As Hurricane Dorian approached Florida a few weeks ago, I was having lunch with a friend who is an insurance adjuster. He explained to me that if a Category 5 hurricane hit Florida, he would be busy for over a year and could make quite a bit of money. I asked, “Are you telling me you’re rooting for Dorian to hit Florida and roll down the coastline?” He said, “Yes.” I replied, “That’s awful. You need to find a new occupation.” He responded quickly, “Look who’s talking—the guy who wants the stock market to crash!” Our exchange on hurricanes and the financial markets stuck with me throughout the day. Was rooting for a bear market the same as rooting for a hurricane to make landfall? And if so, does this make me a bad person?

Before answering the question “Are bears bad people?” I believe it’s important to clarify something: As absolute return investors, we are not always bearish nor do we particularly enjoy being bears. We’d much rather be bullish and fully invested, since such positioning would indicate opportunities are abundant and potential future returns are attractive. Unfortunately, with small cap valuations as expensive as they are today, we are not fully invested and find ourselves with little choice but to patiently wait for a more advantageous opportunity set.

Q2 hedge fund letters, conference, scoops etc

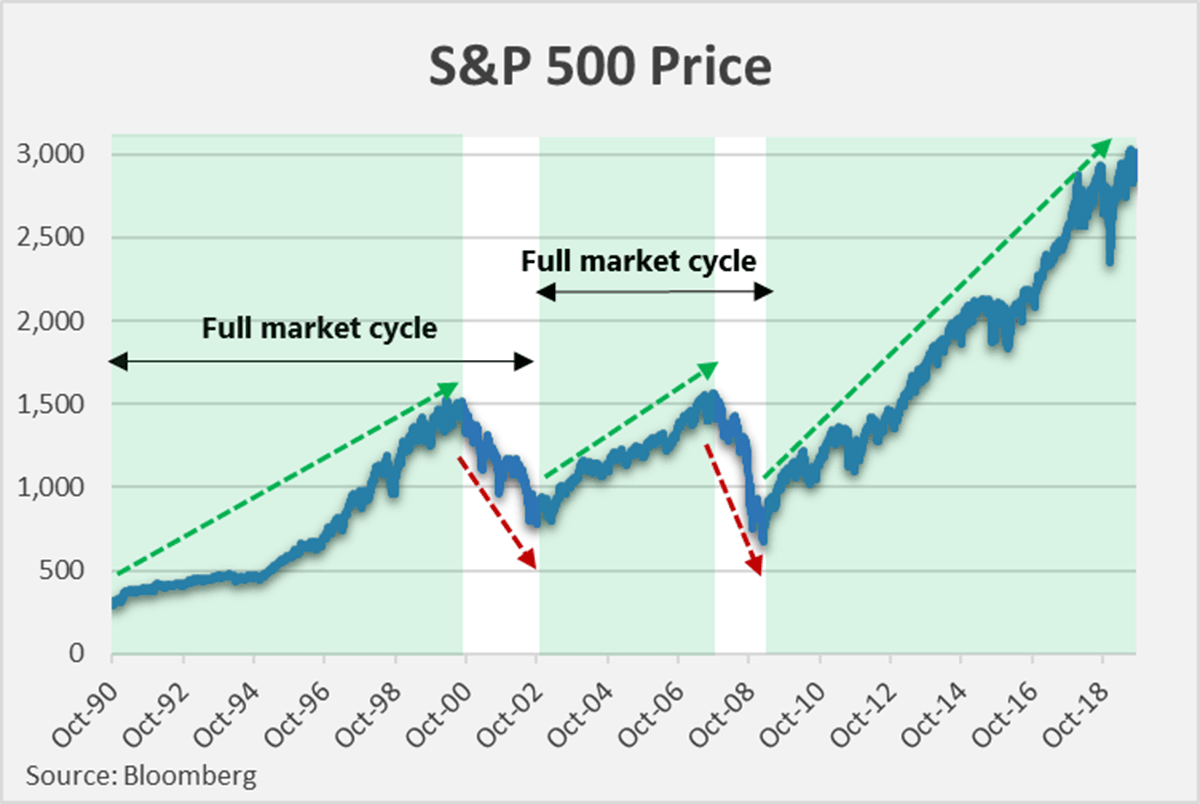

While we believe our positioning is appropriate, we do not anticipate remaining defensive indefinitely. During every market cycle, we expect there will be a time when we are being adequately compensated for risk assumed. This cycle is no exception. As the current market cycle eventually concludes, we anticipate our positioning to transition from defensive (bearish) to aggressive (bullish).

