At Sure Dividend, we make no secret of the fact that we are huge proponents of investing in high-quality dividend growth stocks. Specifically, we suggest investors looking for the best dividend growth stocks take a hard look at the Dividend Aristocrats.

Q1 hedge fund letters, conference, scoops etc, Also read Lear Capital: Financial Products You Should Avoid?

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

The Dividend Aristocrats are a select group of 53 stocks in the S&P 500 Index, with 25+ consecutive years of dividend increases. You can download an Excel spreadsheet of all 53 (with metrics that matter) by clicking the link below:

Click here to download your Dividend Aristocrats Excel Spreadsheet List now.

The reason why we are such big fans of the Dividend Aristocrats is simple. Thanks to their strong brands, durable competitive advantages, and steady growth, they have significantly outperformed the broader stock market.

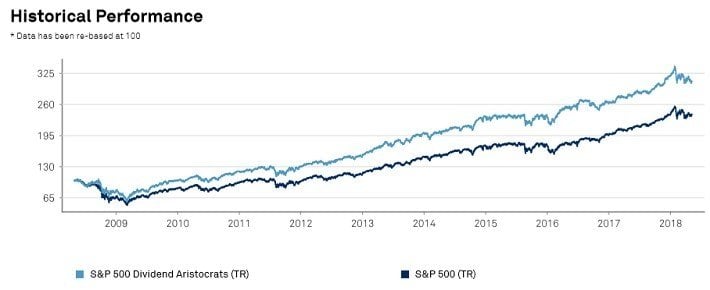

Source: Standard & Poor’s

Dividend growth stocks are typically viewed as safe, “widow-and-orphan” stocks that should be held for steady dividend income instead of high share price appreciation. But as the above image shows, the Dividend Aristocrats have actually outperformed the broader S&P 500 Index since the Great Recession ended.

In the past 10 years, the Dividend Aristocrats generated total returns of 12% per year, compared with 9% for the S&P 500 Index.

This article will discuss the top 10 Dividend Aristocrats today. The rankings in this article are derived from our expected total return estimates for every Dividend Aristocrat (and 100+ other stocks) found in the Sure Analysis Research Database.

Keep reading this article to see the Top 10 highest expected total return Dividend Aristocrats today.

Top Dividend Aristocrat #10: S&P Global Inc. (SPGI)

S&P Global has a very impressive dividend track record. It has paid a dividend each year since 1937, and has increased its dividend for 45 years, including a 22% hike in February.

S&P Global offers financial services, including credit ratings, benchmarks, analytics, and data, to the global capital and commodity markets. For example, the S&P 500 is arguably the most widely-known stock market index in the world.

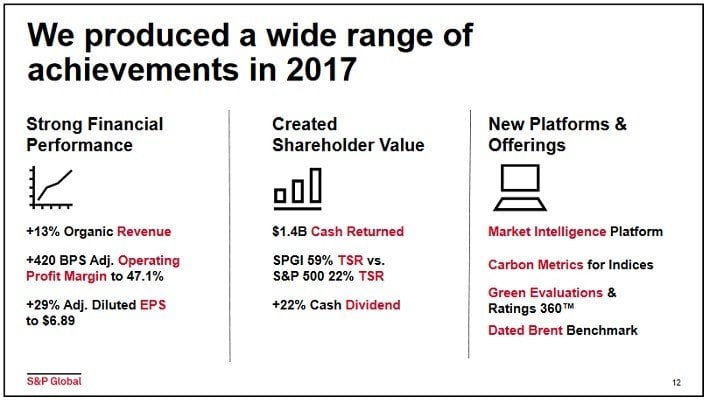

S&P Global has a long track record of growth. 2017 was another strong year, with 13% organic revenue growth, and 29% adjusted earnings-per-share growth for the year.

Source: 2018 Annual Shareholders Meeting, page 12

S&P Global has significant catalysts for future growth. S&P Global recently announced it will acquire Kensho, to bolster its capabilities in artificial intelligence and data analytics, both of which are growth categories.

And, S&P Global enjoys multiple competitive advantages. It operates in a highly concentrated industry. It is one of only three major credit ratings agencies in the U.S., along with Moody’s (MCO) and Fitch Ratings.

