Background/Introduction:

For some reason I ran into a “Twitter battle” about Auto1, with the main Bull case being that Auto1 Group SE (ETR:AG1) is the German Carvana. In addition, some good investors that I follow have revealed Carvana Co (NYSE:CVNA) as a position.

Q4 2021 hedge fund letters, conferences and more

Time to have an “Armchair investor” look into Carvana. The goal here is two fold:

- Understanding if Carvana as such is a good business (and maybe even interesting as investment)

- Finding out if Auto1 could indeed is or can become the “German Carvana”

Full disclosure: the guy who is writing this, lost significant money with investing into Cars.com, another US online car company. So as always: PLEASE DO YOUR OWN RESEARCH !!!

The Carvana Business “Bull Case”

important: Just as I was about to finish the post, Rob Vinall has released his 2021 letter to investors with a very convincing pitch for Carvana. I highly recommend to read it first.

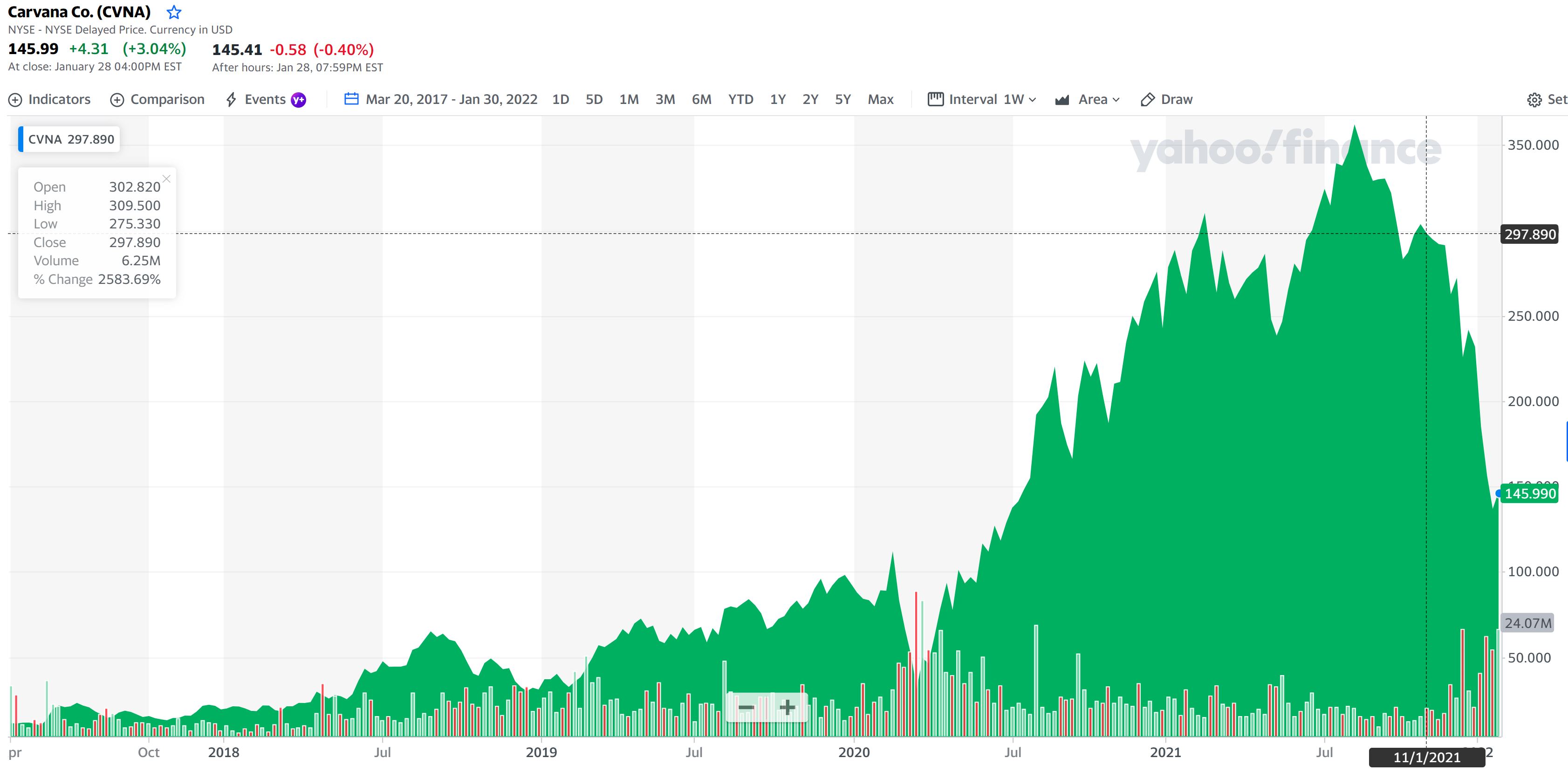

Carvana is a 25 bn USD market cap company, that similar to Auto1 is buying and selling used cars online. The share price has been suffering lately:

A big difference to Auto1 is that Carvana historically mostly bought wholesale (i.e. from rental companies and the well developed US auction market) and then sold directly to Consumers (B2C) whereas Auto1 still mostly buys from consumers and sells to businesses (C2B).

