“Davidson” submits:

Since the election outcome, markets have been swirling with change. The shifts in certain areas have been massive. Many are scrambling to adjust portfolios to what thy believe is a new era and an acceleration in economic activity. In my opinion this is the beginning of the swing towards market optimism from an overly long period of pessimism. While market psychology can change overnight, economies change only slowly. The economic impact of any new policies by the new administration will only be apparent many months after Pres-elect Trump is sworn in. Nonetheless, market psychology has resulted in significant capital shifts.

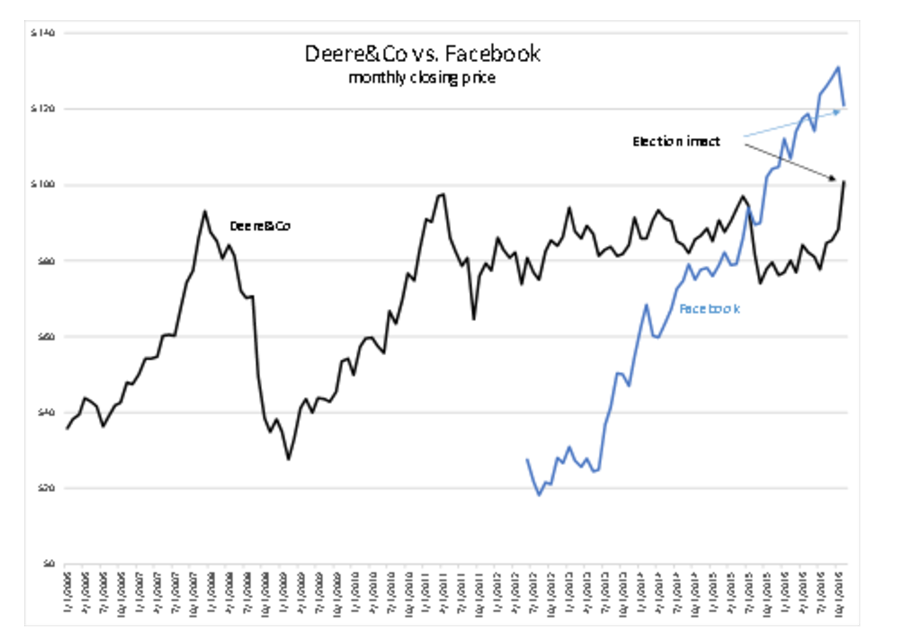

There have been highly visible shifts in pricing in several areas as a new investor psychology has emerged. It is still based on investors seeking the best returns for capital. First we have seen a significant shift out of the FANG (Facebook, Amazon, Netflix and Google) type stocks which dominated market indices for several years. The shift has favored industrial, infrastructure and commodity related issues. The relative shifts in Deere&Co.(DE) vs. Facebook(FB) serve as a good example of this.

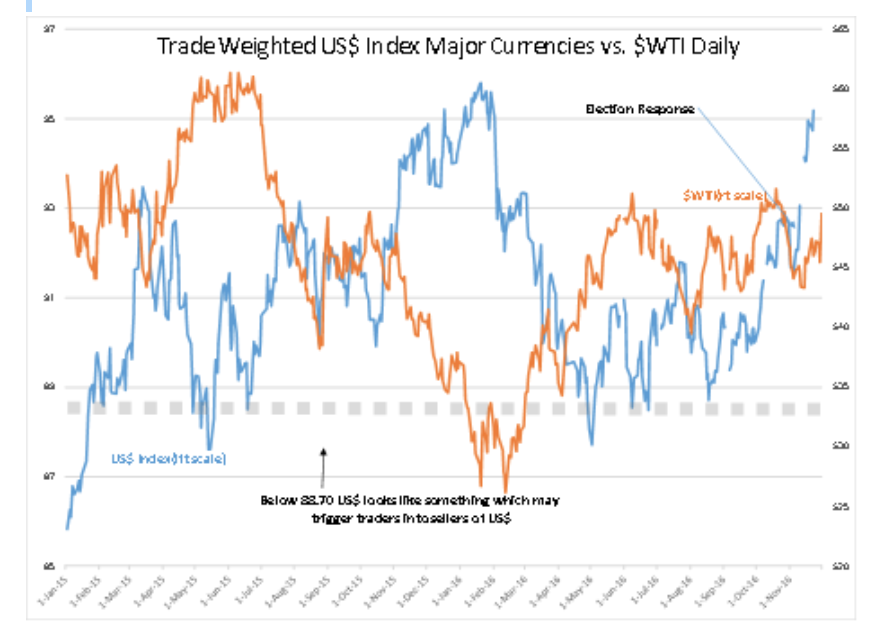

The second shift is seen in the US$ which has broken its algorithmic inverse relationship with oil prices. The rising US$ is one of the reasons for a weak industrial economy as the strength in the US$ is directly correlated to weak US exports and weak commodity prices. Market psychology has caused both to rise as investors anticipate US investments to produce the better returns. Capital has surged into the US. Oil had already come off its lows of Feb 2016. OPEC finally decided to agree to control production. This has resulted in more than a $4BBL rise today. I continue to anticipate that changes in US foreign policy will result eventually in capital returning to developing markets as the US revives its global support of Democratic institutions.

