- Icahn Enterprises (NASDAQ:IEP) is an ~$18 billion market cap holding company run by corporate raider and activist investor Carl Icahn, who, along with his son Brett, own approximately 85% of the company.

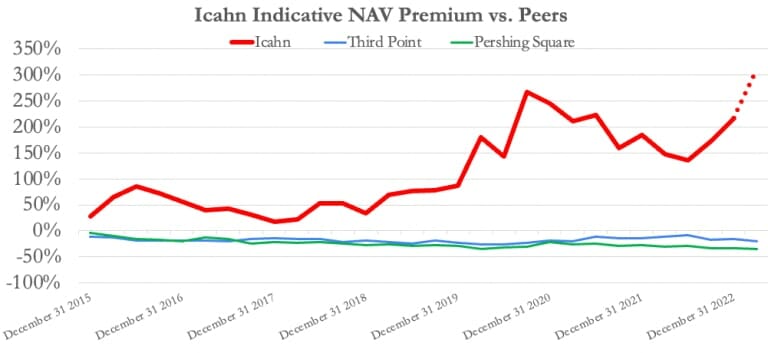

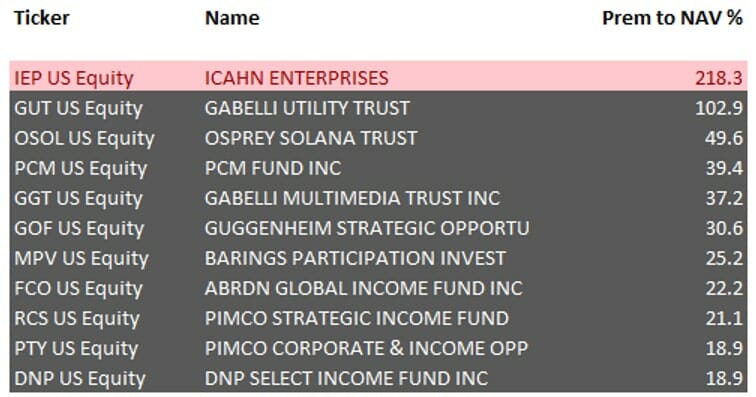

- Our research has found that IEP units are inflated by 75%+ due to 3 key reasons: (1) IEP trades at a 218% premium to its last reported net asset value (NAV), vastly higher than all comparables (2) we’ve uncovered clear evidence of inflated valuation marks for IEP’s less liquid and private assets (3) the company has suffered additional performance losses year to date following its last disclosure.

- Most closed-end holding companies trade around or at a discount to their NAVs. For comparison, vehicles run by other star managers, like Dan Loeb’s Third Point and Bill Ackman’s Pershing Square, trade at discounts of 14% and 35% to NAV, respectively.

- We further compared IEP to all 526 U.S.-based closed end funds (CEFs) in Bloomberg’s database. Icahn Enterprises’ premium to NAV was higher than all of them and more than double the next highest we found.

- A reason for IEP’s extreme premium to NAV, based on a review of retail investor-oriented media, is that average investors are attracted to (a) IEP’s large dividend yield and (b) the prospect of investing alongside Wall Street legend Carl Icahn. Institutional investors have virtually no ownership in IEP.

- Icahn Enterprises’ current dividend yield is ~15.8%, making it the highest dividend yield of any U.S. large cap company by far, with the next closest at ~9.9%.

- As a result of the company’s elevated unit price, its annual dividend rate equates to an absurd 50.5% of last reported indicative net asset value.

- The company’s outlier dividend is made possible (for now) because Carl Icahn owns roughly 85% of IEP and has been largely taking dividends in units (instead of cash), reducing the overall cash outlay required to meet the dividend payment for remaining unitholders.

