“Risk means more things can happen than will happen.” – Elroy Dimson

As we discussed in our previous articles (here and here) on this topic, the Wuhan coronavirus (coronavirus) has significant uncertainty around potential outcomes. While some countries have started to lift lockdowns and there are talks of returning to normalcy, it is not clear what will that normal look like. It appears much less likely that people will return to their normal ways especially in countries that have been hit hard by the coronavirus.

Q1 2020 hedge fund letters, conferences and more

Will we go out and watch a movie in a theater once the lockdowns have been lifted? Will you sit in tightly packed aircraft seats while not knowing whether the person sitting next to has been infected with the Wuhan coronavirus? Fear is an important driver of human actions. Fear of catching the infection will likely serve as a powerful motivator. Efforts of getting back to normal will be hindered by such fears, acting as impediment to economic restarts.

For global trade and economy to start finding its way back, we need two outcomes to pan out. One, we need testing kits that can “quickly” identify those infected with the coronavirus. The test needs to be low cost, easy to administer, and need to be widely available. Such testing kits, when appropriately administered, will lower the risk of meeting an infected person within closed spaces. And two, absent a vaccine (which could take anywhere from 18 months to three years), we need to have efficacious treatments that ensure that those who do get infected will have a very low probability of serious health complications.

As we currently do not have either of the outcomes in place, the risks and uncertainties associated with the coronavirus persists. So how does this affect the investment evaluation process? How should one account for the elevated risks when researching any business?

As the quote by Mr Dimson highlights, risk means more things can happen than will happen. It is a profound statement about risk and analysis of investment outcomes. Investing is an exercise in probabilities. It means that every expected investment outcome is associated with a range of outcomes around it.

The Wuhan coronavirus impacts investments and portfolios in two ways. One, it has lowered the underlying return for a vast majority of businesses. For a large proportion of businesses, lockdowns result in loss of cashflows as they operate at suboptimal utilization levels. This means that the cashflows that shareholders expect to receive, some of that will be lost forever. And two, it significantly expands the range of outcomes. Importantly, the range expansion is largely to the downside. As a result, expected investment returns drop further lower.

Wuhan Coronaivrus Primary Impacts: The Balance Sheet, Revenues, And Competitive Positioning

As discussed below, there are three primary impacts that one must understand to prepare one’s portfolio to weather this storm.

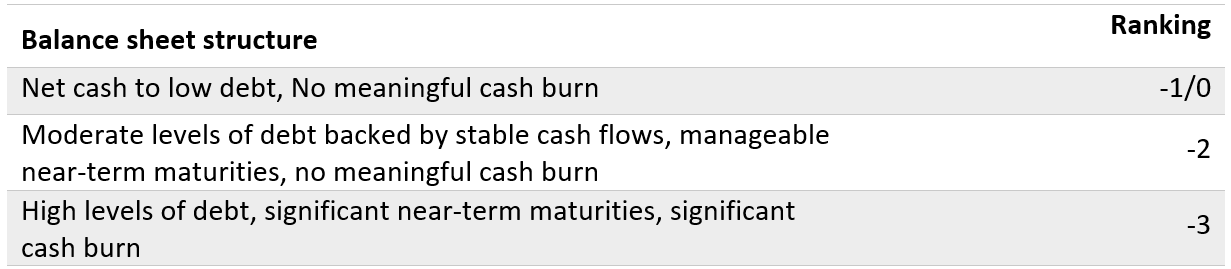

- Balance sheet – the immediate impact. While managers and even investors talk about fortress like balance sheets, the fact is that most balance sheets are structured anything but like a fortress. Attend any business school and chances are that you will be taught about optimal capital structures. These so-called optimal capital structures are optimal only for periods of normalcy or sadly, for the pockets of executives. Talk to any CFO and chances are they will be talking about value they added by buying back stock and levering up their balance sheet.

As you evaluate investments in this environment, you want to take a thorough look at the balance sheets of businesses you own. Are they funded well enough so that they can survive the once-in-a-hundred-year flood? Do they have significant near-term maturities? Are their cash flows contractually guaranteed or embedded in necessities such that cash flows will be sufficient to pay for those maturities?

