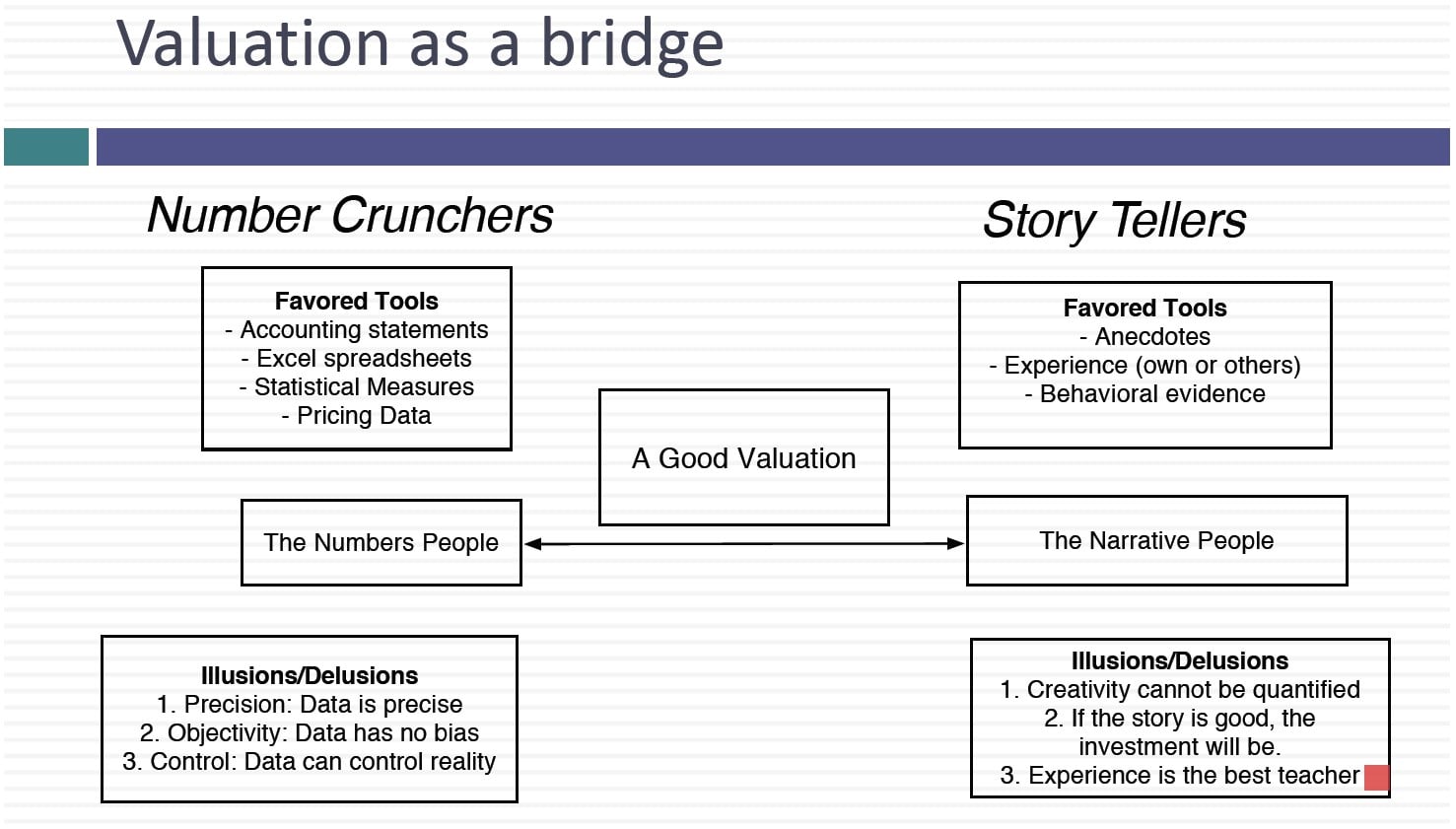

In this session, we spent the bulk of our time talking about why you need stories to hold valuations together, and the process of doing so, using Uber in June 2014 as an example.

Slides: http://www.stern.nyu.edu/

Session 13: Better Value – Stories And Numbers

Q4 hedge fund letters, conference, scoops etc

Transcript

One today we're actually going to you know this is what 13 session of the class how many companies have actually valued in the class. Not one. I've done the cash flow one company discount rate for another company growth rate for a third company. I haven't actually valued and this was supposed to be a valuation class right. You think what a waste of funds sessions. Those 12 sessions are going to be the foundation that's going to allow us to start valuing companies today. So before I start on those valuations let's look at some things that have come up. Any time you do a valuation. First. When you value a publicly traded company you almost always will come up with the value that's different from the press. That's why we have valuation classes. So here's my question. What is your reading of the difference. The first is. You are right and the market is strong. You believe this. You have a serious case of hubris. You got to let it go because this is going to get into serious trouble if you can. You're wrong and the market is right. If you believe this then I'll just tell you what's going to happen the evaluation it's going to go on a journey. You know the destination is going to be the values going to meet the price. And trust me for some of you that's where you're going to end up because you don't trust yourself enough right now. And it's not your fault. I mean that's that's going to come over time. So when you get a value of 15. This is especially true of your value is very different from the price. First reaction is going to be must have screwed up and it's not a bad reaction. But if you let it play out. Then the point devaluation disappears. The third is your Bartrop. You think both Trump. That's really a presumption in investing that we're both wrong but that you are less wrong than the market that's what are hoping and praying for. It's not that you want to be right you just want to be less strong than the market because you can't both be right because then the numbers can't be different.

Oh can you.

What game are you playing when you do discounted cash flow valuation. You're playing the value game what's a market play the pricing game.

It might have the right price given demand and supply in fact. By definition if it is the price it is the right price because that's a market clearing price. And finally none of the above which I think is a cop out position. My point is you are going to value your company. It is going to make you uncomfortable if that value is different from the price don't let that make you go in and do bad things like what. Replace growth rate the analysts estimate because that gives you a better value. Better value in what sense? A value close to the price. Often people define better value as close to the price that must be a better value. A very strange definition of value because there's no point to this class if that's your definition of it. Let's move on. Let's say you value the bank. You write of value of twelve dollars per share using a dividend discount on.

The regulatory capital guys are woken up to the fact that banks are risky and they've said hey we're going to raise the capital requirements or capital ratios for all banks.

How will that affect your value per share increase your value decrease your value. No change in mind.

Dividend discussion moderate. So it should be no fair trade your dividends or your dividends or does it matter what dreg you think down. Why.

Tell me the mechanism that well let's make it about your foot when you have to raise capital ratios. How is it affecting your capacity to pay future dividends.

Remember. Fundamental grotesque ways and I'll give you a clue what was the fundamental growth for this dividend is going to be over time your retention rate short times your return and equity whatever just done by raising your capital requirements of lower due to turn equities. Even though this year's dividend obviously is not changing. I've just lowered your growth potential as a bag with me even if I use a conventional dividend discard model. My value per share for your company will now be lower than it was before. That's why we spent so much time on these in the weeds right. Looking at all these mechanisms because ultimately the weight feeds into value is going to be to one of those mechanisms. Final question you value a high growth company and this is a very very because lots of people including VCs get this wrong. Let's see if we can get this right. You take cash loss equity you just come back at the cost of equity. You arrive at a value for equity of 100 million. The company has 10 million shares outstanding. Today but remember the high gold.