Whitney Tilson’s email to investors discussing his write-up on Tesla; An important message from Porter Stansberry… Introducing Empire Financial Research… The latest warning from the man who nailed the top in Internet stocks, housing, bitcoin, pot stocks, and 3D printing… Please join us on Wednesday, April 17…

After Porter Stansberry’s kind introduction and plug for the webinar we’re doing together on April 17th to launch my new newsletter (you can register for it here – it’s free), he turns over the rest of his email to me to lay out why I think Tesla’s stock is going to collapse – and soon. Be sure to read Glenn’s story about what happened to his Model 3, which he sold back to the company.

Q4 hedge fund letters, conference, scoops etc

Tesla's Weird Purchase Obligations

Yet another bit of inexplicable financial weirdness at Tesla – one of a roughly a dozen things that make me think that there’s a 50% chance that there’s some sort of major fraud going on at the company (the #1 reason is how so many top people in the legal and accounting area suddenly quit!).

HeadbutterBot tweeted this:

2/2 $tsla

BUT their estimate of 2019's obligation more than doubled to $4.9 b.

That's odd because the total estimated obligation didn't change by much.

So did Tesla get a break from it's suppliers in 2018 that it now expects to pay back in 2019?? pic.twitter.com/jXHebYyRnV

— HeadbutterBot (@4xRevenue) April 6, 2019

At the end of 2017, Tesla estimated they would owe suppliers $2.7b over the course of 2018 and an additional $2.3b over the course of 2019. Fast forward to end of 2018, we don't know how much of the $2.3b was paid over 2018, BUT their estimate of 2019's obligation more than doubled to $4.9 b. That's odd because the total estimated obligation didn't change by much. So did Tesla get a break from it's suppliers in 2018 that it now expects to pay back in 2019??

Other people tweeted:

- Either they got a break (highly likely) or just incurred $2 BILLION more POs for 2019. Wonder if a lot of this is Panasonic. Helps explain why the executives in charge of Tesla account resigned in shame.

- This is a huge topic for me, with declining sales the negative cash flow has to be crushing. If same sales as q2 I have them running out of cash around end of June. Unless suppliers financing again or some other new financing.

- Likely that Pana cut them some slack in 2018, prisoners’ dilemma

- Holy smokes, add in the convert payment and we're approaching 6 Bill. Yikes, that's trouble with declining sales and declining ASP.

- There was some rumblings about Tesla having to hand the Gigafactory over to Panasonic depending on 1Q 2019 results. Wonder if it is tied to this.... Here was the post: https://twitter.com/MikeFlo46795160/status/1099911235858886657. I've heard tonight from 4 different employees (2 upper managment). Different departments. One is a Pana employee. All have the same story. And they're all scared shitless knowing EVERYONE is on the line. Told Pana taking over "if Tesla doesn't make Q1 numbers" You decide.

My comments (and Glenn’s): It's like 2018 just got rolled into 2019. What are these purchase obligations? If I were to guess, it’s mostly Panasonic battery commitments. Panasonic likely gave them a break in 2018 on both quantity and price (thus q3 and q4 unexpected profitability) and now there is take-or-pay agreement in 2019. The Panasonic champion was fired/quit a few months ago, so won’t be as easy for Tesla going forward. Other vendors are likely in the same situation, but batteries are the biggest costs.

Mark your calendars for Wednesday, April 17...

That night, at 8 p.m. Eastern time, I (Porter) will announce a major decision I've waited 20 years to share with you.

You might not believe the details. But the fact is, you could make an extraordinary amount of money as a result of this announcement... if you prepare today.

It's a story that involves the likes of Berkshire Hathaway's (BRK) Warren Buffett... former Presidents Barack Obama and Bill Clinton... and three Wall Street billionaires. And you, too, if you're interested.

Just keep in mind, we expect massive demand for this. In fact, one billionaire Wall Street big shot – who manages more than $8 billion – has already agreed to get into this opportunity.

In today's Friday Digest, we're doing something different. We're sharing this brand-new video so you can see why we're so excited. Watch it below.

Today, you're going to hear from my friend Whitney Tilson...

