5 Rules to Buy Quality Dividend Stocks over Deep Value Butts

(This is a guest post and may not reflect the views of Old School Value)

Value investing is simply buying an asset (generally a stock) for less than its fair value.

Traditional value investing focuses on buying mediocre businesses for less than their book value or net current asset value.

This style of investing makes intuitive sense for bargain hunters and those who generally seek good deals.

Not only does it make intuitive sense, it has greatly outperformed the market.

Buying an equally weighted portfolio of the lowest 10% of stocks by P/B has a CAGR of over 20% from the period from 1926 to 2013.

Compare this to the highest priced decile of stocks, which has a CAGR of about 6.3% within the same time period.

Value investing works.

![]()

Glamour vs Value Performance | Enlarge (source)

Glamour vs Value Performance | Enlarge (source)The Pitfalls of Value Investing

Buying a well diversified portfolio of small and micro cap stocks trading at a large discount to book value and/or net current asset value is generally the best way to generate high returns investing in the stock market.

Unfortunately, this strategy suffers from high volatility.

Additionally, there is something psychologically frightening (at least to most people) about putting your hard earned money into businesses that are poorly managed or unprofitable.

The data shows deep value investing works, but it can be fraught with anxiety.

I believe applying value investing in a different manner will still produce market-beating returns (though less than traditional value investing) with significant reductions in both qualitative risk and total drawdowns.

The difference; this investing strategy is about purchasing high quality businesses that tend to have lower volatility than the typical stock and have a strong competitive advantage as well.

The idea is to trade some of the excess returns of value investing for a significant boost in ‘sleeping easy at night’ and not worrying about your investments.

Quality and Value

Value doesn’t have to mean buying mediocre businesses for less than they are worth.

Value can also be found in purchasing exceptional businesses when they are priced as regular businesses.

In doing so, you are still exploiting the same gap between intrinsic value and market prices that traditional value investing benefits from.

The difference is you can purchase businesses that rarely need to be sold.

“It is far better to buy a wonderful company at a fair price than a fair company at a wonderful price. I would rather be certain of a good result than hopeful of a great one.”

– Warren Buffett

A business with a strong, durable competitive advantage and a long history of rewarding shareholders through dividends and share repurchases will compound your initial investment as it grows over time.

These businesses are not common, but they are well known.

Examples of businesses with durable competitive advantages and long histories of dividend growth include;

- Coca-Cola

- Wal-Mart

- Procter & Gamble

- and ExxonMobil

Enter the Dividend Aristocrats

Coca-Cola, Wal-Mart, Procter & Gamble, and ExxonMobil are all Dividend Aristocrats.

Dividend Aristocrats are businesses that have increased their dividend payments for 25+ consecutive years.

Interestingly, Coca-Cola, Wal-Mart, Procter & Gamble, and ExxonMobil are all stocks Warren Buffett holds in his Top 7 holdings.

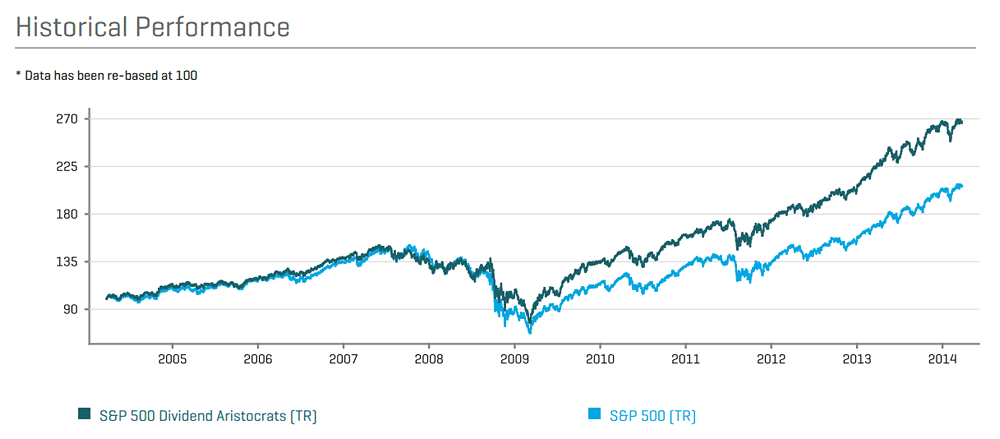

Dividend Aristocrats have historically outperformed the stock market by about 2 percentage points a year over the last decade.

Performance with Dividends | Enlarge (source)

Performance with Dividends | Enlarge (source)I believe Dividend Aristocrats have outperformed because they are generally high quality businesses.

A business must have a strong competitive advantage in order to grow its dividend year after year, decade after decade.

