Whole Foods Market, Inc. Market Update – Did I Make a Mistake?

Written by

Jae Jun

follow me on

Whole Foods Market – What You’ll Learn

- What’s happening with Whole Foods?

- Are the fundamentals broken?

- My updated intrinsic value ranges

- Whether to sell or hold Whole Foods (it’s definitely not a buy)

I’ve been holding Whole Foods for close to two years now and it’s one of my bigger losers.

In fact, it’s brooding at me with its ugly blood shot eyes, flashing -32%.

Not a position I want to be in.

However, one rule of thumb I learned early was not to throw in the towel too early for good companies.

By good, I’m referring to companies that has a proven record of delivering, has strong numbers relative to industry peers with a competitive advantage.

Give it at least 3 years to see how it works out because it takes time for systems, processes and new business strategies to propagate throughout the company and make its way onto the financial statements.

But I want to revisit and explore Whole Foods Market again.

First – Does Whole Foods Fit the Selling Criteria?

To reduce eliminate overreactions or emotional decisions with losing positions, I take it through a simple selling checklist.

Here’s a very high level version of when I sell

- made a crucial mistake when analyzing a company. e.g. didn’t notice huge off balance sheet debt, lots of insider transactions or non-accountable board of directors

- fundamentals are damaged

- found a better opportunity that I need to buy with conviction

- stock price is over my intrinsic value calculation and exceeds expected growth

The question is, does Whole Foods fit any of these 4 points? Two years in, it’s definitely not #3 or #4, so let me focus on #1 and #2.

Question #1. Did I Make a Crucial Mistake (regarding competition)?

Here are my two articles that I wrote about Whole Foods.

- Whole Foods Market is a BMW. Stop Comparing it to a Kia.

- What Whole Foods is Worth Today and What That Means for Shareholders

One year after I wrote the second article, I was up 50% at that point. My main mistake was not taking some money off the table.

I’ve always been a bad seller. I tend to get lazy and complacent. It improved a lot in 2015, but I still made mistakes here and there.

Getting back to the question.

Whole Foods situation 1 year ago when I was up 50% vs today, down 30%, is largely the same.

As I said, a company of this size doesn’t change overnight and the signs of competition was always there. So it’s not something I overlooked.

The argument could be that I discounted the competition too much. That I overestimated the value of its brand and moat.

Until last year, same store sales were doing quite well.

Now?

Same store sales are down as the average price per basked dropped slightly as a result of discounting and also changing up pricing for some items.

Recent bad press related to overcharging New York residents and backlash to selling pre-peeled oranges is not helping.

In the two weeks after the [New York] announcement, comparable-store sales growth fell to just 0.4 percent, after running on average at 2.5 percent in the weeks before the findings were released. – NYT

Wall Street analysts are negative on the company again. Worried that competition (Sprouts, Wegmans, Trader Joes) are eating its lunch and mainstream retailers (Kroger, WalMart, Safeway) eating more of the pie as well.

My initial reason for investing in Whole Foods wasn’t for growth. I categorized it as a Buffett+Munger type investment.

A quality company at a fair price.

Competition is real in the organic and natural industry. Healthy eating and living habits are beginning to be ingrained in the minds of US consumers.

Fierce competition is clearly forcing Whole Foods to come up with new growth strategies like opening up the 365 stores, somewhat similar to a Trader Joes.

According to management, it’s the same concept as what Nordstrom Rack is to Nordstrom.

Whole Foods Market will be the site where you can find everything with a wide variety of the best of the best.

The 365 stores will be less expensive to build, deploy more technology and be more self-service than Whole Foods stores. By utilizing its supply chain better, it will lead to increased efficiency and lower costs.

More than 90 percent of the product selection and pricing for 365 will be set centrally, from Whole Foods’ offices in Austin, Tex., whereas such decisions are made for Whole Foods stores by regional teams and even at a store level.

And if you think lowering prices at Whole Foods is going to solve the problem, think again.

Wall Street analysts have never run a business. They have no operational experience and have zero ideas on what consumers want.

Short term solutions like lowering prices across the board will likely jeopardize the company further and it’s going to take a lot more than that to change the “whole paycheck” image.

In an interview John Mackey points out that

The Whole Foods Market brand may never shake that label

In fact, it can take over a decade for a company image to change.

It took Hyundai more than 10 years to change its image from a low quality, cheap Asian car, to now one that customers recognize as high quality at a reasonable price.

