Farnam Street letter to investors for the month of July 2019.

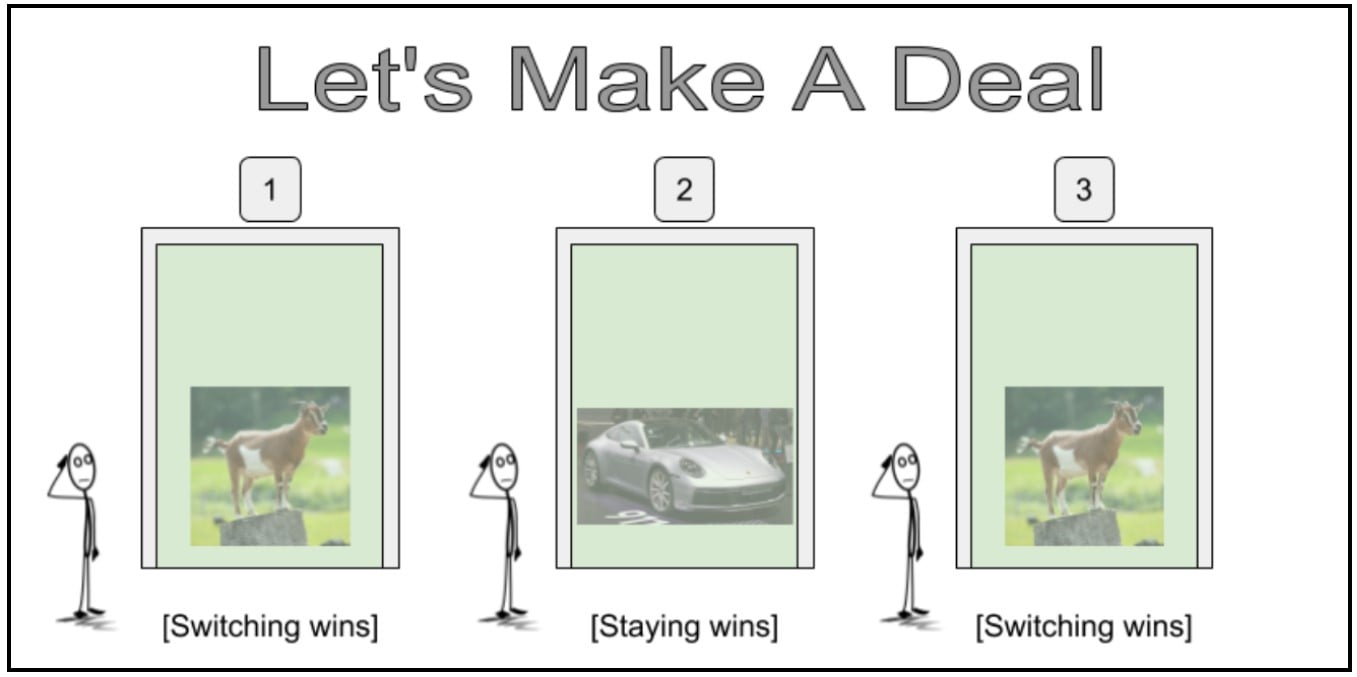

Let’s Make a Deal

The TV game show Let’s Make a Deal first aired in 1963, with the beloved Monty Hall serving as host for nearly 30 years. The final segment of every show was called the “Big Deal” and involved a contestant choosing one of three doors. Two doors contained basically nothing, called “zonks” on the show. Behind the remaining door would be a new car.

Q2 hedge fund letters, conference, scoops etc

Marilyn vos Savant was a columnist for Parade magazine and was recognized by Guinness as the woman with the highest IQ for five consecutive years (measured at 228). She caused a stir in 1990 when she proposed the following brain teaser called the “Monty Hall problem” (in her words):

Suppose you are on a game show, and you’re given the choice of three doors. Behind one door is a car, behind the others, goats. You pick a door, say number 1, and the host, who knows what’s behind the doors, opens another door, say number 3, which has a goat. He says to you, “Do you want to pick door number 2?” Is it to your advantage to switch your choice of doors?

Would you stay or switch?