Quality is difficult to quantify, but most people would agree that they “know it when they see it”.

A look at the businesses that make up the Dividend Aristocrat index should alert your brain’s quality detector to start buzzing.

How To Find Quality Businesses

I am a fan of systematic investing processes because they remove bias.

You can use systems to either identify candidates for further research (a la Old School Value’s excellent screens), or to actually make your investment selections.

The 5 Buy Rules from the 8 Rules of Dividend Investing are used to identify high quality businesses trading at fair or better prices.

To give you an idea of how the process works, ExxonMobil will be examined below using the 5 Buy Rules from the 8 Rules of Dividend Investing.

The reasoning behind why each rule is used will be included as well.

Examining ExxonMobil (XOM) using 5 Rules

Rule 1: 25+ Years of Dividend Payments without a Reduction

ExxonMobil has paid increasing dividends for 32 consecutive years.

The business has a storied history and is the successor to Rockefeller’s Standard Oil.

ExxonMobil passes the screen of having to pay dividends for 25 or more years without a reduction.

132 businesses total pass this test.

Why it matters: The Dividend Aristocrats (stocks with 25-plus years of rising dividends) have outperformed the S&P 500 over the last 10 years by 2.41 percentage points per year.

Source: S&P 500 Dividend Aristocrats Factsheet

Rule 2: Rank by Dividend Yield

ExxonMobil has a dividend yield of 2.8%, which is the 56th highest out of 132 businesses with 25+ years of dividend payments without a reduction.

Why it Matters: Stocks with higher dividend yields have historically outperformed stocks with lower dividend yields.

The highest-yielding quintile of stocks outperformed the lowest-yielding quintile by 1.76 percentage points per year from 1928 to 2013.

Source: Dividends: A Review of Historical Returns

Rule 3: Rank by Payout Ratio

ExxonMobil has a payout ratio of about 35%.

The company has the 36th lowest payout ratio out of 132 businesses with 25+ years of dividend payments without a reduction.

ExxonMobil’s low payout ratio gives the company ample room to increase dividends faster than overall company growth going forward.

Why it Matters: High-yield, low-payout ratio stocks outperformed high-yield, high-payout ratio stocks by 8.2 percentage points per year from 1990 to 2006.

Source: High Yield, Low Payout by Barefoot, Patel, & Yao, page 3

Rule 4: Rank by 10 Year Historical Growth Rate

To find a company’s historical growth rate, the lower of 10 year revenue per share or 10 year dividend per share growth is used. Revenue per share is used instead of earnings per share because earnings tend to fluctuate more year to year than revenue per share. ExxonMobil has managed to grow revenue per share at about 6.3% per year over the last decade. The company has the 41st highest growth rate out of 132 businesses with 25+ years of dividend payments without a reduction.

Why it Matters: Growing dividend stocks have outperformed stocks with unchanging dividends by 2.4 percentage points per year from 1972 to 2013.

Source: Rising Dividends Fund, Oppenheimer, page 4

Rule 5: Rank by 10 Year Standard Deviation

ExxonMobil’s 10 year standard deviation is about 25%, which is the 48th lowest out of 132 businesses with 25+ years of dividend payments without a reduction.

The company has a below average standard deviation despite its earnings having a high level of variability due to exposure to oil prices.

Why it Matters: The S&P Low Volatility index outperformed the S&P 500 by 2 percentage points per year for the 20-year period ending September 30th, 2011.

Source: Low & Slow Could Win the Race

Tying It All Together

ExxonMobil is the 8th highest ranked stock based on The 5 Buy Rules from the 8 Rules of Dividend Investing.

The company is fairly cheap with a P/E ratio under 13.

Notice that ExxonMobil does not stand out in any one category, but performs well over all of them.

It does not have an extremely high yield, or exceptionally low volatility, nor is its growth rate phenomenal.

Overall, ExxonMobil is a solid business that has rewarded shareholders with decades of increasing dividends. The company is not a traditional value stock, but does offer investors solid returns with relatively low risk.

Investing in businesses that seem fairly priced (or slightly undervalued), but offer investors a high likelihood of success and an above average long-term compound average growth rate will likely offer investors strong risk adjusted returns.

ExxonMobil is an example of a company that fits this profile in today’s largely overvalued market.

Investing in high quality dividend growth stocks will not appeal to everyone. I believe it is an excellent choice for those with somewhat lower risk tolerances who may find it difficult to fully commit to deep value investing, but agree with the philosophy of value investing.

About the Author

Ben Reynolds is the author of Sure Dividend which focuses on high quality dividend growth stocks with a tilt toward quantitative investing.

This post was first published at old school value.