Spruce Point Capital Management, LLC (“Spruce Point” or “we” or “us”), a New York-based investment management firm that focuses on forensic research and short-selling, today issued a detailed report entitled “Mr. Irrelevant… It Doesn’t Take A Genius” that outlines why we believe shares of Genius Sports Ltd (NYSE:GENI) (“Genius” or the “Company”), face up to 60% to 80% long-term downside risk, or $3.25 – $6.50 per share.

Q2 2021 hedge fund letters, conferences and more

Genius Sports: 55 Million Reasons To Sell In The Near-Term

Genius Sports (“GENI” or “the Company”), a provider of live sports data from its partnerships with sports leagues to sportsbook customers, has recently gone public through an acquisition by DMY Technology Group (DMYD), a special purpose acquisition company (SPAC). While the market’s current view of Genius reflects the growth of the sports betting industry, in reality, our view is that Genius is just another intermediary that provides similar data to its competitors and will likely fail to capitalize on the wider industry growth. Spruce Point has conducted an in-depth analysis of Genius including speaking with various industry experts and analyzing partner contracts. A sports data providers’ competitive advantage is its key exclusive rights (NFL & Premier League for Genius), which Genius is paying considerable fees for. In the case of the NFL rights, a Sportradar executive explains that Sportradar was unable to justify the price Genius is paying the NFL. We find exclusive rights are only valuable for live/in-game betting and less so for the majority of wagers placed on the final result of matches.

Our research suggests Genius’ business is under pressure and struggling to achieve its high growth targets after the initial one-time boosts from purchasing the exclusive rights. Genius’ bull thesis revolves around a stated 5% revenue share rate of gross gaming revenue (GGR). Our research shows this figure is more than double the current market rate and typically only applies for exclusive data rights. We have significant concerns regarding the Company’s “noncash” revenues, a result of contra/barter deals with sports league partners where services are provided “at no cost” in return for rights to league data, that may result in inflated revenue and may lead to future financial reporting issues. In addition, we believe investors may be misguided by potential “fake news” around growth opportunities, including betting revenue from NCAA events where Genius does not own the betting rights. We believe Genius’ shares have significant long-term downside to our price target range of $3.25 – $6.50 per share, a discount below the $10 acquisition price where its previous private equity sponsor sold shares in its IPO. In the near term, we believe there could be up to 55m shares of GENI that could be sold. We estimate 35m insider shares become unlocked next week after a 60-day period following the June 21st equity offering, 11.2m NFL warrants are exercisable through next week, and 9.2m public warrants can be exercised on August 18th.

