Boyar Value Group commentary for the third quarter ended September 30, 2021.

Q3 2021 hedge fund letters, conferences and more

“Cryptocurrencies, regardless of where they’re trading today, Will eventually prove to be worthless. Once the exuberance Wears off, or liquidity dries up, they will go to zero. I wouldn’t recommend anyone invest in Cryptocurrencies.” – John Paulson

Stock market investors have a laundry list of worries these days, from partisan bickering over the infrastructure package and a massive social and climate spending bill (amid a high-stakes game of political chicken over the debt ceiling) to supply chain disruptions and a spike in the costs of critical commodities. Geopolitical tensions are escalating between the United States and China—which is undergoing a significant regulatory crackdown—and question marks surround the future of interest rates and the consequences of a future Fed taper. And that’s to say nothing of the coronavirus!

So it’s no surprise that investors are on edge—we’re getting depressed just reading through the list. Yet volatility in 2021, measured by how much the S&P 500 has decreased from its all-time high (~5%), has been tame. (According to David Lebovitz, a global market strategist with JP Morgan, the average peak-totrough decline for the S&P 500 over the past 41 years has been 14.3%.)

In fact, until September, the S&P 500 was regularly charting new all-time highs, at ~54 and counting. But then the stock market got spooked, with the S&P 500 suffering its worst monthly performance (down 4.65%) since March 2020 and its worst September performance since 2011 (during the European debt crisis). Worse, all but one sector was in the red, with Energy the only advancer. Despite a 4.65% September loss, the S&P 500 eked out a 2% gain for the quarter, marking the sixth consecutive quarter of advances. But its 227 days without a 5% drop from the high ended on September 29—the seventh-longest such streak on record, Jacob Sonenshine of Barron’s tells us. The Dow and the Nasdaq were less fortunate, with their fivequarter winning streaks ending after respective falls of 4.2% and 5.31% in September. The Dow declined by 1.46% for the quarter, and the Nasdaq fell by 0.38%.

Historically speaking, a September decline in the S&P 500 isn’t surprising: the past 100 years have seen 89 monthly drops of more than 5%. Felice Maranz of Bloomberg notes that September and October have accounted for 12 of the 26 times the market has dropped by more than 10% in a month. Encouragingly, these 26 drops were followed by subsequent 12-month gains on 16 occasions (for an average gain of 6.8%).

Bond yields also began to increase (the 10-year Treasury went from 1.18% to 1.61% in less than 3 months), which dragged down technology shares. Higher yields on long-term risk-free investments make future profits less valuable, harming many tech company valuations, which are often based on expectations of significant profits many years down the line. Since technology companies are weighted heavily in the S&P 500 (nearly 28%, or more than 2x the weighting of the next-largest sector, Health Care, at 13.3%), the index dropped quite a bit more than the average stock did. (In September the S&P 500 index declined by 4.65%, while the S&P 500 equal-weighted index fell 3.90%.)

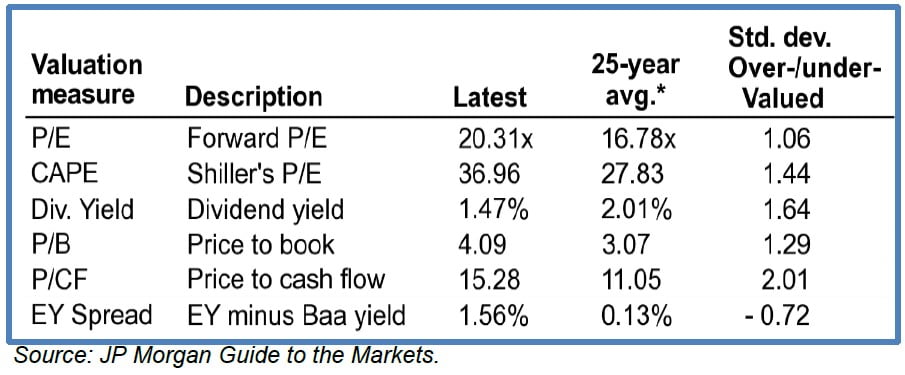

The S&P 500 finished 3Q 2021 selling for 20.3x earnings (fwd.) versus 19.2x at its February 19, 2020, pre-COVID peak and 13.3x at its March 23, 2020, pandemic low. Since the March 23 bottom, the S&P 500 has gained well over 90%. By most traditional valuation measures (price to earnings, price to book, price to free cash flow, etc.), the S&P 500 is historically overvalued.

Overvaluation against historical averages does not mean that investors should avoid equities, because extraordinarily low interest rates make prior valuation comparisons less meaningful. More important, at The Boyar Value Group, we don’t buy “the market”; rather, we purchase, and hold, businesses that sell far below our estimate of their worth. It might be especially hard uncovering bargains right now, but we’ve identified quite a few businesses selling at attractive levels even so.

