In his latest strategy note, Alastair George, the Chief Investment Strategist for international investment research and consultancy firm Edison Group, gives his outlook on global equity markets and explains why he believes the risk/reward for global equities now only justifies a neutral position on valuation grounds. Below is an excerpt from the report.

[soros]Q4 2020 hedge fund letters, conferences and more

Global Perspectives: Valuation-Led Downgrade

- Global equity and credit markets now offer relatively little risk premium for bumps on the road towards a post COVID-19 recovery. It is remarkable at a time when much of the developed world continues to face a significant degree of COVID-19 disruption and is operating well below trend GDP that forward US price/book (P/B) multiples are at a 12-year record high and the risk premium for corporate credit risk is at cyclical

- Evidence of speculative excess in pockets of the equity A bumper period for equity issuance highlights the current demand for risk by investors. A surge in valuations for more speculative companies also lends weight to the idea of a bubble forming in certain sectors. We believe it is time for investors to stick to a value-based discipline as valuations for the world’s fastest growing stocks have surged.

- Vaccines offer hope but no guarantee of a return to ‘normal’ in the short or medium The emergence of new and more contagious strains of COVID-19 highlights the new reality that despite vaccine programmes, social restrictions may be in place for rather longer than expected as recently as December. Outside developed markets vaccination has been negligible which highlights the medium- term challenges facing the travel industry.

- Continued K-shape recovery. COVID-19 has resulted in a step-change in the nature of economic Digital economic interactions have grown and the shift towards the 21st century economic objectives of new energy and environmental protection have accelerated. These sectoral shifts should be reflected in portfolio asset allocations in our view as they are likely to persist even after the acute phase of the pandemic.

- Global equity markets have risen since December even as the likely duration of pandemic disruption has increased. While we started the year with a positive outlook on equities, the risk/reward balance is tilted back towards neutral. We now favour relatively COVID-secure and less cyclical sectors, preferring to accept lower expected returns for greater predictability. We remain of the view that bond yields will face upward Inflation expectations may have increased but real rates remain at record lows.

Valuations drive equity downgrade

Since the turn of the year, the race between the deployment of effective vaccines and the evolution of new, more contagious variants of COVID-19 has tightened considerably. Across the US and Europe there has been a steady drift towards longer lockdown restrictions as case numbers and hospital admissions have remained stubbornly high. For the listed corporate sector there is still a significant degree of cushioning provided by fiscal support for demand and the ability of larger companies to continue to operate under COVID-secure protocols compared to the SME sector. This cushioning has contributed to the resilience of 2021 consensus earnings forecasts despite the extended lockdowns now in place.

Due to the recent resilience of corporate earnings, in our view the risk is growing of a mis-placed confidence that the second wave of COVID-19 will represent the end of the affair. A more likely scenario at this time is that social restrictions will be removed only slowly across developed markets during 2021. Furthermore, international travel will remain significantly impeded by requirements for quarantine, regardless of vaccination or test status. Outside developed markets, vaccination programmes are moving only slowly. While it is easy to state that on the projected vaccination programme delivery much of the developed world will have received immunity by late 2021, this does not mean that social restrictions can be fully lifted.

For example, the extent to which vaccination prevents asymptomatic transmission is not well understood as confidence intervals in existing trials are large and further studies are necessary. The enhanced reproduction rates for new variants of COVID-19 point to very demanding levels of vaccination of 80% or more before social restrictions could be fully removed. Given the transmissibility of new variants, COVID-19 appears unlikely to be eradicated at this stage. The prospect of new variants in unvaccinated populations in developing nations may require an ongoing annual vaccination programme, similar to that of influenza.

