Stanphyl Capital commentary for the month ended September 30, 2020, discussing the decline in revenue due to the COVID-affected Q2.

Q2 2020 hedge fund letters, conferences and more

Friends and Fellow Investors:

For September 2020 the fund was up 1.0% net of all fees and expenses. By way of comparison, the S&P 500 was down 3.8% while the Russell 2000 was down 3.3%.

Growth Stocks Vs. Value Stocks

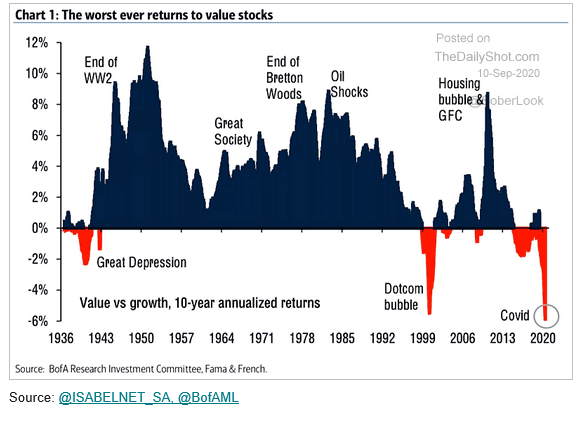

It’s been an awful last several years for the fund, as we remain “long value/short bubbles” in a market in which “bubbles” have hugely outperformed “value.” This is well illustrated in the long-term chart below, showing a record divergence in the performance of “growth stocks” vs. “value stocks”:

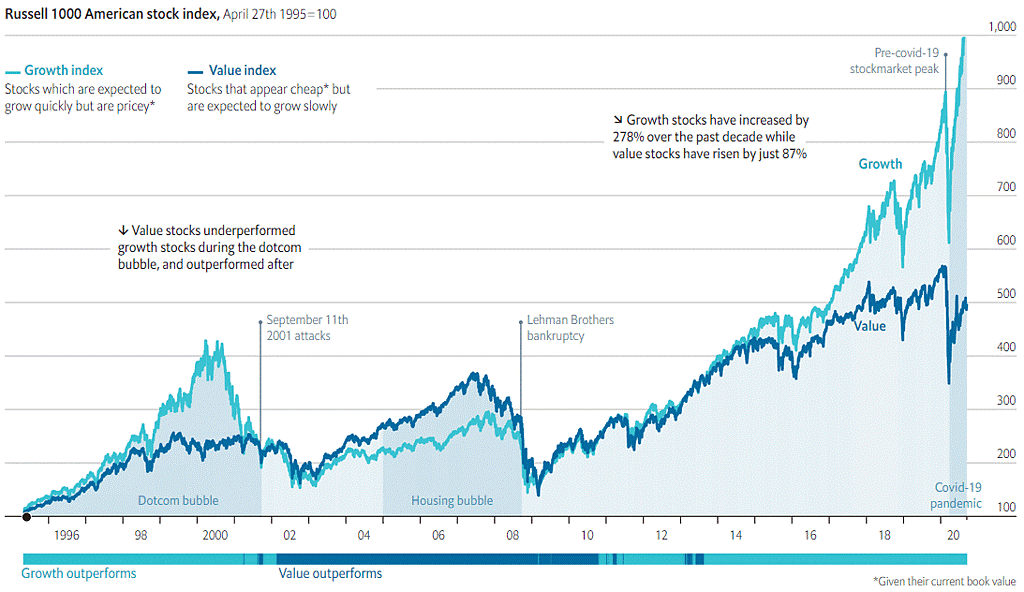

And here (from @TheEconomist) is another perspective:

Yet as has always happened in the past, I’m confident that this relationship will mean-revert in our favor:

