Disclaimer: This is not investment advice but my personal (and often unqualified) opinion. PLEASE DO YOUR OWN RESEARCH !!!

Q4 2021 hedge fund letters, conferences and more

Background & Intro

Long term readers of my blog might remember a certain obsession with travel companies over the past few years. Among other posts, the main analysis were these ones:

- Part 1 – Lastminute.com

- Part 2 – Expedia

- Part 3 – Trivago

- Part 4 – Flight Centre – book review

- Part 5 – Flight Centre

- Part 6 – Tripadvisor

- Part 7 – Tripadvisor (cont)

- Part 8 – GDS (Sabre, Amadeus etc.)

- Part 9 – Expedia (cont)

- Part 10 – AirBnB

With the exception of a short, mildly successful (and very lucky) speculation in Expedia, I found the sector as “too hard” for me to invest as too many things were moving at the same time:

The more I look into those companies, the more difficult the sector seems to become. There is a lot of fundamental change going on, Which on the one side is good for agile players but on the other hand makes it very difficult to predict anything and extrapolate trends from the past.

As a Value Investor, unpredictable fast-moving industry changes are difficult. In order to invest in such a sector, there should either be a significant moat and/or fantastic management or a very cheap valuation.

So why now looking again at a travel company ? To be honest, I was motivated by a comment from “Celebrity investor” Philipp “Pip” Kloeckner in my Twitter feed as I introduced HomeToGo as a part of my “Bumsbuden Wikifolio” where I collect German shares that I think are staying away from makes a lot of sense.

Pip commented that he has a very different opinion, which is not surprising, as he is sitting on the Supervisory board and seem to hold around 100k shares that he received for consulting in the early days of the company.

HomeToGo – The company and the business: Vacation rentals

HomeToGo SE (ETR:HTG) was founded in 2014 and went public on September 22nd 2021 via a SPAC (more on that later). It’s business focuses on vacation rentals, basically it is a kind of German version of AirBNB.

The big difference to AirBnB is that HomeToGo acts both, as an aggregator as well as selling its own inventory. These are of course two very different models:

The aggregator model, i.e. aggregating and “reselling” inventory from competitors is low margin but also low maintenance. However, as Trivago shows, reseller models are not easy to run in the long term as resellers get squeezed from all sides (big guys, Google).

Vacation rentals is an interesting business. In essence, it is a two sided market place with renters on one side and landlords on the other. AirBNB is the big guy, but also Booking and Expedia have massively moved into this area.

As I have outlined in the AirBNB post, a market place with lots of participants on both sides and very heterogeneous goods is not easy to maintain and does not scale easily. These businesses have to acquire and retain a lot of participants on both sides of the market place which is expensive.

As far as I understand, HTG started as pure Meta search (like Trivago) but has taken over a few companies with rental inventory and are pushing hard to sell their own inventory, which if I am not mistaken, they call “on site revenue”. This clearly pushes up take rates which have improved from ~6% historically to ~9% in Q3 2021.

HTG’s recent growth relative to competitors:

This is at an aggregate level how HTG managed to grow in 9M 2021

9M numbers HTG 2021 (vs. year ago):

Gross revenue +9% (not Booking revenue)

Net Revenue +28%

This looks pretty decent, but let’s compare this with the big guys:

Gross bookings: +48%

Revenue +67%

9M Expedia numbers:

Lodging +87% (Hotels & Rentals)

So both, top line and net revenue growth pales compared to the big guys. This is pretty disappointing, as HTG has increased marketing spend significantly compared to 2020. Over the 9M 2021, HTG spend 1,15x their gross profit on marketing alone vs. 0,8x in 2020. In the first 6M, pre SPAC this ratio was even higher with 1,3x.

To compare this with AirBNB: They spend 0.23 of gross profit for sales and marketing in 9M 2021 vs 0.3 in 9M 2020. So HTG hat to increase marketing spend by several magnitudes compared to AirBNB in order to get a fraction of growth.

So it is quite clear that growth comes almost exclusively from massive marketing spend and acquisitions and they are nowhere near a scale where marketing costs would allow to grow and earn money. There seems to be little “organic” growth which for a year like 2021 is very surprising.

