Fintel’s QVF quant screen shows shares could be opportunity for long-term investors seeking maximum return

Activist investor Steamboat Capital has turned up the heat on CPI Card Group Inc (NASDAQ:PMTS) as evidenced in its amended Schedule 13D filing on Friday that revealed the New York-based investment manager has boosted its stake in the company to 6.2% from around 5% reported at the end of 2022.

Q4 2022 hedge fund letters, conferences and more

Find A Qualified Financial Advisor

Finding a qualified financial advisor doesn't have to be hard. SmartAsset's free tool matches you with up to 3 fiduciary financial advisors in your area in 5 minutes.

Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests.

If you're ready to be matched with local advisors that can help you achieve your financial goals, get started now.

CPI is a leading payments solutions provider offering credit, debit and prepaid debit card solutions and digital offerings. The PMTS stock price has been on a tear over the 12 months, rising more than 160% with shares trading around five-year highs after recovering all losses from late 2021.

Although the stock is trading significantly higher this year, the shares continue to trade on an undemanding price-to-earnings ratio of around 16x, which is cheap for a growth stock.

In the latest filing, Steamboat Capital disclosed that it is seeking to put its managing director and portfolio manager Parsa Kiai on the CPI board of directors. The fund delivered a letter on Feb. 24 to the company's board seeking his nomination for a vote at the upcoming 2023 annual shareholder meeting.

Recall that on Dec. 14, Steamboat's initial filing first disclosed it held a 5% stake and proposed the idea of CPI adding Kiai to its board.

While CPI is yet to publicly respond to Steamboat's request with public dialogue, we would expect to see a response prior to the shareholder meeting in May.

Regardless of the outcome, we looked a little deeper into the PMTS stock to see how it stacks up in Fintel's quantitative metrics analysis.

Research on the platform revealed that PMTS stock is screening highly on the QVF quant model leaderboard (quality, value, fund sentiment) in 120th spot with a score of 74.27. This particular model has been design to reveal opportunities for patient investors who want maximum returns over the long term.

The scoring model consists of a quality score of 82.03 based on the company’s strong cash flow generation from operating activities. This is explained by a strong operating cash return on investor capital which has strengthened over the last three years but has turned negative following the last results on Nov. 3.

The second factor is a value score of 62.59, which is the lagging factor in the quant model. With the stock price rallying faster than earnings growth, the PE ratio has increased to 15.8x.

The final factor in the quant model is the high Fintel fund sentiment score of 94.93. The score ranks PMTS in the top 1% when screened against 36,855 other global securities for the highest levels of institutional buying activity.

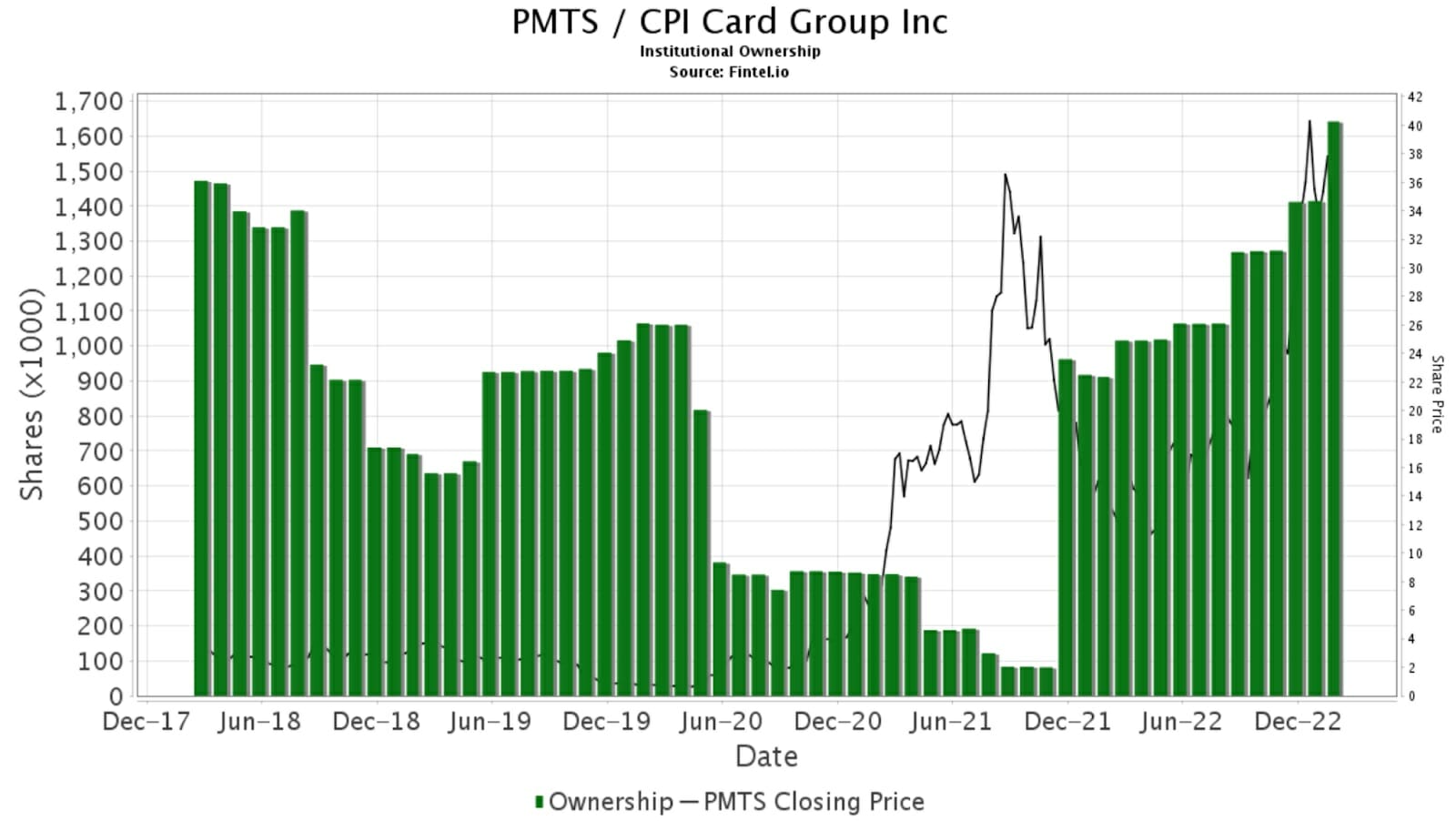

PMTS has 52 institutional owners on the register that collectively own 1.64 million shares or around 14.5% of the float. The largest shareholders on the register include: Steamboat Capital Partners LLC, Vector Capital Management, Vanguard Group Inc, UBS Group AG, EAM Investors LLC, BlackRock Inc, Geode Capital Management LLC, and Susquehanna International Group.

The chart to below illustrates the significant growth in fund buying activity over the last year after the stock retreated from its significant pandemic rally.

CPI Card Group will update investors again this week with the release of fourth quarter and full year results before the market open on March 8.

The Street is expecting sales of around $450 million for the full year, up 20% from the $375 million generated in 2021.

Lake Street Capital Markets analyst and director of research, Jaeson Schmidt, thinks the company can build on from the strong momentum built up over the last year and believes the company remains on its path to see continued sales and profit growth over 2023 and 2024.

Lake Street recently upgraded its "buy" call target price to $42 from $28, for almost 27% upside, for the year ahead on continued contactless card momentum.

Article by Ben Ward, Fintel