Three Reasons Why Gold Isn’t Behaving Like Gold Right Now by Frank Holmes

As many of you know, I was in San Francisco last week where I had been invited to speak at the MoneyShow, one of the biggest, most preeminent investor conferences in the world. Over the past couple of decades I’ve spoken at many MoneyShows, all around the country. I’ve covered many different topics through the years and gold investing is one that often draws a big crowd. Not this year. Guess which natural resource stole the show?

Another commodity was attracting attendees’ attention, one that until pretty recently could only be grown and harvested under the shroud of secrecy. Marijuana. Currently legal in 23 states and the District of Columbia, medical marijuana generated $2.7 billion in 2014 and is expected to bring in $3.4 billion this year. Investors are taking notice. The cash crop is even starting to change intranational migration. Whereas many retired seniors flock to warmer climates in which to live out their golden years, others now factor in whether a state will permit them to self-medicate in order to treat their arthritis, according to a recent Time article.

Investors themselves who might have suffered from arthritis attended the pot presentation at their own risk, as it was standing room only. They couldn’t have been pulled away even to sit comfortably in the scarcely occupied room next door. Sentiment toward gold was indeed very bearish at the MoneyShow, as it is around the world right now.

Gold is universally recognized as a safe-haven investment, a go-to asset class when others look uncertain. Following the 2008 financial crisis, for instance, the metal’s price surged, eventually topping out at $1,900 per ounce in August 2011.

But this week has been a particularly rocky one for the metal, even with Greece and Puerto Rico’s debt dilemmas, not to mention the recent Shanghai stock market decline, fresh in investors’ minds. Gold has traded down for 10 straight sessions to end the week at $1,099 per ounce, its lowest point in more than five years. Commodities in general have dropped to a 13-year low.

Gold stocks, as expressed by the XAU, have also tumbled.

The selloff was given a huge push last Friday when China, for the first time in six years, revealed the amount of gold its central bank holds. Although the number jumped nearly 60 percent since 2009 to 1,658 tonnes, markets were underwhelmed, as they had expected to see double the amount.

Then in the early hours on Monday, gold experienced a “mini flash-crash” after five tonnes appeared on the Asian market. Initially this might not sound like a lot, but five tonnes equates to 176,370 ounces, or about $2.7 billion. It also represents about a fifth of a normal day’s trading volume. Suffice it to say, price discovery was effectively disrupted. In a matter of seconds, gold fell 4 percent before bouncing back somewhat.

Reflecting on the trading session, widely-respected market analyst Keith Fitz-Gerald noted: “Far from being a one-day crash, this could represent one of the best gold-buying opportunities of the year.”

The last time the metal descended this quickly was 18 months ago, on January 6, 2014, when someone brought a massive gold sell order on the market before retracting it in a high-frequency trading tactic called “quote stuffing.” Last month I shared with you that we now know who might have been responsible for the action—and many others that preceded it—and pointed out that the accused party’s penalty of $200,000 was grossly inadequate. On Monday I told Daniela Cambone during this week’s Gold Game Film that such downward price manipulation seems to result in little more than a slap on the wrist. But if manipulation is done on the upside, traders could get into serious trouble.

Besides apparent price manipulation, other factors are affecting gold’s behavior right now, three in particular.

- Strong U.S. Dollar

Like crude oil, gold around the world is priced in U.S. dollars. This means that when the greenback gains in strength, the yellow metal becomes more expensive for overseas buyers. With the U.S. economy on the mend after the recession, the dollar index remains steady at a 12-year high.

It’s important to recognize, though, that gold is still strong in other world currencies, including the Canadian dollar. As such, our precious metals funds have hedged Canadian dollar exposure for Canadian gold stocks, which has benefited our overall performance.

- Interest Rates on the Rise?

Federal Reserve Chair Janet Yellen continues to hint that interest rates might be hiked sometime this year, perhaps even as early as September. When rates move higher, non-yielding assets such as gold often take a hit.

As you can see, the 10-year Treasury bond yield and gold have an inverse relationship. When the yield starts to rise, investors might find bonds a more attractive asset class.

