“Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly and one by one.” – Charles MacKay, Extraordinary Popular Delusions and the Madness of Crowds

Every bull market has its stars – companies and industries that are supposed to be growth champions and investors who generate supernormal returns during that cycle. Frequently, investors lineup to pour money into these hot stocks and industries and to invest with these newfound investment superstars driven by their hopes of quick riches. Wall Street capitalizes on this behavioral tendency of investors to chase hottest stocks, sectors, and investors. Indeed, this is the primary rationale why financial intermediaries have concepts like flavor of the month. It is also the reason why these intermediaries push the strongest performing funds of the last one to three years. Such products are easy to sell to investors salivating over prospects of large investment returns as they extrapolate the recent strong performance long into the future.

Q2 hedge fund letters, conference, scoops etc

This is also the reason why nobody pays attention to that universally applicable disclaimer, “past performance is no guarantee of future results.” To our kind of thinking, focusing solely on the recent investment performance is a surefire way to capital destruction. As we see it, there are two primary problems associated with fund performances, at least, the way they are presented when investment products are being sold.

Problem #1. Insufficient Evidence

Let’s consider the game of cricket to help us understand the issues with investment performance evaluation. As the cricket world cup recently concluded, this is our way of plugging into our industry’s flavor of the month tendencies. In a typical game of one day international (ODI), there are three hundred deliveries that the batting attack of a team faces[1]. The star batsman of the current generation, Virat Kohli, on average plays fifty-three deliveries in each innings he has played[2]. Consider that this is not very dissimilar to the number of potential investment actions a typical “investment” manager evaluates in a typical year. What this means is that the amount of data that Virat Kohli generates in a day’s outing, is similar to one-year worth of data for a typical “investment” manager.

And therein lies the problem in assessing the quality of an investment manager based on one to three year performances. As of this writing, Virat Kohli’s average runs scored per inning in ODIs is 49.5. It means that on an average, Mr. Kohli has scored 49.5 runs in each inning he has played[3].

If you were trying to assess the batting abilities of a cricketer, will you rely largely on their performance in the last three innings? Yet, the idea of investing primarily based on last three years performance is not very dissimilar to making a decision that a batsman is as good as Mr. Kohli just because in the last three innings, this batsman has averaged 49.5 runs per inning!

Problem #2. Inappropriate Evidence

Note that it is not that the performance numbers of the past three or five years do not contain valuable information. However, frequently, because of the design of the process by which investment opportunities are presented to investors, it serves as inappropriate evidence.

Going back to our cricketing example, in order to make an effective assessment, we will need to dig deeper. A proper assessment process will involve understanding the player’s practice and training processes, performance under pressure, actions when scoring conditions are relatively easy – do they start throwing their bat at everything or do they stick to their game plan, and performance under different batting conditions and pitches, etc.

Similarly, when evaluating the quality of an investment manager, you will want to see a well-structured decision-making process that leads to repeatable and replicable investment actions. You will want to understand their process during unfavorable market conditions. The minimum requirement will be to look at their drawdowns[4]. Further, you will want to understand the quality of their investment actions during good times – did they stick to their investment process or did they take undue risks in order to strike that homerun.

The minimum requirement to make an effective assessment, of a cricketer or an investment manager, is to go through their actions during times of good as well as poor performances. The rationale for the suggested evaluation process is driven by the fact that both these activities have elements of luck associated with them. Investing, likely, has a higher component of luck involved when compared to the game of cricket. If on the other hand, either of these activities were purely a matter of skill, the performance numbers will suffice.

Bill Gross, in one of his investment outlooks, tackled this topic and suggested that in the business of investing, it is possible that even 20+ years’ worth of performance data may be insufficient[5]. When looking at investment strategies that have a narrow focus, it is extremely important to understand the applicable epoch and whether or not that epoch is about to turn. Odds are that the supernormal investment abilities of the investor are largely a result of a cyclical upturn in their focused investment area.

So, the next time you hear about the skill of an investment manager, ask yourself whether the evidence is sufficient and whether it is appropriate.

NBFCs[6] and Mid & Small Cap Stocks

“When a bubble collapses, it usually gives back not just some, but all, of its gains.” – Maggie Mahar, Bull!: A History of the Boom and Bust, 1982 - 2004

Our discussion on investment performance evaluation and the chase for hot stocks and investors leads us towards the current bout of pain that investors have inflicted on themselves. Between late 2016 and early 2018, the hot “new” interest of speculation for investors in Indian equities included the mid and small capitalization stocks and stocks of NBFCs.

As we look at what has transpired since, it reminds us of a scene from a Bollywood movie, Trimurti. Anil Kapoor, one of the heroes of the movie, is having a telephonic conversation with Mohan Agashe, the chief villain of the story. On being instigated by Mohan Agashe, Anil Kapoor shoots at the glass roof. The result, as to be expected, is that the roof comes down crashing. We think that when it comes to investments, the process of shooting for stars, frequently results in similar outcomes. Stars, they usually stay out of reach of investors. However, shooting for extraordinarily high returns frequently results in destruction of existing capital.

