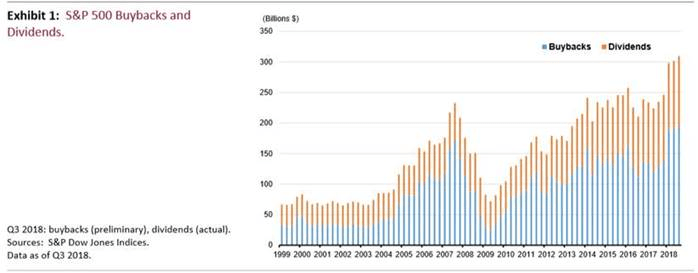

Corporations have never been as generous in returning capital to shareholders via buybacks and dividends than they have been this year. For all of 2018, S&P 500 combined share buybacks and dividends will top $1 trillion for the first time.

However, according to a new report from Bank of America, U.S. Trust, this corporate generosity has not done much to boost equities for a number of reasons, ranging from the one-off nature of returns and the overpowering/ negative effects of Federal Reserve (Fed) tightening and simmering U.S.-Sino trade tensions. And investors have not been overly impressed. Even a sum in excess of $1 trillion can’t buy you love in this market.

Q3 hedge fund letters, conference, scoops etc

Money Can’t Buy You Love

U.S. corporations are on pace to return a record $1.2 trillion to shareholders this year via share buybacks and dividends - a staggering sum that ironically has not done much to support either investor confidence in equities or equities themselves.

According to preliminary figures from the S&P Dow Jones Indices, companies in the S&P 500 spent a combined $309 billion on buybacks and dividends in the third quarter of this year, following robust figures in Q2 ($302 billion) and Q1 ($298 billion). A similar figure is expected in the fourth quarter of the year, which would boost the yearly total in excess of $1 trillion for the first time.

However, notwithstanding the outsized giveback on the part of corporations, both the S&P and Dow Jones Industrial Average are up only marginally for the year. Healthy buybacks and dividends are typically supportive of equities, so what gives this time around?

A number of factors could explain the market disconnect. First, this year’s surge in total shareholder returns is likely to be a one-off, supported by large repatriation inflows that trail off next year, so investors have already started to discount lower levels in 2019. Second, as the cost of capital continues to rise, firms will probably resort to more holding of cash/capital next year, versus doling it back to shareholders via buybacks and dividends. Third, the flip side of returning capital to shareholders is soggy capital investment outlays, with business investment expanding by just an 0.8% annual rate in the third quarter, versus 8.7% in the prior quarter. The fear among investors: In deploying their capital, firms are focused on the short term (buybacks and dividends) as opposed to investing long term to boost output and efficiencies. Finally, even with the record spend on buybacks and dividends, fears around excessive Fed tightening and simmering U.S.-Sino trade tensions have overpowered all other market dynamics in Q4, triggering more market volatility and investor uncertainty.

In the end, while corporations have never been as generous in returning capital to shareholders as they have been this year—spreading the spoils or love, so to speak—investors have not been overly impressed. Even a sum in excess of $1 trillion can’t buy you love in this market.

The named research analysts in these materials certify that: the views expressed in these materials accurately reflect the analysts’ personal opinions about the securities, investments and/or economic subjects discussed and that no part of the analysts’ compensation was is or will be related to any specific views contained in these materials. This publication is designed to provide general information about economics, asset classes and strategies. It is for discussion purposes only since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Always consult with your independent attorney, tax advisor, and investment manager for final recommendations and before changing or implementing any financial strategy.

The information contained herein has been obtained from sources believed to be reliable, but we cannot guarantee its accuracy or completeness. Opinions and estimates expressed herein are as of the date of the report and are subject to change without notice at any time. Equities: Investments in equities are subject to the risks of fluctuating stock prices, which can generate investment losses. Equities have historically been more volatile than alternatives such as fixed income securities. Fixed income securities: Fixed income investments fluctuate in value in response to changes in interest rates. Mortgage-backed securities are subject to credit risk and the risk that the mortgages will be prepaid, so that portfolio management may be faced with replenishing the portfolio in a possibly disadvantageous interest rate environment. Commodities: Commodities investments are highly volatile and are speculative. Commodities prices may be affected by overall market movements, changes in interest rates, and other factors such as weather, disease, embargoes, and international political and economic developments. Alternative Investments such as derivatives, hedge funds, private equity funds, and funds of funds can result in higher return potential but also higher loss potential. Changes in economic conditions or other circumstances may adversely affect your investments. Before you invest in alternative investments, you should consider your overall financial situation, how much money you have to invest, your need for liquidity, and your tolerance for risk.

This report is solely for informational purposes and does not purport to address the financial objectives, situation or specific needs of any individual reader. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. These comments are not necessarily representative of the opinions and views of portfolio managers or of the firm as a whole. Past performance is not a guarantee of future results.

Diversification does not ensure a profit or guarantee against loss.

U.S. Trust, Bank of America Private Wealth Management operates through Bank of America, N.A. and other subsidiaries of Bank of America Corporation. Bank of America N.A., Member FDIC.

Copyright © 2018, Bank of America Corporation. All rights reserved. No portion hereof is to be reproduced or distributed to any unauthorized person without the proprietor's prior written consent.