None of the 11 S&P 500 GICS sectors had standout performance in 3Q 2021, with 4 in negative territory and 1 flat (Consumer Discretionary). The biggest gainer, Financials, advanced a mere 2.7%. (For comparison, last quarter’s biggest gainer, Real Estate, advanced 13.1%.) By the end of 3Q, no sector was in negative territory YTD, and the best-performing sector by far was Energy (+43.2%). However, its low weighting in the S&P 500 (2.7%) gave it little effect on the index’s return, and its fantastic rise should be viewed in context, following as it did a loss of 37.3% in 2020. Other notable gainers thus far in 2021 have been Financials (+29.1%), Real Estate (+24.4%), and Communication Services (+21.6%). Interestingly, according to JP Morgan, since the market bottomed in March 2020, the S&P 500 had advanced ~97.3% as of September 30, 2021—leaving the index “only” ~30.6% above its February 2020 peak.

The FAAMG stocks (Facebook, Apple, Amazon, Microsoft, and Alphabet—formerly Google), which have seemingly been leading the market ever upward, have struggled lately. Since their September peak, they have lost ~9%, or nearly $1 trillion, in market value. Due to FAAMG’s heavy weighting in the S&P 500 (~22%), if this area of the market continues struggling, the S&P 500 likely won’t perform well. Even so, we think there could be plenty of opportunities to make money investing in companies that have lower index weightings and/or that are outside the major indices.

Some of the biggest “pandemic winners” are struggling too, with shares in Zoom Video Communications Inc (NASDAQ:ZM), Peloton Interactive Inc (NASDAQ:PTON), and Teladoc Health Inc (NYSE:TDOC) down 24%, 43%, and 34%, respectively, in 2021. (Though it’s worth noting that each company’s share price is trading significantly higher than before the pandemic.) One pandemic standout that has continued to soar throughout 2021 is vaccine maker Moderna, whose shares are up 192% in 2021 and up over 1,000% since March 2020.

In hindsight, many signs of an imminent pullback were present. Market sentiment, for example, was very bullish (usually a contrarian indicator). At the beginning of August, two-thirds of JP Morgan clients surveyed were planning to increase their stock exposure in the coming weeks. A recent Bank of America gauge that tracks levels of optimism among market strategists was at a postcrisis high, and as of mid-August, 56% of all Wall Street analyst recommendations on S&P 500 index components were buys, the highest figure since 2002. However, we aren’t market timers. That’s because we know that trying to pinpoint the exact start of a market correction is a fool’s errand that impedes long-term results by prompting more trades (making results less tax-efficient) while removing the chance to make spectacular gains with companies that may be temporarily overvalued based on current earnings but that still have great long-term potential. When selling a high-quality company that has temporarily gotten ahead of itself in terms of valuation but that has excellent future growth prospects, knowing when to repurchase shares is extremely difficult, because the company’s share price often never drops enough to tempt investors into buying it again. So if you sell early to lock in a profit, anticipating a future correction, your profit on a well-timed sale might short-change you on future outsized gains.

Reasons for Optimism

According to Bloomberg, the final quarter of the year has been the strongest quarter for stocks since 2001, with an average increase of 4.1%. If history is any guide, 4Q 2021 could be a good quarter: 412 members of the S&P 500 are heading into it with gains for the year, the third-highest figure during the past 20 years. During that same period, each time 400 or more stocks have been positive through 3Q, the S&P 500 has produced a gain for 4Q.In another potentially bullish sign for stocks, cash holdings among S&P 500 companies hit $1.8 trillion in August 2021, as reported by Dow Jones Market Data—an increase of almost 30% from 3Q 2019. According to recent research by Goldman Sachs cited by Hardika Singh in a Wall Street Journal article, corporate America seems unlikely to be hoarding this cash, with S&P 500 companies expected to increase cash spending to $2.8 trillion in 2021 (mostly on capital expenditures, mergers, and business investment). Corporations also seem willing to buy back their own shares, having collectively authorized ~$870 billion in share repurchases thus far in 2021, $50 billion ahead of the record set in the first 9 months of 2018. If they deploy this capital wisely, share buybacks could buoy share prices in the short run, with capital investments spurring long-term earnings growth.

What Does TINA Have to Do with the Stock Market?