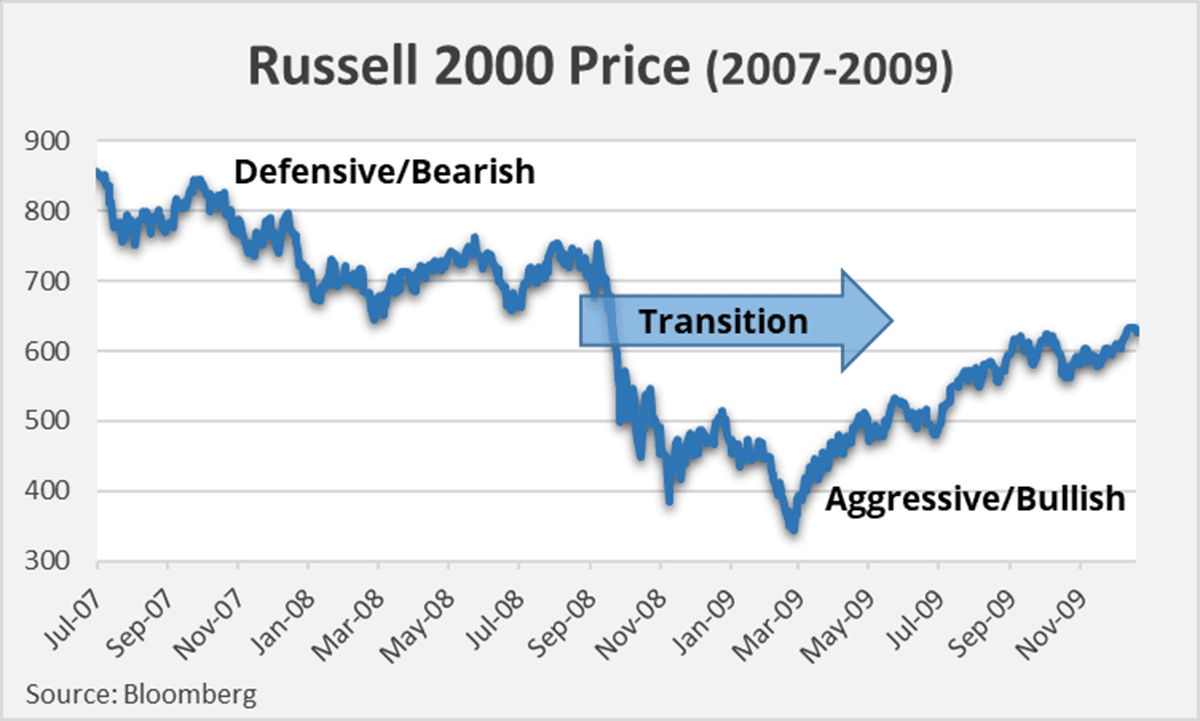

The 2008-2009 financial crisis is a good example of when it paid to transition from defensive to aggressive. Heading into the crisis, small cap valuations were near record levels and a defensive and patient mindset appeared warranted. However, once the cycle ended and small cap stocks declined sharply, opportunities blossomed. As the bids plummeted, it was a wonderful time to be liquid and have the ability to buy depressed shares. Instead of causing anxiety, the market’s sudden and violent decline was a tremendous relief for investors who were patiently waiting for better opportunity.

I remember the 2008-2009 equity market selloff well. After several years of bearishness, I was excited to be finding value again and was more than happy to reclassify myself as a bull. Although I rarely watch financial television, one of my favorite routines during the crisis was turning on CNBC after dinner and listening to Larry Kudlow talk about signs of economic green shoots. “Green shoots,” I thought, “Yeah, that’s the ticket, green shoots!” Whatever would make stocks go up was fine by me – I was running with the bulls! After several rounds of rate cuts, stimulus programs, and quantitative easing (QE), stocks eventually did go up…and went up by a lot. It was a fun time to be bullish.

In the years following the credit crisis, stock prices continued to increase and valuations became less attractive. As much as I enjoyed rooting for stocks to rise, I found myself becoming increasingly uncomfortable being a bull and ultimately transitioned back to a more defensive position, where we find ourselves today.

As of June 30, 2019, the Palm Valley Capital Fund had 92% of its assets invested in cash and Treasury bills. Given such a large position in cash, we wouldn’t argue with being characterized as bears rooting for more favorable (lower) prices. And this gets us back to the original question of this post. Does our bearish positioning and desire for lower prices make us bad people? We don’t think so. On the contrary, at this stage of the cycle, we consider our positioning as necessary, prudent, and frankly, the right thing to do.

At today’s valuations, we believe a fully invested position would require us to knowingly overpay for small cap securities. In our opinion, following our process and being disciplined does not make us bad people, but knowingly overpaying for stocks might! Fortunately, we are not required to remain fully invested and can rest easy knowing our moral compass is not being compromised by an inflexible mandate or a relative return objective.

When the current market cycle ends, we believe many investors will incur significant losses. Such potential losses would be very unfortunate, and we do not wish financial harm on anyone. However, we also respect the necessity of market cycles. Just as with the circle of life, market cycles are born, thrive, and ultimately die. During each cycle, investors are compensated and impaired, corporations are rewarded and disciplined, and policy makers are celebrated and humbled. The booms and busts of market cycles provide invaluable information and experiences that help market participants better manage future cycles. In fact, the lessons we’ve learned from past cycles have heavily influenced our investment process and current positioning.

Hurricane Dorian never made landfall in Florida. Although my friend was disappointed, he reminded me the current hurricane season is far from over. I informed him the current market cycle isn’t over either. When it ends, we expect to be as busy as he would have been if Hurricane Dorian hit Florida. Similar to a Category 5 hurricane, we believe today’s inflated equity valuations are dangerous and will ultimately be very destructive. In preparation, we plan to remain defensive and are ready to transition to a more aggressive posture at a moment’s notice. Regardless of whether our bearish stance causes us to be perceived as good or bad, we are confident in its appropriateness as it relates to our goal of generating attractive absolute returns over a full market cycle.

Index performance is not indicative of a fund’s performance. Past performance does not guarantee future results. Current performance of the Fund can be obtained by calling 904-747-2345.

There is no guarantee that a particular investment strategy will be successful. Opinions expressed are subject to change at any time, are not guaranteed, and should not be considered investment advice.

Fund holdings are subject to change and are not recommendations to buy or sell any security. Current and future portfolio holdings are subject to risk.

Definitions:

Russell 2000: The Russell 2000 Index is an American small-cap stock market index based on

the market capitalizations of the bottom 2,000 companies in the Russell 3000 Index. One cannot invest directly in an index.

S&P 500: The Standard & Poor's 500 is an American stock market index based on the market capitalizations of 500 large companies.

Article by Eric Cinnamond, Palm Valley Capital Management

{kind=link}