Introduction

The Great Recession of 2008 – which ended in the spring of 2009 – brought on one of the greatest and longest bull markets in modern history. For true value-oriented dividend growth investors, the recession created a virtual cornucopia of excellent dividend growth stock investment opportunities that existed until the end of August 2013. However, by the end of 2013 to current time most dividend growth stocks have progressively become more and more richly valued. As a result, at least two very dangerous scenarios have become manifest.

First, this long-running bull market appears to have created overconfidence and perhaps complacency in the minds of many investors. On the other hand, this long-running bull market has also begun to elicit fears that a bear market has surely become past-due. Consequently, the recent weakness in stock prices is being perceived by many as the correction (or start thereof) that they’ve been fearfully waiting for. When investors become anxious they also tend to become more reactive and even impetuous with how they handle their portfolios. In simple terms, anxiety breeds volatility which further adds to nervousness. The recent increase in stock market volatility supports this contention.

This brings me to what I fear is the second potentially dangerous scenario I referenced above. The recent selloff in the stock market has led some investors into believing that the market in general has now gone on sale. I would agree that stocks are cheaper today than they were a few weeks ago, but the real question is: have stocks gotten cheap enough to be attractive? Unfortunately, I suggest that the fact remains that most high-quality dividend growth stocks are still far from being available at fair value.

However, as I often posit: “it is a market of stocks and not a stock market.” Therefore, although most blue-chip dividend growth stocks remain overvalued, they are not all overvalued. With this series of articles, I will present 50 dividend growth stocks in 5 groups of 10 that currently appear attractively valued. As an aside, there are several additional companies that are getting close to fair value but are not quite there yet.

To summarize, although stocks in general have recently contracted, valuations for the most part remain high relative to historical norms and/or intrinsic value calculations. Therefore, from my value investor’s perspective, many best of breed dividend growth stocks are still too rich. Moreover, once investor sentiment changes from optimistic to pessimistic (and it may already have begun) the market could potentially overreact to the downside just as it has overreacted to the upside during this long-running bull market. I believe that this represents a significant short-term risk. Therefore, if this were in fact to happen, both volatility and investor anxiety are sure to be heightened. A simple awareness of this potentiality can assist the more levelheaded and prudent investor in remaining calm during tumultuous market environments.

Why is Valuation So Important?

To many of my regular readers I am also known as “Mr. Valuation.” Frankly, I can never remember writing an article that didn’t focus extensively on the importance of only being willing to invest in a stock when it is soundly or attractively valued. So obviously, valuation is extremely important to me. Nevertheless, from reading many comments on my articles and from numerous discussions with investors, I have concluded that the importance of valuation is often misunderstood. Consequently, I offer this discussion to clarify the relative importance of focusing on valuation when managing stock portfolios. Hopefully, I can also help to clarify certain misconceptions about the impact that valuation has on both performance and risk.

First, I believe it’s important to understand that investing in an overvalued stock does not simultaneously mean that the investment will lose money. If the stock you are investing in is growing fast or at an above-average rate, you can overpay for it and still generate an acceptable long-term rate of return. The faster this company grows in the future, the more likely you are to make money even if you initially overpay to buy it. The incredible law of compounding comes into play here.

On the other hand, if you initially pay too much for even a fast-growing company, your returns will be less than they could have or ought to have been had you invested at a better valuation. Furthermore, by paying too much you are also taking on more risk than you need to or should. Everything I’ve written thus far is predicated on an important understanding of stock market efficiency. According to modern portfolio theory (a.k.a. MPT), the market is always efficiently pricing stocks because all publicly available information is known and included. Therefore, investors should not waste their time trying to find or exploit mis-priced securities. This hypothesis led Warren Buffett to once quip “I’d be a bum on the street with a tin cup if the markets were always efficient.”

However, I believe that MPT advocates are not totally wrong. Instead, I suggest that there is a level of efficiency that the market is constantly struggling with. Consequently, I offer that it is more accurate to state that the market is “always seeking efficiency” even though it can be very inefficiently pricing securities at any moment in time. Therefore, during times when the market is inefficiently pricing stocks, all the investor need do is wait for the inevitable movement back to rational pricing and values. This applies to stocks when they are overvalued as well as when they are undervalued.

Unfortunately, although I believe it is inevitable that stocks will move into alignment with true worth valuation, the exact timing of that occurrence is unpredictable. Sometimes a stock will move back into alignment very quickly, and at other times it can take years for realignment to occur. Nevertheless, I believe that common sense dictates that it will happen, only the “when” is uncertain.

This last principle is what often gets investors in trouble because waiting too long can try their patience to the extent that they no longer believe it will occur. When valuations are excessively high, this can lead to significant losses of both time and money. In contrast, when valuations are extremely low, it can cause investors to sell what they should be buying thereby locking in unnecessary losses.