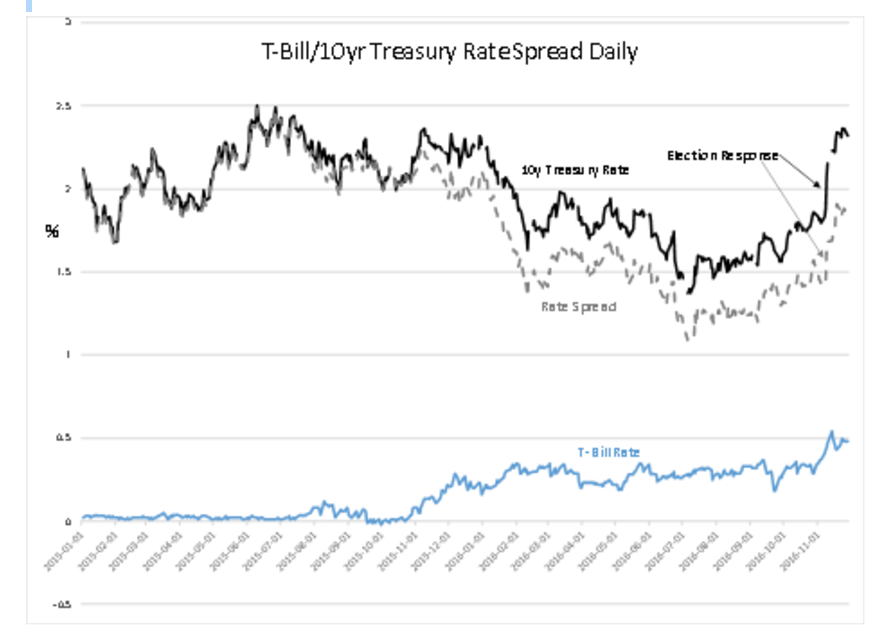

The third shift comes in T-Bill and 10yr Treasury rates. After being driven to lower rates by the influx of foreign capital, both have risen sharply since the election. The 10yr Treasury has risen more rapidly as investors shifted capital. Importantly, the rate spread of the T-Bill/10yr Treasury has widened sharply. Lending institution’s profits are highly dependent on this spread. The wider the spread the higher the profit opportunity. Wider spreads let lenders issue credit to those with weaker credit ratings as there is more profit to provide for credit reserves to protect against defaults than when spreads were narrower. Economic activity expands when the T-Bill/19yr Treasury rate spread widens. NOTE: Those who continue to hold the 10yr Treasury have suffered ~15% capital losses. As rates rise, losses rise. This typically forces investors to sell at an accelerated pace. I have not recommended long term fixed income for some time but for selected situations.