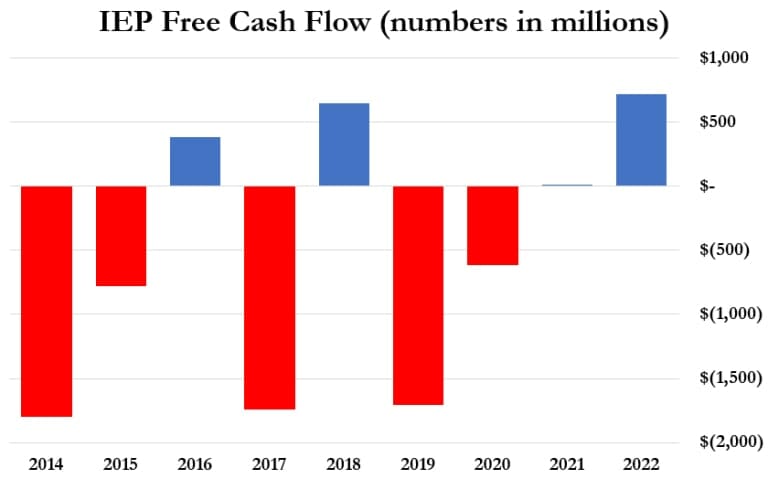

- The dividend is entirely unsupported by IEP’s cash flow and investment performance, which has been negative for years. IEP’s investment portfolio has lost ~53% since 2014. The company’s free cash flow figures show IEP has cumulatively burned ~$4.9 billion over the same period.

- Despite its negative financial performance, IEP has raised its dividend 3 times since 2014. IEP’s most recent dividend increase came in 2019, when it raised quarterly distributions from $1.75 to $2.00 per unit. IEP’s free cash flow was negative $1.7 billion in the same year.

- Given that the investment and operating performance of IEP has burned billions in capital, the company has been forced to support its dividend using regular open market sales of IEP units through at-the-market (ATM) offerings, totaling $1.7 billion since 2019.

- In brief, Icahn has been using money taken in from new investors to pay out dividends to old investors. Such ponzi-like economic structures are sustainable only to the extent that new money is willing to risk being the last one “holding the bag”.

- Supporting this structure is Jefferies, the only large investment bank with research coverage on IEP. It has continuously placed a “buy” rating on IEP units. In one of the worst cases of sell-side research malpractice we’ve seen, Jefferies’ research assumes in all cases, even in its bear case, that IEP’s dividend will be safe “into perpetuity”, despite providing no support for that assumption.

- Since 2019, one bank has run all of IEP’s $1.7 billion in ATM offerings: Jefferies. In essence, Jefferies is luring in retail investors through its research arm under the guise of IEP’s ‘safe’ dividend, while also selling billions in IEP units through its investment banking arm to support the very same dividend.

- Adding to evidence of IEP’s unsustainability, we estimate that IEP’s last reported indicative year-end NAV of $5.6 billion is inflated by at least 22%, due to a combination of overly aggressive marks on IEP’s less liquid/private investments and continued year to date underperformance.

- In one example, IEP owns 90% of a publicly traded meat packaging business that it valued at $243 million at year-end. The company had a market value of only $89 million at the time. In other words, IEP marked the value of its public company equity holdings 204% above the prevailing public market price.

- The mark is even more irregular given that IEP bought over a million shares of the company in December before immediately writing up the value of those shares by ~194% in the same month.

- In another instance, IEP marked its “Automotive Parts” division at $381 million in December 2022. Its key subsidiary declared bankruptcy a month later.

- IEP reported $455 million in “real estate holdings” in its most recent quarter. The reported values in this segment have been remarkably stable for years despite declining net income and despite including (i) the Trump Plaza in Atlantic City, which was razed to the ground in 2021; (ii) a country club that became nearly insolvent in 2020 before ownership reverted to its members in 2021; and (iii) a lack of transparency on other assets and valuations.

- The irregular valuation marks fit a pattern: In January of 2020, UBS dropped coverage of IEP citing a “lack of transparency” following its research showing marks that were “divergent from their public market values”, among other issues.

- Beyond aggressive marks, Icahn’s liquid portfolio has continued to generate losses. Our analysis of Icahn’s latest December 2022 13-F filing indicates that IEP’s long holdings have lost ~$471 million in value year to date, despite the S&P gaining ~9.2% in the same time frame.

- IEP disclosed that its investment fund had a 47% notional short bet in its December 2022 filings. Given the positive market performance, we estimate this short bet has contributed at least a further $272 million in year-to-date losses.

- Overall, we estimate IEP’s current NAV as being closer to $4.4 billion, or 22% lower than its disclosed year-end indicative NAV of $5.6 billion. The analysis suggests that units currently trade at a 310% premium to NAV, with an annual dividend rate of 64% of NAV.

- Tightening matters further, IEP is highly levered, with $5.3 billion in Holdco debt and maturities of $1.1 billion, $1.36 billion, and $1.35 billion due in 2024, 2025, and 2026, respectively.

- IEP’s debt covenants limit the company’s financial flexibility: IEP is not permitted to incur additional indebtedness and is only allowed to refinance old debt. With interest rates having increased, IEP will need to pay significantly higher interest expenses on future refinancings.