Put together, these three companies control over 90% of the global financial debt rating industry, with S&P Global on top.

In terms of valuation, S&P Global is richly valued. We estimate fair value for S&P Global stock to be $178 per share. As a result, we see the stock as slightly overvalued. A declining price-to-earnings ratio could reduce annual returns by approximately 1.7% per year.

However, the company can still generate strong total returns, through earnings growth and dividends. With expectations of 10% earnings growth per year, including a 1% dividend yield, total returns would reach approximately 10% annually, including impact of valuation changes.

Top Dividend Aristocrat #9: Exxon Mobil (XOM)

Exxon Mobil is one of only two energy stocks on the list of Dividend Aristocrats, the other being Chevron. Exxon Mobil is the largest oil and gas company in the U.S., with a market capitalization of $330 billion. Exxon Mobil also has an attractive dividend yield of 4.2%, and the company has increased its dividends for over 30 consecutive years.

Going forward, 2018 will likely be another year of growth for Exxon Mobil. Growth will be fueled by new projects set to come on line or ramp up.

With a more favorable pricing environment, this could accelerate upstream earnings growth in 2018. Exxon Mobil’s revenue and earnings-per-share increased 6% and 16%, respectively, in the first quarter.

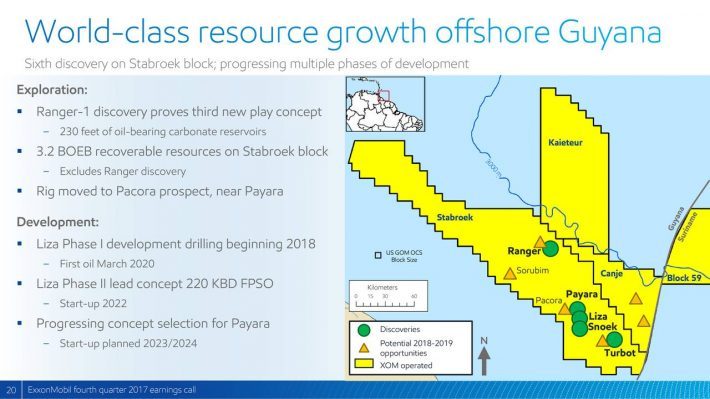

Exxon Mobil’s most significant new project could be offshore Guyana.

Source: Earnings Presentation, page 20

Discoveries from offshore Guyana are now estimated to total more than 3.2 billion recoverable oil-equivalent barrels. In addition, the resources discovered can be drilled and produced very profitably. For example, Exxon Mobil’s deep-water discoveries have breakeven costs, including taxes, of just $26 per barrel, while Brent oil currently trades for $75 per barrel.

Guyana will be a major driver of Exxon’s future production growth. At its 2017 Analyst Meeting presentation, Exxon gave guidance for annual production to rise to 4.0-4.4 million barrels per day by 2020.

Despite operating in a cyclical, and often highly volatile industry, Exxon Mobil has a stable dividend payout. As an integrated major, Exxon Mobil has large businesses across the upstream and downstream sides of the industry, which helps it generate cash flow even when oil and gas prices decline.

Including Exxon Mobil’s 4.2% dividend yield and expectations of 8%-9% annual earnings growth, we estimate total returns to be 12%+ per year.

Top Dividend Aristocrat #8: PPG Industries, Inc. (PPG)

PPG Industries was originally founded all the way back in 1883. Today, it is the largest paint company in the world. It is also one of the most reliable dividend stocks. PPG has paid dividends every quarter since 1899, and it has increased its dividend for 46 years in a row.

PPG dominates the paints industry, along with Sherwin-Williams (SHW). PPG has grown into an industry giant, thanks to a history of innovation. The company has approximately 3,500 technical employees located in more than 70 countries at 100 unique locations. The company’s research and development focus is a key competitive advantage for PPG.

