Pershing Square Holdings commentary for the third quarter ended September 30, 2018.

Dear Shareholder:

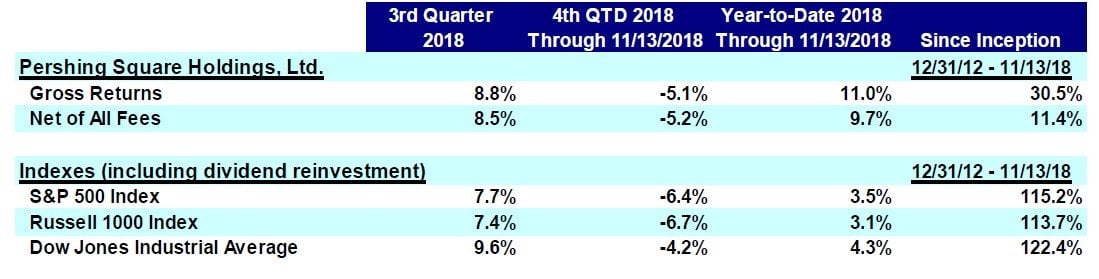

The performance of the Pershing Square Holdings, Ltd. is set forth below:

Pershing Square Holdings has continued to make significant progress in the year to date. NAV per share has increased by 9.7%, compared with the S&P 500’s year-to-date performance of 3.5%. This outperformance has been driven primarily by our investments in ADP, Lowe’s, Starbucks, and Chipotle, which we describe in detail below.

Q3 hedge fund letters, conference, scoops etc

During the third quarter, we exited our investment in Mondelez and acquired a substantial position in Starbucks Corporation. We presented our investment case on Starbucks at the Grant’s Conference on October 9th, 2 in which we described the company’s highly attractive brand, market position, and economic model, and enumerated steps that management has taken to address the recent deterioration in same-store sales growth. To date, Starbucks shares have appreciated 32% including dividends versus our average cost at announcement of $51 per share. The company’s quarterly earnings and same-store sales results reported on November 1st were above expectations and provided evidence that the business is making positive progress.

PSH’s NAV declined during October due to the general stock market decline, but has rebounded due to strong earnings reports from all of our portfolio companies that have reported. While we seek to identify businesses that can withstand difficult macro environments, none of our investments’ stock prices is immune to sharp stock market declines. Fortunately, however, most of our portfolio companies – including ADP, Starbucks, Hilton, Restaurant Brands, Lowe’s and Chipotle – are buyers of their own shares. Pershing Square Holdings will be a long-term beneficiary of shares purchased at even deeper discounts to intrinsic value which occur during market breaks. Furthermore, market downturns create attractive entry points for new investments for Pershing Square Holdings. To that end, in October, we acquired a large stake in Hilton.

We first invested in Hilton in the third quarter of 2016, but due to the stock’s rapid rise during our initial accumulation period, we were not able to build a sufficiently large stake. We exited the position a year later to allocate capital to other opportunities. Hilton’s intrinsic value has continued to increase since the sale of our investment due to increased free cash flow and share repurchases which have led to a substantial reduction in shares outstanding over the last year. As a result, at our recent entry price, we have reacquired Hilton at a substantially lower valuation than when we exited more than a year ago.

On October 26, 2018, Pershing Square Holdings announced that PSH Board Member Nick Botta and I bought an additional $116 million of PSH shares, bringing total purchases of PSH stock by insiders to more than $520 million since May 29, 2018. Inclusive of these purchases and assuming the conversion of all PSH Management Shares to PSH Public Shares, Pershing Square affiliates and I would own a total of approximately 44.2 million PSH Public Shares or 20.0% of PSH on a fully diluted basis. We believe that this investment represents one of the largest purchases by a management team of a FTSE 250 company, and demonstrates our belief in the undervaluation of PSH and its long-term potential. Our purchases along with the company’s self-tender for 9.5% of shares outstanding earlier this year reduced the public float of PSH, and should help lead to a reduction in the discount to NAV at which PSH shares trade. We continue to believe that the most effective action we can take to close the discount is to continue to deliver improved investment performance.