- Slowing Manufacturing Activity

Earlier this month I wrote about the downtrend in manufacturing activity across the globe. As many loyal readers are well aware, we closely monitor the global purchasing manager’s index (PMI) because, as our research has shown, when the one-month reading has fallen below the three-month moving average, select commodity prices have receded six months later.

China is the 800-pound commodity gorilla, and its own PMI has remained below the important 50 threshold for the last three months, indicating contraction. The preliminary flash PMI, released today, reveals that manufacturing has dipped to 48.2, a 15-month low. For gold and other commodities to recover, it’s crucial that China jumpstart its economy.

In the meantime, we’re encouraged by news that the slump in prices has accelerated retail demand in both China and India, which, when combined, account for half of the world’s gold consumption.

Battening Down the Hatches

They say that a smooth sea never made a skillful sailor. No one embodies this more than Ralph Aldis, portfolio manager of our precious metals funds. He and our talented team of analysts are doing a commendable job weathering this storm. We’re invested in strong, reliable companies, and when commodities eventually turn around, we should be in a good position to catch the wind.

We look forward to the second half of the year, when gold prices have historically seen a bump in anticipation of Diwali, which falls on November 11 this year, and the Chinese New Year. As you can see, average monthly gold performance has ramped up starting in September.

“Gold is down 15 to 25 percent below production levels,” Ralph says. “That might cause some companies to halt production.”

And, in so doing, help prices find firmer footing.

After my San Francisco experience it only seems fitting that I traveled to Colorado, one of the first states to legalize cannabis for recreational use. It was only a coincidence that Julia Guth chose to retreat to the state’s beautiful mountains for the Oxford Club’s educational seminar. It was a privilege to present to two assemblies of curious investors like yourself. I enjoy meeting many of you when I’m on the road.

Index Summary

- The major market indices were down this week. The Dow Jones Industrial Average fell 2.86 percent. The S&P 500 Stock Index lost 2.21 percent, while the Nasdaq Composite fell 2.33 percent. The Russell 2000 small capitalization index fell 3.24 percent this week.

- The Hang Seng Composite fell 1.04 percent this week; while Taiwan fell 3.07 percent and the KOSPI fell 1.48 percent.

- The 10-year Treasury bond yield fell 8 basis points to 2.26 percent.

Domestic Equity Market

Strengths

- Consumer discretionary was the best performing sector in the S&P 500 Index this week as investors moved out of areas with a large degree of foreign and/or commodity exposure. The S&P 500 Consumer Discretionary Sector Index fell 0.46 percent this week.

- Existing home sales in the U.S. climbed to the highest rate since February 2007. The housing market has been gaining strength over the last few months.

- Initial jobless claims fell to the lowest level in over 40 years, highlighting the tightening labor market in the U.S.

Weaknesses

- Materials got hammered this week as precious metals stocks declined over concerns of a September rate hike, while base metals stocks fell on concerns over a slowdown in the Chinese economy. The S&P 500 Materials Sector Index fell 5.47 percent this week.

- Energy slumped this week as crude oil prices continue to fall, testing the lows seen earlier this year. The S&P 500 Energy Sector Index fell 4.07 percent this week.

- Industrials underperformed given the lack of faith in Chinese growth as well as a depressed energy market. The S&P 500 Industrials Sector Index fell 3.81 percent this week.

Opportunities

- The Markit U.S. manufacturing purchasing managers’ index (PMI) remains well above the 50 mark, with the most preliminary reading for June coming in at 53.8.

- The Conference Board U.S. Leading Index, comprised of economic variables that tend to move before changes in the overall economy, rose by 0.6 percent from the prior month, exceeding analysts’ estimates.

- After contracting in the first quarter, the United States economy is expected to have grown by 2.6 percent in the second quarter, according to a Bloomberg survey of economists.

Threats

- Inflationary pressures should start becoming more prevalent in the economy as the labor market continues to tighten and wages rise. If there is a noticeable positive shift in inflation it would only strengthen the Federal Reserve’s decision to raise rates in September, which could cause equities to retreat.

