for a resumption of growth from Tesla’s upcoming Model Y when it launches in March, that car will both massively cannibalize sales of the Model 3 sedan and (later this year and in 2021) face superior competition from the much nicer electric Audi Q4 e–tron, BMW iX3, Mercedes EQB, Volvo XC40 and Volkswagen ID Crozz, while less expensive and available now are the excellent new all-electric Hyundai Kona and Kia Niro, extremely well reviewed small crossovers with an EPA range of 258 miles for the Hyundai and 238 miles for the Kia, at prices of under $30,000 inclusive of the $7500 U.S. tax credit. Meanwhile, the Model 3 will have terrific direct “sedan competition” later this year from Volvo’s beautiful new Polestar 2, the BMW i4 and the premium version of Volkswagen’s ID.3.

Chinese cars

And if you think China is the secret to the resumption of Tesla’s growth, let’s put that market in perspective: prior to a recent 10% VAT exemption Tesla was selling around 30,000 Model 3s a year there, and “the story” is that avoiding the 15% tariff and 10% VAT, plus a $3600 EV incentive that likely expires next year will allow it to sell a lot more. However, the rule of thumb for the elasticity of auto pricing is that every 1% price cut results in a sales increase of up to 2.4%.

If we assume a 2.4x “elasticity multiplier,” domestically produced Model 3s that are 33% cheaper would result in annual sales of just 54,000 (33% x 2.4 = 79% more than the previous 30,000), meaning Tesla’s new Chinese factory would be a massive money-loser by running at just slightly more than 1/3 of its initial 150,000-unit annual capacity and 1/10th of the capacity it will have two years from now.

This guarantees hugely missed growth targets and it is “growth” (or more accurately, the fantasy of growth) that drives Tesla’s stock price. And here’s a great overview of what a dogfight the Chinese EV market has become.

Meanwhile, sales of Tesla’s highest-margin cars (the Models S&X) will be down by roughly 50% worldwide this year vs. their 2018 peak, thanks to cannibalization from the less expensive Model 3 and direct highend competition (especially in Europe and China) from the Audi e–tron, Jaguar I–Pace, Mercedes EQC and Porsche Taycan, with multiple additional electric Audis, Mercedes and Porsches to follow, many at starting prices considerably below those of the high-end Teslas. (See the links below for more details.)

And oh, the joke of a “pickup truck” Tesla introduced in November won’t be any kind of “growth engine” either, especially as if it’s ever built it will enter a dogfight of a market.

Audi e-tron vs Tesla consumer reports

Meanwhile, Tesla has the most executive departures I’ve ever seen from any company; here’s the astounding full list of escapees. These people aren’t leaving because things are going great (or even passably) at Tesla; rather, they’re likely leaving because Musk is either an outright crook or the world’s biggest jerk to work for (or both). In January Aaron Greenspan of @PlainSite published a terrific treatise on the long history of Tesla fraud; please read it!

Reliable?

In May Consumer Reports completely eviscerated the safety of Tesla’s so-called “Autopilot” system; in fact, Teslas have far more pro rata (i.e., relative to the number sold) deadly incidents than other comparable new luxury cars; here’s a link to those that have been made public. Meanwhile Consumer Report’s annual auto reliability survey ranks Tesla 23rd out of 30 brands (and that’s with many stockholder/owners undoubtedly underreporting their problems—the real number is almost certainly much worse), and the number of lawsuits of all types against the company continues to escalate– there are now over 800 including one proving blatant fraud by Musk in the SolarCity buyout (if you want to be really entertained, read his deposition!), an allegation that unsafe door handles caused a Tesla driver to burn to death in his car, and evidence that the company secretly rolled back battery performance without compensating owners.

So here is Tesla’s competition in cars such as the Audi e-tron (note: these links are regularly updated)…

Porsche Macan EV to get Taycan platform and tech

Audi e–tron: Electric Has Gone Audi

2020 Audi E–Tron Sportback debuts slick new roofline, a bit more range

AUDI E–TRON GT FIRST DRIVE: LOOK OUT, TESLA (available 2020)

Audi’s Q4 e–tron previews entry–level EV for 2021

Audi e–tron compact hatch to lead brand’s electrification plans

TT set to morph into all–electric crossover

THE AWARD–WINNING ALL–ELECTRIC JAGUAR I–PACE

Jaguar Land Rover readies electric XJ and Range Rover

Mercedes EQC electric SUV available now in Europe & China and in 2021 in the U.S.

Mercedes EQV Electric Minivan Revealed – Available 2020

EQB Small SUV to boost brand’s electric line–up

Mercedes EQS will be built in addition to the S–Class on a new dedicated electric platform

Volvo Polestar 2 Arrives 2020

XC40 Recharge, a 408–HP Electric SUV comes in 2020

Volvo confirms electric version of next XC90

Volkswagen unveils the ID.3, its first ‘electric car for the masses’

VW’s EV crossover for U.S. will be called ID4

VW Group to launch 70 pure electric cars over the next decade

258–Mile Hyundai Kona electric is available now for under $40,000

Genesis Electric Luxury SUV Coming in 2022

239–Mile Kia Niro EV is Available Now For Under $40,000

Kia Soul (available mid–2019) EV’s Range Jumps to 243 Miles

Kia Europe to have six pure electric models by 2022

All–Electric Ford Mustang Mach–E Delivers Power, Style and Freedom for New Generation