Not to mention the millions of dollars it poured into advertising.

Walter Robb knows that lowering prices won’t fix everything and it’s not who they want to be.

Walter Robb, the other co-chief executive, argues that Wall Street’s relentless pressure on the chain to reduce prices is “a race to the bottom.”

“Sure, we could sell cheaper farmed salmon — but it’s terrible for the environment,” Mr. Robb said. “Our products are not the same” as what other grocers are selling.

On a different note, I was driving around Seattle a couple of weeks ago and drove past a Whole Foods Market with the words “Serving the Seattle Community Since 1996? on the side of the building.

Whole Foods Market isn’t immune to business cycles and competition. Many retailers closed down during the recessions, but Whole Foods has managed to survive and thrive past each difficult period.

If you ask me whether Whole Foods will be around for 20 years down the road, my answer is “yes”.

Question #2. Are the Fundamentals Damaged?

Whole Foods still has strong positive FCF to finance new stores and expand with the 365 concept. They are spending at a blistering pace. Frankly, they have never spent money this fast on growth.

Look at the numbers to see how quickly they are expanding. The arrow refers to the development cost of new locations.

WFM Growth Capex Numbers | Enlarge

For 2016, management is targeting the following

- Sales growth of 3% to 5%;

- Approximately 30 new stores, including three 365 stores and two to three relocations;

- Square footage growth of 7% or greater;

- EBITDA margin of approximately 8.5%;

- Capital expenditures of 5% of sales; and

- ROIC greater than 13.5%.

But I am concerned.

Margins have come down and is expected to be lower in 2016 as a result of lowering prices.

Same store sales in the latest quarterly results fell again which underlines the current weakness.

The growth in spending proves that there are cracks showing in the walls. Whole Foods is working on getting it patched up before it becomes a gaping hole.

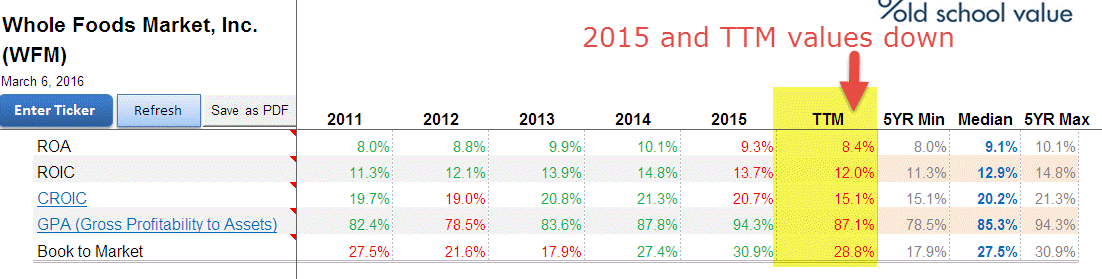

Looking at the latest numbers for ROIC and CROIC, it’s down from 2014. TTM numbers show that 2016 will be lower.

Whole Foods has a high Gross Profit to Asset ratio of 87% which looks at how profitable the company assets are in generating profits.

- Kroger has a TTM GPA of 75%

- Costco GPA is 43% (different business model though)

- The Fresh Market GPA is 111%

- Sprouts GPA is 73%

Fundamentals have weakened, but not damaged.

My Whole Foods Market Intrinsic Value Update

2 years back, my estimate for fair value was between $38 to $50.

Today, it’s more like $32 to $36.

Whole Foods must believe their stock price is cheap relative to where management believes the company will be, because they have taken on $1B in debt to repurchase their stock.

No need for Carl Icahn on this one as the share count has already dropped 6.7% per the last quarterly report. EPS obviously gets a boost when the share count is lower.

Comparing my new intrinsic value ranges, there’s no denying that it’s a large drop in intrinsic value as a result of weakened fundamentals.

Ben Graham was right when he said to buy with a margin of safety.

But how did I get the $32 – $36 range?