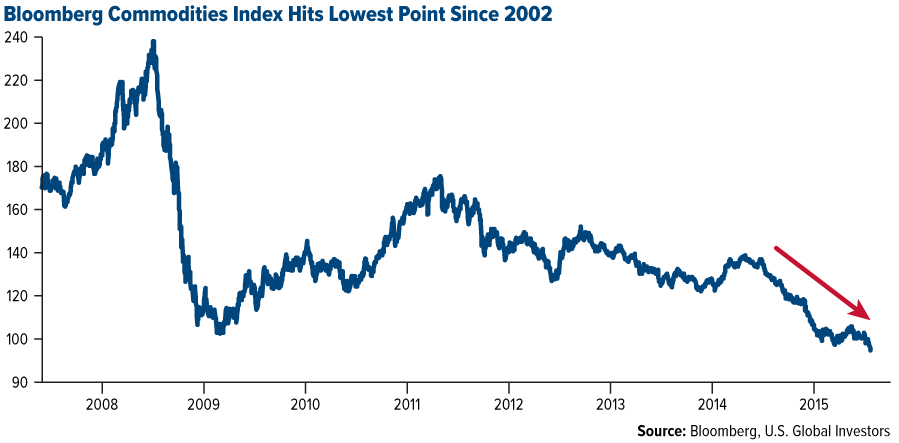

- Commodities are in trouble. The Bloomberg Commodities Index reached its lowest point since 2002, surpassing the lows seen during the financial crisis. With no trend shift in sight, commodity-sensitive plays could remain vulnerable in the near future.

- The Conference Board Consumer Confidence Index is expected to decline next week, which could weigh on retailers as well as other discretionary plays.

The Economy and Bond Market

Stocks retreated globally, largely driven by weak corporate earnings, as U.S. companies posted their second-quarter results. Apple, IBM, Caterpillar and Microsoft were among the big names to miss earnings estimates or cut full-year forecasts. However, Morgan Stanley and Amazon beat expectations. So far, more than 75 percent of companies have exceeded earnings forecasts, while only 52 percent have surpassed revenue expectations.

The yields on the 10-year U.S. Treasury note and 10-year German bund fell to 2.26 percent and 0.69 percent, respectively, as investors sought more safety. The euro rose to near $1.10. Oil prices for U.S. West Texas Intermediate (WTI) and international Brent crude oil tumbled to about $48 and $54.70 per barrel, respectively.

Strengths

- Existing home sales added 3.2 percent month-over-month in June, to a seasonally adjusted annual rate (SAAR) of 5.49 million, and were revised slightly lower in May to 5.32 million, from 5.35 million initially. This was above expectations of 5.40 million SAAR and represents the highest level since early 2007. This report is consistent with a range of housing market indicators that have shown improvement recently.

- Initial jobless claims were reported at 255,000 for the week ending July 18, down from 281,000 in the prior week and below the expected 278,000. This is the lowest level of claims since November 1973 and pushes the four-week moving average down to 278,500 from 282,500. The Labor Department noted that claims are showing “typical volatility this time of year” and that claims for Puerto Rico were estimated. Given this volatility, it’s best to focus on the four-week moving average, which remains healthy.

- Global bonds saw $5.5 billion in inflows for the week, the largest in three months. Flows were across the board as the 10-year U.S. Treasury again failed to break above the 2.5-percent level.

Weaknesses

- New home sales fell 6.8 percent month-over-month in June, decreasing to 482,000, lower than expectations of 548,000. May was revised lower to 517,000 from 546,000 initially, representing a revision to a 1.1 percent month-over-month decrease from a 2.2 percent month-over-month increase initially. April was revised lower to 523,000 from 534,000, and March was revised lower as well to 485,000 from 494,000.

- Equities are at risk from profit disappointment. Companies still lack pricing power: both global-exposed and domestic-exposed equity sector pricing power is contracting for the first time since 2009. Given that wage growth is rising, tighter margins are more probable than pass-through into inflation.

