Elm Ridge commentary for the fourth quarter ended December 31, 2021, titled, “The Punch You Don’t See.”

Q4 2021 hedge fund letters, conferences and more

“Graham and Dodd investors are people who place a very high value on having the last laugh. In exchange for the privilege they have missed out on a lot of laughs in between.” – Michael Lewis

“It’s the punch you don’t see coming that knocks you out.” – Old Boxing Adage

“Everybody has a plan until they get punched in the mouth.” – Mike Tyson

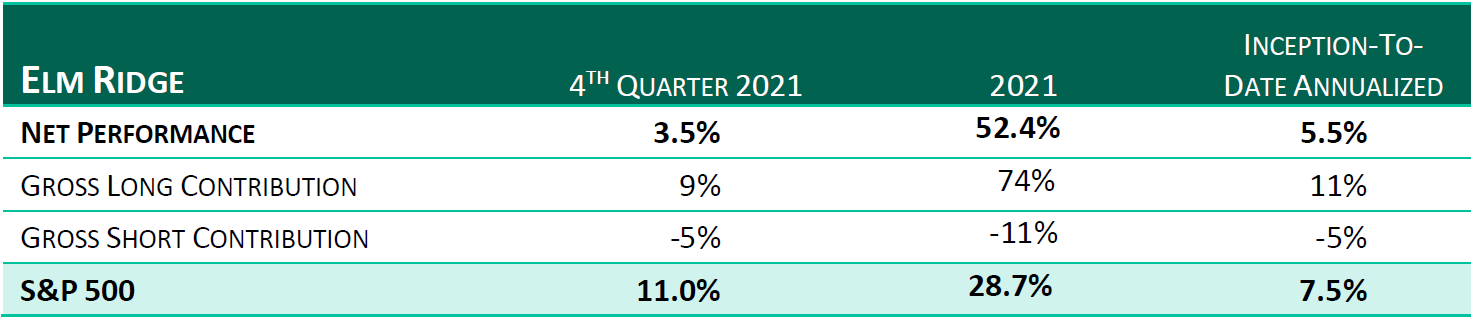

Elm Ridge’s Performance

Despite the weak performance of our energy holdings over the last two months,1 we posted an acceptable fourth quarter and a much better 2021 – although this is just a down payment on the cost of maintaining such a non-consensus portfolio over the past several years. While the broad measures of value continued to underperform (with the Russell 1000 Value Index trailing Growth by four percentage points during both the last quarter and year, extending its annual losing streak to five), our longs nearly tripled the market’s performance, while that of our shorts (adjusted for average exposure) trailed (good for us) by more than 10 points. While our 40% average weight in energy held up its end, with an 80% weighted return, our industrial and materials stocks posted 100+% gains, with consumer discretionary coming in over 70% and financials over 50%. In each case, our picks performed ahead of their sector. In fact, we ended up with positive alpha in 10 of the 11 GIC sectors (save healthcare) and even generated some from our technology shorts,2 despite its continued outperformance. There must have been at least one or two investors or algorithms that decided our left-for-dead “old economy,” non-CBGB (Certified Bonafide Good Businesses,3 with one’s friends providing the certification) holdings might not be so dead after all.

Your eyelids are feeling heavy. But we’ll tempt fate and continue. Even after their 70+% run, our longs’ soaring profitability (we’ll get to the why later) has left them selling at a consensus PE multiple well less than half that of a year ago (7.8x v 21.5x compared to our 5.5x and 9.3x estimates), while that of the broader market has barely budged (21.1x v 22.8x, still higher than any pre-COVID reading since the 1998-2000 tech bubble). While the CBGBs may get priced based on low single-digit free cash flow yields many years out, we calculate that ours will be yielding nearly 20%4 in the coming year. And as they have both cleaned up their balance sheets and taken the market’s direction to limit capital investments, we’ll see most of that through dividends and buybacks. And yet, while this all seems so early 2000, one thing I’ve learned over the past 20+ years is that no one is going to be persuaded by what I think are compelling arguments about the instability of the status quo. No doubt, I’m getting revved up while you’re getting drowsy. But after a decade in which the S&P soared 450% while the Russell 1000 Growth outpaced the 1000 Value by a mere 260%, it seems most everyone is too confident in their investing ability to be swayed by our silly logic and statistics. We’ll just keep this one short(er).