We highly recommend Maggie Mahar’s book referenced above to anyone with even a passing interest in financial history. As Ms. Mahar stated, the collapse of a bubble is usually associated with a total wipeout of all gains achieved during that bubble. This same process is currently underway in both the Indian mid and small cap space in general and in NBFC stocks in particular.

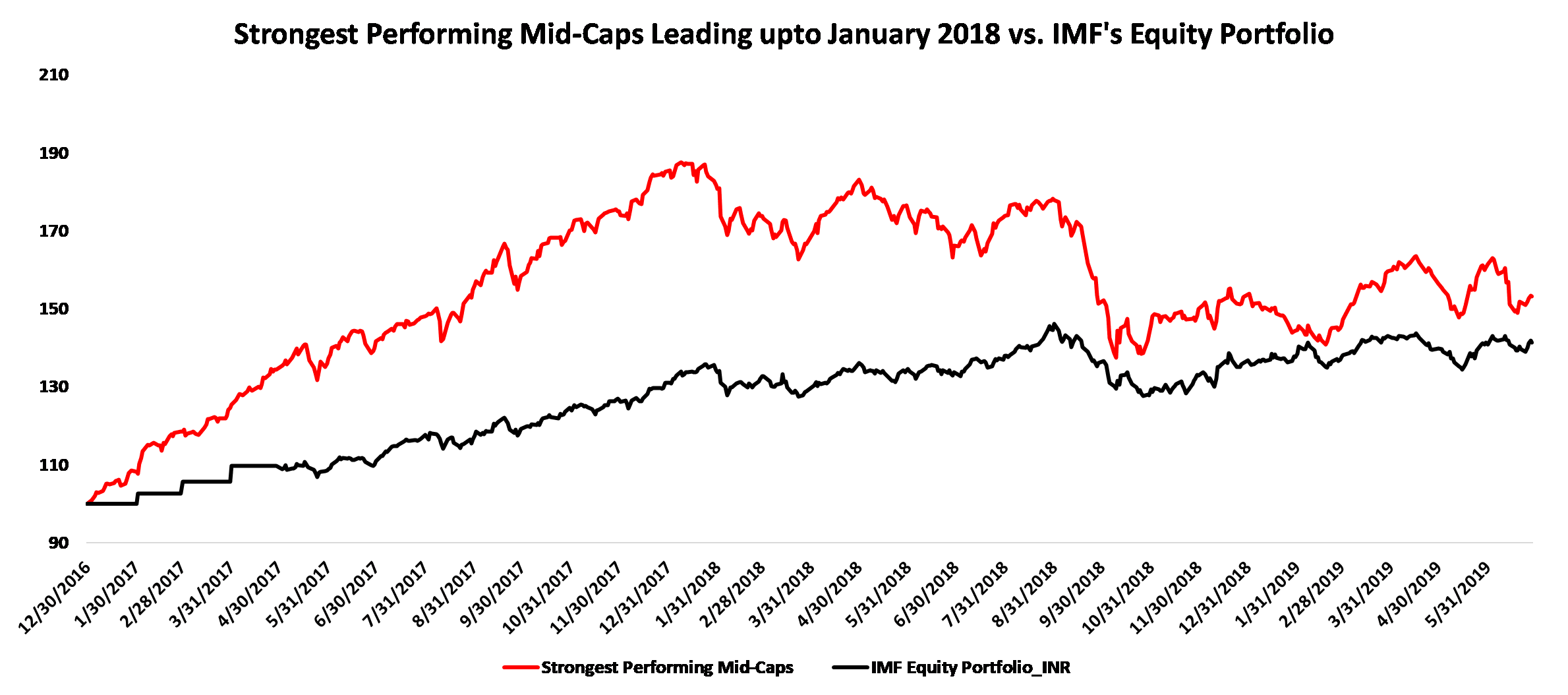

Below we present two charts that document this process. Figure 1 shows the performance of a segment of the Indian mid-cap space, the strongest performing stocks leading up to the peak in January 2018[7]. For the sake of comparison, we have also shown the performance of the India Moats Fund’s (the “Fund” or “IMF”) equity portfolio. Let’s assume that you had the perfect foresight to be able to choose those one-third of stocks from the BSE mid-cap index that ended up generating the strongest performance within the index leading up to January 2018. As Figure 1 shows, if you held on to these same stocks for the next sixteen months as well, nearly all the outperformance you generated when compared to the Fund’s high quality strategy, would have been erased!