Electric Ford F–150 arrives in 2021

Ford to build two European EVs based on VW’s MEB platform

GM to Revive Hummer Name on New Electric Pickup Model

Chevrolet Bolt Now Offers 259 Miles of Range

GM’s Detroit–Hamtramck plant expected to build electric Escalade, Sierra

GM is transforming Cadillac into an electric brand

Nissan LEAF e+ with 226–mile range is available now

Nissan Ariya Electric SUV Concept Is Destined for Production

BMW 1 Series Electric Coming As Early As 2021

BMW iX3 electric crossover goes on sale in 2020

2021 BMW i4 details revealed: 80–kWh battery, 530 hp, 373–mile range

BMW’s 2021 iNEXT Returns In New Teasers Showing Prototypes Production

Rivian electric pickup truck- funded by Amazon, Ford, Cox & others- is on the way

Renault upgrades Zoe electric car as competition intensifies

Peugeot 208 to electrify Europe’s small–car market

Peugeot to offer EV version of new 2008 small crossover

Toyota and Subaru Agree to Jointly Develop BEV–dedicated Platform and BEV SUV

Mazda extends MX name to new MX–30 electric crossover

SEAT will launch 6 electric and hybrid models and develop a new platform for electric vehicles

Opel sees electric Corsa as key EV entry

Opel/Vauxhall will launch electric SUV and van in 2020

Skoda accepting deposits for electric cars

New Citroen C4 Cactus to be first electrified Citroen in 2020

FCA to invest $788M to build new 500 EV in Italy

Maserati to launch electric sports car

Bentley Will Offer Hybrid Versions of Every Car It Makes and Add an EV by 2025

Lucid Motors closes $1 billion deal with Saudi Arabia to fund electric car production

Meet the Canoo, a Subscription–Only EV Pod Coming in 2021

Two new electric cars from Mahindra in India; Global Tesla rival e–car soon

Former Saab factory gets new life building solar–powered Sono Sion electric cars

And in China the Audi e-tron, Volkswagen and others…

VW ramps up China electric car factories, taking aim at Tesla

SAIC Volkswagen to roll out 3 MEB–based EV models in 2020/2021

JAC–Volkswagen Launch SOL E20X, The 1st EV from the Joint Venture

Audi Q2L e–tron debuts at Auto Shanghai

Audi will build Q4 e–tron in China

FAW–Volkswagen’s Foshan plant said to produce e–tron Sportback

Hongqi starts selling electric SUV with 400km range for $32,000

FAW (Hongqi) to roll out 15 electric models by 2025

China’s BYD launches six new electrified vehicles

Daimler & BYD launch new DENZA electric vehicle for the Chinese market

Geely, Mercedes–Benz launch $780 million JV to make electric smart–branded cars

Mercedes styled Denza X 7–seat electric SUV to hit market

Mercedes ‘makes mark’ with China–built EQC

Daimler and BMW to cooperate on affordable electric car in China

BMW, Great Wall to build new China plant for electric cars

BAIC Goes Electric, & Establishes Itself as a Force in China’s New Energy Vehicle Future

BAIC BJEV, Magna ready to pour RMB2 bln in all–electric PV manufacturing JV

Toyota, BYD will jointly develop electric vehicles for China

Lexus to launch EV in China taking on VW and Tesla

GAC Toyota to ramp up annual capacity by 400,000 NEVs

GAC unveils new NEV offshoot dubbed HYCAN

Chevrolet’s new China–only EV is called the Menlo and it looks good

Buick Rolls Out First Electric Car for China

General Motors’ Chinese Venture to Sink $4.3 Billion Into Electric Vehicles by 2024

Nissan & Dongfeng to invest $9.5 billion in China to boost electric vehicles

PSA to accelerate rollout of electrified vehicles in China

Fiat Chrysler, Foxconn Team Up for Electric Vehicles

Hyundai Motor Transforming Chongqing Factory into Electric Vehicle Plant

Jaguar Land Rover’s Chinese arm invests £800m in EV production

Renault reveals series urban e–SUV K–ZE for China

Brilliance & Renault detail electric van lineup for China

Renault forms China electric vehicle venture with JMCG

Honda Debuts New Everus VE–1 All–Electric SUV, But Only For China

Honda to roll out over 20 electric models in China by 2025

Geely launches new electric car brand ‘Geometry’ – will launch 10 EVs by 2025

Mazda to roll out China–only electric vehicles by 2020

Xpeng Motors sells multiple EV models

Chery

China’s cute Ora R1 electric hatch offers a huge range for less than US$9,000

JAC Motors releases new product planning, including many NEVs

Seat to make purely electric cars with JAC VW in China

Iconiq Motors

Hozon

EV maker Bordrin skips flash, keeps real–car focus

NEVS launches electric–car output with Saab 9–3 platform in China

CHJ Automotive begins to accept orders of Leading Ideal ONE

Infiniti to launch Chinese–built EV in 2022

Zotye Auto to roll out 10 plus NEV models by 2020

Skywell makes inroads into China’s NEV domain

Continental, Didi sign deal on developing EVs for China

Mine Mobility (Thailand)

Summary

So in summary, Tesla is about to face a huge onslaught of competition with a market cap larger than Volkswagen’s or Ford’s and GM’s combined, despite selling around 400,000 cars a year while VW sells 10.5 million and Ford and GM sell 6 million and 8 million vehicles respectively, generating billions of dollars in annual profit.

Thus, this cash-burning Musk vanity project is worth vastly less than its roughly $124 billion enterprise value and—thanks to over $30 billion in debt, purchase and lease obligations— may eventually be worth “zero.”

Thanks and regards,

Mark Spiegel