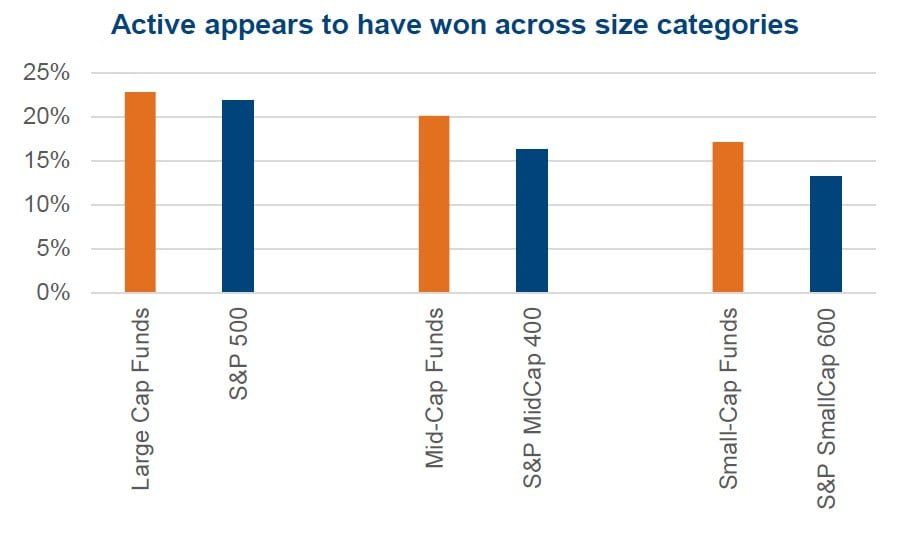

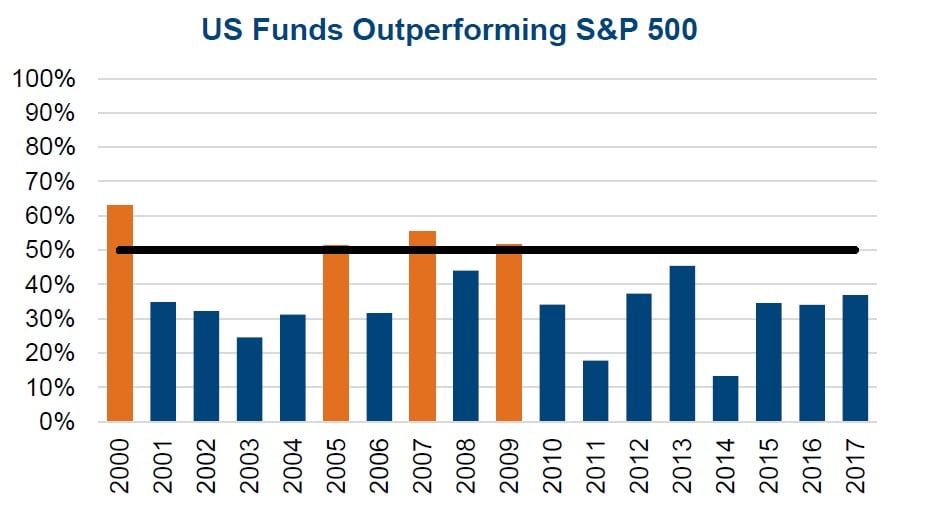

Sacrilege, right? Over the years, have we not been taught that actively managed funds simply don’t stand a chance against the index? Well something happened last year. According to the U.S. SPIVA report, 63% of domestic funds underperformed the index last year. However, on an asset weighted basis, all Large-Cap Funds returned 22.8% compared to 21.8% for the S&P 500. Asset-weighted is a fairer representation of what an investor experienced with their money. The first two charts below include the annual percentage of funds that outperformed the S&P 500 each year and the next one is the asset-weighted fund returns for large, mid and small cap. The outperformance on an asset-weighted basis was even greater among mid and small cap funds.

Check out our 2017 hedge fund letters here.

These results are actually surprising. Not just because most years see the index winning against most active managers, that has certainly been the trend of recent history. But who would expect active to beat passive in a year that had the S&P 500 up 21.8%, S&P MidCap 400 up 16.2% and S&P SmallCap 600 up 13.2%. The mega caps were big contributors last year, with the top ten companies in the S&P 500 representing 6% of the index’s 21.8% gain. Usually when the mega caps lead or contribute so much of the gains, it is simply harder for an active manager to outperform a market capitalizationbased index as they tend to be more broadly diversified. A good example of this is Canada at the moment. The two biggest companies in the TSX Composite are Royal Bank (6.8%) and TD Bank (6.4%). Even a fund manager that likes those two names, would not likely hold such a large position. Thus, if these two companies rock it, will be hard for many active managers to keep pace.