- Equities have become increasingly dependent on rising earnings multiples over the past few years. Since 2013, forward P/E expansion has accounted for 65 percent of the 42 percent S&P 500 total return, with forward earnings growth accounting for the remaining 35 percent. The Federal Reserve’s willingness to hike rates soon reduces the odds of multiple expansion, even if bond yields decline.

Opportunities

- The first GDP growth estimate for the second quarter (Thursday) and the Fed’s preferred wage measure, the employment cost index (Friday), will be released after the Fed meeting. Confirmation that U.S. economic growth picked up in the second quarter and that wage growth is improving will bolster the case for lifting rates this year.

- The Federal Open Market Committee’s (FOMC’s) 2015 growth forecasts have been downgraded to the point where real GDP growth only has to average 2.6 percent to 2.9 percent over the final three quarters of the year for the Fed’s full-year median forecast to be met. The Atlanta Fed’s “GDP Now” forecast of growth in the second quarter is now up to 2.4 percent, with private sector forecasts coming in slightly above that. So it is probably safe to say that the second quarter has evolved in line with the Fed’s expectations.

- The recent broad-based weakening of currencies versus the dollar is due in part to the fact that the U.S. is talking about rate hikes and virtually every other central bank is holding rates steady, cutting rates, or in the case of Europe and Japan, doing active quantitative easing. Global investors are clearly finding U.S. yields more attractive, both in corporate debt and more recently in Treasury debt, according to the U.S. Treasury data on capital flows. These inflows are likely to continue providing support to the dollar.

Threats

- For now, market action is better for U.S. equities than bonds. But the reward/risk tradeoff is moving in favor of bonds versus stocks. Stocks tend to outperform bonds in the early stages of a Fed tightening cycle. However, this time may well be different because multiples are high and the dollar may be more resilient as a result of disappointing growth abroad. In general, relative equity/bond performance tends to deteriorate when the yield curve flattens, the dollar is firm and oil prices are soft, as is expected over the next six to 12 months.

- U.S. non-defense capital goods orders, excluding aircraft, have declined in all but one month this year. With June data being released on Monday, further disappointment on the capex front could weigh on stock prices.

- The solid pace of lending to euro-area households and firms showed some signs of slowdown in May. Eurozone money and lending numbers for June will be released on Monday and a further slowdown would incite concern about the European recovery. Credit flows are an important determinant of the longevity of positive euro-area growth momentum.

Gold Market

For the week, spot gold closed at $1,099.05 down $35.42 per ounce, or 3.12 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, lost 9.72 percent. The U.S. Trade-Weighted Dollar Index lost 0.60 percent for the week.

| Date | Event | Survey | Actual | Prior |

| July -23 | .S. Initial Jobless Claims | 18-Jul | 278K | 255K |

| July -23 | Caixin China PMI Mfg | Jul P | 49.7 | 48.2 |

| July -24 | U.S. New Home Sales | Jun | 548K | 482K |

| July -27 | Hong Kong Exports YoY | Jun | -4.00% | — |

| July -27 | U.S. Durable Goods Orders | Jun | 3.10% | — |

| July -28 | U.S. Consumer Confidence Index | Jun | 100 | — |

| July -29 | FOMC Rate Decision (Upper Bound) | 29-Jul | 0.25% | — |

| July -30 | Germany CPI YoY | Jul P | 0.30% | — |

| July -30 | U.S. GDP Annualized QoQ | 2Q A | 2.60% | — |

| July -30 | U.S. Initial Jobless Claims | 25-Jul | 272K | — |

| July -31 | Eurozone CPI Core YoY | Jul A | 0.80% | — |

Strengths

- On July 17, in the first update since 2009, the People’s Bank of China said it owns about 1,658 metric tons of gold, implying purchases of just 100 tons a year. That’s significantly less than consensus expectations and thus leaves the door open for further accumulation as China attempts to internationalize the renmimbi.

- China has revealed an active yet patient “bargain hunting” accumulation strategy for its gold reserves. Chinese consumers historically bought gold in anticipation of a rally. However, for the government, the metal’s low price remains critical for the central bank to accumulate it.