Carvana is famous for its “24 hours used car vending machines”, but customers can also get their cars delivered to their home with a 7 day “no questions asked return” period. An introduction to the business model of Carvana can be found here.

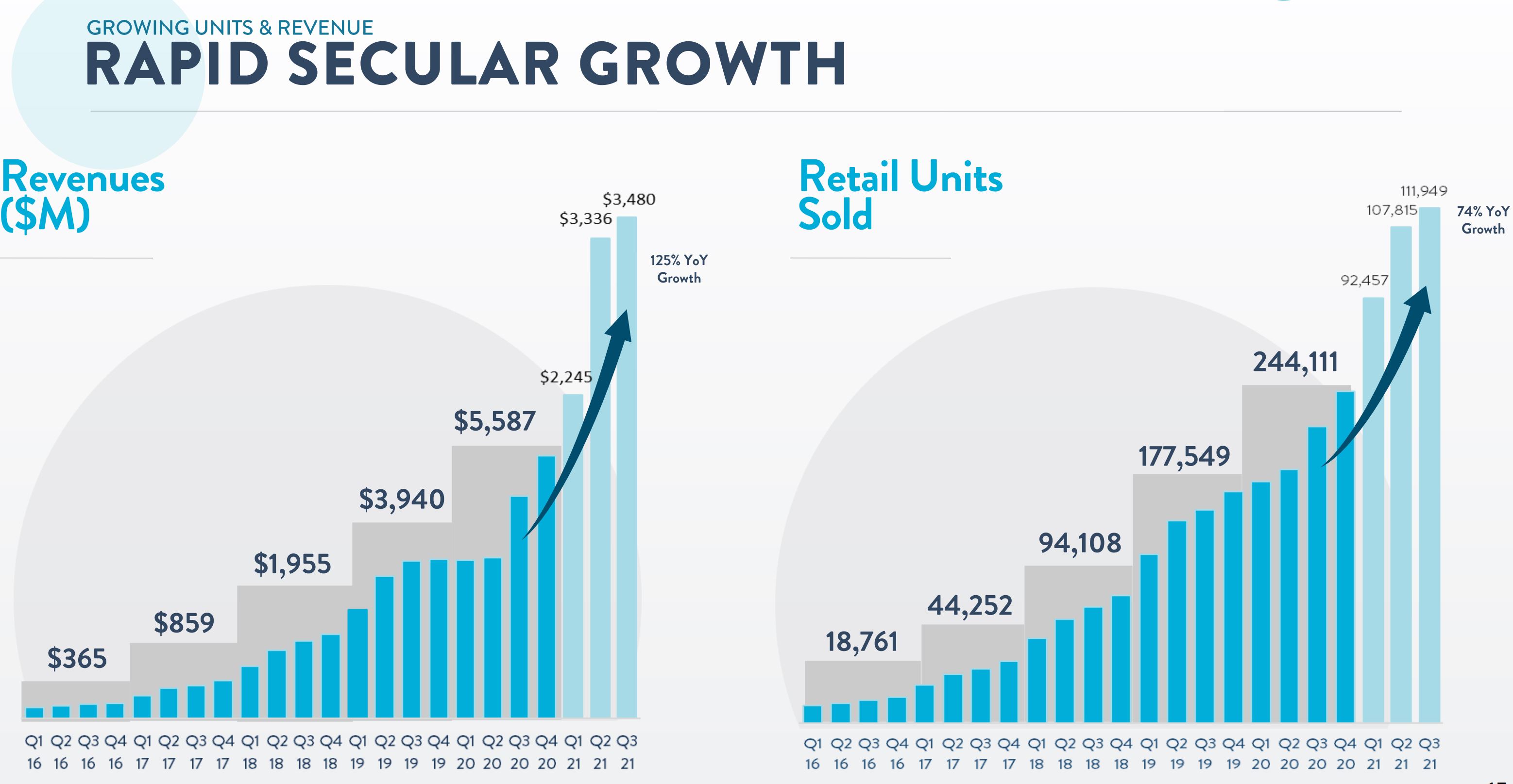

The company has been growing like crazy, from 130 mn USD sales in 2014 to 5,6 bn in 2020 and most likely more than 10 bn in 2021. These charts show the impressive growth:

