Spruce Point Capital Management Releases New FOIA Findings And Evidence of Formal Securities Regulatory Inquiry Into Danimer Scientific Inc (NYSE:DNMR)

[soros]Q1 2021 hedge fund letters, conferences and more

Spruce Point is pleased to issue our third, and perhaps most critical, update on Danimer Scientific (NYSE:DNMR, “Danimer” or “the Company”). Please make sure to continue to follow us on Twitter for exclusive insights and updates.

Danimer Scientifi’s Capital Expenditure And Capacity Anomalies

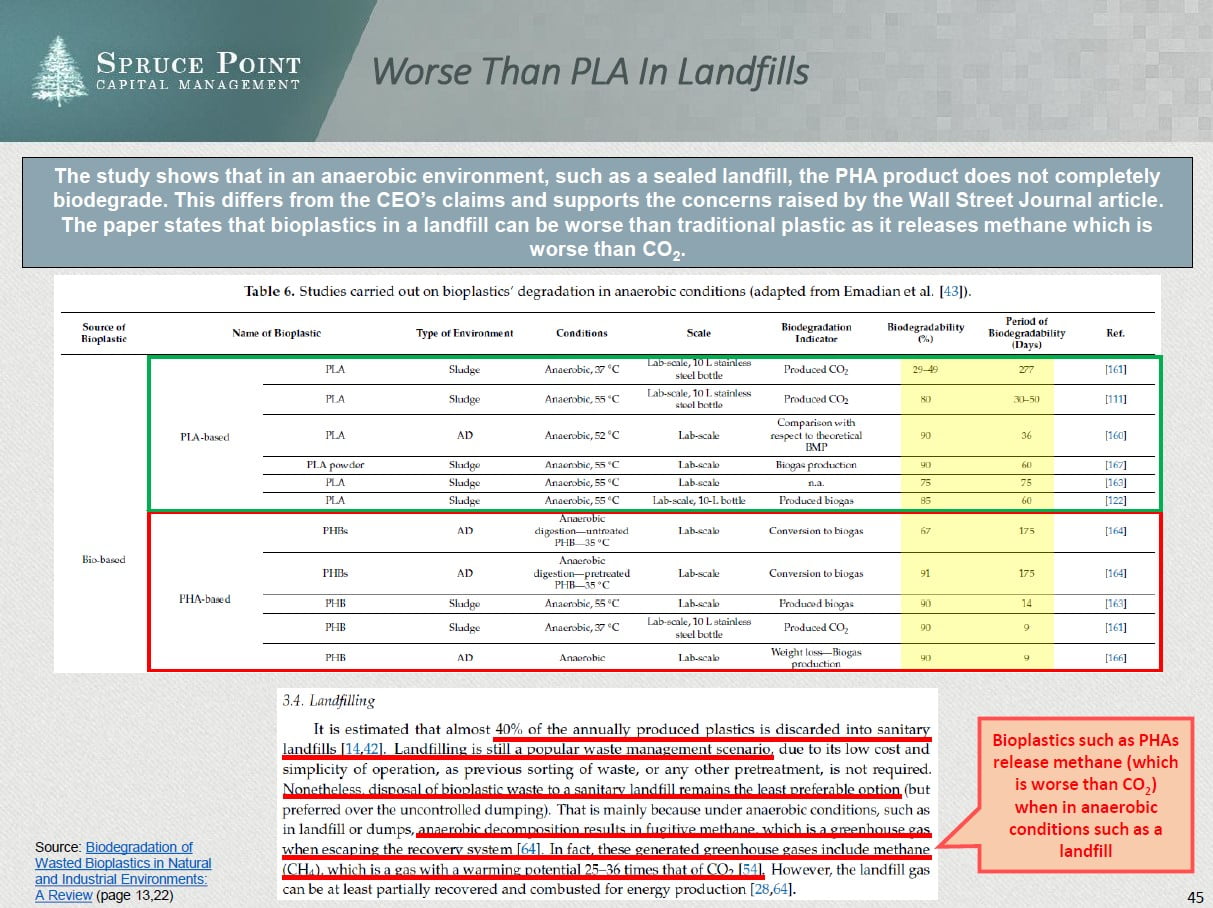

In our initial report and our first follow up report, we warned about Danimer’s capital expenditure and capacity anomalies, as well as history of obscuring failure from current investors. We believe Danimer’s response to our claims to be empty statements backed by little to no evidence that alters our opinion. We felt strongly enough to share our findings with regulators. We are happy to report that the State of Kentucky’s securities regulator, after reviewing our findings, has “opened a formal inquiry” into Danimer.

On Danimer’s recent Q1’21 earnings call, management unexpectedly raised its capital expenditure guidance by 16% – 20%, which reaffirms our belief it suffers from poor financial and operational planning. In addition, CEO Stephen Croskrey made statements about being unable to raise prices further, and the impact of canola oil, that conflict with the Company’s claim of unfettered demand and sold-out capacity. Management is claiming “bottlenecks” in its Kentucky expansion, but we’ll provide evidence that shows broader problems in Georgia with its “greenfield” expansion.

PLA Revenue Reporting

Spruce Point has received an additional Freedom of Information Act (FOIA) response that further calls into question its Georgia capacity utilization and accuracy of its PLA revenue reporting

PLA accounts for approximately 71% of Danimer’s sales and is produced solely in Bainbridge, GA. We now have monthly utility records from its Bainbridge facility which show a material, 70%+ YoY decline in water usage. We believe water is a key input that should highly correlate to the production of PLA. The declines have continued into Q2’2021. On the year end 2020 conference call on March 29, 2021, the CEO stressed the PLA business would grow in 2021. However, this is clearly not true so far. When analyzing Danimer’s reported decline in Q1’2020 PLA revenue vs. the implied decline in Georgia related revenue over the past year, we believe the figures simply do not reconcile. In addition, Danimer’s new disclosures on Q1’2020 PLA revenue now also point to possible revenue misrepresentation.

Analysts price targets and expectations are still too high and should compress. Danimer’s two analysts see an average price target of $48/share. Yet, we now have more evidence of overly optimistic statements made by management around PLA growth (it’s actually declining), and engineering challenges that could delay its greenfield expansion in Georgia. In addition, regulatory risks are now rising due to a formal securities regulatory inquiry. Since coming public at $10/share, we believe Danimer has done nothing but delay timelines, increase capex costs, disclose a material weakness of internal controls, and make statements that we can’t reconcile. We reiterate our belief that shares should trade between $0 and $8.75 per share.