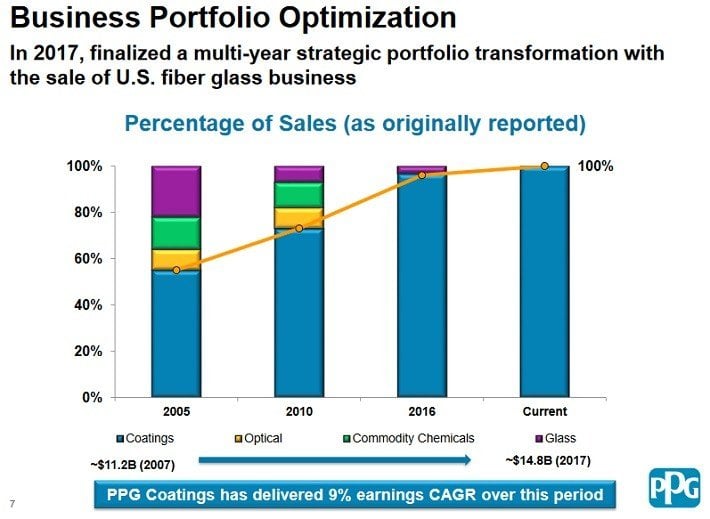

PPG is repositioning its product portfolio, divesting itself of slower-growth businesses and reinvesting more heavily in products that will lead the company’s future.

Source: 2018 Investor Overview, page 7

For example, in 2017 PPG completed the divestiture of its fiberglass business, while conducting four bolt-on acquisitions in its core paints and coatings businesses. And, even though the company experienced higher raw materials costs, adjusted earnings-per-share increased 4%, thanks to cost-cutting.

PPG reported $3.8 billion of revenue in the first quarter of 2018, up 9% year-over-year. Adjusted earnings-per-share from continuing operations increased 4% from the same quarter a year ago.

PPG stock is reasonably valued, with a price-to-earnings ratio of 16.5. In the past 10 years, the stock held an average price-to-earnings ratio of 19.9. The average valuation over the past decade is a reasonable estimate of fair value, which indicates the stock is undervalued.

Over the next five years, expansion of the price-to-earnings ratio could add approximately 2%-3% to PPG’s annual returns. In addition, if earnings grow at 8% annually, plus a current dividend yield of 1.7%, total annual returns could exceed 12% for PPG stock.

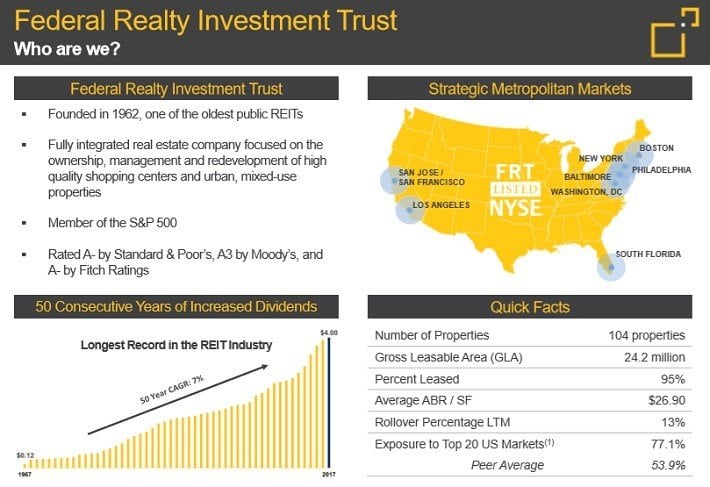

Top Dividend Aristocrat #7: Federal Realty Investment Trust (FRT)

Federal Realty is the only Real Estate Investment Trust, or REIT, on the list of Dividend Aristocrats. Not only that, but Federal Realty is actually a Dividend King, a small group of 24 stocks with 50+ consecutive years of dividend growth.

You can see all 24 Dividend Kings by clicking the link below:

Click here to download my Dividend Kings Excel Spreadsheet now.

Federal Realty primarily owns shopping centers. It also operates in redevelopment of multi-purpose properties including retail, apartments, and condominiums. Federal Realty owns over 100 properties, and focuses on densely-populated, affluent communities, with high demand for commercial and residential real estate.

Source: 2018 Investor Presentation, page 2

These qualities set it apart from the competition. According to the company, its cash rents are 60% above the industry average. Its strategy has led to strong growth rates in recent years. In the 2018 first quarter, Federal Realty’s funds from operation (FFO) increased 4.8% from the same quarter a year ago. Operating income on properties held for at least a year, rose 3.8% for the quarter.