TINA, meaning “there is no alternative,” has become a popular catchphrase among investors, used to express the idea that stocks should continue doing well simply because interest rates are so low as to leave investors few investment options to produce an adequate rate of return. With the 10-year Treasury yielding ~1.6% and municipal bonds yielding ~1.17%, investors certainly are lacking attractive traditionally “safe” investment opportunities! Interest rates are so low that even the yields on some risky European junk bonds don’t earn any real return after factoring in inflation. Until rates rise meaningfully, equities should continue to see support—because there truly are few alternatives.

The State of Value Investing

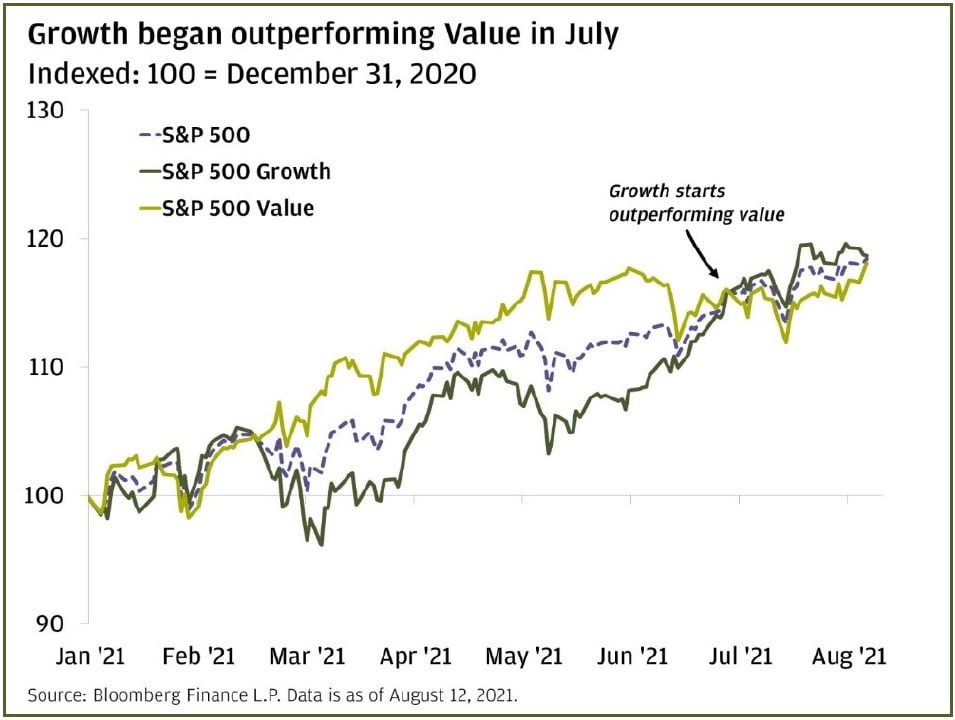

Since April 2020, the S&P 500 value index has risen a little under 60%, while the S&P 500 growth index has surged over 90%, says Jacob Sonenshine of Barron’s. Value stocks should start outperforming if history is any guide: in the first 2 years of a recovery after a recession, value has bested growth by an average of 24%, based on data from Research Affiliates.

The swift rotation back into value shares that began in September 2020 ended abruptly in July of this year as the delta variant slowed down the economic recovery, interest rates fell, and investors once again began embracing technology-oriented shares. But value looks like it might be making a comeback, with interest rates rising again and investors starting to embrace industrial and financial shares.

Market Tops

With the S&P 500 having advanced well over 80% since its March 2020 highs, and in view of all the political and economic uncertainty on the horizon, investors are questioning whether the latest bull market has ended. However, Mark Hulbert of the Wall Street Journal points out that unlike bear-market bottoms, which usually occur quickly (thankfully), bull markets end slowly, because individual sectors or investment styles peak and retreat at different times:

“A recent illustration that not all sectors and styles hit their bull-market highs at the same time came at the top of the internet-stock bubble in early 2000. Though the S&P 500 and Nasdaq Composite indexes hit their bull-market highs in March 2000, value stocks—and small-cap value stocks, in particular—kept on rising. The S&P 500 at its October 2002 bear-market low was 49% lower than its March 2000 high, and the Nasdaq Composite was 78% lower, but the average small-cap value stock was 2% higher than it was in March 2000.

Hulbert analyzed 30 bull-market tops since the mid-1920s, using data maintained by Ned Davis Research, and identified the dates when individual sectors and market styles (value, growth, blend) reached their bull-market peaks, reporting a 225-day spread between the dates when the first and last market sectors reached their bull-market tops. There are exceptions, of course, such as with bear markets caused by exogenous events such as 9/11 and the pandemic, but in general, he says, “it’s more accurate to view a bull-market top as a process rather than a single event.”