What Me Worry?

I graduated from the college of the street

I got a PhD in how to make ends meet

Inflation in the nation don’t bother me

‘Cause I’m a scholar with a dollar

You can plainly see

– Quincy Jones, The Dude, 1981

“How did you go bankrupt?” Bill asked.

”Two ways,” Mike said. “Gradually and then suddenly.”

– Ernest Hemingway, The Sun Also Rises

Not So Temporary Inflation

Six months ago, we argued that ever lower inflation and interest rates have boosted market returns over our investing lifetimes and that almost all popular investments are tied to that same regime. Despite the then prevailing market narrative – that inflation was merely temporary and would reverse once expanded unemployment benefits ran out in the fall – having faltered, the Fed stuck with its monkey business and rates are still lower than they were in early 2019. And so, while the SPAC, IPO and no-profit cohort hit an air pocket, the five high-multiple mega cap franchises5 (NASDAQ:AAPL, NASDAQ:MSFT, NASDAQ:AMZN, NASDAQ:GOOGL and NASDAQ:TSLA), dominating most portfolios, returned an average of 25% over the past six months, with the reported values of most real estate, private equity and venture capital investments tagging along for the ride.

“Price Matters.” So, our lead slide would proclaim as I pitched my GS Value product in the mid-nineties. What an anachronism. In more modern times, numbers get tossed around with little thought. I just read a recommendation for an aircraft supplier with a price target based on a 69x multiple on 2025 earnings discounted back. “How’d they come up with that?” I asked Sheetal. “Because seventy seemed too high.” Meanwhile, even the buy recs on Alcoa, a cost- and carbon-advantaged aluminum producer,6 are using EV/EBITDA7 multiples of 4x or so compared to targets more than four times that for the CBGBs that shape that aluminum into cans. In fact, one recent note admitted that if it sold at a 6x multiple, “the low end of copper and steel mill peers,” their target would be some 50% higher. And only us codgers would remember that the last time Alcoa was in this kind of competitive position – before Chinese producers killed the market with the carbon-spewing coal-based capacity that is now being curtailed as scarce power gets shifted to better uses – it often sold at a 10x multiple, which would get you close to a triple.

I could go through a similar exercise with any number of our holdings. But after 10 years of CBGB success, I understand how that might put most investors to sleep. There is no point arguing what’s around the corner while everyone sees an open road straight ahead. Our stocks won’t matter until the crowd reverses course. They just don’t count.

Turning back to what people care about, it is true that some of today’s tech giants sell at lower multiples than the four horsemen (Microsoft, Intel, Cisco and Lucent) did at the August 2000 peak of the tech bubble (that is if we exclude TSLA, where price targets seem to be discounting back some mid-century alternate reality, when it corners the market on almost every key technology and Elon Musk buys himself a continent). We neither expect another 70% decline, nor the 15 years it would have taken for an investment in them get back to breakeven. Indeed, if AAPL, GOOGL and MSFT are somehow able to defend their competitive positions and keep growing at high rates over the coming decade, from a much higher base – even as they try to impinge upon each other’s core markets – and inflation and interest rates stay low, there is some chance these could produce a reasonable rate of return over time. But if they have just a small stumble on that path, we’d bet that at least some investors will finally begin to look elsewhere and try to bring their friends along as well. With the market cap of the five tech giants nearly 10x the weight of the entire S&P energy sector, a small shift in attitude could go a long way.

This opportunity has been a decade in the making. Although getting to the root cause (if there is one) is an enterprise just too big to flesh out here, we think that ten years of easy money has left us with a massive misallocation of resources and a concomitant generation of investors (who’ve seen the virtues of sticking with their friends and the costs of straying from the herd) currently unable to address it.