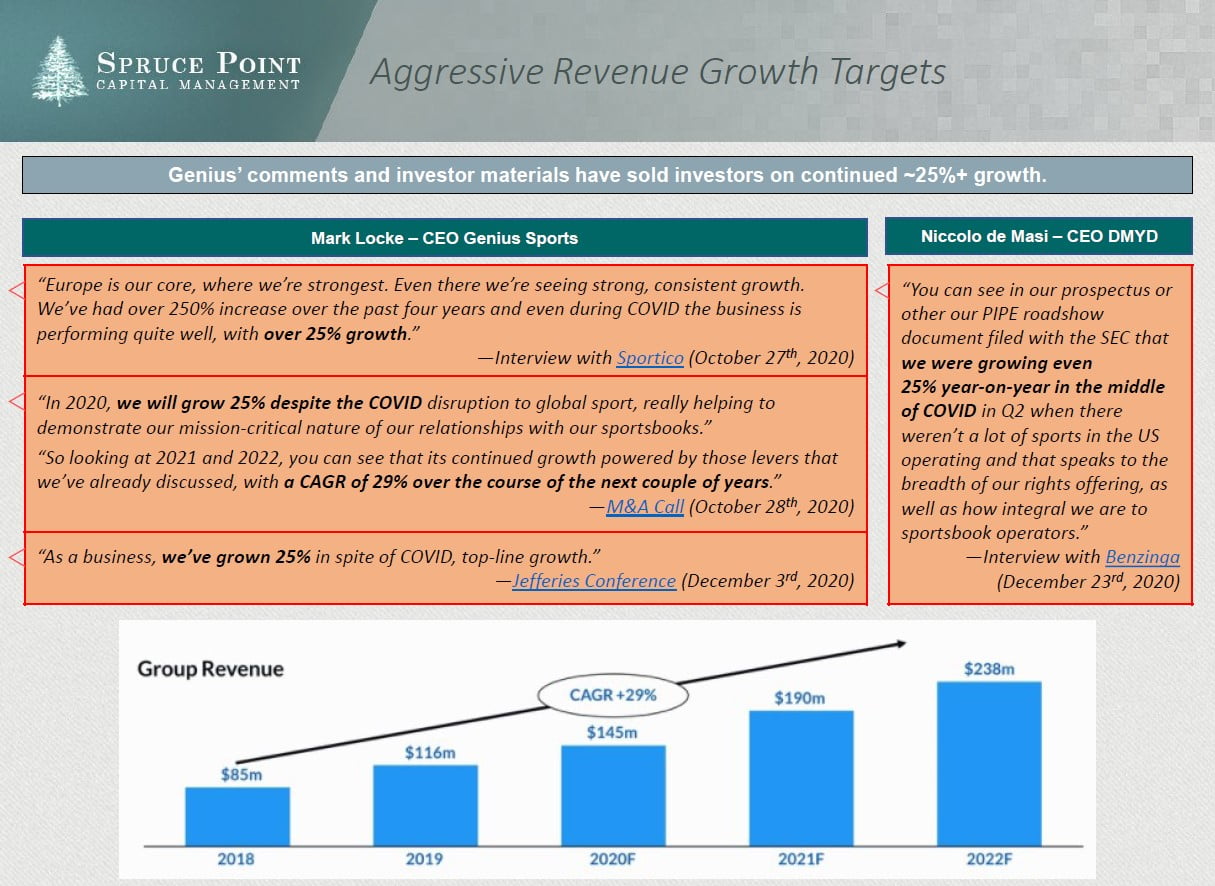

We believe Genius Sports, an overhyped revenue growth story assumed to benefit from the broader sports betting market, is facing competitive pressure and is unlikely to achieve its stated 25%+ growth targets

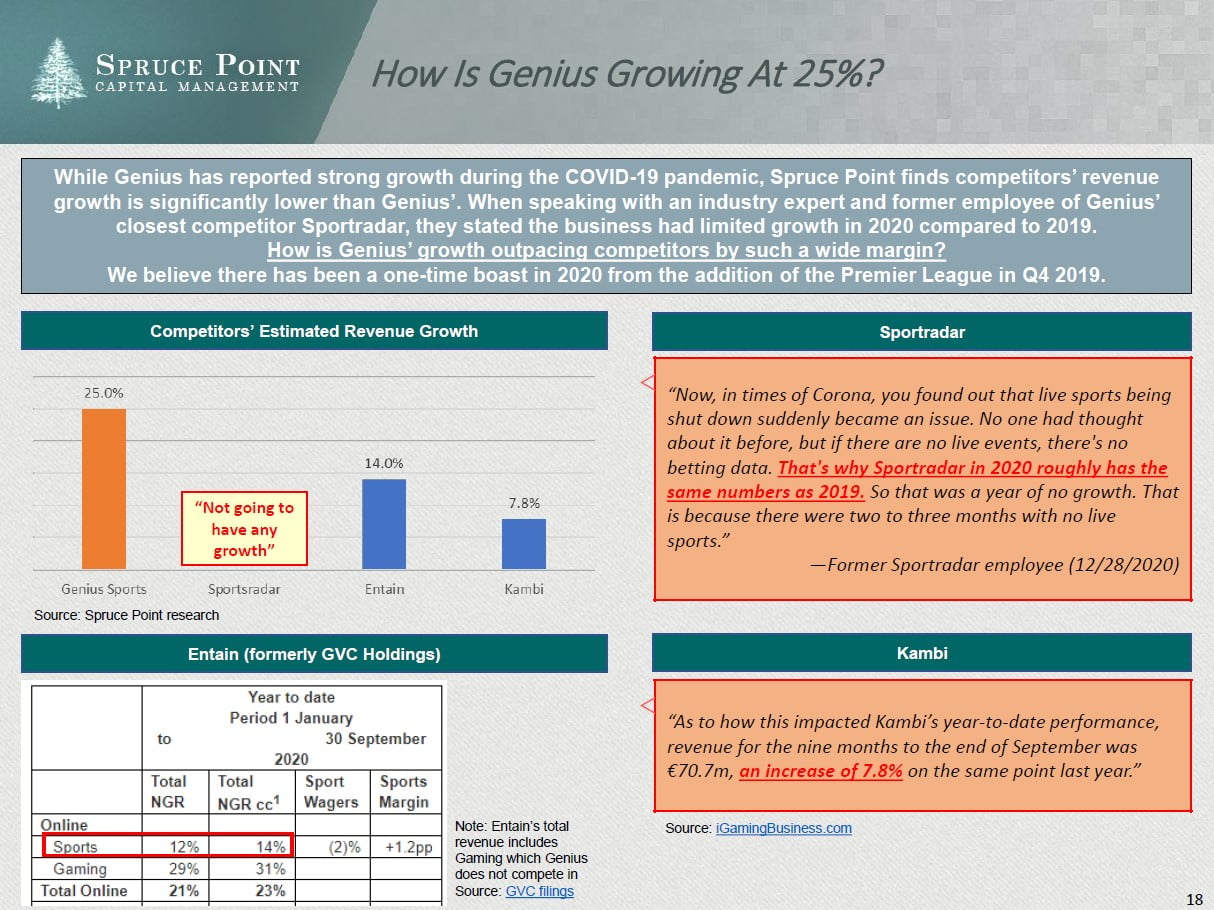

Despite lower revenue growth by competitors in 2020, Genius reported revenue growth of 30% for 2020