- According to Commerzbank AG, after a relentless stretch of losses in the gold price over the past week since the Bank of China’s announcement, is due for a pause. The bank said the market selloff has ended for now and investors should exit their short positions and buy in, perhaps triggering a near term rally in the gold price. It is likely that buying that started late in the afternoon at the close of the week reflected some short covering.

Weaknesses

- In Asian trading hours early in the week, investors dumped more than $500 million worth of bullion in New York in a matter of seconds with selling occurring almost simultaneously on Chinese markets. The sheer scale of order flow across both the Shanghai Gold Exchange and the Shanghai Futures Exchange, where combined volume on Monday surpassed the notional equivalent of 250 tons, led many market trackers to speculate that Chinese hedge funds were behind the move. The moves have the hallmarks of speculative selling to push the price lower, given the size and timing of the orders to sell.

- With gold prices tumbling to five year lows, investors aren’t just selling out, they’re betting against it. Speculators in July amassed record short holdings in the metal. Also telling is that the number of hedge funds that are hoping to profit from declines is near a record high. Further signs of trouble are the fact that Indian jewelry bargain hunters are holding off from buying because they believe the collapse in price has further to run.

- The Bloomberg Commodities Index dropped to a 13-year low this week, weaker than after the financial crisis of 2008 and the eurozone crisis of 2012. South Africa’s index of gold mining stocks fell to the lowest level since April 2001, as the precious metal slid to a five-year low with local producers battling rising costs. Lastly, money managers are holding the smallest net-long bets on gold since the U.S. government data begins in 2006.

Opportunities

- If low gold prices persist this may increase the appeal of mining companies on a valuation basis. Gold mining companies are already trading at an eight-year low on an enterprise value-to-reserve and resource basis, according to Bloomberg Intelligence data. Deals for gold miners reached a two-year high in the second quarter when the premium paid for companies approached its highest in 12 years.

- The ratio of paper claims to physical gold continues to creep higher, going from 75:1 to 95:1 in the last month as gold traded down 7.5 percent. On Monday, about 7,000 gold futures contracts, representing about 21.8 tons of paper gold, were dumped at market in one minute driving the price down to $1,080. This could be a turning point given that in the first two weeks of 2014, the ratio of paper claims to physical gold went from 76:1 to 112:1 and gold went up by almost $200/oz in the following two months.

- Canaccord Genuity maintained its buy rating and C$5.00 price target on Klondex Mines following better than expected consolidated second quarter operating results. Sales exceeded their expectations by 10 percent, primarily due to higher mill throughput and considerably higher gold grades. Management also increased FY2015 guidance to 125-130 thousand ounces. This marks the second consecutive year that Klondex has raised guidance. Klondex currently trades at more than a 10 percent discount to its peers based on premium to net asset value. Canaccord believes this is an attractive entry point into one of the highest quality intermediate gold producers in the sector.

Threats

- According to Morgan Stanley, gold could tumble to $800/oz under their worst case scenario. Getting there would require U.S. policymakers to start raising interest rates, another correction in China’s stock market and a sell-down of reserves by central banks. Furthermore, Barnabas Gan, the most accurate forecaster of precious metals in rankings compiled by Bloomberg, predicts gold will reach $1,050/oz by December.

- Global mining companies are facing a looming succession crisis. Several mining CEOs have reached or are nearing retirement age and industry executives, recruiters and analysts worry that there is not enough people with the right skills and experience to replace the old guard. Mark Bristow, CEO of Randgold Resources, said that there is a shortage of potential CEOs because the industry doesn’t invest in people.

- According to a labor relations consultant, a pay strike at South African gold companies could result in bloodshed at the mines.

Energy and Natural Resources Market

Strengths

- Construction materials outperformed in an overall down market this week. The S&P 500 Construction Materials Index fell 0.77 percent this week.

- Packaged foods stocks were among the best relative outperformers this week as the strong U.S. dollar, concerns out of China, and falling oil prices weighed heavily on more cyclical areas. The S&P 500 Supercomposite Packaged Foods Index fell 0.87 percent this week.