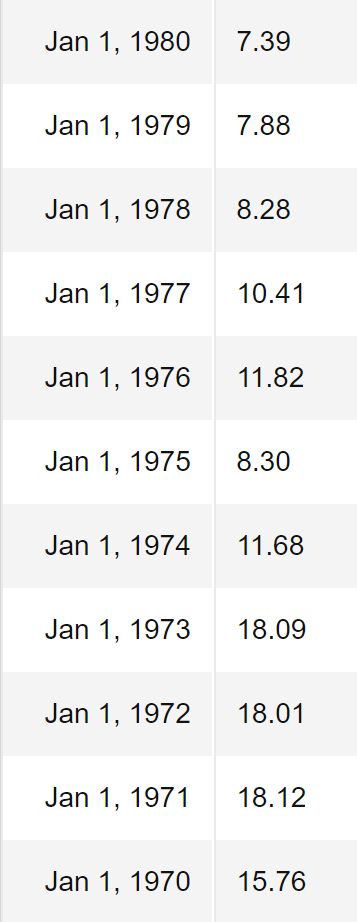

Although we may have a bit of a “disinflationary no-stimulus chasm” to cross between now and January (if Washington remains deadlocked), I believe that the Federal Reserve’s endless money-printing in support of massive deficit spending from both parties (more so from the Democrats if they win in November), along with growth-retarding levels of debt will soon return us to an environment similar to the stagflationary 1970s; i.e., slow growth and high inflation (which we got a hint of this month), and when that happens high-flying stocks (such as the NASDAQ 100 that we’re short via QQQ) will suffer massive PE multiple compression and gold (which we’re long) will do extremely well. Have a look at what happened to S&P 500 PE ratios during the decade of the 1970s, beginning in 1974 when inflation really took off:

By way of comparison, the current TTM GAAP PE ratio on both the NASDAQ 100 and S&P 500 is approximately 35.

For those who believe that a 35x PE ratio is justified because interest rates are currently so low that “there is no alternative,” I’ll point out that Japan has spent decades with similar rates while Europe has had them since the Great Financial Crisis, yet PEs in both places are far lower (currently around 16x on the MSCI Europe Index and 21x on the MSCI Japan Index), and those rates didn’t stop last March’s stock market crash in either place, nor did they stop the 2008 crash in Japan (when Europe also crashed, but under “normalized” rates). Why? Because ultimately it’s growth not interest rates that gets people to “pay up” for stocks. TINA (“There Is No Alternative”) is a stock bubble-justifying fantasy; if real-world inflation takes off there will be alternative places to invest regardless of how artificially low the Fed caps Treasury rates—real estate, floating rate private-sector lending, precious metals, commodities, etc., will all offer far better returns than “capped” (until the Fed eventually loses control) Treasury rates and high PE multiple stocks.

Portfolio Activitiy

Here then are the fund’s specific positions, beginning with the longs; please note that we may add to or reduce position sizes as stocks approach or recede from our target prices…

Aviat Networks' Revenue Down Slightly Due To COVID-Affected Q2

We continue to own Aviat Networks, Inc. (ticker: AVNW), a designer and manufacturer of point-to-point microwave systems for telecom companies, which in August reported a solid Q4 for FY 2020, with COVID-affected revenue down slightly vs. the year-ago quarter but earnings, EBITDA and backlog up substantially, with management guiding to meaningful growth on both the top and bottom lines for FY 2021 (which began this past July). In January Aviat’s board (controlled by activist investor Warren Lichtenstein) appointed a new CEO and the accompanying press release made it quite clear (based on his experience) that he was brought in to dress up the company and get it sold. Meanwhile, Aviat’s closest pure-play competitor Ceragon (CRNT) sells at an EV of approximately 0.65x revenue. If we assume $240 million in annual revenue for Aviat, $33 million of net cash and a (very conservative) $10 million valuation on a combination of $404 million of U.S. NOLs, $8 million of U.S. tax credit carryforwards, $189 million of foreign NOLs and $2.6 million of foreign tax credit carryforwards, we get a current fair market valuation of 0.65 x $240 million = $180 million + $33 million net cash + $10 million for the NOLs = $223 million divided by 5.4 million shares = $37/share.

