Activist Insight is delighted to publish M&A Activism 2019, a report providing a thorough qualitative and quantitative analysis of M&A activism and the trends that have emerged in recent years. The report also features commentary from industry experts at Skadden and MacKenzie Partners.

Forewarned on m&a activism

In the more than two years since Activist Insight’s last report on M&A activism, the landscape has changed in many significant ways, writes Activist Insight’s editor-in-chief, Josh Black.

Q2 hedge fund letters, conference, scoops etc

Take as your starting point the second half of 2018 and M&A activism has apparently swung violently from enjoyment of last year’s record M&A volumes to a trend of opposing large-cap transactions. Cigna and Dell highlighted the trend in the second half of 2018, and this year’s prime specimens – Bristol-Myers Squibb and Occidental Petroleum – provide lessons because of the lengths to which activists and traditional asset managers went in protesting them.

The emergence of traditionally silent market participants as sometimes vocal activist allies has been another key talking point in 2019. They have lent credibility to activist arguments when suspicions have been raised – sometimes without evidence – about activists’ trading activity. Thanks to the deteriorating deference paid to management teams, proxy advisers are important gatekeepers. Few deals have been troubled that were blessed by Institutional Shareholder Services and Glass Lewis, but activists have also made deep impressions with increasingly sophisticated analyses.

While opposition to M&A has indeed spiked from the U.S. to Europe, support for M&A remains a more common strategy for value creation. Some opposition to acquisitions is merely a prelude to a sales process, although a sound standalone strategy is a must-have for such campaigns to succeed.

Then there is the direct approach. Elliott Management’s expansion of its private equity arm in late 2017 fired the starting gun on a new phase of convergence, collaboration, and competition with private equity. Twelve takeover bids were made by hedge funds in the first six months of 2019, equalling 2018’s record, according to Activist Insight Online.

Overall, takeover demands are at their highest level since at least 2013, despite much higher valuations. As Skadden, a sponsor of this report, points out in an interview within these pages, private equity strategies provide flexibility for funds lucky enough to have long-term money but raise questions about their alignment with other market participants.

Indeed, as noted by our other sponsor, MacKenzie Partners, the flexibility of M&A activism – its ability to shift between different types of demands, taking different sides of deals – is a reason why it can flourish at any point in the economic cycle. M&A activism may need M&A but doesn’t need much else to thrive.

We have divided this report up into thematic sections, highlighting new developments as well as lessons in how to defend against M&A activism. We hope its findings, including data on the many strands of this complicated strategy, are helpful to practitioners on all sides.

Our thanks go in particular to our sponsors, Skadden and MacKenzie, but also to all those who agreed to be interviewed over a summer in which there were distinctly few breaks from M&A activism.

Rapid growth in the number of investment banks offering corporate defense services to companies speaks to how intertwined the worlds of activism and M&A have become. The fact that a select number of investment bankers have moved the other way, most recently with Goldman Sachs’ Steven Barg joining Elliott, merely reinforces that point.

This is likely the first special report in a bumper few months for Activist Insight and we are planning an expanded roster for 2020. If you would like to suggest a topic or participate in a future publication, please do get in touch.

Note: Data throughout this report is as of June 30, 2019, although anecdotes and interviews may have taken place later.

Stop that deal

With M&A activity on the rise, activists are not only hunting for the proverbial price bump but also opposing deals on strategic grounds, writes Iuri Struta.

When Starboard Value invested in Bristol-Myers Squibb with the stated intent of blocking the latter’s takeover of Celgene, it seemed like a manifestation of activists' growing desire to shape the U.S. corporate landscape. The hedge fund’s subsequent failure to do so showed their limitations.

In that respect, Starboard is by no means alone. Later in 2019, both Pershing Square Capital Management and Third Point Partners expressed opposition to United Technologies’ plans to acquire Raytheon with stock, although the former exited in protest. Carl Icahn unsuccessfully campaigned against Occidental’s buyout of Anadarko Petroleum and is now pursuing board seats.