You might recognize the name. For many years, Whitney was one of the most famous (and media savvy) hedge fund managers in New York.

With two degrees from Harvard, a great track record, and investment insights worthy of a 60 Minutes profile, Whitney is, in some respects, everything you'd imagine when the phrase "hedge fund titan" comes to mind.

But that's not what led us to admire him so much or to seek out his friendship more than a decade ago. When you meet someone who is as smart and as accomplished as Whitney, you almost never also meet someone who is humble, kind, generous, and loyal. That's especially true on Wall Street, where the world's most inflated egos thrive.

Have you ever seen a purple squirrel?

No, and you probably never will. Likewise, on Wall Street, if you're looking for hedge fund managers with humility, you're searching for a purple squirrel. But Whitney, like our own Steve Sjuggerud, is that rarest kind of intellectual. He is both super-smart and extremely humble.

How many famous hedge fund managers would close a much-ballyhooed short position just because the CEO published an article urging him to? Whitney did when Reed Hastings explained what he'd gotten wrong in his analysis of Netflix (NFLX). In fact, he didn't merely close his short position, he later bought the stock in one of the greatest trades ever! Investing successfully requires that kind of humility. It also takes guts.

If you want investment insights from one of the world's smartest, most experienced, and best-connected investors, you'd be wise to subscribe to Whitney's new venture, Empire Financial Research.

But that's not why I'm asking you to support his new business...

Whitney has done more than anyone else I know over the last two decades to educate investors and help them make better decisions, including publishing the very best in-depth analysis of Berkshire Hathaway year after year – for free.

His efforts began in the late 1990s, writing columns for the Motley Fool... and then he continued as the founder of a mutual fund and his famous hedge fund. Now retired from money management, Whitney is returning to his true passion: seeking out the truth for investors and helping them make vastly better decisions. And that's why you should subscribe – you'll do very well.

But in addition, you ought to subscribe to Empire Financial Research because Whitney is a superb human being – exactly the kind of person you'd want as a close personal friend and mentor. I know that because, over the last several years, that's what Whitney has become to me.

You should know, I believe so strongly in the quality of Whitney's work that Stansberry Research has invested in Empire Financial Research to support its efforts... just like we have in the past with businesses like TradeStops and Casey Research.

It's my sincere honor to introduce you to Whitney in the pages of Stansberry Research. I urge you to read his work carefully and to subscribe to Empire Financial Research.

And I'd urge you to sign up to save your seat for this incredible event on Wednesday, April 17 right here.

One last note before we turn things over to Whitney...

He has had a long career of making major market calls. At the peak of both the Internet and housing bubbles in early 2000 and 2008, respectively, he warned everyone who would listen that they were sure to burst – and soon.

And then, as the market was bottoming in December 2008, he appeared on 60 Minutes, where he called the stock market bottom. He said, "We're the most bullish we've been in 10 years... With U.S. stocks down nearly 50% from their highs, we're actually finding bargains galore. We think corporate America is on sale."

In early 2014, the financial media picked up his warning on 3D printing companies. At the time, he said 3D Systems (DDD) – which was trading north of $90 a share – was sure to collapse. It fell to less than $10 a share within 18 months.

In December 2017, he called the top in bitcoin almost to the hour. And last September, he appeared on Yahoo Finance to call the bubble in pot stocks the exact day that leading cannabis firm Tilray (TLRY) peaked.

As you'll see in today's Digest, Whitney is once again making a prescient, major market call...

Friday, March 1 was the beginning of the end for electric-car maker Tesla (TSLA)...

Ever since I (Whitney) got burned shorting the stock in 2013 – watching it march higher from $35 to $205 a share – I've warned my readers about betting against CEO Elon Musk and his team. They've simply pulled too many rabbits out of their hat over the years.

Though Musk often behaves like a narcissistic brat, he's also an incredible entrepreneur with a remarkable track record. He has almost single-handedly pushed every major car manufacturer in the world to invest heavily in electric vehicles, and we'll all be better off for it. (The same can be said for SpaceX and the aerospace industry.)