- The U.S. dollar did pull back slightly this week, easing some of the tension currently being placed on commodities. The U.S. Dollar Index fell 0.62 percent.

Weaknesses

- Precious metals stocks fell sharply this week as investors are turning away from this asset class in favor of other yielding assets instead. Furthermore, gold has been particularly vulnerable to increasing concerns of a September rate hike. The NYSE Arca Gold Miners Index and the Global X Silver Miners ETF fell 9.72 and 9.46 percent, respectively.

- Upstream oil and gas stocks fell with crude oil as the market continues to see ample supply. The S&P Supercomposite Oil & Gas Drilling Index fell 6.35 percent this week.

- Base metals stocks pulled back as investors continue to fear a slowdown in China’s growth. The S&P/TSX Capped Diversified Metals and Mining Index fell 11.17 percent this week.

Opportunities

- According to recent surveys, China’s manufacturing purchasing managers’ index (PMI) data for July could come in at 50.2, which could positively offset disappointing data from HSBC’s preliminary report.

- Iran has identified 50 oil and gas projects worth $185 billion that it hopes to sign by the year 2020. Using a model contract addresses some of the deficiencies of the old buyback contract and further aligns the short- and long-term interests of parties involved.

- Chinese stockpiles fell to the lowest level in a year as refinery demand surged. Commercially-held inventories dropped by 2.1 percent in June as China boosted refining to a record 10.59 million barrels per day in June.

Threats

- China is spooking the market as investors are quickly losing confidence that the economic juggernaut can grow at the expected pace. Until confidence in the Chinese economy is restored, commodities could face serious headwinds.

- Oil seems to be testing the same lows seen back in March. WTI crude oil could be in a flat-to-down trend for the near future.

- The Federal Reserve has all but said for certain that they will raise interest rates this year. As more investors consider this to be true, precious metals stocks will continue to see pullbacks.

Emerging Markets

Strengths

- In an overall depressing week for emerging markets, Chinese equities outperformed and the mainland market continues to recover from its sharp selloff. The Shanghai Stock Exchange Composite Index rose 2.87 percent this week.

- It appears things could return to normal in Greece as rumors point to markets opening on Monday. While the banks may remain closed and certain restrictions will be put in place for domestic investors, overall the news is positive.

- Both Czech equities and the koruna rallied this week as analysts continue to revise up the Eastern European economy’s GDP forecast. The Prague Stock Exchange Index and the koruna rose 0.57 and 1.21 percent, respectively.

Weaknesses

- Brazilian equities fell sharply this week as the commodity-sensitive economy continues to show signs of weakness along with concerns of a slowdown in China spooking investors. The Ibovespa Brasil Sao Paulo Stock Exchange Index and the real fell 6.08 and 4.62 percent, respectively.

- Turkey is experiencing various security issues concerning ISIL fighters on its southern border, causing equities and the country’s currency to fall this week. Furthermore, the prospects for the formation of a coalition government are becoming weaker, raising the probability for a snap election in November. The Borsa Istanbul 100 Index fell 4.93 percent this week, while the lira depreciated 3.26 against the U.S. dollar.

- Polish equities suffered this week as investors fear the proposals to 1) introduce a new tax on bank assets and 2) convert mortgages denominated in Swiss francs to Polish zloty, could negatively affect economic growth. The WIG20 Index fell 4.26 percent this week.

Opportunities

- Czech’s economy is set to grow at its fastest pace in years with a rapid rise in GDP, according to a Bloomberg economic forecast.

- India is benefiting from the turmoil in Chinese markets as more investors change course and head for calmer emerging markets. India’s economy also grew at a faster rate in the first quarter as falling oil prices boosted economic activity.

- Vietnam stands out among top beneficiaries in Asia of the Trans-Pacific Partnership (TPP) agreement, finalized as soon as next week. The Southeast Asian country has already surpassed China in exports to the U.S. in the last three years, with a young, educated workforce and manufacturing wages more than 50 percent lower than China. Asian companies with investments or manufacturing facilities in Vietnam taking advantage of favorable trade tariffs related to TPP should continue to outperform moving forward.

