Scott Fitzgerald wrote in his 1936 essay, The Crack Up, that “the test of a first-rate intelligence is the ability to hold two opposed ideas in the mind at the same time, and still retain the ability to function.” He continued, “one should, for example, be able to see that things are hopeless and yet be determined to make them otherwise.”

For the last few years, we’ve viewed U.S. stock markets as expensive and priced to deliver subpar long-term returns. At the same time, we’ve held constructive near-term, 1- to 2-year views on markets. This dual view has served us well, as we’ve provided alpha over our benchmark not just since inception, but over the last 1-, 2-, and 3-year periods, even as we’ve become increasingly negative on the future return prospects of broad markets.

To be clear, we are not suggesting that our portfolios will mirror the low returns we expect out of stock indexes. We don’t own the stock market. Instead, we own a small collection of stocks that we’re confident will provide superior, long-term returns. Plus, we have risk management tools that traditional, long-only investors do not.

That said, our investment opportunity set is to some extent influenced by market valuations, and market movements can weigh on our securities, even though we’re positioned quite differently. Therefore, our broad market framework helps us to better understand the investment landscape and to manage (and capitalize on) risk.

OUR DUAL VIEW: MARKETS TODAY OFFER SHORT-TERM GAINS, BUT LONG-TERM PAIN

We still expect the U.S. economy to expand for at least a year or two more. Looser regulation and tax cuts should boost growth over the next 12 to 18 months. Housing construction, which has typically led the economy, continues to grow, and building permits remain below long-term averages. Corporate after-tax profits are at all-time highs and are still growing. Economic growth overseas is also accelerating, which improves growth here. And most critically to our dual view, we see no signs of an impending recession, the very things that have historically stopped bull markets in their tracks.

So, the ongoing economic expansion should provide the necessary environment to keep investors buying stocks for the next couple of years, even though they are, in our opinion, overpaying for most of them. That’s our short-term constructive view.

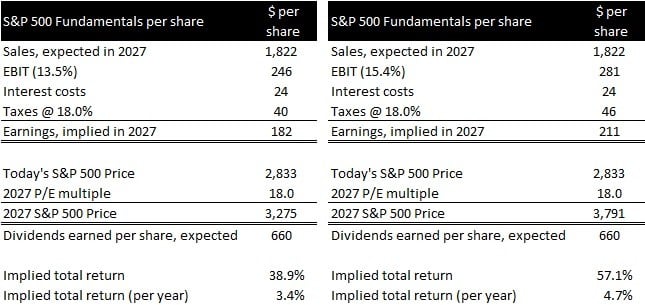

On the other hand, traditional, long-only investors, particularly those in U.S. stock index funds, are likely to earn average returns between 3% and 5%, at best, over the next decade. See Exhibit 1 below.

Exhibit 1: S&P 500 10-Year Expected Returns, Average (13.5%) and Late Cycle (15.4%) EBIT Margins [1]

Source: S&P; Black Cypress Capital Management

NEW CHALLENGES

It is, however, becoming increasingly difficult to justify our dual view. U.S. stocks are now trading for 20 times the consensus 2018 reported earnings estimate of $140 per share, well above the historical average of between 16 and 17 times forward estimates. And while 20 times expected earnings is high by historical standards, we think the underlying earnings estimates themselves are also becoming increasingly aggressive, which is where our dual view is now being challenged. Take the consensus estimate of $152 per share for 2019 S&P 500 reported earnings.

To hit $152 per share in earnings, S&P 500 operating margins need to expand to about 15.0%. Broad market operating margins of that level and higher do occur, though they’re lower than that more than 85% of the time. And margins of that level have historically coincided with near-peak earnings and an economy only a couple of years away from topping out.

Margins surpassed 15.0% for about a year and half prior to the 2000 peak, and for a couple of years prior to the 2007 peak. In both instances the economy was operating at maximum–though unsustainable–profitability, and margins fell by at least half within a couple of years.

If we assume 2019 estimates of $152 per share are accurate–and we think they’re achievable–expected total returns over the next two years would be calculated to be basically flat, as Exhibit 2 shows. That is, even with high operating margins, low interest costs, and the new lower tax rates underpinning 2019 estimates, the market has more than priced it in. This reality is the challenge to our ongoing dual view.

Exhibit 2: S&P 500 Analysis, 2019 Consensus Reported Earnings Estimates

Source: S&P; Black Cypress Capital Management

BEST-CASE AND BUBBLE SCENARIOS

Of course, these estimates could be too conservative. Operating margins might expand to new highs. And investors might be willing to pay higher and higher multiples of earnings. Those are “risks” if you’re conservatively-positioned or short, at least while margins and multiples hold.

During the last two economic expansions, operating margins peaked at 16.1% in the third quarter of 2000 and at 17.6% in the second quarter of 2007. If we assume that operating margins reach a new all-time-high by year-end 2020, markets may well return another 25% to 20%, noted in Exhibit 3.

Exhibit 3: S&P 500 Analysis, New EBIT Peak by 2020

Source: S&P; Black Cypress Capital Management

One could go all in bullish and assume that operating margins not only reach new all-time-highs by 2020, but are also accompanied by above average P/E multiples, of say 20 or higher. Markets topped out with an 18 multiple at the 2007 peak, though the technology bubble ended with a mid-20s P/E.

New all-time-high margins and a 20 P/E might drive the S&P 500 up to 3,700, another 32% return from today’s 2,803 level. This bullish scenario is not our target for the S&P 500, but we are cognizant it’s a possibility. But that level would, in our opinion, represent a full-blown bubble.

THE HOPELESS REALITY

The problem with price targets built on high teen operating margins, at least to us, is that they are likely to be short-lived, even if realized.

Exhibit 4: High Returns into a Cycle Peak Possible, but Long-term Returns Still Subpar

Source: S&P; Black Cypress Capital Management

Operating margins did touch 17.6% in 2007, but they marked the peak of the cycle, not some newfound level of profitability. In fact, it took until 2016, nine years later, before the same level of operating income was earned again. Earnings per share did regain the 2007 level by 2011, well before operating profits regained 2007’s peak, but that was due to unprecedented monetary policy on the part of the Federal Reserve, which reduced corporate interest costs by a whopping 60%.

The majority (over 69%) of earnings growth from the 2007 peak to 2018 will have come from reduced interest costs and falling tax rates. Operating profits, on the other hand, are only up about 1.0% per year since 2007. When operating profits peaked in 2007 at a 17.6% margin, they peaked for nearly a decade.

Exhibit 5: S&P 500 Earnings Growth Analysis

Source: S&P; Black Cypress Capital Management

Moving forward, earnings growth is going to have to come from gains in underlying corporate operating profitability, because interest cost reductions and corporate tax cuts are now behind us. So, when operating margins do peak again in the years ahead, monetary and fiscal policy won’t be as effective to bail out investors like last cycle.

Our view is therefore that the exceptional returns of late have largely pulled forward returns investors would have otherwise earned in the years ahead. While markets may continue to climb to new heights, they do so on the shaky foundation of high operating margins and above-average P/Es. And that’s a recipe for disaster.

And so, Mr. Fitzgerald’s quote resonates with us today. We think future long-term stock market returns will be hopelessly low, and yet we’re determined to make it otherwise for our clients.

[1] In each of our 10-year return scenarios, we assume sales grow 4.0% per year, dividends grow 6.0% per year, interest costs remain near current lows, tax rates decline under the new corporate tax rate structure, and P/E multiples normalize to the long-term historical average of 18.Article by Alan Hartley, CFA - Black Cypress Capital