But Tesla has almost done too good of a job. Now, it faces a massive wave of competition. Electric cars from high-end European manufacturers Audi and Jaguar are already vastly outselling Tesla's Model S and Model X cars in Europe. Meanwhile... Toyota, Kia, Hyundai, Volkswagen, Nissan, and Renault are developing their own lower-priced electric vehicles.

As a result of this new competition, I told readers of my free daily e-letter last month that Musk has no more rabbits to pull out of his hat.

I believe Tesla's stock – which closed yesterday around $268 a share – will be trading below $100 by the end of 2019.

I don't get in the habit of making these types of calls often...

As Porter so generously pointed out above, I've made some big calls – but I only do so when three things line up perfectly, as I believe they do now for Tesla: the fundamentals, my "boots on the ground" research, and investor sentiment.

The company's fundamentals are terrible. Demand is weak, inventories are piling up, and investors are finally starting to lose confidence in Musk.

On Wednesday night, Tesla reported a huge miss...

It delivered 63,000 vehicles in the first quarter – far lower than Wall Street's estimates of 76,000. That number represented a stunning 31% drop from the previous quarter. The stock got clobbered on the news, falling more than 8% in yesterday's trading.

But the miss wasn't a surprise to me, thanks to the behind-the-scenes research I've been doing.

For years, I've warned my short-selling friends about shorting Tesla. It's extremely dangerous to short open-ended growth stories based on fundamentals alone. The company has indeed grown its revenues nearly 200 times over the past decade, and its cult-like followers step in to buy on every dip. Trying to short a stock like that is a good way to get your face ripped off.

That said, it can also be extremely profitable to short these story stocks when the growth is busted, but it's not priced into the stock yet. (That's exactly what happened with 3D Systems in 2015.)

Tesla has more red flags than just about any company I've studied in my two decades on Wall Street...

With a market cap of $46 billion – nearly that of General Motors (GM) – the stock is still priced for perfection. This makes no sense given that sales plunged last quarter and the company is closing stores, slashing prices, laying off huge numbers of employees, and for good measure, declaring war on the U.S. Securities and Exchange Commission!

(Plus, I'm 99% certain that Tesla is using extremely aggressive accounting, and I believe there's at least a 50% likelihood that the company is committing outright fraud.)

Consider this story my former business partner, Glenn Tongue, told me. He is one of the biggest tech geeks I know. He bought (and loved) a Model S, and recently purchased a Model 3. He shared the following mind-boggling anecdote with me...

Last September, I sold my Model S to purchase a souped-up Model 3 – the performance version with breathtaking acceleration. I was excited when I first received my new car. But after a short while, I began to miss the features and roominess of the Model S. And then Tesla cut its prices on the Model 3, which made me feel like a chump for having paid a higher price. So I called Tesla and said I wanted to sell my new car back to them. To my surprise, the company let me.

As it turns out, I still have the app on my phone that allows me to track my old car's location, so I was curious to see what Tesla did with it. The answer: Not much. The company immediately moved it to a used-car facility where it has been sitting in an open lot ever since, all winter. The battery has long since drained to zero. It just sits there, losing value every month.

Something isn't right here. Why isn't Tesla selling it? Is it even trying? Why isn't the company periodically charging it to keep it in good enough shape to sell at some point? How is it accounting for this car? Has it taken a write-down? How many more cars are there like mine?

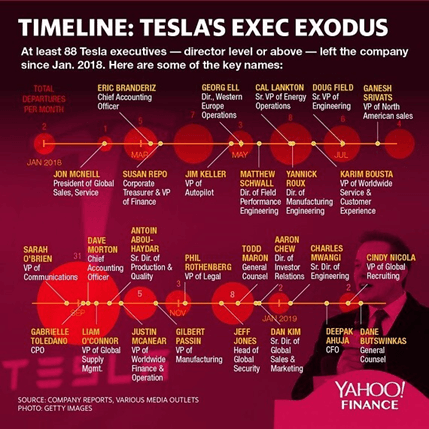

Another big warning flag is the huge number of departures by senior executives. I've never seen anything like it. This graphic that Yahoo Finance put together captures it beautifully...

Notice how heavily skewed the departures are in the legal and accounting areas of the company. That's exactly what you would expect to see if fraud is occurring.

Tesla is in deep trouble...

