Speed Read:

- While the Federal Reserve maintains its commitment to keep frontend rates near zero, US backend rates are trending higher

Q1 2021 hedge fund letters, conferences and more

- Signals of higher-than-expected inflation, a strong post-pandemic recovery, and the recent economic stimulus suggest this trend will continue

- The performance of tech stocks is typically inversely correlated to backend rates. Recent market fatigue for high valuations in this sector suggest a shift in investor behavior

- Financial services firms should be aware of the portfolio, collateral, and liquidity implications of these macro trends

On Wednesday, March 17, the Federal Reserve kept rates anchored near zero and maintained the current pace of asset purchase. The announcement was in line with market expectations and soothed the nervous rates traders who have been experiencing a steady rise in rates since fall of 2020.

Although the Fed did not change their dovish policy, the markets are showing signs that an upward trend in rates might be here to stay for a while. Let’s take a look at what are driving long-term rates higher.

-

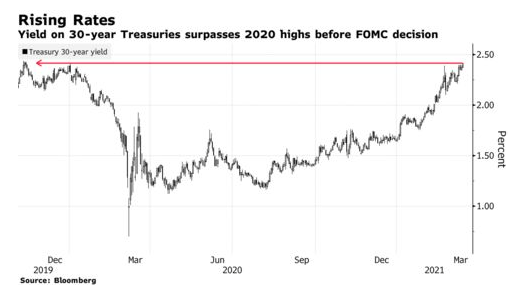

Nowhere To Go But Up

During the first surge of the 2020 pandemic, 10-year rates plummeted to all-time lows of .318. Fear, panic, and the unknown, plus a Fed that flooded the markets with credit drove rates to unprecedented levels. The Federal Reserve’s easy stance continues to put pressure on the front end and will continue to hold short-term rates near zero for the foreseeable future; yet, a 10-year return of only .318 is unsustainable due to better returns elsewhere in the markets, a rebound quickly occurred and now a sustainable trend higher seems more likely.

-

Growth Out Of A Pandemic

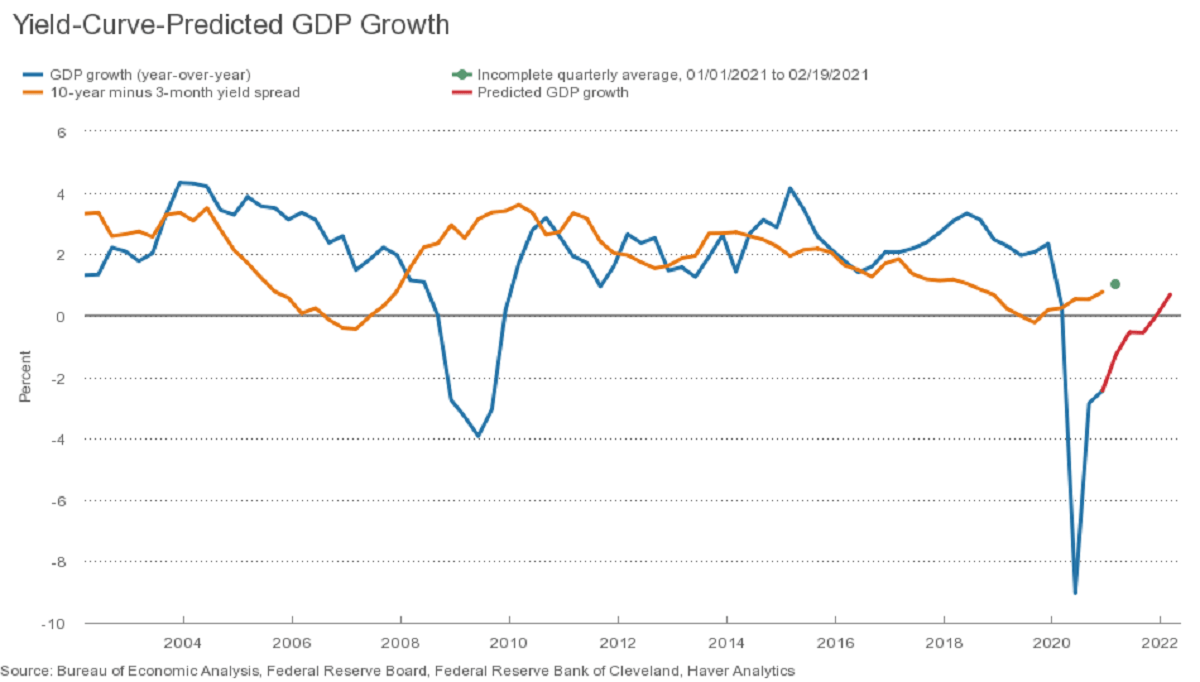

The Fed might not be signaling a change in policy any time soon, but that does not mean the U.S. consumer is not doing better. Treasury secretary Janet Yellen believes the economy will strengthen greatly post-pandemic. Her comments on the COVID relief bill says as much. “This is a bill that will really provide Americans the relief they need to get to the other side of the pandemic, and we expect the resources here to really fuel a very strong economic recovery,” Yellen said in an interview on MSNBC.

The chart below illustrates the inverted relationship of backend rates and GDP. As GDP increases, the yield curve steepens. Fueled with stimulus checks, the American consumer is looking good and this fuel a tailwind to back-end rates for the next year or so.