Most people choose to stay. The regret of mistakenly switching away from the car would be hard to bear. However, that’s the wrong choice according to Savant. Her advice to always switch lead to more than ten thousand letters, many of them from PhDs, some of them offensive:

“You blew it! If one door is shown to be a loser, that information changes the probabilities of either remaining choice, neither of which has any reason to be more likely, to one-half. There is enough mathematical illiteracy in this country, and we don’t need the world’s highest IQ propagating more. Shame!”

“I am sure you will receive many letters on this topic from high school and college students. Perhaps you should keep a few addresses for help with future columns.”

“You made a mistake, but look at the positive side. If all those Ph.D.’s were wrong, the country would be in some very serious trouble.”

“You cannot apply feminine logic to odds. The new situation is one of two equal chances. You are the goat!”

On the surface, the letter-writers’ arguments appear logical. One remaining door has a car, one has a goat, therefore it’s fifty-fifty, right?

Not quite. The odds are 2-out-of-3 that you should switch. Huh?

The trick to solving the Monty Hall problem is to think of yourself as not alone. (This is also called using “natural frequencies” in the decision-making literature.) Imagine there are three contestants standing in front of the three doors. The contestant in front of door 1 wins by switching to door 2. The contestant who initially chose door 3 will also win switching to door 2. Only the contestant who chose door 2 and switches loses. The math is that in 2-of-3 cases, it pays to switch.

“Logic” isn’t always so logical, fancy degrees and male chauvinism notwithstanding.

We classify this scenario using the term “risk” because we know all of the potential outcomes and implied probabilities. We don’t necessarily know if we’ll win or lose due to chance, but we can calculate the odds of getting a car or getting zonked (if we’re as smart as vos Savant).

Risk Versus Uncertainty

Rarely is the world of decision-making as contained as choosing a gameshow door. We don’t always know the probabilities we’re facing, or the exact magnitude of outcomes. We can differentiate this new layer of cloudiness as “uncertainty,” as opposed to risk.

An illustration will help. What if we were to play the same game, only this time, Monty had the option to offer us the switch or not, at his discretion. How would we decide with this new wrinkle of uncertainty added? We now have to factor in psychology, economics, incentives, and a broad swath of nonmathematical domains.

Is Monty feeling generous or like a trickster today? Did he get a good night’s sleep? Does he have low blood sugar?

Has the show been giving away too many big prizes and the network is demanding they tighten the purse strings?

Or have the show’s ratings been lagging and they need to inject more excitement with big winners?

Do we think Monty likes or dislikes us for some reason?

Suddenly, probability theory isn’t enough.

The below is actual dialogue from one of the shows. In a familiar set up, after the contestant chooses Door 1, Monty opened Door 3, revealing a goat. Monty pulls out a large wad of bills and offers $3,000 not to switch to Door 2:

“I’ll switch to it,” insisted the contestant.

“Three thousand dollars,” Monty Hall said. “Cash money. It could be a car, but it could be a goat. Four thousand.”

“I’ll try the door,” the contestant says, rejecting the cash offer.

“Forty-five hundred. Forty-seven. My last offer: five thousand dollars.”

“Let’s open the door.” The contestant is hell-bent on switching.

“You just ended up with a goat,” Monty says. “Now do you see what happened there? The higher I got, the more you thought that the car was behind Door 2. I wanted to con you into switching there, because I knew the car was behind 1. That’s the kind of thing I can do when I’m in control of the game.”

Perhaps Monty didn’t get a good night’s sleep?

When we make decisions in highly uncertain environments, one useful strategy goes by the name the “minimax rule.” It simply means, choose the alternative that avoids the worst outcome. “Minimax” gets its name because it aims to minimize your losses if the maximum-loss scenario plays out.

For our contestant, ending up with a goat and no cash is the worst possible outcome. This only happens if they switch. The minimax rule tells us to take the money and stick with Door 1. At least we get the cash, the car is still a potential upside, and we’re no longer subject to Monty’s headgames. We’ve removed some of the uncertainty by minimizing the worst case.

Another application of the minimax rule is called value investing. Value investors obsess over worst case scenarios and protecting the downside. They use concepts like margin of safety and circle of competence to minimize the maximum potential for loss. Value investing guru Mohnish Pabrai made famous the concept of a “Dhandho Bet”: heads you win, tails you don’t lose very much. (This also goes under the fancy name “asymmetric outcomes.”) It doesn’t mean every investment works out; the investing world is more random than Let’s Make a Deal. But it’s a logical approach to tame an uncertain world.