The answers to these questions will allow you to rank businesses by their balance sheet strength. You can bucket them into groups by your impact assessment, e.g., high impact, moderate impact, and low/no impact[1]. Table 1 summarizes the process and a ranking system that we are currently employing.

Table 1: Assessing the Balance Sheet Impact of Wuhan Coronavirus

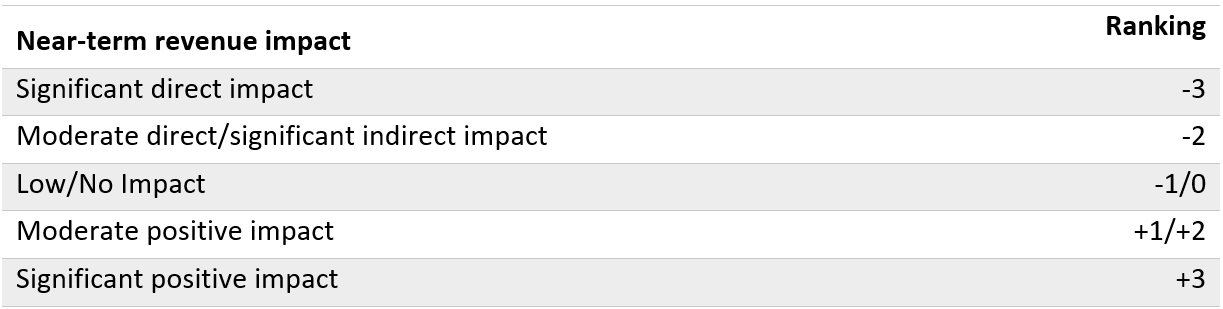

- Revenues – the near-term impact. This is the most obvious impact of the coronavirus driven lockdowns. The lockdowns are causing a significant majority of businesses to lose revenues. At the same time, there are some beneficiaries too that benefit from work from home conditions. Table 2 shows a ranking system that we have employed to assess the revenue impact.

Table 2: Assessing the Revenue Impact of Coronavirus

- Competitive positioning – the intermediate-term impact. This is the relatively indirect and an important impact. As equity owners, our investment values are driven by cash flows that the business will generate over extended periods of time. To the extent that the coronavirus alters those cash flows over extended periods, the investment valuations will be impacted; possibly significantly.

The primary question to ask yourself is whether the coronavirus has altered the competitive positioning of the business. Consider that the coronavirus is frequently deadly for people that have preexisting health complications. It’s impact on businesses is no different. Businesses that were ailing with poor business models will likely be the worst hit as the virus will speed up their demise.

Given the uncertainty involved in such an assessment, we propose a ranking system with limited degrees of freedom. The primary question we are trying to answer is whether the business’s competitive positioning has been meaningfully altered. Table 3 shows a suggested ranking system which you should feel free to modify as per your own investment thinking.