Third Quarter and Year-to-Date Performance Attribution

Investments that contributed or detracted at least 50 basis points to gross performance for the quarter and year-to-date are outlined below1,3:

New Positions

Starbucks Corporation (SBUX)

On October 9th, we gave a presentation at the Grant’s Interest Rate Observer conference detailing our new investment in Starbucks which we purchased at an average price of $51 per share. Starbucks has built the world’s most valuable specialty coffee brand by first creating the category in the U.S., and then expanding globally. The Starbucks brand is synonymous with premium products and a high-end experience for both customers and employees (whom the company refers to, and treats, as “partners”). Starbucks is the dominant player in specialist coffee shops globally with a leading omnichannel presence in North America and significant opportunity for growth overseas. Starbucks operates and licenses over 29,000 stores that generate $35 billion in annual systemwide sales, with a roughly even mix of U.S. and international locations as well as owned and licensed units.

The specialty coffee category is secularly growing and attractive. It has a loyal customer base with a daily or greater consumption habit and trade-up potential, and a product that is well-aligned with health and wellness and sustainability priorities, which are increasingly important to consumers. Starbucks is the category killer with a wide competitive moat, underpinned by quality and innovation advantages over low-cost coffee and quick service restaurant (QSR) players, with convenience, technological, and cost advantages compared with higher-end, boutique coffee shops.

New Starbucks stores have industry-leading unit economics, which we estimate generate a pretax return on investment of ~65% in the U.S. and ~85% in China in their first full year of operations. Starbucks is one of the rare mega-cap businesses with a long runway for reinvesting free cash flow at exceptionally high rates of return, as we estimate that every dollar the company spends on building a new store in one of its major markets is worth $10 to $15 after the store opens. We believe that the company should continue to grow its global store count at a high-single-digit rate for the foreseeable future driven by underpenetrated markets such as China where per capita coffee consumption is less than 1% of U.S. levels.

Starbucks has a phenomenal long-term track record with average annual same-store sales growth of 5% both in the U.S. and globally, unit growth in the high-single-digits, and annualized total shareholder returns over the last ten years of greater than 30%, more than double the S&P 500. The stock was down modestly over the three years prior to our investment despite EPS growth over that time of roughly 50%, allowing us to build our position at a ~25% discount to the company’s historical average valuation multiple of ~26 times forward earnings. We believe that the reduced valuation was driven by concerns regarding a slowdown in U.S. same-store sales, lower long-term financial growth targets, and uncertainty due to the company’s senior leadership transition and management turnover.

The company demonstrated strong progress in addressing each of these concerns when it reported fourth quarter and fiscal 2018 earnings on November 1st. U.S. same-store sales grew 4% in the fourth quarter, the best result in the last five quarters, driven by a resurgence in Starbucks’ core beverage category which contributed 75% of that growth. Several initiatives are underway to improve throughput and enhance the customer and partner experience, including the redeployment of several hours per day from in-store administrative work to customer-facing activity, and new features that continue to expand the reach of the company’s best-in-class digital and loyalty platform. The company is also driving beverage innovation, particularly in healthier offerings such as Nitro Cold Brew, which is now available in only one-third of Starbucks’ U.S. company-operated stores, that aim to offset declining sales of Frappuccino and other more indulgent products. Management guidance for fiscal 2019 projects same-store sales growth at the low end of its current long-term range of 3% to 5%, as well as underlying growth in organic revenue and EPS that is well within the company’s long-term targets of high-single-digit and at greater than 12% growth, respectively.