- We believe this growth is likely a result of a one-time benefit driven by the new Premier League partnership

Genius’ competitive advantage and main driver of 2020 revenue growth is its exclusive Premier League rights which are expensive at a cost of ~$14m/yr

- Genius is facing an anti-competitive lawsuit from Sportradar relating to The Premier League contract, a risk to Genius’ major source of revenue

Genius purchased the NFL rights for ~$120 million per year including equity

- Based on our research, Genius likely overpaid for the rights as competitor Sportradar did not find the price economical.

Our research shows a significant disconnect between management’s guidance and reality

- $60bn Total Addressable Market includes pre-match betting (we estimate ~30%) where it is hard to charge revenue share as there is no value in exclusive data

- We believe revenue shares are typically in the range of 1.5%-2%, for tier 1 exclusive deals

- Growing competitive pressures from sports leagues and sportsbooks will likely pressure margins

Disintermediation Risk: a customer told us they plan to directly approach sports leagues to “break the model” and eliminate the middleman

“This is definitely a possibility. Another guy and I within the company have already been tasked to go direct, to approach the actual source of the data and see if we can do direct deals.” “You can get more from us and our competitors and we can pay less because there is no middleman to be paid…” “Its all doable, its not even near impossible.”

Genius is not a “bet on every horse”, it’s a bet on being able to secure exclusive, yet expensive, sports league rights

- We believe the value of U.S. sports league data rights will be high enough that they will be unprofitable for data providers as the economics are captured by the leagues. The price of the NFL rights will likely put significant pressure on Genius’ bottom-line for the next few years

- Genius’ NCAA rights are for media and not betting purposes, and it is unlikely the NCAA will venture into sports betting to protect its athletes

- Competitor Sportradar has high profile investors including multiple NBA Owners (Michael Jordan, Mark Cuban, Ted Leonsis)

- While investors may draw comparisons between Genius and high flying DraftKings (DKNG), DraftKings and other consumer focused brands appear better positioned to benefit from industry growth including the opening of sports betting in the United States

- We believe Genius lacks a competitive edge, is required to pay large sums for exclusive U.S. data and faces competition

- While DKNG grew revenue 90% in 2020 and expects 2021 growth of 63-79%, this is likely a result of investment in operating expenses, an investment GENI is unlikely willing to make. DKNG experienced monthly paying user growth of 114% in Q1’21

- Genius compares itself to “Online Gaming” peers, however, we believe these consumer-focused companies are not direct peers to Genius

- Genius’ key revenue driver is sportsbooks customer growth while online gaming peers will benefit directly from the growth of dollars waged. It is unlikely sportsbooks will be willing to concede meaningful economics to data providers, especially for non-exclusive data

- We believe these peers are better positioned to capitalize on the opening of sports betting in the United States

Revenue attributed to “noncash consideration”, a result of value-in-kind / contra deals (i.e. barter transactions), raises significant concerns regarding Genius’ revenue recognition and reported / forecasted growth

- Red Flag: industry experts have told us 11% of revenues from leagues seems high; Sportradar’s revenue from leagues is at most 5%

- As part of contra deals, Genius exchanges its services (e.g. software) for the rights to leagues’ data and sells the data to sportsbook customers

- Genius likely records the assigned values of these provided services as revenue

- Our biggest concern is management’s ability to potentially manipulate the “fair value” assigned to these services, inflating revenue and growth

- Red Flag: from our conversation with a former Genius Sports Manager, it is unlikely that the sports league partners have the means to pay the assigned values of Genius’ services stated in the partnership contracts

We believe Genius shares are a poor risk / reward with unrealistic growth assumptions

- Genius’ recent share price performance has been the result of investors flocking to companies with sports betting exposure

- It is highly unlikely Genius will ever live up to the baked in expectations that justify its current valuation

- Genius has become extremely expensive on a revenue multiple basis since its merger with DMYD

- At the time of the deal, with revenue growth guidance of 25%+, Genius may have appeared cheap at 7.4x 2021E and 5.9x 2022E revenues

- Genius’ private equity owner decided to sell at what appeared to be a discount to market for unexplained reasons

- GENI now trades over 13x 2021E revenues

- We believe these are unsustainable levels as it appears growth has slowed after the initial benefit from the Premier League

- Current share price reflects multiples of “online gaming” peers whose revenue growth is higher with a different customer base

- Spruce Point believes Genius’ shares have significant downside to our price target range of $3.25 -$6.50 per share, below the $10 acquisition price where its previous private equity sponsor sold shares in its IPO

Read the full report here by Spruce Point Capital Management