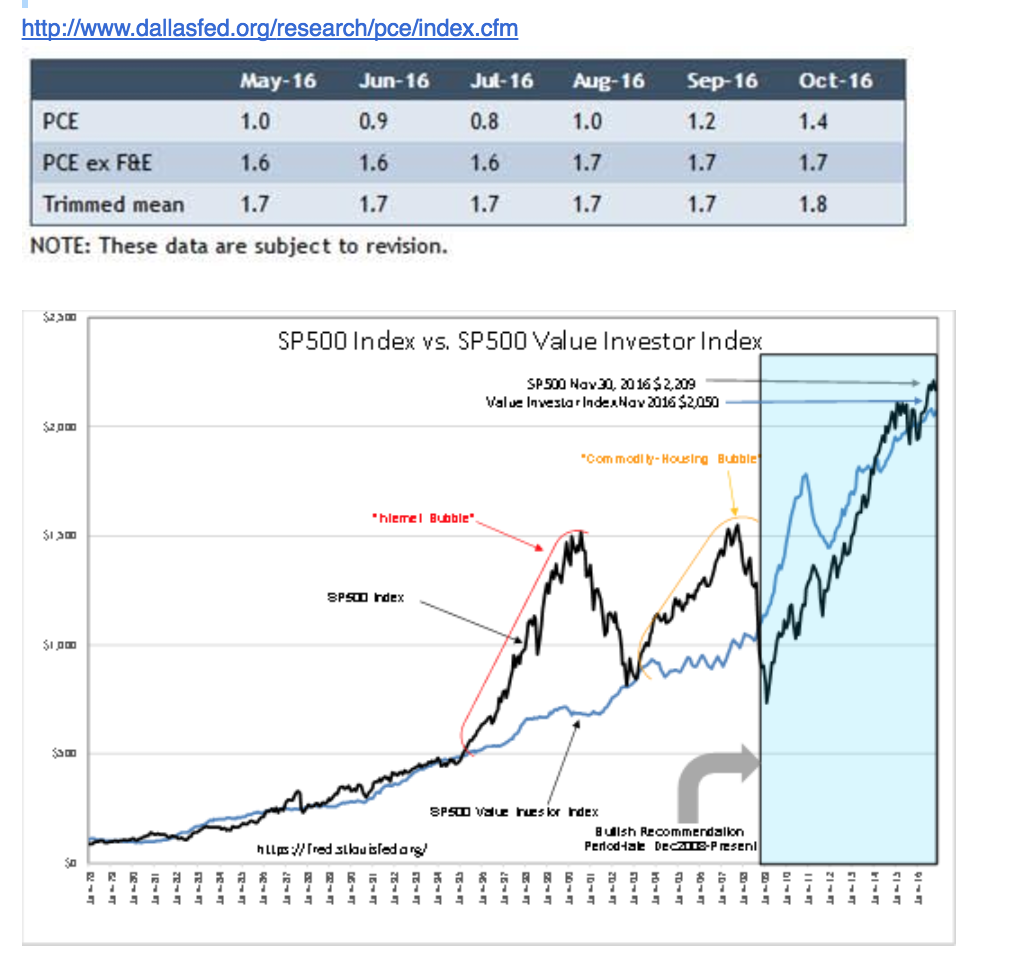

Market psychology aside, fundamentals remain positive. With the 12mo Trimmed Mean PCE(Dallas Fed inflation measure) reported at 1.8%, the long term SP500 Value Investor Index shifts slightly lower to $2050 from last month’s $2,104. Comparison to the SP500 at $2,209 reflects a continued low level of general investor speculation even with the clear signs of optimism since the election. What has occurred is a shift from speculative FANG stocks towards those companies like Deere&Co., Caterpillar and many neglected infrastructure issues which have risen 10%-20%. Net/net, these shifts leave the SP500 only slightly higher with some issues falling as others have risen. The SP500 remains at historically attractive levels.

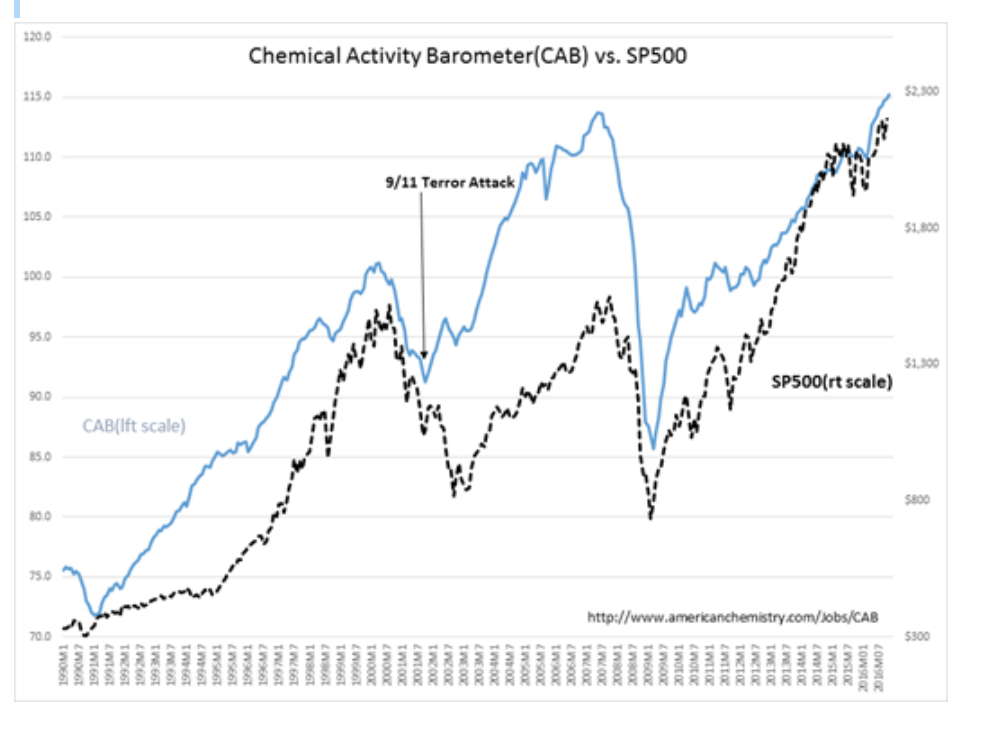

One might have expected the dramatic shift in investor psychology to be reflected in economic trends. Psychology does not work that way. Market psychology follows economics. It does not presage economics as many believe. That the economy has been in and continues a long-term expansion can be seen in the Chemical Activity Barometer(CAB).

CAB reached another historical high last week. After pausing 12mos (Mar 2015-Apr 2016) the CAB has pushed thru a series of successive new highs since. Employment levels, Real Retail Sales and Real Personal Income have also trended thru a series of successive new highs.

Trump’s win has every Momentum Investor falling over themselves as they shift from abject pessimism to optimism. Commodity prices and 10yr Treasury rates have risen sharply with this change in expectation. Value Investors have favored infrastructure and related issues. The gains in these issues the past few weeks are likely to be met with even higher gains the next few years as economic expansion continues.

I recommend investors read Brian Wesbury’s commentary: Big Boom for Stocks