This past quarter was the first in which CEO Kevin Johnson, who assumed the role in April 2017, led the company without the active involvement of founder Howard Schultz, who stepped down as Executive Chairman in June of this year. We are impressed by the bold actions that Mr. Johnson and his team have taken to date to simplify the business in order to drive accelerated growth and shareholder returns. Over the last year or so, the company has sold its consumer packaged goods (CPG) and foodservice business to Nestle in exchange for an upfront cash payment and an ongoing sales royalty, divested the Tazo tea brand to Unilever, closed underperforming Teavana retail stores, and optimized its mix of company-operated and licensed locations. These actions should allow Starbucks management to focus on its targeted longterm growth markets of the U.S. and China, which now account for approximately 80% of earnings, while creating a global expansion opportunity for Starbucks-branded CPG and foodservice products, heretofore distributed mainly in North America, through their alliance with Nestle, the global leader in these channels. Management is reducing overhead expenses as a percentage of systemwide sales by ~22% net of reinvestment over the next three years, with the goal of increasing the pace of innovation through faster decision making. Management is acutely aware of the stock’s undervaluation and has implemented a large three-year share buyback program of nearly $20 billion, shrinking the share count by 7% this past fiscal year and a further ~13% over the next two years.

We are pleased with the stock’s increase of 32% versus our average cost and continue to believe that Starbucks remains undervalued, and should generate highly attractive returns from current levels over the next several years. We look forward to the company’s biennial investor day in New York in December.

Hilton Worldwide Holdings Inc. (HLT)

We re-established a new substantially larger investment in Hilton during the recent market selloff as a significant decline in the company’s share price provided us with an opportunity to once again own Hilton at an attractive price. Hilton is a high-quality, asset-light, high-margin business with significant growth potential led by a superb management team. The company primarily franchises and manages hotel properties under more than a dozen hotel brands, including Hilton, Hampton, DoubleTree, and Hilton Garden Inn.

Hilton’s extensive and growing network of brands and properties offers a significant and self-reinforcing value proposition to both guests and hotel owners, which creates a strong competitive moat around the business. For guests, Hilton provides a consistent and reliable experience in a large variety of destinations at divergent price points, as well as an attractive loyalty program with enhanced customer service, amenities, and awards. For hotel owners, Hilton provides access to its more than 80 million loyalty program members, large-scale marketing programs, reservation and IT systems, as well as supply chain purchasing power.

We previously exited our position during the summer of 2017 to allocate capital to other investment opportunities after the shares’ substantial appreciation. Since then, Hilton has grown its free cash flow per share by more than 30% due to a combination of strong RevPAR growth (a measure of same-store sales for the lodging industry) and net unit growth, margin expansion, a lower tax rate due to U.S. tax reform, and significant share repurchases. Despite its meaningfully positive business progress and earnings growth, Hilton’s share price is only modestly above the price at which we sold it nearly a year and a half ago – while its valuation, due to increased free cash flow and reduced shares outstanding – is now 25% lower than before. We attribute the recent decline in Hilton’s share price to investor concerns regarding a potential downturn in the lodging cycle and broader worries about the impact of a potential economic slowdown on Hilton’s business.

While future RevPAR growth may decelerate from the 3% average achieved over the last couple of years, we believe RevPAR growth will remain positive. Moreover, our study of prior lodging cycles suggests that even if RevPAR declines in a recession, it is likely to recover quickly as the economy turns. Unlike a typical hotel owner, Hilton’s high-margin, fee-based business model insulates the company from an outsized negative impact on profitability due to a slowdown or decline in RevPAR. In addition, the embedded growth in Hilton’s industry-leading pipeline of hotel rooms should allow the company to maintain its current 6% to 7% annual growth in room count and drive earnings growth even if RevPAR slows or declines. Hilton’s pipeline, more than half of which is under construction, currently amounts to more than 40% of Hilton’s existing hotel rooms. We believe that Hilton can maintain its current pace of unit growth over the longer term as the company expands its international footprint with its existing brands, continues to create new brands, and converts unbranded hotels to Hilton’s network of brands. At the current share price, Hilton is trading at only 20 times our estimate of next year’s free cash flow. This is one of the lowest valuations at which Hilton has traded since the spinoff of its owned hotels and timeshare business at the beginning of 2017, significantly below our estimate of the company’s intrinsic value based upon its high-quality, fee-based business model and strong future growth potential.