One potential risk for Federal Realty is rising interest rates. REITs typically rely heavily on debt to finance new property acquisitions. Indeed, Federal Realty has a debt-to-EBIDTA ratio of 5.8. However, the company expects to reduce its leverage ratio to 5.2 by the end of 2018.

Plus, approximately 99% of Federal Realty’s debt is fixed-rate, which helps shield the company from the impact of a sudden jump in interest rates. Federal Realty also has a strong credit rating of A-, which is solidly investment-grade and helps reduce the company’s cost of capital.

Assuming 5% to 6% annual earnings growth over the next five years, combined with 4% returns from an expanding valuation and its 3.4% dividend yield, total returns are expected to reach or exceed 12% per year.

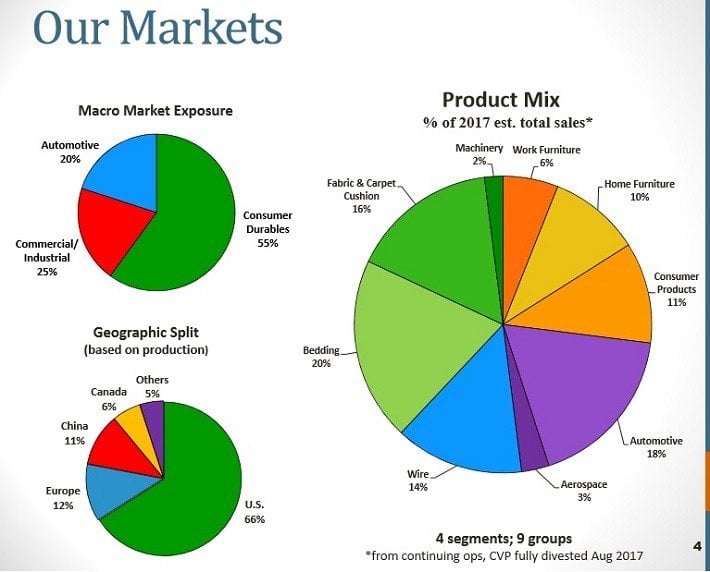

Top Dividend Aristocrat #6: Leggett & Platt Inc. (LEG)

Leggett & Platt has been in business since 1883. Today, the company designs and manufactures a wide range of products found in most homes and automobiles.

Through 130 manufacturing facilities across 19 countries, Leggett & Platt manufactures bedding components, bedding industry machinery, steel wire, adjustable beds, carpet cushioning, and vehicle seat support systems.

Source: Investor Presentation, page 4

Leggett & Platt possesses multiple competitive advantages that are typical of Dividend Aristocrats. It has over 120 manufacturing facilities across the world. In addition, Leggett & Platt has an extensive patent portfolio, which is critical to preserving market share. It has 1,500 patents issued and nearly 1,000 registered trademarks.

Leggett & Platt’s growth will be achieved through organic expansion, as well as acquisitions.

For example, in 2017 Leggett & Platt completed three small acquisitions, including a distributor and installer of Geo Components, a surface critical bent tube manufacturer to support its work furniture segment, and a producer of bonded carpet underlay.

So far in 2018, Leggett & Platt acquired Precision Hydraulics Cylinders, or PHC, a leading global manufacturer of engineered hydraulic cylinders. The acquisition is expected to add 2% to overall sales growth in 2018.

First-quarter revenue increased 7%, while earnings-per-share fell 8%, due to cost inflation. Still, Leggett & Platt expects at least 5% earnings-per-share growth in 2018.

Plus, the stock is significantly undervalued. Leggett & Platt shares trade for a price-to-earnings ratio of 15.4. In the past 10 years, the stock traded for an average price-to-earnings ratio of 19.8. As a result, we believe a return to fair value could add 5% to Leggett & Platt’s annual returns.

In addition to ~5% annual earnings growth and a 3.6% dividend yield, total returns could exceed 13% per year, after including valuation changes.