Other observations:

- HTG generates relatively little working capital “float” which ifor other online travel businesses is an important internal financing instrument

- Gross profit calculation in my opinion looks quite strange compared for instance to AirBNB which “only” shows gross margins of 80% vs. 95% for HTG

- quite intensive use of “alternative” metrics such as “Gross Booking revenue” and “future receivables”

- the management of HTG only holds 7% of the company in aggregate which indicates limited value creation before the SPAC

- Initially, the SPAC expected to raise 350 mn (275 SPAC + 75 mn pipe). in the end, only 250 mn EUR cash was raised (see below)

- also in 2019, pre pandemic, growth was quite low with 20% for such a young company despite having acquired two businesses in 2018. The high growth phase seems to have been over by then.

- Vacation rentals enjoyed a “special boost” because of people wanting to avoid crowded hotels in the last year. It needs to be seen if this will continue or if tourists at some point in time go back to “full service”

- They acquired a small Software company Smoobu for around 20 mn EUR in 2021 which seems to be their “subscription” business that they show in the investor presentation

- A significant contribution to past growth seem to have been acquisitions, such as Casamundo in 2018 or Tripping.com. Acquisitions seem to be the cornerstone of their growth strategy

- Interestingly, all employees of Casamundo were fired in 2020. That might have saved the bottom line but is maybe a bad start to acquire similar businesses in the future

- Before getting “SPACed”, they raised already around 175 mn USD, which explains the low shares of the founders

- As part of its Meta-search business, form 2018-2020, around 60% of revenues were concentrated on the biggest 3 partners, according to the prospectus, for the first 6M 2021 the biggest partner alone accounted for 40% of revenues

- From 2018-2020 HomeToGo has burnt around 25 mn EUR per year, the 150 mn uSD raised in December 2018 seem to have been gone by the time of the SPAC

- As of 6M 2021, according to the prospectus, still 60% of sales came via 3 partners, thereof 40% from one partner. So the Meta search business seems to have the exact same issues as struggling Trivago

- Acquiring retail customers is expensive and I didn’t really find good information how valuable these customer relationships are. Vacation rentals are more infrequent purchase which usually means that LTVs are not so great.

- Competition even in the mid market is fierce. There seem to be at least another 5-10 or so larger players competing both, for renters and landlords.

- On a personal level as customer, I find HTG’s UX quite mediocre. HTG’s own inventory often has very few ratings. They claim to aggregate among other AIRBnB but when I did a few checks, AIRBnB inventory didn’t show up. From a customer perspective, I do not think that they have any USP.

- Again, on a personal level, I did use almost exclusively vacation rentals during the pandemic, but I am longing to go back to comfortable hotels.

The SPAC

The SPAC that actually merged with HTG was initiated by Klaus Hommels, who, surprise, was already invested into HTG before. Hommels is a European VC with a decent reputation.

The SPAC as such was not so bad as others, especially with regard to the SPAC’s founders shares which had to clear a certain hurdle in order to vest according to the prospectus (Prospectus-_2021-09-20

Investment by the Founders – The Founders hold class B shares (“Founder Shares” and together with the class A shares of the Company, the “Shares”) that are convertible into class A shares of the Company (the “Public Shares”) and 5,350,875 Class B warrants (the “Founder Warrants”) that will be exercisable for Public Shares. 2,551,667 Founder Shares (including the 207,372 Founder Shares redeemed by the Sponsor as part of the payback of the remaining amount under the additional sponsor subscription, which are now held as treasury shares by the Company) convert into Public Shares on the trading day following the consummation of the Business Combination. 2,291,667 Founder Shares convert into Public Shares if, post consummation of the Business Combination, the closing price of the Public Shares for any 10 trading days within a 30 trading day period exceeds €12.00, and 2,291,666 Founder Shares convert into Public Shares if, post consummation of the Business Combination, the closing price of the Public Shares for any 10 trading days within a 30 trading day period exceeds €14.00 (the “Promote Schedule”). The Founder Warrants have substantially the same terms as the Class A warrants to subscribe for one Public Share, ISIN LU2290524383 (the “Public Warrants”), including the same stated exercise price.

Looking at the chart, we can see that the shares never even got close to the hurdle and I guess that’s why the company now has a lot of treasury shares:

Actually, 36,6% of the initial SPAC investors wanted their money back which was then celebrated as a success by the initiators. So instead of 350 mn, they only raised 250, leaving them short 100 mn.