Portfolio Update

Automatic Data Processing, Inc. (ADP)

ADP’s total return was 13% during the third quarter, including dividends, as the market positively responded to ADP’s June analyst day and fiscal 2019 guidance. We concluded our ADP proxy campaign just over a year ago and believe that the company’s progress following the campaign indicates that ADP is in the early innings of a long-term transformation. At the end of October, ADP reported fiscal first quarter 2019 results and positively updated its FY 2019 guidance. Fiscal first quarter results provided an early validation of the transformation underway at ADP as organic revenue growth accelerated and margins increased at Employer Services following actions taken by management earlier this calendar year. We are also encouraged that management noted on its first quarter earnings call that it is embracing ADP’s “transformation from a service company supported by technology to a technology company that offers great service” [Emphasis added].4

In response to the better-than-anticipated first quarter performance, ADP updated FY 2019 Adjusted EPS to $5.20 to $5.30 per share. At present, ADP trades at ~25 times our estimate of ADP’s next-twelvemonth of earnings, which continue to significantly understate the company’s earnings power if operated optimally. As discussed previously in our June 20th investor letter, we believe there is clear line of sight for ADP to achieve more than $7 of EPS by FY 2021 (which begins less than 20 months from now on July 1, 2020) and for future accelerated progress thereafter. We anticipate further share price appreciation from current levels as ADP’s business transformation takes hold. Furthermore, we believe ADP’s UScentric business model (~85% of profits are generated in the United States) – which benefits from rising interest rates due to the large amount of float it receives from its clients and unleveraged balance sheet – should enable the company to perform well in the current market environment.

Despite some recent volatility which saw ADP shares modestly retreat in the month of October amidst the broader market decline, ADP shares have appreciated 25% year-to-date. We believe there continue to be a number of catalysts for short and long-term value creation at the company. Notably, investors continue to await further clarity on who will become ADP’s new CFO. We believe that the hiring of a new CFO with technology experience and operational expertise in executing business transformations would be well received by shareholders.

Restaurant Brands International Inc. (QSR)

QSR’s total shareholder return declined 1% during the third quarter and by 7% year to date. Despite the stock’s performance, overall results remain strong, as free cash flow per share growth has increased more than 30% this year due to a combination of positive same-store stores growth, strong net unit growth and a substantial benefit from last year’s refinancing of high-cost preferred stock. We attribute the weakness in the company’s share price to investor concerns regarding the ongoing slowdown in same-store sales at Tim Hortons, which were flat in 2017 and have not yet shown a meaningful improvement in 2018. We remain confident that QSR can return Tim Hortons to a healthy level of same-store sales growth over time. Earlier this year, QSR replaced the prior management at Tim Hortons with the same team that had previously improved same-store sales results at Burger King several years ago. The company also announced a new operational plan, entitled “Winning Together,” which incorporates a variety of initiatives including menu innovation, enhanced marketing, store re-imaging, and investments in digital technology. While Tim Hortons’ management has just started to implement some of these new initiatives, same-store sales growth this quarter improved from the first two quarters of this year. We expect continued improvement as the new management team implements more of the recently announced initiatives.

While the market is focused on near-term same-store sales results at Tim Hortons (to an excessive extent in our view), we believe it is overlooking the sizeable long-term unit growth opportunity at each of QSR’s brands:

- Burger King’s fast growing international business is still much smaller than competitor McDonald’s, which has more than three times the numbers of international stores.

- Tim Hortons’ U.S. business is a fraction of the size of Dunkin’s, which has almost ten times the number of U.S. stores. In addition, Tim Hortons is beginning to expand internationally, including a recent franchise agreement to add 1,500 stores in China (~30% of the current store count), which we believe highlights the power of the brand’s overseas potential.

- Popeyes has a small store count compared to KFC, which has close to eight times the number of total stores.

Moreover, QSR’s deep network of global franchisee partners who have successfully opened stores under one of the company’s brands provides an advantage in accelerating unit growth for other brands in QSR’s portfolio. The company’s ability to continue to close the current store count gap with each of its brand’s closest peers should allow it to maintain its current 6% net unit growth rate for many years to come. We believe that QSR’s unit-growth potential underpins a long-term earnings growth rate in the mid-teens, and should allow the company to maintain strong earnings growth even during a period of weaker same-store sales results.