As the first mover, the company had nearly the entire electric-vehicle market to itself, which led to incredible growth in recent years. That has led Musk and his loyal followers to dramatically overestimate the true demand.

That's easy to do with new, innovative products – which early adopters eagerly buy. But very few such products go mainstream. For every blockbuster hit product like Apple's (AAPL) iPhone, dozens of others fizzle out.

No doubt, Tesla's cars are extremely appealing for wealthy, environmentally conscious tech lovers who are willing to spend a lot of money to drive a cool new toy. But that's a niche market.

Tesla recognizes this, which is why it developed its much-hyped, lower-priced Model 3. But as Glenn discovered, it's not nearly as good of a car. So it's not surprising that once Tesla fulfilled the big backlog of demand from early adopters, sales appear to be falling off a cliff.

I don't think the big sales shortfall in the first quarter is a one-time hiccup. Instead, it's likely a harbinger of things to come. Sales are going to be under even more pressure as competition ramps up.

And even if Tesla's big price cuts stimulate sales, what will that do to the company's margins? It's not clear, for example, that Tesla makes any money at all selling the lowest-priced ($35,000) version of the Model 3.

As for Tesla's investors, even the biggest bulls are growing skeptical...

Galileo Russell, the young millennial host of a finance-focused YouTube channel, gained the Tesla spotlight last summer when Musk cut off "bonehead" Wall Street analysts on an earnings call and instead had a conversation with the 25-year-old.

It's a credit to Russell that he's beginning to question all the insane, inexplicable things that the company and its CEO are doing. Most people I've found do the opposite once they've committed to something, especially if they've done so publicly: They dig in their heels, block out disconfirming information, and attack anyone who questions them.

In contrast, Russell hosted a 28-minute YouTube video last month with his tens of thousands of followers in which he outlined his concerns and practically begged Tesla to raise money. Why it hasn't done so remains a great mystery, but its failure to do so could be its undoing.

Still, you have to give Musk and his team credit where it's due...

They've successfully navigated through one crisis after another for years now, thanks mainly to huge demand for their cars. But now that this appears to be ending, I think their luck has run out.

In fact, I'm so sure that this is the beginning of the end that last month, I offered a friendly wager. I put $10,000 of my own money on the line and challenged Tesla bulls that if the company reports even one profitable quarter this year, I'd donate to the charity of the winner's choice.

A dozen of my readers – including my friend and famed short-seller Andrew Left, who's super-bullish on the stock – took me up on the bet! After this week's news, I'm more confident than ever before that they are going to need their checkbooks by the end of the year.

Mark my words: Tesla shares are going to crash by the end of the year.

One last note before I sign off...

As Porter mentioned at the start of today's Digest, he and I are appearing on camera on Wednesday, April 17 to discuss my biggest investment prediction in 20 years.

I'll be giving away the name and ticker of my No. 1 retirement stock in America just for tuning in. I hope you'll join us. Again, you can save your seat right here.

New 52-week highs (as of 4/4/19): Dow (DOW), Hershey (HSY), Ingersoll Rand (IR), O'Reilly Automotive (ORLY), Rio Tinto (RIO), Starbucks (SBUX), SPDR S&P Dividend Fund (SDY), and W.R. Berkley (WRB).

The mailbag is quiet today. We'd love to hear your thoughts about Tesla. As always, you can send your comments to [email protected].

Regards,

Porter Stansberry and Whitney Tilson

Baltimore, Maryland and New York, New York

April 5, 2019

Stansberry Research Top 10 Open Recommendations

Top 10 highest-returning open positions across all Stansberry Research portfolios

Please note: Securities appearing in the Top 10 are not necessarily recommended buys at current prices. The list reflects the best-performing positions currently in the model portfolio of any Stansberry Research publication. The buy date reflects when the editor recommended the investment in the listed publication, and the return shows its performance since that date. To learn if a security is still a recommended buy today, you must be a subscriber to that publication and refer to the most recent portfolio.

* Position originally recommended by Tom Dyson in The 12% Letter portfolio and carried over into Income Intelligence.

Stansberry Research Hall of Fame

Top 10 all-time, highest-returning closed positions across all Stansberry portfolios