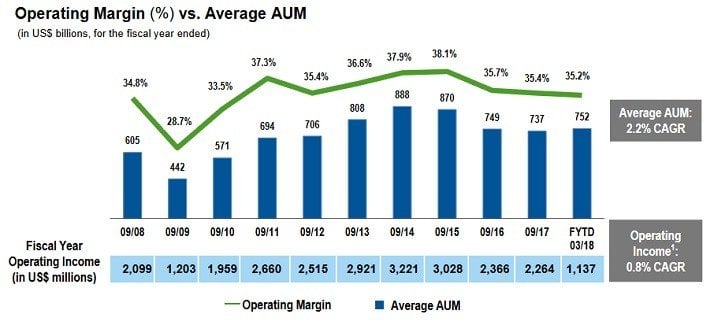

Top Dividend Aristocrat #5: Franklin Resources Inc. (BEN)

Franklin Resources has increased its dividend for 37 years, including a 15% dividend raise on 12/12/17. It has a solid current dividend yield of 2.7%.

Franklin Resources is an investment management company. It manages the Franklin and Templeton families of mutual funds.

The past few years have been difficult for Franklin Resources. Earnings-per-share declined by over 10% in 2015 and 2016. Fortunately, the company bounced back in 2017, with 2% earnings-per-share growth. Franklin Resource’s declining earnings were due to under-performance across multiple of the company’s flagship funds.

Weak performance is a big problem for an asset manager, because it typically results in lower assets under management. When funds do poorly, investors take their money elsewhere.

The good news is, assets under management have returned to growth.

Source: Earnings Presentation, page 10

Despite the difficult operating environment, there are reasons to be optimistic about the company’s long-term growth. The U.S. is an aging population. There are thousands of Baby Boomers retiring every day. Combined with rising life expectancies, there is a great need for investment planning.

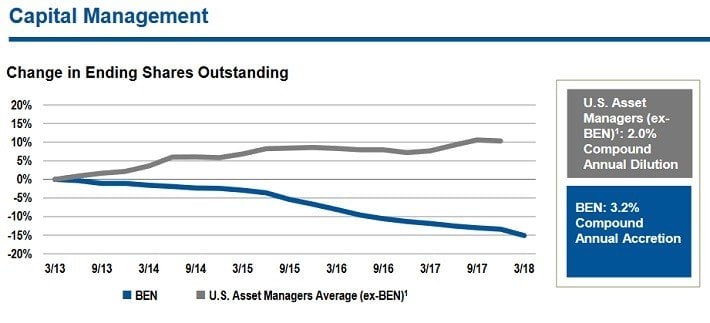

In addition, cost cuts and share repurchases are helping drive an earnings recovery.

Source: Earnings Presentation, page 12

Franklin Resources also distributes cash through dividends. In addition to its 2.7% current yield, on 2/14/18 the company declared a special cash dividend of $3.00 per share.

For 2018, analysts expect the company to generate earnings-per-share of $3.30. Based on this, the stock has a price-to-earnings ratio of 9.9. In the past 10 years, the stock held an average price-to-earnings ratio of 14.5. If it returns to fair value over the next five years, the expansion of the price-to-earnings ratio could add 8% to annual returns.

Meanwhile, Franklin Resources is expected to grow earnings-per-share by 4% per year over the next five years. Therefore, the combination of earnings growth, valuation changes, and dividends, could yield 14% annual returns over the next five years.

Top Dividend Aristocrat #4: AT&T (T)

AT&T is the highest-yielding Dividend Aristocrat. It has a current yield of 6.4%. AT&T is one of 421 stocks with a 5%+ dividend yield in Sure Dividend’s database. You can see all 5%+ yielding stocks here.

AT&T’s first-quarter earnings report disappointed investors. For the 2018 first quarter, AT&T reported revenue of $38.04 billion and earnings-per-share of $0.85. Revenue and earnings-per-share missed analyst estimates by $1.27 billion and $0.02 per share, respectively.

Source: Earnings Presentation, page 3

AT&T saw sales growth of wireless equipment and strategic business services, but this was more than offset by declines in legacy wireline services, domestic video, and wireless service revenues.