One of the reasons activists have struggled may be that, with the growth of passive investing, deals are evaluated as a whole, rather than from only one side of a transaction. “It's important when looking at a deal to understand the economic crossownership at the fund level," says Pete Michelsen, head of activism and shareholder advisory for the Americas at Goldman Sachs. "An investor that may be on the fence on the buyside could be receiving a premium on the seller's side.”

Advisers interviewed for this report said activists’ track record in stopping deals counts for little, given the specificity of each situation. “Activists tend to be a pretty confident bunch and I suspect most of them think that they would have different success in other campaigns,” David Rosewater, global head of activism defense at Morgan Stanley, told Activist Insight.

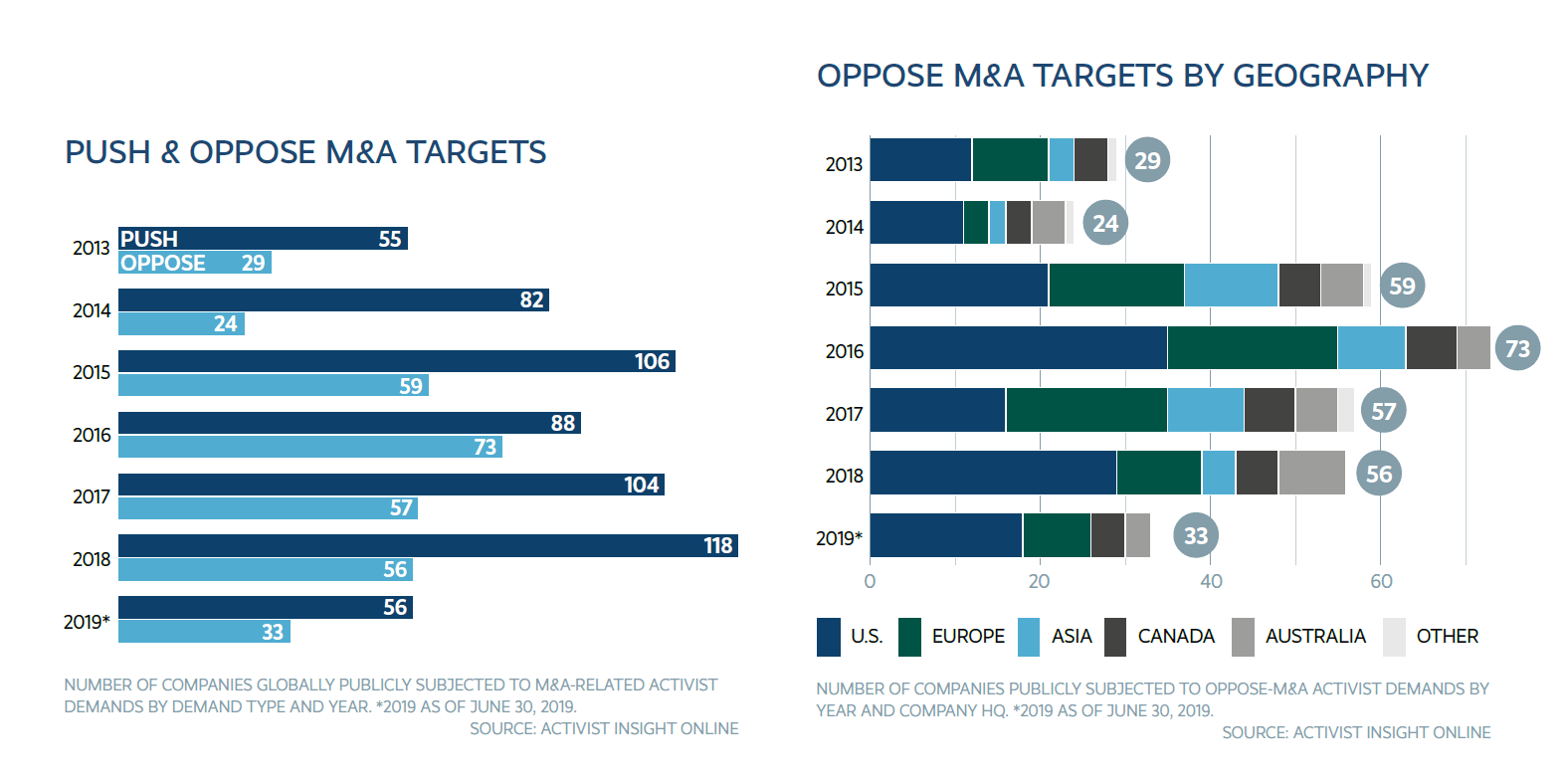

Indeed, 18 U.S. companies have seen their deals opposed in 2019 so far, the highest number in the opening six months of the year since at least 2013. Europe, a historically fertile ground for bumpitrage campaigns, experienced a resurgence of these kinds of demands, with eight companies targeted in the first half of 2019 – already close to the 10 registered in the entire of 2018. In 2019, globally, 33 deals were opposed, nearing the record of 35 reached in the same period of 2016, although opposition to deals was lower in Asia, and Japan than recently (see charts overleaf).

Questioning the bidder

While in Europe most of the activity centered around squeezing out higher prices from the bidder, the U.S. increasingly saw activists questioning the strategic rationale of the acquirer.

A favorable environment marked by falling interest rates, high equity valuations and plentiful cash from U.S. tax reforms has created opportunities for companies to boost earnings growth through mergers. Averse to empire-building and keen on more focused companies, shareholders have started to rebel.

At the same time, deals are increasingly questioned not only by dedicated activists but by traditional investors, part of a broad trend of institutional investors becoming more vocal with their shareholdings. So far this year, five companies have seen opposition from institutional investors that do not typically engage in activism.