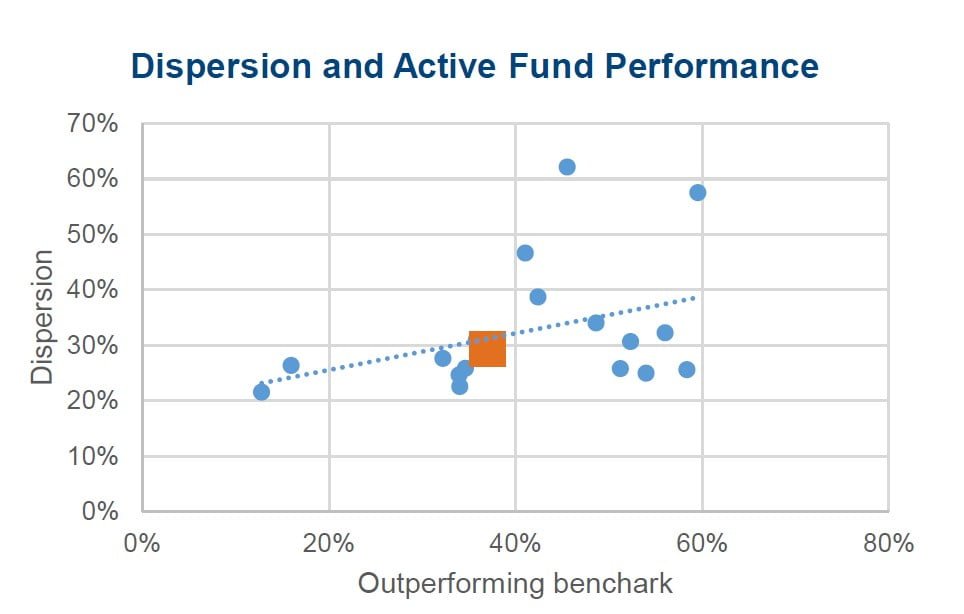

In the financial world, much time is spent trying to discover and explain what has happened. We could attribute Active’s decent year to rising dispersion in the index. Greater disparity does make it easier for an active manager with skill to add value. And one would hope the bigger funds based on assets, would be managed by some of the better or more skillful managers. The top chart on page 2 is the percentage of funds beating the index as a function of index disparity. 2017 saw the highest disparity since 2010. So far in 2018, this trend of rising disparity has continued. We measure disparity a number of ways. The chart is the percentage of S&P 500 constituents that beat the index by +25% or underperformed by -25%. Essentially the percentage of companies well outside a normal distribution. Sector divergence has also been rising. Safe to say, the index had been moving more homogenously for many of the past years, with all stocks moving more closely together. And now that appears to be loosening up, giving an advantage to active managers. Well an advantage if they can pick the big winners and avoid the big losers.

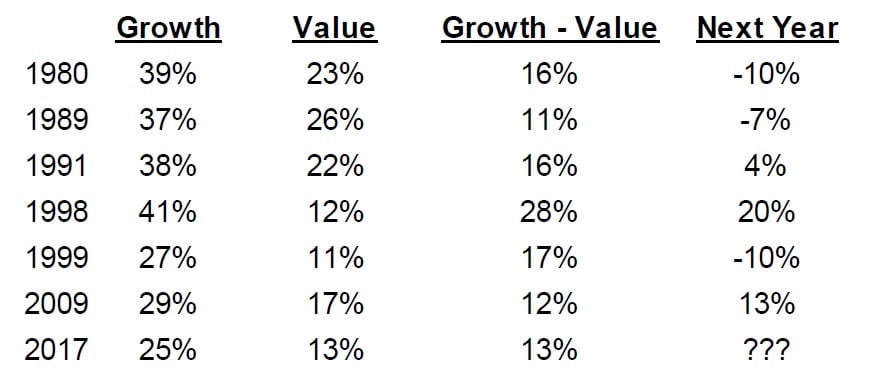

One area that saw the biggest divergence in performance was between value and growth investing. The S&P 500 Growth Index rose 25% in 2017 while the S&P 500 Value Index was up a mediocre 13% (mediocre and 13% rarely go together, 2017 was a good year). It is worth noting the market performance following years that saw growth dominate value by a material amount, has not done too well (table).

Don’t Bail on Passive

We remain fans of both active and passive management styles, for different reasons. Passive can provide broad market exposure at a very attractive price point from a management fee perspective. And we could easily see passive beat active in 2018 on an asset-weighted basis. After all, the assetweighted relative returns over the past 3, 5 and 10 years certainly still point to an historical period that passive dominated. If you believe in the trend, one counter year does not mean it has changed.

However, the sheer volume of money flowing into passive market cap-based ETFs over the past few years has likely caused some market distortions. We are aware that some companies, based on their index weight and liquidity, get pushed around more from ETF flows than other companies. And the index itself (S&P 500) has become riskier over the past decade. This has been a growth/momentum market for most of the past decade, which has caused those companies to now carry a higher weight in the index. This skewness reduces diversification and increases risk.

Still one can’t argue with the numbers. Allocating a portion of a portfolio to a passive lower cost solution has benefits.

Maybe Active Managers are Changing

The active fund industry has been changing significantly over the past few years. Fees have continued to come down, in part due to necessity. Approaches are changing too, with many asset management firms adding more quantitative capabilities. Another change that appears to be on the rise is actually the approach of active managers. Acknowledging any strategy that is similar to a broad index will be readily replaced with a lower cost index solution, many managers have now deployed strategies that are very different than the index. Either purposefully designing a strategy to better complement an index ETF within a portfolio, or determining the best strategy to beat the index based on its compositions.

The markets change over time due to technology, demographics and participants. Before 2000, most all equity investors were active in price discovery. Now HFT and ETF basket traders are dominant, with little or no price discovery. Not saying right or wrong, but when the investment landscape changes, successful investment strategies must adapt as well. This isn’t your grandpa’s market.

Article by Craig Basinger, Chris Kerlow, Derek Benedet, Shane Obata - RichardsonGMP

{kind=link}