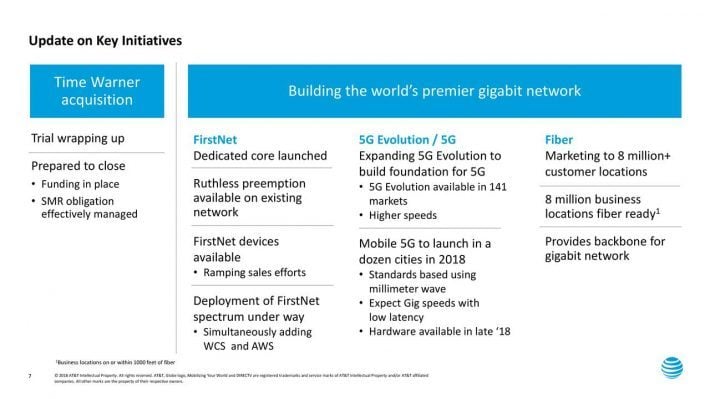

The major catalyst for AT&T moving forward is the pending $85 billion acquisition of Time Warner (TWX), which has a number of strong media properties, including TBS, TNT, HBO, and the Warner Bros. movie studio.

If the Time Warner acquisition receives approval, the combined company would have over 140 million mobile subscribers, and another 45 million video subscribers, worldwide. Along with 5G development, the Time Warner deal is among AT&T’s major growth catalysts.

Source: Earnings Presentation, page 7

However, in November the Department of Justice sued to block the proposed transaction, on antitrust grounds. The main portion of the trail recently concluded, with a final decision expected on 6/12, meaning investors will soon know the fate of the acquisition.

AT&T stock currently trades for a price-to-earnings ratio of just 9.1, compared with an average of 13.4, over the past 10 years. We believe the stock is currently undervalued, and the expanding price-to-earnings ratio could add 8% to shareholder returns each year.

Even if we assume very low earnings growth of 2% per year, AT&T can still provide high returns. We forecast total returns of 16% per year for AT&T, through the combination of an expanding valuation, earnings growth, and dividends.

Top Dividend Aristocrat #3: AbbVie (ABBV)

AbbVie is a research-focused biopharmaceutical company that was spun-off from Abbott Laboratories (ABT) in 2013. AbbVie has become successful, due largely to its flagship drug Humira.

On 4/26/18, AbbVie reported first-quarter financial results. The company delivered excellent growth in both revenues and earnings. Net revenue increased by 18%, while adjusted earnings-per-share rose by more than 40%.

Global Humira sales increased by 11% for the quarter. Going forward, AbbVie will continue to generate growth from Humira, as well as from a robust drug pipeline. Last quarter, Imbruvica revenue increased 38%.

AbbVie also increased full-year guidance, and now expects 38% adjusted earnings-per-share growth in 2018. The company is now expected to generate adjusted earnings-per-share in the range of $7.66 to $7.76 this year.

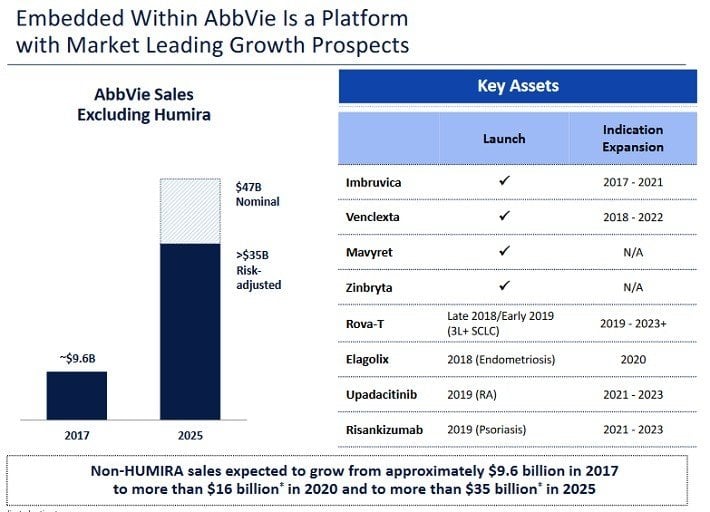

AbbVie management believes Humira will continue growing at a high rate through 2020. After that, the company expects new products to take the lead.

Source: JP Morgan Healthcare Conference, page 15

AbbVie expects non-Humira sales to reach more than $16 billion by 2020, and more than $35 billion by 2025. The company expects to launch 20 new products or indications by 2020. It also is preparing to cut costs, which should result in expanding operating margins by 1% to 2% per year.