Figure 1. Performance of Strongest Mid-Cap Stocks vs IMF’s Equity Portfolio

Source: Sapphire’s calculations, Data from Factset

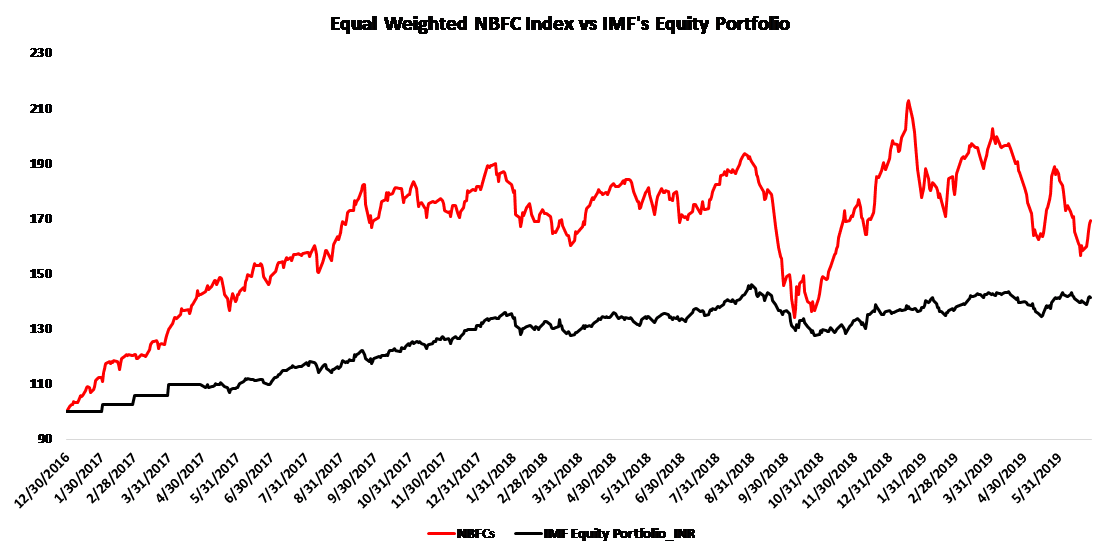

Figure 2 shows the performance of an equal-weighted basket of NBFC stocks as compared to that of the Fund’s equity portfolio. As is seen, the process of erasing excess performance is well underway here as well.

Figure 2. Equal-Weighted NBFC Index vs IMF’s Equity Portfolio

Source: Sapphire’s calculations, Data from Factset

There is one benefit that investors in these two baskets can claim over that of investing in a basket like ours. These investors have had a hell of a ride! As Ed Seykota noted in Market Wizards, “Win or lose, everybody gets what they want out of the market.”

As you look at the equity curves of the two baskets in relation to that of the Fund’s equity holdings, it should be clear that those two baskets were associated with significantly greater risk. If the ride is what you want, riskier securities are clearly the way.

We end this discourse with a reminder about the nature of riskier assets; one that is frequently forgotten by investors or conveniently skipped by the financial intermediaries when driving investors towards them. The higher risk of a basket of securities does not guarantee higher returns. It only offers a chance of higher returns.

When evaluating investment managers, dig in to the source of those returns over the period such returns are being scrutinized. If they emanated from high risk sources, possibility is that in the period under scrutiny, the chance of high returns materialized. Now, the important question beckons: what is the probability of such chances materializing in the future.

Article By Baijnath Ramraika and Prashant K. Trivedi

Baijnath Ramraika, CFA, is a cofounder and the CEO & CIO of Multi-Act Equiglobe (MAEG) Limited and is the Executive Director at Sapphire Capital. As a portfolio manager, he manages the Global Moats Fund and the India Moats Fund. Contact him at [email protected]. Baijnath’s thoughts and ideas can be read at his blog at www.symantaka.com

Prashant K. Trivedi, CFA, is a cofounder of MAEG and the founder and chairman of Multi-Act Trade and Investments Pvt. Ltd.

MAEG is an investment manager and manages the Global Moats Fund, an investment fund that invests in a global portfolio of high-quality businesses with sustainable competitive advantages. Sapphire manages the India Moats Fund, an investment fund that invests in a portfolio of high-quality Indian businesses with sustainable competitive advantages.

Multi-Act is a financial services provider operating an investment advisory business and an independent equity research services business based in Mumbai, India.

Footnotes

[1] In practice, it is usually more than three hundred deliveries because of extras like no balls and wides which require the bowler to re-bowl the delivery. On the other hand, if the team gets all out before completing full fifty overs, it will likely end up facing less than three hundred deliveries. [2] As of the date of this article, Virat Kohli has played 228 innings and has faced 12,135 deliveries for an average of 53.2 delivery per inning. Source: http://www.espncricinfo.com/india/content/player/253802.html [3] Note that when calculating player’s averages, the total runs scored are divided by the number of times the batsman got out. Because of this quirk, the commonly reported averages of a batsman do not represent average runs per inning. Indeed, while the commonly reported average for Virat is 59.4, the average runs scored per inning is 49.5 (11,286 runs scored in 228 innings). [4] A drawdown is defined as the peak to trough percentage decline for an investment account or fund. [5] https://www.pimco.com/en-us/insights/economic-and-market-commentary/investment-outlook/a-man-in-the-mirror/ [6] NBFCs refers to non-banking financial companies. [7] This index was constructed by taking a third of the strongest performing BSE mid-cap index components leading up to the peak in January 2018.