Despite the high-quality nature of QSR’s capital-light business model and its significant long-term growth potential, the company’s shares trade at only 19 times our estimate of next year’s free cash flow per share. The current multiple is one of the lowest since our initial investment in the company and is significantly below that of its capital-light peers, such as McDonald’s, Yum! and Dunkin, which have lower unit growth potential and trade at an average of 24 times analyst estimates of next year’s free cash flow per share. As QSR continues to make progress on same-store sales growth at Tim Hortons and maintains its high level of unit growth, we believe the company’s share price will appreciate significantly from current levels. Management appears to share our view of the company’s undervaluation as the company recently repurchased $560 million of common stock.

Lowe’s Companies, Inc. (LOW)

Lowe’s shares appreciated 21% during the third quarter as investors responded enthusiastically to new CEO Marvin Ellison’s initial commentary regarding Lowe’s significant long-term potential. On his first earnings call, Mr. Ellison provided detailed examples that highlighted the opportunities for improvement and outlined a list of short and long-term initiatives to enhance the company’s operational performance. Since then, Mr. Ellison has completed the hiring of his executive team and announced the closure of 50 underperforming stores (~2% of total stores). We expect the company to provide additional detail on its long-term strategic plans and financial targets at the upcoming analyst day in December. Based on Mr. Ellison’s public commentary and initial actions, we have increased confidence that Lowe’s can meaningfully narrow the performance gap with Home Depot over time.

Since the end of the quarter, Lowe’s share price has declined 16% as investors have become concerned about the housing cycle based upon weaker trends in recent housing statistics and broader worries about a potential economic slowdown and rising interest rates. We believe the market’s response is an overreaction as there is likely further upside to the housing cycle as many of the fundamental drivers of the housing market remain well below their long-term average levels. In addition, Lowe’s derives a meaningful portion of its revenue from less-cyclical repair and maintenance spend which should moderate the impact of fluctuations in the housing cycle. Most importantly, we believe that successful execution of the significant opportunity for operational improvement at the company will allow Lowe’s to generate strong earnings growth over the next several years, even if the housing market and economy soften. Lowe’s currently trades at 17 times analyst estimates of next year’s earnings, which do not yet reflect the operational improvements that we expect Mr. Ellison to achieve over the next several years. We believe there is substantial upside potential if the company can narrow the performance gap with Home Depot, which will significantly increase earnings and likely result in a valuation that better reflects the company’s underlying business quality and growth prospects.

Chipotle Mexican Grill, Inc. (CMG)

Chipotle shares rose 5% in the third quarter. The company held its third quarter earnings call on October 25th during which management described improving momentum in the business over the last few months and outlined a robust pipeline of initiatives to reignite transaction growth. Same-store sales increased 4.4% in the third quarter, comprised of a 5.5% increase in average check and a 1.1% decline in transactions. After slowing from mid-single-digit growth in July and August to low-single-digit growth in September, same-store sales reaccelerated to 4% growth in the first few weeks of October following the launch of the company’s new marketing campaign, which includes both national TV advertising and social media. The success of this campaign stands in contrast to a series of ineffective marketing efforts last year, and bodes well for new management’s ability to drive transaction growth with the right content in the right channels in the years to come. Digital sales grew 48% in the quarter, an acceleration from the first half of the year, with particularly strong momentum in delivery.

Since CEO Brian Niccol joined Chipotle in March, he and the rest of the management team have made significant progress in restructuring the organization, rebuilding the culture, and ensuring that the company has the right people, strategy, and initiatives in place to execute with excellence and drive sustainable long-term growth. Initiatives currently in their early stages that should drive growth in 2019 and thereafter include Chipotle’s first-ever ongoing loyalty program, slated for a national launch sometime next year, in-store pickup shelves and drive-up windows for guests to pick up digital orders, a multi-pronged effort to increase throughput back towards peak levels, and potential new menu items.