Later in the FAST Graphs analyze out loud video I will provide clear examples of how these principles work in real-world situations. In this part 1, I will be presenting the initial 10 of 50 currently fairly- valued dividend growth stocks in order of dividend yield highest to lowest. In parts 2 through 5 I will present each of the additional fairly-valued research candidates by order of dividend yield highest to lowest.

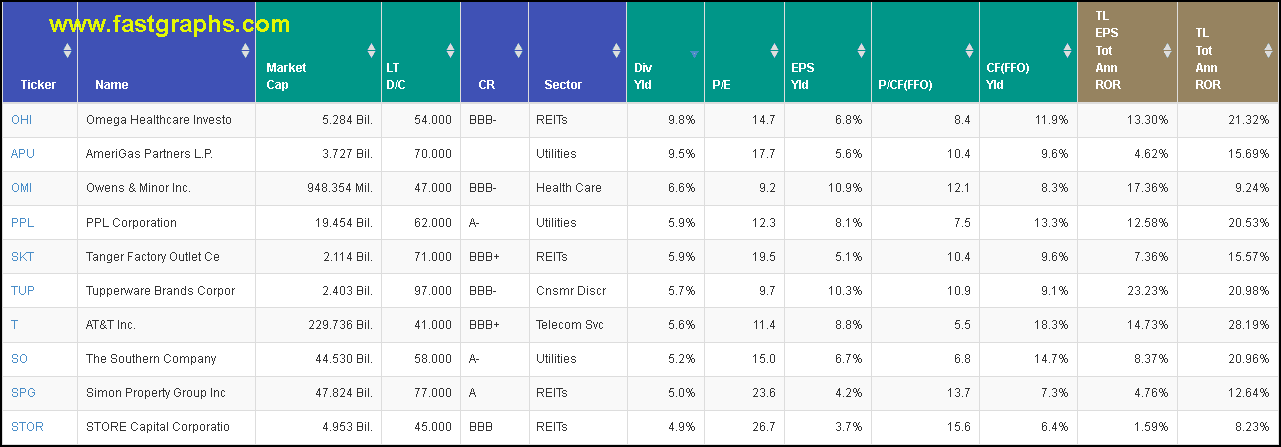

FAST Graphs Portfolio Review: Top 10 by Yield

The following portfolio review provides a summary of important metrics for the 10 highest yielding fairly-valued research candidates. The reader should note that the last 2 columns (light brown) provide annualized total return estimates based on the consensus 3 to 5 years trend line analyst estimates of either cash flows or earnings. The 1st light brown column provides annual return estimates based on earnings, and the 2nd light brown column provides annual return estimates based on cash flows or FFO (funds from operations) for MLPs and/or REITs.

It’s also important that the reader understands that the primary attribute that each of these 10 research candidates have in common is fair valuation. Moreover, each individual candidate will not necessarily be an appropriate investment for every dividend growth investor. I believe is vitally important that each investor builds portfolios according to their own unique goals, objectives and risk tolerances. For example, some of these candidates might be appropriate to boost the yield of an existing portfolio while others might be more appropriate for investors seeking a higher total long-term return. Therefore, I suggest that readers might pick and/or choose to examine only those that meet their own personal needs. I will be elaborating more on this important aspect in the FAST Graphs analyze out loud video to follow.

FAST Graphs Analyze out Loud Video

In the following video I will briefly illustrate why I believe each of these 10 research candidates are currently fairly-valued. Additionally, I will provide commentary on what type of portfolio or dividend growth investor they may be appropriate for.

NOTE: Because I will be covering 10 individual stocks in the video, it will be moderately longer than most. However, I think you will find that the pace of the video will keep your attention and is worth viewing.

Summary and Conclusions

As I illustrated in the video, the only metric that each of these higher-yielding research candidates have in common is that they are all currently fairly-valued relative to fundamentals. Outside of that, they each possess their own unique attributes and characteristics. Therefore, my suggestion is that the reader focuses their attention primarily on those research candidates that meet their own goals or needs.

Furthermore, I believe that all investors, regardless of their goals and objectives, should apply a disciplined valuation strategy. Being fiercely disciplined to only be willing to invest in any type of stock when valuation is sound is and should be a universally applied principle. Executing a prudent valuation discipline will reduce risk while simultaneously enhancing future returns. However, fair value is only one aspect of a successful investment strategy. When it comes to achieving a certain long-term total return, each company’s potential future growth will also be a driving factor.

That last statement will become clearer as I present each of the next four articles in this series. As a rule (and there are always exceptions to every rule), investors generally face a trade-off between growth and income. This same principle applies to risk. In theory, investors must be willing to take on greater risk in order to achieve higher rates of return. These principles speak directly to why investors need to invest according to their own goals, objectives and risk tolerances.

Disclosure: Long OHI, SKT, TUP, T, SO, STOR at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Article by F.A.S.T. Graphs