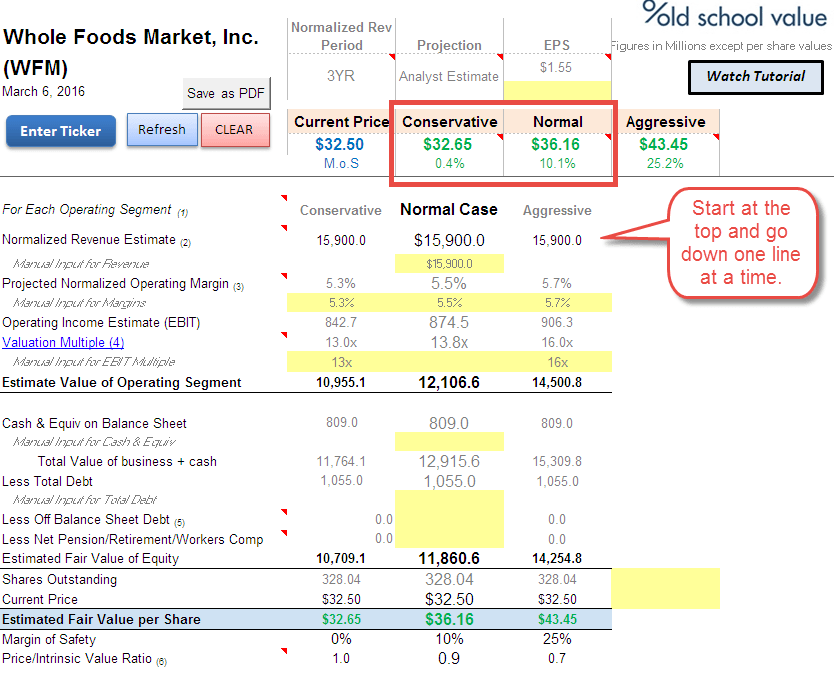

You can follow along by hand, but I’m using my Old School Value Analyzer as a shortcut with the 2016 guided numbers.

I’ve got an online EBIT calculator you can play with. Here’s a short tutorial video explaining how it’s done.

Here are the steps:

- Sales growth of 3% is $15.9B rounded up from last year numbers.

- EBITDA margin of 8.5% translates to about 5.5% in EBIT for WFM. I know this because it’s historically been 3% lower. An example of how long term numbers give you insight into the business.

- Over the last 5 years, the lower end of EV/EBIT multiple is 13x, median is around 14x and high end is 16x.

Follow the screenshot below to get the operating value of the company.

Then add the cash portion and subtract the debt to get the final equity value.

My conservative valuation assumptions

- $15.9B sales

- 5.3% EBIT margin

- 13x EV/EBIT multiple

- $32 fair value

The normal case assumptions based on management guidance

- $15.9B sales

- 5.5% EBIT margin

- 13.8x EV/EBIT multiple

- $36 fair value

Company Has Slowed Down and Fundamentals Have Weakened

I certainly won’t be adding to Whole Foods at this stage.

Put another way, it’s at the tipping point between selling and holding. It’s a wager that management will execute.

The latest numbers suggests that the turnaround is slowly taking place. Just not at the speed everyone wishes.

And at this stage, Whole Foods isn’t crumbling like Radio Shack or Aeropostale so I’ll continue to hold and monitor progress.

Let me quickly summarize all of this.

Reasons to Sell

- Falling margins

- Falling same store sales

- Expensive image is too hard to break

- Competition is here to stay

- Numbers show that fundamentals have weakened (I didn’t discuss all quality metrics like CROIC, DuPont, Cash Conversion Cycle)

Reasons to Hold

- Business acknowledges competition and is spending to improve situation

- Investments in 365 stores haven’t made it to the financial statements yet

- Latest quarter showing slight improvements

- Balance sheet still very healthy

- Plenty of FCF to fund expansion internally

- Clear goals and shareholder friendly

- Great philosophy behind company

Conclusion?

Hold

Disclosure

Long Whole Foods Market

Whole Foods Market – Additional Articles I Recommend

- What Whole Foods is Worth Today and What That Means for… What You Will Learn Whether it’s time to sell Whole…

- Whole Foods Market is a BMW. Stop Comparing it to a Kia. Whole Foods Market (WFM) is a “Buffett and Munger” cheap…

- Why Whole Foods is Cheap. Take Advantage of Mr… Whole Foods Market is cheap with long term growth. Mr…

- Quick Updates on 8 Stocks I Hold Ok I lied. I don’t hold all 8 stocks anymore.…

- The Next Hot Investment Trend – Organic and Natural… This is a continuation of my quest to go through…

This post was first published at old school value.

You can read the original blog post here Whole Foods Market Update – Did I Make a Mistake?.