Although the stock is up 68% year-to-date, it is worth noting that Chipotle shares were trading near current levels as recently as June 2017, despite progress made by Brian Niccol, the additional investment of over $300 million of capital expenditures to build 124 net new stores and significantly upgrade the company’s digital capabilities, and the enactment of corporate tax reform which has increased the value of every pretax dollar the company earns by more than 15%. As management indicated on the third quarter call, if Chipotle can grow average annual sales per restaurant to $2.2 million from just under $2.0 million today – still well below peak levels of $2.5 million which were achieved in 2015 – restaurant margins would expand to approximately 22% from just over 18% in the last twelve months (LTM). For illustrative purposes, assuming overhead and depreciation expenses in-line with LTM levels and a tax rate of 29%, earnings per share would be approximately $17, more than double LTM levels and ~10% above peak levels in 2015, when the stock traded for more than $750 per share. This reflects no benefit from building new stores, which continue to generate high rates of return on capital, supporting management’s plan for ~6% growth in the store count next year alone.

The Howard Hughes Corporation (HHC)

HHC’s share price decreased 6% during the third quarter, and has declined nearly 17% year-to-date. We believe this underperformance is due to investor concern regarding a potential housing slowdown as higher interest rates and increasing labor and material costs make homes less affordable. Homebuilders, which purchase land and manufacture and sell homes to generate cash flow, have been particularly impacted with many home builder stocks down 30% or more this year.

By comparison, however, HHC’s business fundamentals, performance and execution tell a much different story. In its master planned communities (MPCs), HHC recorded its highest ever residential land sales in the third quarter with no signs of a housing slowdown. HHC owns some of the most desirable and well-located MPCs in the country which benefit from in-migration to Las Vegas and Houston as those markets have no state income tax. Furthermore, HHC controls the supply and distribution of its MPC land (while generating 75% to 99% cash margins on its land sales), so it can be patient to protect the long-term value of its MPCs if it experiences a future slow-down in sales activity. While time is not the friend of the homebuilder to the extent new-built homes remain unsold, time is the friend of the MPC owner of well-located land which benefits from long-term land price appreciation due to population growth and inflation.

A growing percentage of HHC’s value and cash flow are now being generated from stable and recurring real estate cash flows (net operating income or NOI) from its Operating Asset segment. Since going public eight years ago, HHC has grown its Operating Asset NOI from $49 million to a current run rate of $184 million with an NOI target of $318 million upon stabilization (excluding the Seaport) making its Operating Asset segment a much larger contributor to its overall enterprise value. The growth of HHC’s Operating Asset segment further differentiates HHC from the homebuilding sector.

HHC also continues to make meaningful progress at its important Ward Village and Seaport assets. In the 60-acre waterfront Ward Village, Honolulu community, HHC just broke ground on its fifth condo tower (A’ali’i). HHC began public sales on this condo tower in January and is already 77% pre-sold as of the end of October, highlighting the significant demand for its Ward Village condo product. At the Seaport, HHC recently signed a 23,000 sq. ft. lease with Nike for creative office space, and has experienced significant demand for the balance of the office space. 10 Corso Como (29,000 sq. ft.) an iconic Milan-based fashion and design retailer opened at the Seaport in September to considerable acclaim and customer response. HHC welcomed more than five million visitors to the Seaport during the summer despite ongoing construction. HHC is positioning the Seaport for long-term success by carefully cultivating and attracting world-class tenants and partners.

We recently sold a block of HHC shares for portfolio management purposes as the size of our HHC investment had become disproportionately large in the private Pershing Square funds. Senior management acquired $6 million of shares from our block sale. The Pershing Square private funds’ sale of HHC shares replaces its previously announced 10b5-1 sale program. Pershing Square Holdings maintains a large, long-term investment in HHC held through total return swaps which create the same economic exposure as ownership of the common stock. We consider today’s current share price, which was first achieved more than five years ago, to be particularly attractive in light of HHC’s substantial continued business progress.