- Carl Icahn’s ownership in IEP comprises about 85% of his overall net worth, according to Forbes, giving him limited room to maneuver with his own outside capital. We have assessed that Icahn has little ability or reason to bail out IEP with a capital injection, particularly at such elevated unit prices.

- Further underscoring Icahn’s limited financial flexibility, he has pledged 181.4 million units, ~60% of his IEP holdings, for personal margin loans. Margin loans are a risky form of debt often reliant on high share (or unit) prices.

- Icahn has not disclosed basic metrics around his margin loans like loan to value (LTV), maintenance thresholds, principal amount, or interest rates. We think unitholders deserve this information in order to understand the risk of margin calls should IEP unit prices revert toward NAV, a reality we see as inevitable.

- Given limited financial flexibility and worsening liquidity, we expect Icahn Enterprises will eventually cut or eliminate its dividend entirely, barring a miracle turnaround in investment performance.

- Overall, we think Icahn, a legend of Wall Street, has made a classic mistake of taking on too much leverage in the face of sustained losses: a combination that rarely ends well.

Initial Disclosure: After extensive research, we have taken a short position in units of Icahn Enterprises L.P. (NASDAQ:IEP). This report represents our opinion, and we encourage every reader to do their own due diligence. Please see our full disclaimer at the bottom of the report. Figures current as of market close on April 28, 2023.

Background And Bull Case: Collect A 15.8% Dividend While Investing Alongside Legendary Corporate Raider Carl Icahn

Carl Icahn is an iconic and legendary activist investor with a reputation for taking stakes in companies and then unlocking shareholder value, usually by accusing corporate executives of mismanagement or malfeasance and claiming to act in the interests of regular investors.

“A lot of people die fighting tyranny. The least I can do is vote against it.” – Carl Icahn, Texaco Annual Shareholder Meeting 1988

(Source: Carlicahn.com)

Icahn has used his reputation to fuel Icahn Enterprises, an ~$18 billion market cap NASDAQ-listed investment vehicle offering exposure to Icahn’s personal portfolio, including a mix of public and private companies such as petroleum refiners, auto parts distributors, food packaging companies and real estate. [Pg. 6]

The company began as American Real Estate Partners L.P., a publicly traded master limited partnership formed in 1987. [Pgs. 1-3] In 2007, the name was changed to Icahn Enterprises after it purchased Icahn’s private asset management business for $810 million. [1]

Carl Icahn and his son Brett manage the company and are its largest holders, with 85% of the company. Bulls believe this stake aligns Icahn’s incentives with public investors, as Icahn’s holdings in IEP comprise ~85% of his net worth, based on Forbes data.

Beyond the allure of investing with one of the most well-known names on Wall Street, the other key draw to Icahn Enterprises units has been the company’s consistent $2 per quarter cash dividend, amounting to an annualized yield of about 15.8%, giving IEP the highest dividend yield of any large cap (>$10 billion) company by far, with the next closest being a 9.9% yield, according to FactSet screening.[2]

IEP’s dividend – paid consistently for 71 quarters straight – has been the key allure for IEP’s retail investor base. [Pg. 4] The company has a history of increasing its dividends, with the current dividend of $2.00 per unit per quarter in place since Q1 2019. [Slide 4][3]

Background And Bull Case: Investment Bank Jefferies, The Only Major Sell-Side Firm Covering IEP, Has Consistently Given It A “Buy” Rating and Has Indicated To Retail Investors That The Dividend Is Safe “Into Perpetuity”

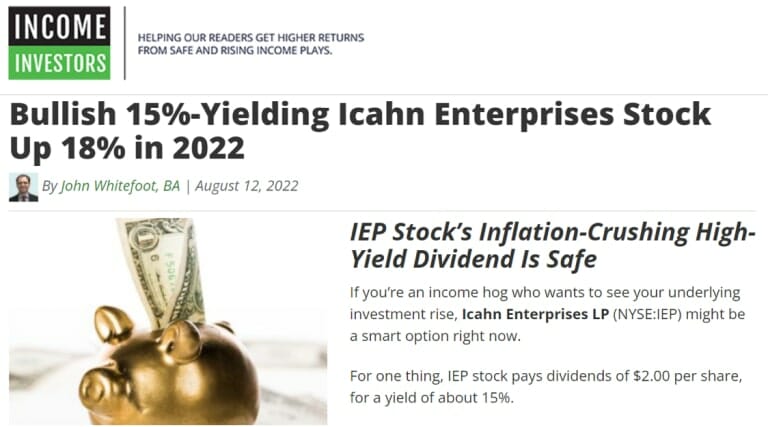

Other Retail Investor-Focused Media Outlets Have Also Focused On IEP’s Dividend Yield And Icahn’s Star Status