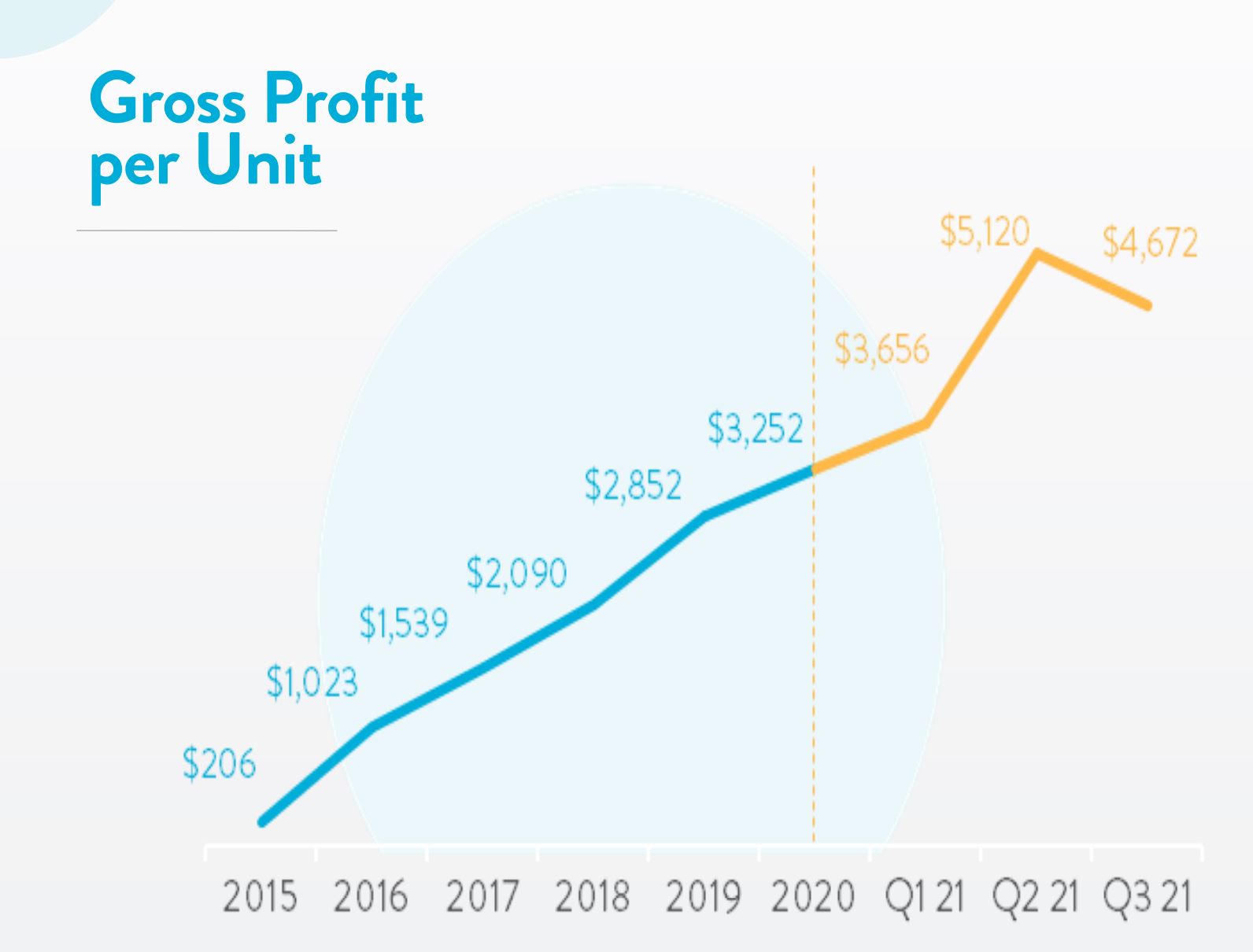

Even more astonishing is the gross profit per unit:

Despite the growth, Carvana still only is about 1% of the 900 bn USD US used car market, so there is a lot of room to grow for them based on TAM.

The company turned EBITDA positive in Q3 2021 and in the long term plans to have much higher margins:

So let’s assume that Carvana will eventually reach 10% market share (not much) and 10% EBITDA margins, this would mean roughly 90 bn in sales and 9 bn EBITDA which compared to today’s valuation of 25 bn looks like a steal, depending on when the reach it.