As Hulbert points out, even the so-called experts can’t determine when a market peaks. Over the past 40 years, on days when the S&P 500 reached a bull-market high, the market timers that he followed recommended equity exposure at an average of 65.7%—a higher level of recommended investment than on 95% of all other days over the period. The experts were even worse at picking bear market lows, with their average equity exposure at market lows over the same period a mere 5%—yet another example of investors buying high and selling low!

The takeaway is that knowing when a market has peaked is pretty much impossible to do regularly: even the so-called experts are consistently wrong. Individual investors would do much better to base their decisions on the value of each of their holdings rather than trying to guess whether they’re in a bull or bear market.

Speculation in the Market

The amount of speculation in the stock market worries us. A good example is the heightened use of stock options, which have legitimate hedging purposes, but which individuals seem to have recently embraced for speculative purposes. CBOE data indicate that option trading by individual investors has risen 4x over the past 5 years. As noted by Gundan Banerdi in the Wall Street Journal,

“Nine of 10 of the most-active call-options trading days in history have taken place in 2021, Cboe Global Markets data show. Almost 39 million option contracts have changed hands on an average day this year, up 31% from 2020 and the highest level since the market’s inception in 1973, according to figures from the Options Clearing Corp.”

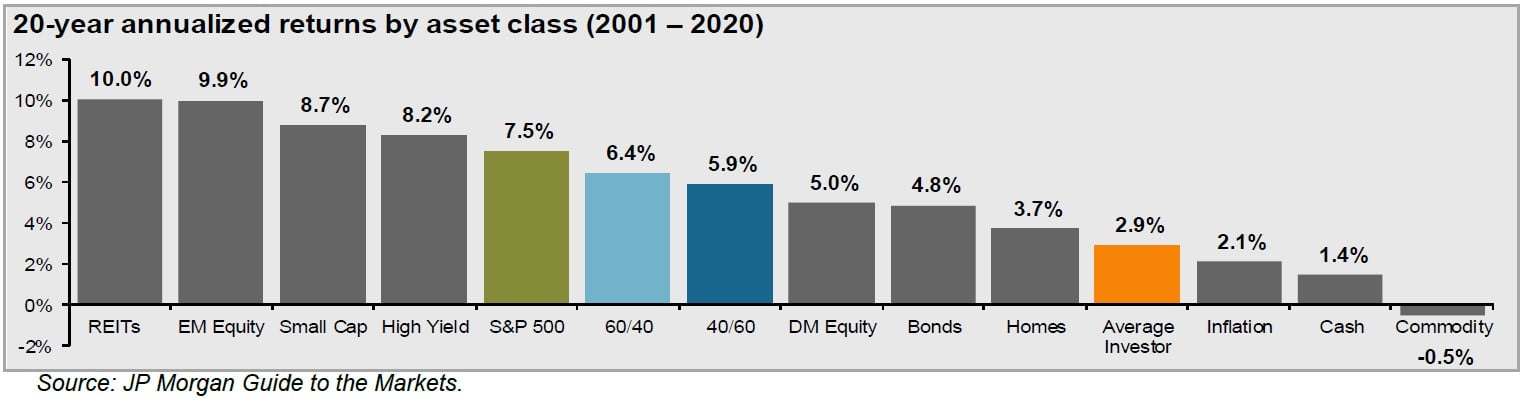

As a result, the options market has grown so large that in some respects it’s bigger than the stock market. In 2021, for example, according to CBOE data, the daily average notional value of single stock options was over $432 billion, compared with $404 billion in stocks. We’ve said it before, and we’ll say it again: staying the course and taking a long-term view is one of individual investors’ best ways of stacking the odds of investment success in their favor. According to Dalbar, over the past 20 years the S&P 500 has advanced 7.5% annually, yet the average investor has gained a mere 2.9% (barely beating the 2.1% inflation over the period). Why this underperformance? Partly because investors let their emotions get the best of them and chase the latest investment fad (or they pile into equities at market peaks and sell out at market troughs)—or sell for nonfundamental reasons, such as simply because a company’s share price (or an index) has increased in value.

By contrast, taking a multiyear view tilts the odds of success in investors’ favor. Since 1950, the range of stock market returns measured by the S&P 500 (using data supplied by JP Morgan) in any given year has been from +47% to -39%. For any given 5-year period, however, that range is +28% to -3%—and for any given 20-year period, it is +17% to +6%. In short, since 1950, there has never been a 20-year period when investors did not make at least 6% per year in the stock market. Although past performance is certainly no guarantee of future returns, history shows that the longer the time frame you give yourself, the better your chances of earning a satisfactory return.

As always, we’re available to answer any questions you might have. If you’d like to discuss these issues further, please reach out to us at [email protected] or 212-995-8300.

Best regards,

Mark A. Boyar

Jonathan I. Boyar