Valuation

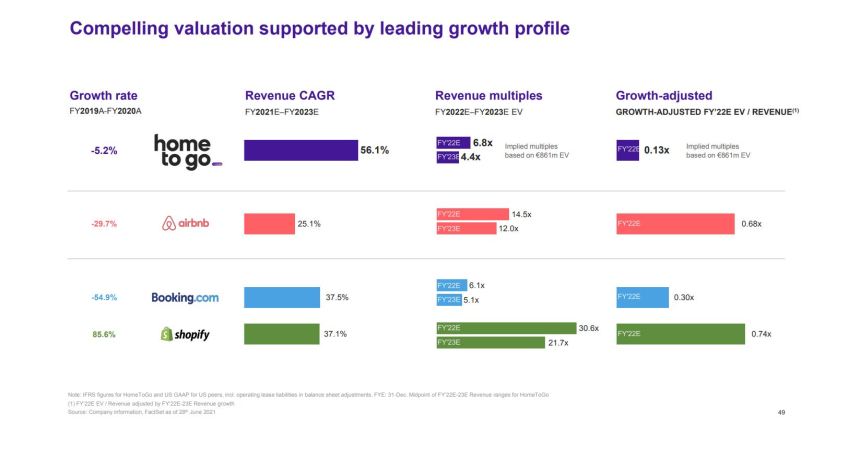

In the original SPAC presentation, this slide was presented to “anchor” HTG’s valuation, humbly comparing HTG with AirBNB; Booking and Shopify (!!!). I guess only the very astute observer sees the small “trick” they used: They omitted 2021 in the growth rate I wonder why ?

Another rather embarrassing mistake is labeling the 4th column EV/Revenue as it is rather obviously Revenue/EV. They also added a chart for “financial guidance” which looks as such:

Anyway, according to the company website, HTG has 127 mn shares outstanding, thereof 8,1% seem to be “Treasury shares”. From the SPAC IPO, the got 250 mn EUR cash and I assume that ~200 can be assumed “free” for 2022.

So this means Enterprise value is (127*0,92*6,50)-200 ~ 550 mn EUR at the time of writing, ignoring the warrants.

Based on trailing revenues, one is getting 85-90 mn in 2021 revenues. Now the big question is clearly how fast can they grow and what margins can they achieve.

Personally, I do think the envisaged 50% growth p.a. and 35% target EBITDA margin is not realistic. 35% is the EBITDA margin that Booking.com realized pre pandemic and let’s be honest: HTG is no Booking. As I mentioned in my AIRBnB post, even AIRBnB is no Booking either. In my opinion, achieving 20% EBITDA is already a stretch.

Assuming that they can increase their revenues to 200 mn in 5 years, this would mean 40 mn EV/EBITDA in 2026. This again would mean that HTG is trading at around 14x 2026 EV/EBITDA which to me looks rich and a significant premium to Booking and Expedia, which trade on the same levels based on 2022 earnings.

My gut feeling says that I would want to pay a max of 7-10 times that number to make it a long investment.which would mean that my “fair” value would be at somewhere between 3-4 EUR per share to fully reflect the risks of the current transformation and the competitive environment.

Overall, the bull case could be made like this:

The company is growing and increasing take rates. The amount raised via the SPAC will allow them to roll up smaller sites which increases revenues and take rates. Ultimately, HTG could become a take-over target for the bigger guys (Booking, Expedia) and can be sold at a premium.

The bear case could be seen as such:

HTG is undergoing a forced Pivot as the original Meta search model is squeezed from all sides similar to Trivago (Google, Booking & Co). The business at the moment is sub-scale and had burned the 150 mn USD raised end of 2018 quickly without a lot of additional growth. They were forced to do a SPAC and it needs to be seen if 250 mn EUR is enough to achieve scale as competition in this area is fierce, both for renters and landlords. In any case, the question is how scalable and profitable vacation rentals are in a “normal” environment. So the risk is high that HTG gets “stuck” along the way and the big guys just need to wait in order to snatch the assets cheaply.

Summary

At this stage I can summarize what can be observed from the outside:

HomeToGo is an online vacation rental company that is currently undergoing a business transformation from a Meta search engine ala Trivago to something more similar than AirBNB.

At the moment some KPIs look ok (take rate) but so far the business doesn’t seem to scale as growth needs to be bought with massive ad spending and the scalability of vacation rentals as such is not yet proven. In addition, competition is fierce from big players but also a lot of mid size players.

As mentioned above, my fair value would be at around 3-4 EUR per share, so the shares still look expensive despite the drop after the IPO/SPAC.

So HTG is clearly not the “worst Bumsbude” in my Wikifolio and within the SPAC universe, it might be even one of the slightly better ones. However it doesn’t look like a potential high flyer either.

Disclaimer: This is not investment advice but my personal (and often unqualified) opinion. PLEASE DO YOUR OWN RESEARCH !!!

Article by memyselfandi007, Value And Opportunity