Some observations:

- The number of vending machines hasn’t increased since 2020. It seems that these machines are more a marketing gag than an integral part of the business model

- They operate a small B2B vehicle selling business with much lower GPUs and average ticket size. The GPU for Retail is really substantially higher.

- By its nature, the business is capital intensive. Carvana had to raise capital several times since is IPO and is carrying net debt of around 3,3 bn USD. More sales mean more inventory which means more capital required.

- Free Cashflow in the first 9M 2021 was minus 1,8 bn USD. It needs to be seen when and if they can fund the growth from internal CF

- The business had extreme tailwinds from the increase in used car prices over the past months. This helped to increase sales as well as GPU. It needs to be seen how these KPIs develop when the market is normalizing

- more than 50% of the GPU are not from selling vehicles but from providing financing (and insurance) to customers

- Carvana originates car loans but sells them on and records an upfront profit. They seem to keep a portion of the securitization vehicle on balance sheet.

Here it gets kind of interesting. The father Ernest Garcia II of the current CEO Ernest Garcia III owns a company that also sells used cars and provides auto loans. This company is called DriveTime and used to be a listed company called UglyDuckling. The company IPOed in 1996 and then was taken private at a much lower value in the early 2000s. DriveTime seems to have focused always on clients with a “problematic” credit rating.

To make things even more interesting, Carvana sells the loans to a company owned by the father Ernest Garcia II (who is a convicted felon). This has arised interest from the press a few times and articles can be found for instance in Forbes and the WSJ. Carvana is actually a spin-off of DriveTime, which itself seems to sell mostly B2B.

To make things more complicated, Carvana also buys cars from DriveTime, buys and leases back inspection centers from another Garcia company and Ernest Garcia III seems to own a significant stake in DriveTime.

To top off things, Garcia II has sold around 3,6 bn USD worth of shares already. Not surprisingly, short sellers are circling the company and claim that Caravan is a big fraud.

One other aspect to be considered is the following: It seems that most of Carvana’s business comprises sub prime auto financing. This is from a comparison site:

Carvana considers working with consumers regardless of their credit history — although there are age and income minimums. Because it doesn’t require people to have minimum credit scores for a car loan, you might qualify for a Carvana loan even if you have low credit scores.

and

Since there are no minimum credit score requirements or prepayment penalties, it could also be a good fit if your credit history has a few dings or if you plan to pay off your car loan early.

Carvana is not disclosing a split of how much of their loans is subprime. However selling cars to people who would otherwise not get any vehicle or a comparably expensive vehicle can explain the growth achieved to a certain extent. One question that would be interesting to look at is the following: How large is the sub prime market and how would GPU etc. look for the Prime market ?

Assuming a 10% market share overall for Carvana doesn’t seem much, however if that would be 50% or more of the subprime market, then it might be already a “stretch goal”.

Limits of Armchair Investing

For me as an “armchair” investor, both, the related party topics and the subprime angle make Carvana uninvestable. However, for professional investors who know the US market and can judge how long the arms of the Gracia’s are when they transact between themselves, things could be different.

A quick look at the share price shows that similar to other highflyers, Carvana’s stock has suffered and is (almost) back to pre pandemic levels, without being cheap based on my understanding of the business:

However competitor Vroom Inc (NASDAQ:VRM) has been hit much harder by the recent selldown than Carvana, similar to Auto1:

And this despite Vroom’s effort to mimikri Carvana by buying a non-prime auto lender recently.

Auto1 vs Carvana

The current bull case for Auto1 is that Auto1 is actually the German Carvana and should be valued accordingly (i.e. more like 2,5-3 times sales vs the current <1 multiple.

As mentioned above, this is very questionable, as Carvana is mostly a B2C business whereas Auto1 is exactly the opposite, i.e. buying retail and selling wholesale (C2B).

This is why the avg selling price for an Auto1 car is only around 1/3 of Carvana, and the GPU only around 700 EUR which in my opinion maybe just covers marketing cost.

With Autohero, Auto1 has now added a copy of the Carvana model and tries to sell retail. The segment grows relatively quickly but is currently only around 14% of sales and GPUs are even lower at around 400 EUR. And this is before marketing costs.

The main problems in my opinion with Autohero are the following:

1) They had to create a separate brand which makes advertising very costly. The original brand says “we buy your car” and is obviously not a good fit for this business model. So they are now in the strange position, that they need to advertise separately to buy and then to sell a car which in my opinion is not sustainable at all.

2) My main issue with Autohero is that the used car market is very different in Europe and Germany compared to the US. The used car market in the US is ~900 bn annually, Germany is around 100 bn EUR annually and Europe seems to be 400 bn EUR, so roughly half of the size. Rolling out across Europe is much harder, due to different languages, preferences and cultural differences compared to the US (and in some countries, the steering wheels are on the wrong side).