Table 3: Assessing the Competitive Positioning Impact of Coronavirus

Tying it all together

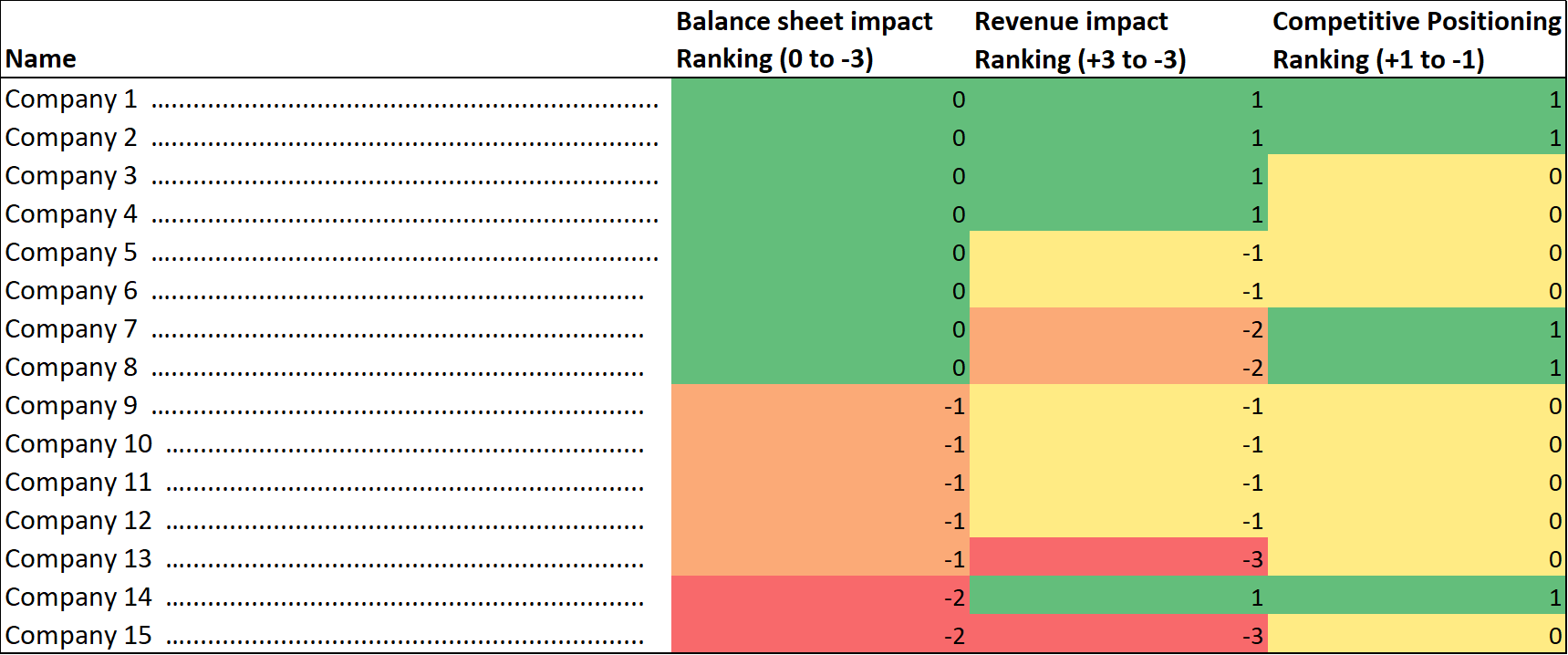

Once you have completed the analysis on each one of these elements, we can then bring it all together by creating a matrix shown in Table 4. As is seen, the process allows one to quickly differentiate the high-risk names from those that are the likely beneficiaries.

For names that show up with all greens, one should be willing to accept lower expected returns as there is a probability of a larger positive outcome. On the other hand, names in all red should likely be avoided. Any investment allocations to such names should only be made at very large discounts to the assessment of business values. In our own portfolios, we maintain zero tolerance for names with negative competitive positioning impacts. We also have zero tolerance for businesses with poorly structured balance sheets. In our opinion, equity allocations to businesses with poorly structured balance sheets should be kept to a minimum. While sometimes such names do offer significant potential upside, they also carry a very high risk of permanent loss of capital.

Table 4: Assessment of Coronavirus’s Impact on Investment Portfolio

Summary

In this article, we discussed a framework for assessing the impact of the Wuhan coronavirus on investment evaluation and portfolio construction. The key point to note is that the coronavirus expands the range of potential outcomes and for vast majority of businesses, it skews the range of outcomes towards the negative side. While we cannot reduce the uncertainty introduced by the coronavirus, consistent application of a well structured risk evaluation process allows us to differentiate businesses where risks are positively skewed from those with significant negative skew.

Wade carefully. Do not go too deep trying to buy the dips.

[1] In general, balance sheets will not be positively impacted by the coronavirus. Of course, policymaker actions do give rise to a perverse situation wherein a business with poor balance sheet gets bailed out and thus improves it balance sheet.