Threats

- The Athens Stock Exchange General Index could get hit hard when it reopens The Global X FTSE Greece 20 ETF. As a proxy for the Greek market, it has lost over 13 percent since the country’s stock market froze.

- Turkey is experiencing a high degree of uncertainty at the moment with a coalition government yet to be formed and emerging security threats along the southern border. These risks could push the Turkish lira down further.

- There is little indication that a price war in the Chinese automobile market initiated by foreign manufacturers since April has revived demand. In addition, recent local stock market volatility does not help support consumer confidence for big ticket item purchases. Investor sentiment towards automobile-related stocks could remain subdued in the near term.

Leaders and Laggards

| Weekly Performance | |||

| Index | Close | Weekly Change($) |

Weekly Change(%) |

| DJIA | 17,568.53 | -517.92 | -2.86% |

| S&P 500 | 2,079.65 | -46.99 | -2.21% |

| S&P Energy | 510.24 | -21.62 | -4.06% |

| S&P Basic Materials | 282.66 | -16.34 | -5.46% |

| Nasdaq | 5,088.63 | -121.51 | -2.33% |

| Russell 2000 | 1,225.99 | -41.10 | -3.24% |

| Hang Seng Composite Index | 3,441.47 | -36.00 | -1.04% |

| Korean KOSPI Index | 2,045.96 | -30.83 | -1.48% |

| S&P/TSX Canadian Gold Index | 124.54 | -12.18 | -8.91% |

| XAU | 48.52 | -5.68 | -10.48% |

| Gold Futures | 1,099.00 | -34.50 | -3.04% |

| Oil Futures | 48.07 | -2.82 | -5.54% |

| Natural Gas Futures | 2.78 | -0.09 | -3.14% |

| 10-Yr Treasury Bond | 2.26 | -0.09 | -3.62% |

| Monthly Performance | |||

| Index | Close | Monthly Change($) |

Monthly Change(%) |

| DJIA | 17,568.53 | -397.54 | -2.21% |

| S&P 500 | 2,079.65 | -28.93 | -1.37% |

| S&P Energy | 510.24 | -51.48 | -9.16% |

| S&P Basic Materials | 282.66 | -29.08 | -9.33% |

| Nasdaq | 5,088.63 | -33.78 | -0.66% |

| Russell 2000 | 1,225.99 | -57.93 | -4.51% |

| Hang Seng Composite Index | 3,441.47 | -356.73 | -9.39% |

| Korean KOSPI Index | 2,045.96 | -39.57 | -1.90% |

| S&P/TSX Canadian Gold Index | 124.54 | -30.00 | -19.41% |

| XAU | 48.52 | -17.33 | -26.32% |

| Gold Futures | 1,099.00 | -76.10 | -6.48% |

| Oil Futures | 48.07 | -12.20 | -20.24% |

| Natural Gas Futures | 2.78 | +0.02 | +0.76% |

| 10-Yr Treasury Bond | 2.26 | -0.11 | -4.43% |

| Quarterly Performance | |||

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

| DJIA | 17,568.53 | -511.61 | -2.83% |

| S&P 500 | 2,079.65 | -38.04 | -1.80% |

| S&P Energy | 510.24 | -87.74 | -14.67% |

| S&P Basic Materials | 282.66 | -32.64 | -10.35% |

| Nasdaq | 5,088.63 | -3.46 | -0.07% |

| Russell 2000 | 1,225.99 | -41.54 | -3.28% |

| Hang Seng Composite Index | 3,441.47 | -510.65 | -12.92% |

| Korean KOSPI Index | 2,045.96 | -113.84 | -5.27% |

| S&P/TSX Canadian Gold Index | 124.54 | -37.23 | -23.01% |

| XAU | 48.52 | -21.43 | -30.64% |

| Gold Futures | 1,099.00 | -78.70 | -6.68% |

| Oil Futures | 48.07 | -9.08 | -15.89% |

| Natural Gas Futures | 2.78 | +0.25 | +9.84% |

| 10-Yr Treasury Bond | 2.26 | +0.35 | +18.54% |

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

{kind=link}

{kind=link}