Repurchasing Data I/O Corporation

We continue to own Data I/O Corporation (DAIO), a manufacturer of semiconductor programming devices. (Here’s the company’s investor presentation.) We previously owned this stock in 2016 when we bought it in the $2s and sold it a year later in the $4s and $5s (it eventually ran to the $16s before collapsing, as it got way ahead of itself as new holders failed to account for its cyclicality), and now we’ve repurchased it for another run. In 2019 (a year that without 2020’s COVID would have marked a cyclical low for the company) DAIO did $21.6 million in revenue with a 58% gross margin. In August it reported a COVID-affected Q2, in which it did $4.7 million in revenue (still with a 52.4% gross margin) accompanied by an $878,000 operating loss, but negative free cash flow was only $438,000 and the company ended the quarter with $13.3 million in cash and no debt, and with its increased backlog & bookings should be able to return to profitability within a couple of quarters. Using 2019’s revenue and valuing DAIO at 2x that cyclically low figure (this company is much more levered to customer technology cycles than economic cycles), then adding in $13 million of cash would make this stock worth around $6.80/share.

Amtech Systems' Revenue Also Down Due COVID-Affected Q2

We continue to own Amtech Systems, Inc. (ASYS), a manufacturer of semiconductor production and automation systems, which in August reported a breakeven Q2 that was down (revenue-wise) 28% year-over-year (due to COVID-affected Q2) and roughly flat with Q1. Disappointingly, the company guided to no revenue improvement in Q3 and a decline in earnings. Nevertheless, this is a mid-30% gross margin company that does around $80 million a year in normalized (ex-COVID) revenue with around $4 million/year in operating income (again, ex-COVID), and has around $39 million in net cash and over $80 million in NOLs. If we subtract $1 million from Amtech’s cash to account for two more quarters of “COVID hit,” then value the company at 1x normalized revenue with $8 million for the NOLs, we get fair value of around $9/share. The biggest risk here (other than underestimating “the COVID effect”) is that management—which *is* acquisitive—blows that cash pile on something stupid.

Evolving Systems Had A Solid Quarter

We continue to own Evolving Systems, Inc. (EVOL), a small telecom services marketing company that in August reported a solid Q2 (considering the COVID situation), with revenue up a tiny bit vs. both year-over-year and the previous quarter. EVOL generates over $1 million/year in free cash flow on $25 million of 65% gross margin revenue and would make a great buy for a strategic acquirer, as $1.5 million/year in savings from eliminating the C-suite and cost of being a standalone public company would mean around $2.5 million/year in free cash flow. Thus, at an acquisition price of just $2.25/share (which is nearly a 100% premium to the current price) a buyer would be paying only around 10x free cash flow and 1x revenue (inclusive of .25/share in net cash).

Reduced Position In Communications Systems

We continue to own Communications Systems, Inc. (ticker: JCS), an IOT (“Internet of Things”) and internet connectivity & services company, although I reduced the position size considerably in August when it reported Q2 revenue up a very nice 5% sequentially, but accompanied by a very ugly $1.6 million operating loss. Although this company is still cheap on an EV-to-revenue basis (it has around $2.60/share in net cash), a combination of that Q2 loss plus management’s headline in the earnings release that it’s “seeking new acquisitions” (which I read as “potentially blowing a beautiful balance sheet on something stupid”) mean that I now have a “wait and see” attitude and no longer want to carry a large position here.

Continue To Hold Gold

Finally on the long side, as central banks increase their money-printing to ever higher levels in order to fund multi-trillion-dollar annual deficits, we continue to hold a substantial long position in the gold ETF (GLD); the likelihood of negative real interest rates for years to come adds a substantial tailwind to this position.

Thanks and stay healthy,

Mark Spiegel