AbbVie is currently trading for a price-to-earnings ratio of about 13.1. Since the spin-off from Abbott in 2013, AbbVie has held an average price-to-earnings ratio of 14.2.

Assuming a price-to-earnings ratio of at least 15.0, AbbVie stock could see annual returns boosted by roughly 2.7% per year, from a rising valuation. In addition, we believe that investors can count on annualized earnings-per-share growth of about 10% over full economic cycles.

Combined with the 3.8% dividend yield, AbbVie could generate total returns of approximately 16% to 17% per year over the next five years.

Top Dividend Aristocrat #2: Cardinal Health (CAH)

Cardinal Health is a distributor of medical supplies and pharmaceutical products. The past few years have been rough for Cardinal Health, as the company has struggled with price deflation and rising competition in its core business of pharmaceutical distribution.

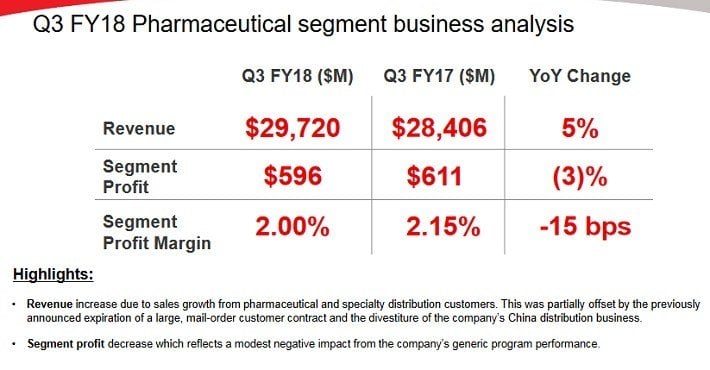

On 5/3/18, Cardinal Health reported mixed fiscal third-quarter. Revenue increased 5.7% from the same quarter a year ago, and beat analyst expectations by $150 million. However, adjusted earnings-per-share of $1.39 declined 9%, and missed expectations by $0.12 per share.

Following a familiar trend, Cardinal Health saw price deflation in the pharmaceutical segment, due to generics, which drove down segment operating profit by 3% last quarter.

Source: Earnings Presentation, page 5

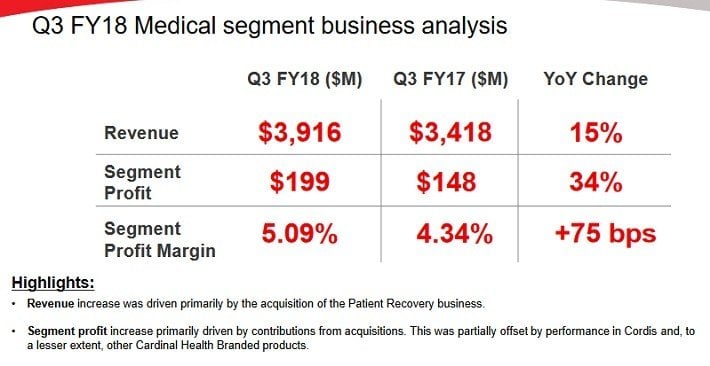

Helping to offset this, was higher volumes, which resulted in 5% revenue growth for the pharmaceutical segment. Meanwhile, the medical segment continued to perform well, with revenue and operating profit growth of 15% and 34%, respectively.

Source: Earnings Presentation, page 6

However, the pharmaceutical segment comprises nearly 90% of Cardinal Health’s total revenue, which limits the impact of the medical segment.

The company now expects adjusted earnings-per-share in a range of $4.85 to $4.95, a significant reduction from previous guidance of $5.25 to $5.50.

Based on 2018 earnings estimates, the stock has a price-to-earnings ratio of 10.8. We estimate a price-to-earnings ratio of 16.8 as fair value, which is equal to its 10-year average.

An expansion of the price-to-earnings ratio could generate 9% annual returns. In addition, Cardinal Health can generate returns through earnings growth and dividends. Assuming 5% annual earnings growth and a 3.6% dividend yield, total returns could reach nearly 18% per year going forward.

