2017 was a year in which markets experienced depressed levels of realised volatility. From an option trader’s point of view 2017 was a selling paradise – a lucrative opportunity to collect favourably priced premiums as volatility drifted steadily lower with time. 2017 saw a gradual climb in major stock markets and related ETFs – a key example is the Dow Jones Industrial Average ETF (DIA), which achieved impressive vol-adjusted (realised vol of 7%) returns that exceeded 28%. Continuing a historical trend, upward stock market moves were accompanied by a steady decline in volatility levels. However, 2017 came to a close with murmurings, and indeed option pricings, of an expected turnaround in the dynamics of market activity for 2018, according to a new report from Goldman Sachs which looks at options pricing and other volatility metrics.

2017 versus 2018 – Biggest Changes in Options pricing Volatility

Overall, the options market has priced in an increased amount of preparation for higher levels of volatility for 2018 – markedly so in certain asset classes. Options pricing on the DJIA are indicating the highest year-on-year percentage increase in volatility. Additionally, ETFs are growing in popularity and options pricing is indicating significantly higher volatility in Index, High Yield, Consumer and Tech stock based ETFs over the coming year.

Likewise, we are seeing volatility priced in at higher levels for options on the S&P 500, consumer and tech stocks and junk bonds. As specific examples, options on the DIA are currently pricing in double the volatility as compared to 2017 and in Consumer Discretionary ETFs, XLY options are being priced with a 73% increase in volatility compared to 2017. In terms of absolute price movement option investors are showing an expectation of an average S&P500 constituent to trade +/-22% over the course of 2018.

2017 versus 2018 – Smallest Changes in Volatility

Options pricing indicates that investors can expect somewhat consistent year-on-year dynamics in price activity from these asset classes in 2018: Gold, Exploration & Production (E&P) and Biotech stocks. However, it is worth noting that despite the expectation of similar levels of volatility, the options market is expecting some absolute price movements of the greatest magnitude in Gold (GDXJ +/-27%), Oil (OIH +/-23%) and E&P Stocks (XOP +/-23%).

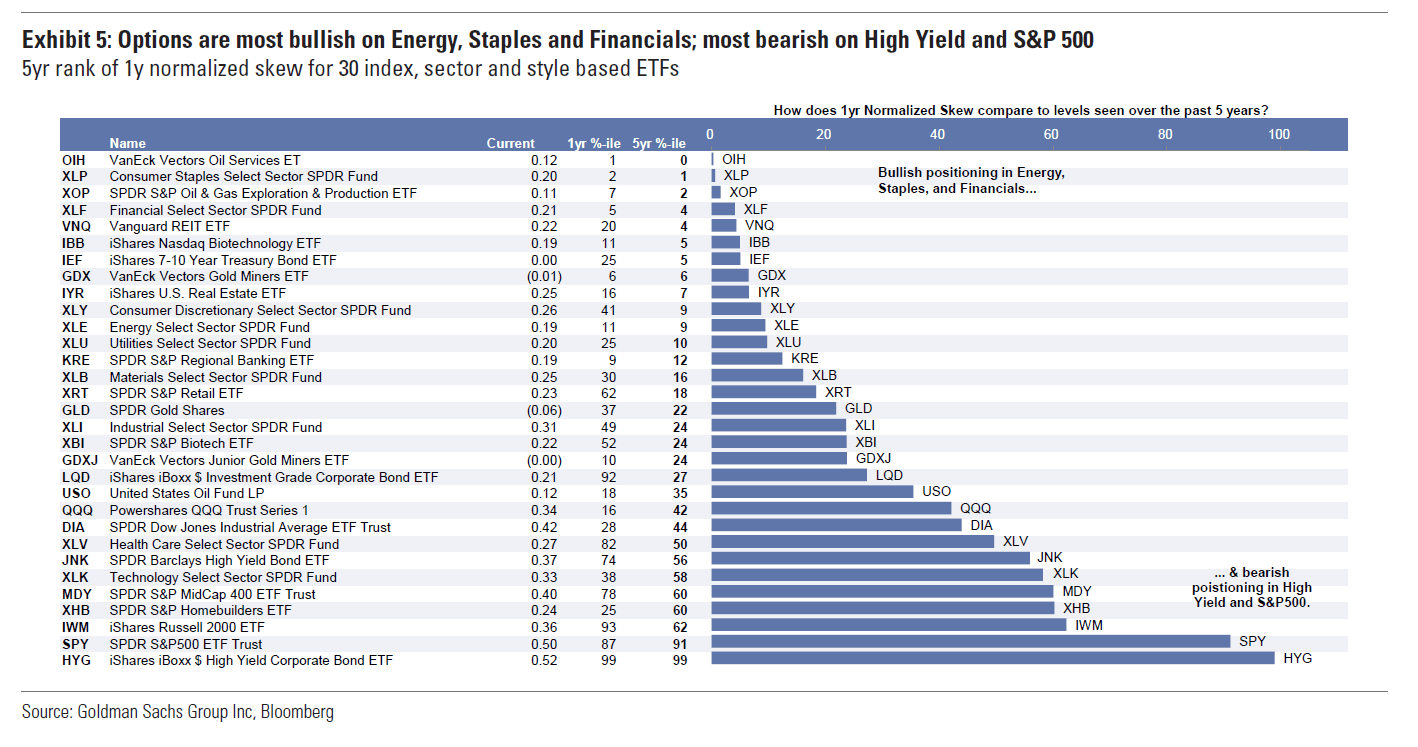

Options Pricing Directional Bias – Bullish Skew

Skew gives us an idea of where we can expect directional sentiment to be over the next year. Looking at options pricing we can see that there are bullish expectations (lower relative skew) for the Energy, Consumer Staples, and Financials sectors. Specifically, especially low premiums are being priced for puts relative to calls in Oil (OIH), Staples (XLP), E&Ps (XOP) and Financials (XLF) – supporting bullish sentiment in these ETFs.

Directional Bias – Bearish Skew

Options pricing also shows bearish sentiment for popular hedging instruments such as S&P500 and HYG. Specifically, we see high premiums in out of the money puts relative to calls in both High Yield (HYG) and S&P500 (SPY) ETFs. We can observe higher relative skew in these typical hedging instruments – most likely a result of investors protecting their portfolios from the low volatility environment of 2017.

>2018 – New Year, New Opportunities?

2017 was a year of steady upward momentum in market pricing and low volatility. A year on and the global market climate and investor sentiment has moved on significantly. Certain political fears have been assuaged and liquidity has been rising - slowly nudging managers towards “risk-on” positioning. Options pricing indicates prudent investors should brace for a more volatile ride in 2018. Meanwhile, the sharpest managers will be preparing to exploit the fact that increased volatility creates expanded capacity for opportunity.