United Technologies Corporation (UTX)

United Technologies stock price increased 12% in the third quarter as shareholders expected the Rockwell Collins acquisition to close by quarter end. The stock declined 8% since then largely due to concern about a delay in the closing and uncertainty about economic growth and the impact on the company’s businesses from a potential trade war with China. While some of UTX’s businesses exhibit economic cyclicality, a large portion of its portfolio, particularly the aerospace and Otis Elevator service businesses, are relatively insulated from macro shocks due to strong order books, multiyear backlogs, and the long-term nature of proprietary service contracts. The Rockwell Collins acquisition is still awaiting approval from the Chinese regulator. UTX recently stated that it expects to receive approval and close the transaction in the next several weeks.

UTX has continued studying a business separation, and has committed to announcing a decision as soon as the company closes the Rockwell deal. Based on management’s recent comments, we believe that the company has all but confirmed that it will execute a breakup for which shareholders are highly supportive, particularly in light of GE’s recent woes. While management initially pointed to dis-synergies and one-time separation costs as potential issues, it has recently stated that it believes these costs are manageable and not material in the context of the overall value creation potential of a separation. UTX recently expanded its board and appointed two veteran CEOs who guided their companies through businesses separations.

UTX currently trades at approximately 15 times our estimate of next year’s earnings (pro forma for the Rockwell Collins acquisition), which is significantly below our estimate of the company’s underlying value. We continue to believe that a separation of the company will accelerate shareholder value realization and will serve as a catalyst for investors who will be able to value each of UTX’s businesses separately.

Platform Specialty Products Corporation (PAH)

Platform’s shares increased 8% during the quarter, but are still well below the highs reached earlier this summer shortly after the company announced an agreement to sell its agricultural business to a strategic acquirer in an all-cash transaction. While management has recently reaffirmed that they remain on track to close the sale at, or shortly after, the end of the year, we believe that investors are not yet valuing Platform’s shares based upon the future earnings potential of its remaining business, Performance Solutions. We believe that few investors today are willing to consider an investment in Platform until the sale transaction closes, and the company pays down debt.

Performance Solutions is a high-quality business with a strong competitive position in secularly growing end markets which will operate with significantly less financial leverage than Platform has today. Based on analyst estimates for the remaining business, Platform’s shares trade at less than 12 times next year’s earnings, a large discount to competitors. We believe the closing of the sale will simplify Platform’s business portfolio, meaningfully reduce financial leverage, provide capacity for large share repurchases, and serve as a catalyst for future share price appreciation.

Fannie Mae (FNMA) / Freddie Mac (FMCC)

There are no material third quarter updates for Fannie and Freddie regarding housing finance reform or the underlying businesses, which continue to perform well. We believe that last week’s U.S. midterm elections, which resulted in Democrats gaining control of one branch of Congress, make it incrementally more likely that the Trump administration will take the lead on housing finance reform.

Treasury Secretary Steven Mnuchin has repeatedly cited housing finance reform as a priority for 2019. The first step in these efforts is likely the appointment of a new director of the FHFA, Fannie and Freddie’s primary regulator, when the current director’s term ends in January. We will be submitting a public comment letter on FHFA’s draft capital rules for Fannie and Freddie later this week. On the legal front, we and other plaintiffs have filed papers opposing the government’s motion to dismiss 12 cases asserting an unconstitutional taking and related claims and, given delays in the briefing schedule, expect a decision on the motion in late 2019 or early 2020.

Exited Positions

Mondelez International, Inc. (MDLZ)

We reduced our position in Mondelez in recent quarters in order to allocate capital to other opportunities. We sold the balance of our investment during the third quarter. We initially invested in Mondelez because we believed it to be a high quality, defensive business with a meaningful opportunity to increase efficiency that was also an excellent merger candidate in a sector ripe for consolidation. While the company achieved margin expansion in-line with our original thesis, a combination of lower than expected organic growth and higher interest rates led to a reduced price-earnings multiple for Mondelez and, to an even greater extent, the broader packaged food sector.

Save the Date

Please mark your calendar for our Annual Investor Day on February 13, 2019, in London. Details of the event will be forthcoming.

Please contact the investor relations team if you have any questions. We greatly appreciate your support.

Sincerely,

William A. Ackman

{kind=link}