-

Inflation Perks Up

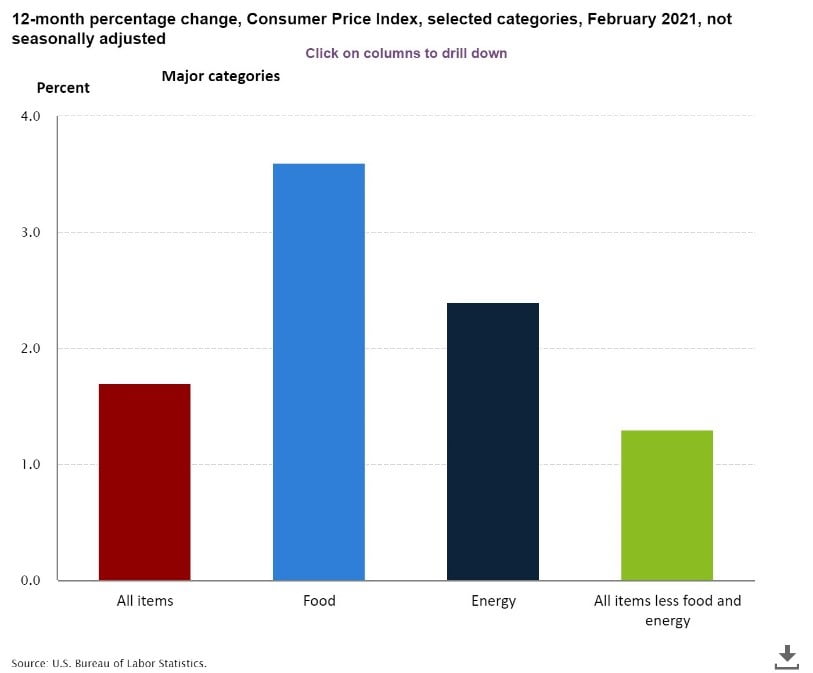

By no means has inflation moved to uncomfortable levels in the U.S., however, has the inflation train started to move out of the station? Possibly. It’s worth watching for sure. The Consumer Price Index for All Urban Consumers increased 0.4% in February. Over the last 12 months, the all items index increased 1.7 percent before seasonal adjustments. Food prices are a big contributor to the jump, as well as oil that has returned to pre-COVID levels.

The Fed now projects 2.4% inflation this year, overshooting their 2% target. Inflation erodes the value of long-term bonds, therefore as inflation elevates, even at a steady rate, demand for the back end will be reduced.

-

Auction Demand Worries

One of the hiccups in rates this year, so far, has been the result of poor demand for treasuries at auction. Both a seven-year and a 20-year auction went poorly resulting in rate spikes. March’s 10=year auction went smoothly. It is a high-demand product in general, however, it is worth watching supply effects on these markets.

A lack of demand for long-term treasuries would be a concerning signal for rates. Foreign investors hold the cards here; however, the Fed is still a huge player in treasury purchases and a twist-type play is an option if rates rise too fast.

-

Tech Stock Froth

Stocks, in general, remain close to all-time highs which makes sense with the forecasted growth picture. Recently, tech stocks are starting to show some fatigue at their high valuation and are not continuing their explosive price movements in a post-pandemic dip. As a rule of thumb, tech stocks emulate bond returns due to both being considered speculative and long term. In a CNBC article, Peter Boockvar, chief investment officer at Bleakley Global Advisors, illustrates this well: “When rates are very low, valuations don’t matter to people. If rates are low, there’s no penalty. If rates start to go up, people become much more sensitive to valuations, and that’s what we’ve seen here.” It would be logical for this correlated trend to continue. If tech stock gains remain lackluster, then bond rated most likely will remain elevated and vice-versa.

Financial Institution Considerations

By no means are backend rates signaling a crisis and, in general, rates are extremely low. But it is worth noting that a significant change in trend has happened, and adjustments to thoughts of long-term free credit should change. These changes to market conditions can affect the credit portfolio management (CPM) of financial institutions. Market conditions can affect risk, capital, and liquidity of credit portfolios. Considerations to monitoring risk and liquidity, especially intraday monitoring, should be made as fixed income trends change.

Article By Stephanie Colling

About The Author

Stephanie Colling is a senior consultant at Capco, a global management and technology consultancy dedicated to the financial services industry.

Sources:

- https://www.reuters.com/article/us-usa-economy-yellen/yellen-says-biden-covid-bill-to-fuel-very-strong-u-s-recovery-idUSKBN2B01MJ

- https://www.bloomberg.com/news/articles/2021-03-16/asian-stocks-to-open-steady-oil-declines-markets-wrap?srnd=premium

- https://www.cnbc.com/2021/03/12/the-fed-could-be-a-catalyst-for-bonds-and-that-could-drive-growth-stocks-in-week-ahead.html?recirc=taboolainternal

- https://www.cnbc.com/2021/03/10/us-bonds-treasury-yields-climb-ahead-of-february-inflation-data.html

- https://www.cnbc.com/2021/03/12/the-fed-could-be-a-catalyst-for-bonds-and-that-could-drive-growth-stocks-in-week-ahead.html?recirc=taboolainternal