Lower Borrowing Costs

Theoretically, lower borrowing costs should spur real investment. And although they do have an immediate effect on housing demand, I’ve never heard a company justify a capital expansion project based on lower rates. But in the current regime, where professional investors are worried about any actions that might prove embarrassing or detract from current stock prices, the market has bestowed excessive rewards to those who: acquire capacity (or technology) rather than developing it in-house; lever-up asset-light businesses that rely on others to supply them with product; switch to subscription models over pay-as-you-go (regardless if such a move improves long-term cash flows); or promise huge theoretical TAMs8 that can’t be proven too optimistic for years to come. Meanwhile, the capacity to build and deliver goods in industries outside of those velvet ropes (and investors’ comfort zones) has fallen by the wayside.

Soaring asset prices have come at a cost to consumers in general.9 Rather than directing funds toward meeting the demands of a growing world and fixing our aging infrastructure, we’ve sent it to the insiders selling shares in excessively valued innovation stories and producing and powering tech hardware that creates nothing (I’m sorry, Crypto10). The world is now short some of the basic building blocks (aluminum, steel, chemicals, power, transport capacity, etc.) that support an industrial economy. And given that these forlorn industries face such enormous hurdle rates (e.g., compared to buying in their own depressed shares), they will need to be rewarded with much higher profits and prices than would have otherwise been the case.

From a very narrow point of view, we, that is Elm Ridge, don’t need this situation to correct itself in the short term. Buybacks will allow our ownership stakes to grow at maybe double-digit rates while we wait. If we get a big market setback in the interim, these will work even better. Add in the enhanced profitability needed to meet demand along with valuations more in line with historical averages, and you have a Triple Lindy.11 As was the case in the aftermath of the 1998-2000 tech and 2005-07 housing bubbles, we would guess, when all is said and done (and at this point we admit there’s been far more said than done12), we’ll end up getting much more than paid back for what we’ve endured thus far. And three, now four, pages in, it’s pretty clear that I still can’t restrain myself from spewing some venom at the folks who will have allowed us to make it.

Keep your head moving.

Footnotes

1 The S&P E&P Index (SPSIOPTR) fell almost 10% during that time, leaving it flat on the quarter or 11% behind the S&P.

2 As the hit from our shorts’ 20% performance here, still trailed the S&P by 8 points and that of the sector by nearly 15.

3 We discussed these in more depth in our 1q letter that we’d be glad to resend.

4 That is ex financials, whose leverage makes that measure rather meaningless. And it would still yield more than 17% excluding the three

commodity chemical and steel companies that are probably overearning.

5 The word “company” does not show them the proper respect.

6 With both advantages stemming from its heavy use of captive hydropower. Yes, I used this comparison in the last letter. But as cash flow

estimates for Alcoa are up some 20% since the summer while those of the can producer has edged downward, the gap has only widened.

7 Enterprise Value/EBITDA or Market Value + Debt/Cash Earnings before interest and taxes.

8 Total Addressable Markets.

9 See “The Fed’s Doomsday Prophet has a Dire Warning about Where We’re Headed,” Politico, 12/28/21. https://www.politico.com/news/magazine/2021/12/28/inflation-interest-rates-thomas-hoenig-federal-reserve-526177

10 It now takes about the equivalent of nine years of household-equivalent electricity to mine one bitcoin, with its usage/bitcoin growing at a 400% compound growth rate over the last decade. https://www.nytimes.com/interactive/2021/09/03/climate/bitcoin-carbon-footprint-electricity.html I know you didn’t ask for my opinion on Crypto, but I know I’ll get a bunch of pitches after every letter. While I am not 100% sure most Crypto will eventually end up almost worthless, I’d go with a 95+% number. The case is simple. I just saw an ad for a company that will allow you to “invest” in Crypto for your IRA that “offers easy access to more than 100 cryptocurrencies, like Bitcoin, Ethereum, and Solana…”

11 https://www.youtube.com/watch?v=rDMMYT3vkTk . Finally, a change from our usual Redd Foxx reference.

12 I thought this came from Lou Holtz but in looking for the reference I found that he lifted it from Aesop.