Cardinal Health is a time-tested company. It has increased its dividend for 33 years in a row, including a 3% hike on 5/9/18. With a new annualized dividend payout of $1.905 per share, Cardinal Health stock yields 3.6%.

Top Dividend Aristocrat #1: Walgreens Boots Alliance (WBA)

The top Dividend Aristocrat is pharmacy retail giant Walgreens Boots Alliance. Walgreens is the largest retail pharmacy in both the United States and Europe. The company operates approximately 13,200 stores in 11 countries.

It also operates one of the largest global pharmaceutical wholesale and distribution networks, with more than 390 distribution centers that deliver to upwards of 230,000 pharmacies, doctors, health centers, and hospitals each year.

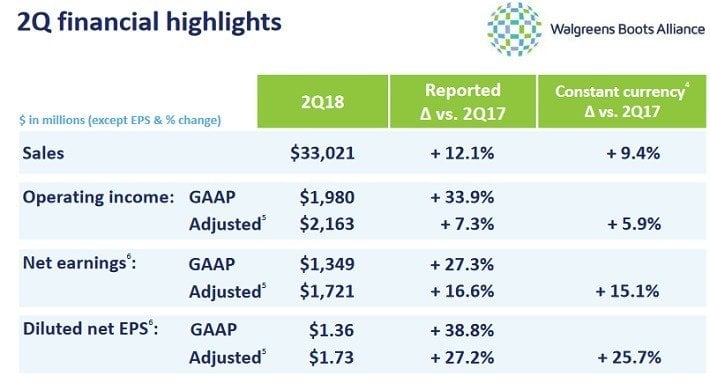

On 3/28/18, Walgreens reported fiscal second-quarter earnings. For the quarter, organic sales increased 9.4%, while adjusted earnings-per-share increased by 26%.

Source: Earnings Presentation, page 7

These were exceptionally strong growth rates for Walgreens, even though the company is fighting through a number of headwinds.

The broader retail environment is extremely challenged right now, particularly for pharmaceutical products, which have seen price deflation in recent years. In addition, the threat of Amazon (AMZN) entering healthcare retail is a constant overhang.

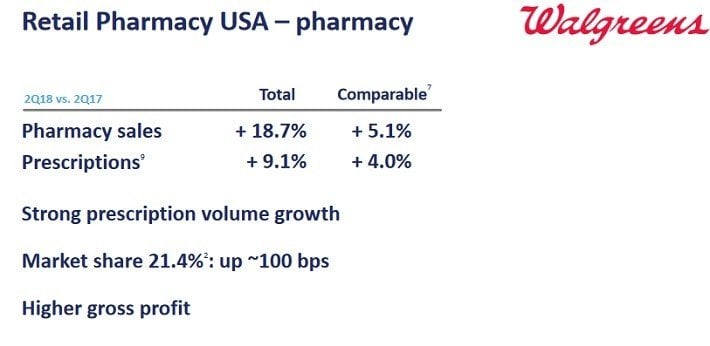

Despite these pressures, Walgreens grew its Retail Pharmacy segment comparable-store sales by 2.4% last quarter. However, comparable retail sales declined by 2.7% for the quarter. Fortunately, the pharmacy side of the business performed extremely well, with 5.1% comparable sales growth and 4.0% comparable prescription growth.

Source: Earnings Presentation, page 10

Along with quarterly results, Walgreens raised full-year earnings guidance. The company now expects adjusted earnings-per-share of $5.85 to $6.05 this year. At the midpoint of guidance, Walgreens expects 17% earnings growth for 2018.

Given the company’s strong track record of growth, we believe that 8%-10% annualized growth in earnings per share is feasible for the foreseeable future. In addition, returns will be boosted by Walgreens’ 2.5% dividend yield, as well as a rising valuation.

Based on the midpoint of 2018 earnings guidance, the stock trades for a price-to-earnings ratio of just 10.6. This is well below our estimate of fair value, which is a price-to-earnings ratio of is 16.7. If the company’s valuation can revert to its historical mean over a time period of 5 years, this will add 9.5% to the company’s annualized returns.

Combined with dividends and earnings growth, Walgreens could produce excellent total returns of 20%+ each year moving forward.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

Article by by Bob Ciura, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.