“Wall Street can not distinguish between risk and uncertainty and gets confused between the two. Savvy investors like Buffett and Graham have been taking advantage of this handicap that Mr. Market possesses for decades with spectacular results.” -- Mohnish Pabrai

Benjamin Graham made famous an investment approach that epitomizes the minimax rule. In the business world, the typical worst case scenario is that the company declares bankruptcy and is liquidated. Graham would estimate what a company’s assets would sell for on the courthouse steps of a liquidation. If he could pay significantly less than his estimation, it was an attractive investment opportunity. Minimax in action.

At Farnam Street, we continue to search the world for similar minimax situations. They’re rare, especially in overly-inflated markets, but they do occur. In 2011, a tsunami and nuclear disaster struck Japan. Panicked investors abandoned Japanese securities en masse. We were happy buyers of these businesses at prices Graham would have approved of.

Around the same time, a high profile bankruptcy of Solyndra sparked a panic in the solar panel manufacturing space. It took a few years to unfold, as everything takes longer than you think it should. By early 2013, a basket of these solar companies had fallen 95% from its highs. The only question we had to answer was, “In a worst case scenario, would we get more for these assets on the courthouse steps than we’re paying now?” That was a safe bet, so we scooped them up for cheap. Both our Japanese and solar industry investments produce terrific returns.

It doesn’t always work. We’ve made other investments using the same methodology that didn’t pan out. Sometimes we misestimate the worst case scenario, like when the price can languish without the threat of a liquidation event. Sometimes the wad of cash Monty is offering dwindles. But across enough investments of this style, you don’t need a perfect batting average to do quite well. Warren Buffett made his earliest (and largest percentage gains) following this exact strategy. He still invests this way in his personal investment account.

“Investing is simple, but it isn’t easy.” -- Warren Buffett

In our opinion, a Grahamian minimax approach to investing is a self-evident truth. Of course it works. A logical follow-up: why doesn’t everyone do it then? First, it’s hard to maintain the required level of patience and discipline to faithfully execute such a strategy. The markets are mostly efficient, and assets aren’t regularly priced at such risk-absolving discounts. You have to bide your time. Plus, it’s more fun to talk about recent hot IPOs (fake meat?) or speculate on new business models (cannabis?).

“Without the aggression and the idea that opportunities will be few, you’re not going to have a great result as an investor over a lifetime.” -- Charlie Munger

Second, often Graham-style investments are only available in smaller companies. The sophisticated investors are too big to participate in these smaller ponds. Our small size is a definite advantage and increases the chances we’ll find low-risk/high-reward situations.

The pickings are slim in today’s expensive world. But the next time a handful of these opportunities arise, expect a call from us that now is the time to put money to work.

“Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble.” -- Warren Buffett

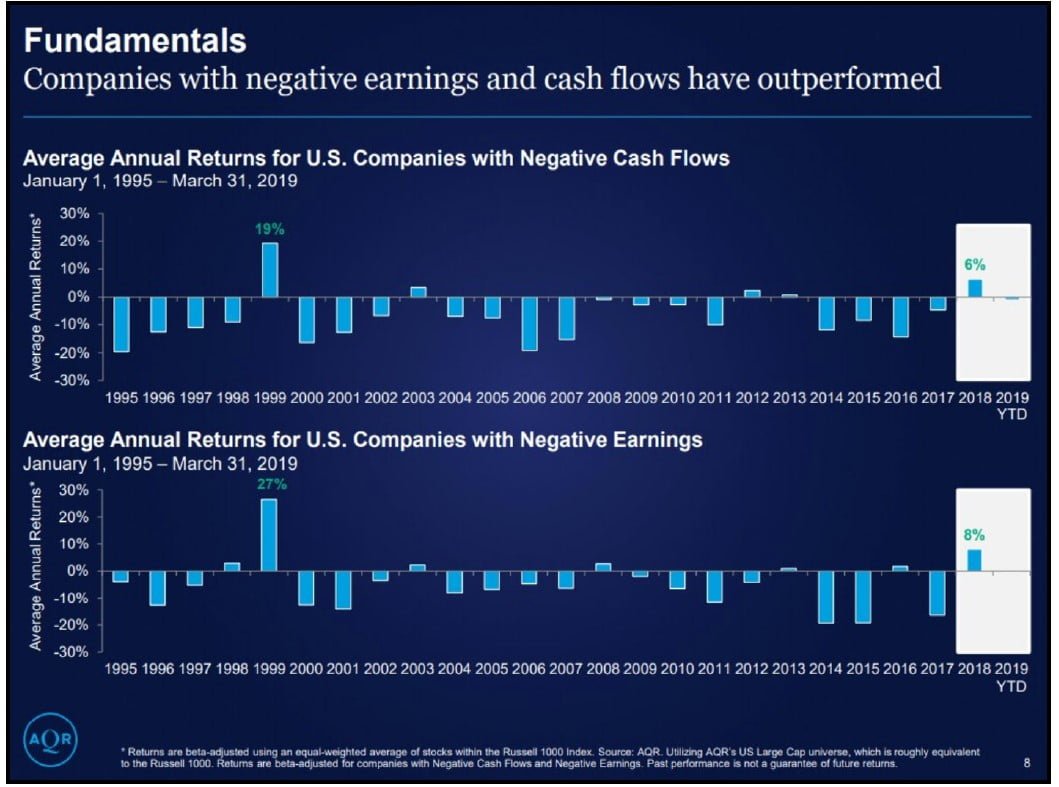

Fun-duh-mentals?

Counterintuitively, companies with negative earnings and cash flows have seen their stock prices outperforming lately. The last time investors were this unconcerned with business fundamentals was 1999.

When will fundamentals matter again? The truth is, no one knows, including the experts. In late 2007, Bloomberg polled a group of professional market forecasters. They all agreed 2008 was shaping up to be a prosperous year; the average prediction was a gain of 11 percent. No one predicted a down year. By the end of 2008, the S&P 500 was down -38%. Swing and a miss. Today’s professional forecasters won’t see the next one coming either, so don’t look to them for a heads up.

Travel

It was a busy quarter for travel. Plenty of opportunity to kick the tires on current investments, explore new ones, and converse with other professional investors. It’s cold comfort that most are also struggling to find good investment ideas in today’s climate.

In April I traveled to Toronto for my usual visit to Fairfax Financial and Prem Watsa. Lonnie and I also traveled to New York for the Biglari Holdings shareholders’ meeting. Early May took us to Omaha for our predictable annual pilgrimage to see Warren and Charlie. If you want to see what all the fuss is about, someone uploaded on youtube the Q&A sessions for the meetings going back to 1994. Watching these videos is like painting the Golden Gate Bridge for me. Once the painters get to one end, it’s time to start again at the other. It’s hard to absorb too much wisdom from these guys.

In mid-May I took an unexpected trip. At the last minute, a friend asked me if I wanted his ticket to a new event called Capital Camp (thanks Jeff!). It was an eclectic mix of value investors, quants, private equity, debt, and venture capital--every continent of the investment world was represented. It was held in Columbia, Missouri--for excitement, a big tornado touched down about 20 miles from us. The speakers were phenomenal, as were the other attendees (it wasn’t a cheap ticket). I didn’t have a bad conversation the entire 4 days. I found it insightful that even outside of my value bubble, investors generally feel there’s too much money chasing too few good ideas. Everyone has doubts about forward returns keeping pace with previous results. They can’t always admit it publicly for fear of investors pulling money. Some things don’t change.

In June, I made a trip up to Intel’s campus in Portland, Oregon and gave a talk. My host instructed me to aim the message toward a beginner audience. That got me thinking about what are some first principles of investing--fundamental ideas that we all might agree are true. I titled the talk “A Few ‘Capital-T’ Truths of Investing.” It was against Intel policy to record the talk, but the slides are available here. (They aren’t terribly informative as I don’t like a lot of words on my presentation slides, but maybe each picture is worth a thousand words?)

As always, we’re thankful to have such great partners in this wealth creation journey.

Jake & Lonnie

This article first appeared on ValueWalk Premium

{kind=link}