“You can’t ignore any of your top shareholders anymore. It’s not just waiting for an Icahn,” Christopher Ludwig, head of shareholder advisory and M&A at Credit Suisse, told Activist Insight.

You see a convergence of the trends on opposing M&A and typical institutional investors who don't use activism coming out more regularly," Rosewater agreed. Wellington Management backed Starboard in its opposition to Bristol-Myers’ deal, while the tie-up between Occidental and Anadarko stirred the public anger of T. Rowe Price. In Europe, Fidelity International and Legal and General joined activist Odey Asset Management in demanding a higher price for their shares in Acacia Mining.

Mixed record on m&a activism

Of the 54 U.S. cash-only deals that have seen opposition since 2013, over half proceeded unamended and 19% were canceled, according to Activist Insight Online data. In Europe, 29% of the 34 cash-only deals opposed by activists since 2013 completed in their original form, with the rest either abandoned or changed and in part, that may be because minority shareholders are afforded more protections in Europe.

In the U.S., not all acquirers provide a shareholder vote, as in Occidental’s purchase of Anadarko. Moreover, pressure is higher on the activists to show there are better options when they try to scuttle a deal than when they ask for a price increase for the buyout target. For one thing, it is more difficult to convince proxy advisers Institutional Shareholder Services and Glass Lewis, particularly if there is no clear affront to corporate governance best practices.

“The problem of when you are attacking an acquirer is that the campaign is certainly more amorphous. Even though the math may be black and white on a spreadsheet, it’s harder to translate

that into an effective campaign,” Darren Novak, global head of activist defense at UBS, said in an interview for this report.

Activists have tried to resolve the problem of upside visibility by promising a sale, with mixed success. Icahn, for instance, successfully stopped Xerox and SandRidge Energy completing their respective deals with Fujifilm and Bonanza Creek Energy in mid-2018, while Corvex Management and 40 North blocked Clariant’s takeover of U.S. peer Huntsman. All three campaigns had unique circumstances that helped the activists win, but each promised to ultimately sell the company and failed.

M&A activism in numbers

Read the full report here by Activist Insight