Another big difference is that the market as such is structured very differently from the US:

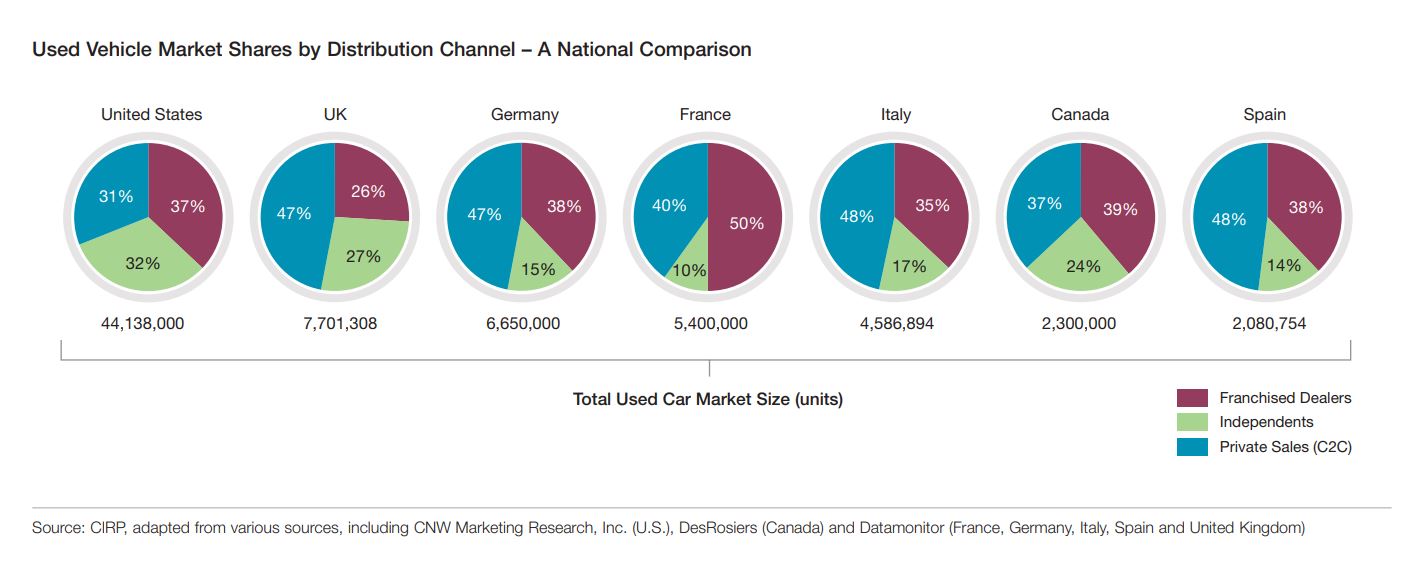

Germany for instance has a very developed C2C market (see above) dominated by the big portals Autoscout and mobile. the share in value of the C2C market is much higher than in units. This makes the market quite transparent. Both, Autoscout24 and Mobile have already started to create and sell their own inventory online (smyle for Autoscout, mobile vs. Instamotion).

Another difference is that in Germany the share of independent dealers, who might struggle to offer an online channel is very low. Most dealers actually belong to OEMs and they are rolling out online business models at large scale as well.

So even if Autohero would become a success, its TAM and runway would be a lot shorter than Carvana’s in the US, but looking at the competition, this will be really hard and expensive.

On top of all this, I think it will be very difficult for Auto1 to pull off an equally profitable car financing business. The subprime market as in the US doesn’t really exist like in the US and in general financial institutions are not getting away in charging interest rates like in the uS.

Auto1 has bungled Auto1 Fintech via a series of shady deals that forced co-founder Hakan Koc to step out form the Management. All the other competitors (portals, OEM) offer cheap and easy financing, so I think with regard to the subprime part of Cravana, this can not be replicated in Europe and Germany.

Finally, Auto1 will face much more dilution than Carvana which was able to raise the required capital at a much higher valuation.

Wrapping up Auto1 vs Carvana:

Overall, for me the answer to the initial questions look as follows:

- Carvana itself is hard to judge for me as an “Armchair investor”. From the outside, there seem to be many question marks. However I have to acknowledge that Rob Vinall’s pitch sounds quite convincing.

- No matter how good Cravana’s business is, Auto1 will most likely not be able to follow the trajectory of Carvana, as the German/European used car market is very different, much smaller and Auto1 has a very different starting position. To me, Auto1 rather looks like the German version of Vroom than Carvana.

Article by memyselfandi007, Value And Opportunity