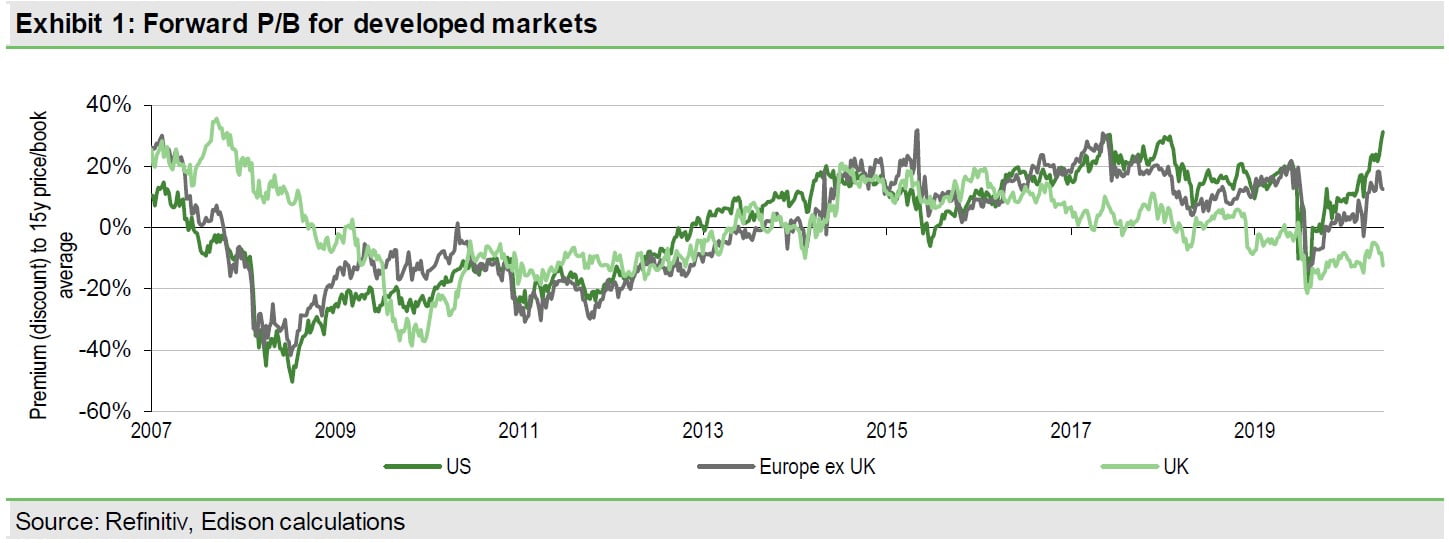

Despite this scenario of an enduring impact from COVID-19, the global appetite for risk assets has only strengthened. In our view this tilts the overall equity risk/reward balance back to neutral from the positive outlook we expressed at the turn of the year. We note that market P/B valuations in the US are now at 12-year highs while continental European valuations have seen a full recovery from the sharp declines at the early stages of the pandemic, Exhibit 1. We note that UK markets still languish some way below their 15-year price/book average due in part to the years of uncertainty created by Brexit.

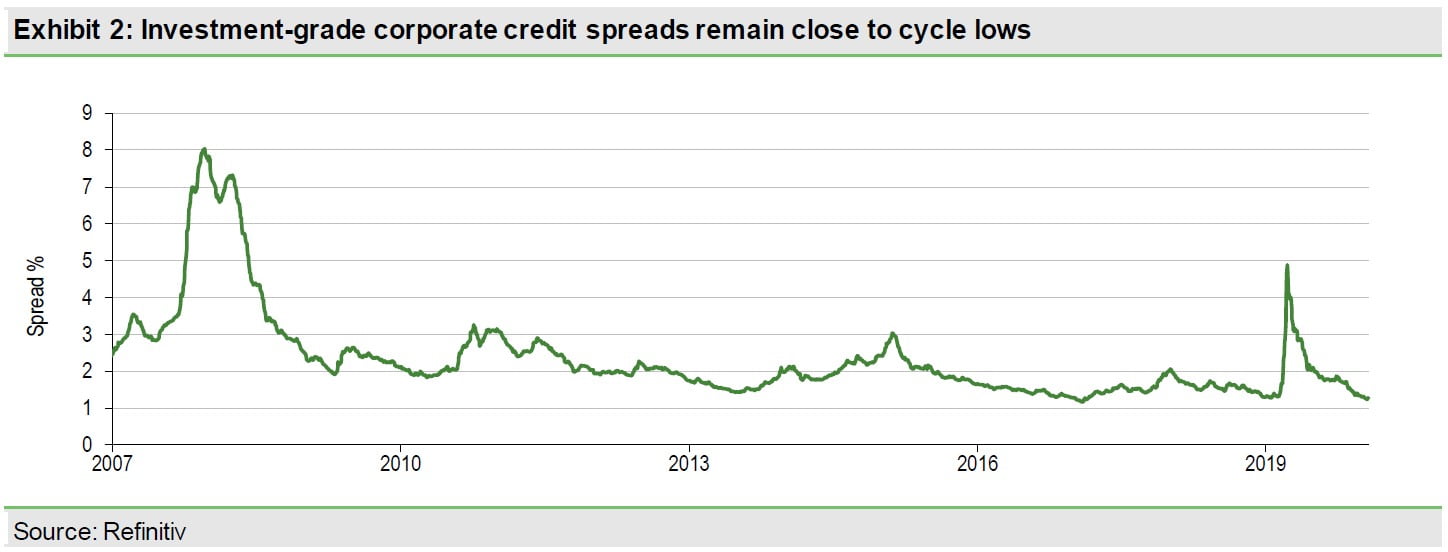

Within corporate credit markets the impact of central bank policy and the fiscal support for the economy has been clearly felt. Policies designed to prevent a credit freeze have resulted in credit risk premia, as represented by the difference in yield between risky and risk-free bonds, narrowing back to 15-year lows. This is a remarkable feat at a time of such economic uncertainty, especially given the increasing levels of leverage within the corporate sector in recent years.

Recent evidence of speculative activity in markets, such as outsize gains for early stage or unprofitable US technology companies, highlights the turn in sentiment since the investor panic of Q120. For years during the long US bull market, investors have been comforted by the relative absence of retail investors as a sign that markets had not yet peaked. Since the pandemic there has been something of an explosion in retail trading, as evidenced by the number of small lots being traded in US markets, and the surprising performance of more speculative securities.

With both equity and credit markets buoyant, if not effervescent at times, further stimulus from central banks remains unlikely in the short term.

……………

Conclusion

We believe the risk/reward for global equities now only justifies a neutral position on valuation grounds. It is remarkable in many respects that we would downgrade equities on a valuation basis at a time when much of the developed world continues to face a significant degree of COVID-19 disruption and is operating well below trend GDP. Nevertheless, since our last outlook global equity indices have risen while at the same time new, more transmissible variants of COVID-19 have been discovered and the probability of a long period of disruptive social restrictions extending well into 2021 has increased.

With the fastest-growing companies trading at record-high valuations, investors should in our view focus on companies that meet traditional valuation criteria but are also on the right arm of the ‘K’ shaped recovery. This includes companies that may be slower growing but as importantly, are not struggling. We understand this may narrow the universe of potential investments, but it is in our view important to remain focused on growth, where it can be obtained at a reasonable price.

In terms of government bonds, the still ultra-low real rate on offer highlights that the bond market has still not bought into the recovery while inflation expectations have risen. We expect further upward pressure on yields during 2021 and would remain underweight.