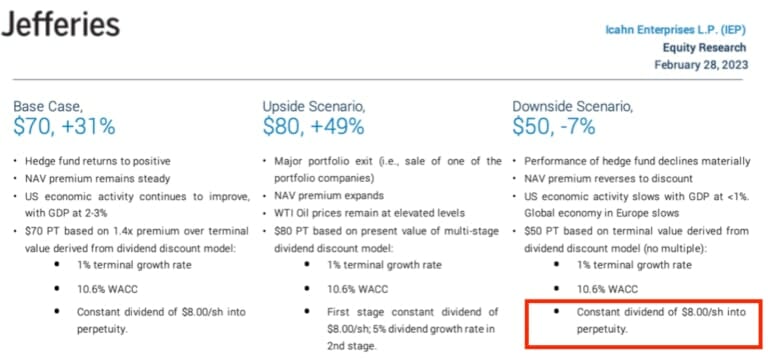

Jefferies, the only large bank covering IEP, has consistently given it a “buy” rating. It reiterated its “buy” rating in a February 2023 fourth quarter recap report.

To arrive at price targets for its “Base Case”, “Upside Scenario” and “Downside Scenario”, the bank assumed in all cases that IEP’s generous dividend would be paid in perpetuity, giving investors the impression that the yield is extremely safe. [1, 2]

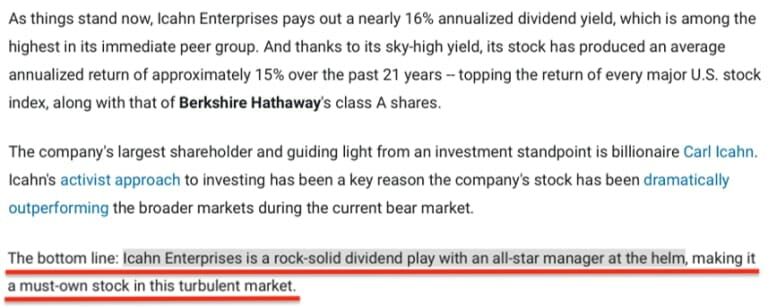

In July 2022, retail investor-focused news outlet Motley Fool wrote that Icahn’s ~16% dividend had “room to grow” and the company was a “rock-solid dividend play”, owing to Icahn’s star status.

A similar October 2022 piece by Motley Fool said that IEP sported “ultra-high dividend yields, fundamentally strong businesses, and a proven ability to generate healthy levels of free cash flows in an uncertain economic environment.”

In an October 2022 article by InvestorPlace, IEP was listed among the three stocks to buy “with your social security increase” because of its 14.8% dividend at the time.

Similar articles have appeared in other retail outlets focused on the safety of the dividend.

Overall, regular investors have been led to believe that IEP’s dividend is safe, despite being abnormally high.

Before examining the sustainability of IEP’s dividend, we first compared the company’s valuation to peers on a fundamental basis.

We assessed Icahn Enterprises compared to similar celebrity investor-controlled investment vehicles, such as Dan Loeb’s Third Point and Bill Ackman’s Pershing Square. Third Point and Pershing Square investment vehicles both trade at discounts to NAV, likely due to the investments being closed-end (i.e. investors can’t redeem) and high fees paid to the sponsors.

By comparison, Icahn’s vehicle, similar to other closed-end funds, does not provide redemptions, and while it may charge lower fees than its peers, Icahn’s vehicle trades at about a 218% premium to its December 2022 reported “indicative net asset value”.[4]

|

|

Icahn Enterprises (NASDAQ: IEP) |

Third Point (LSE: TPOU) |

Pershing Square (OTC:PSHZF) |

|

Net Asset Value |

$5,643,000,000 |

~$700,000,000 |

$10,100,000,000 |

|

NAV per Share (Unit) |

$15.96 |

$23.06 |

$53.88 |

|

Price per Share (Unit) |

$50.82 |

$19.83 |

$34.75 |

|

Premium (discount) to NAV per share (Unit) |

218% |

-14% |

-35% |

(Source: Company Filings 1, 2, 3, 4)

(Source: Company filings. Dotted line represents Hindenburg calculation of YTD IEP premium/NAV estimate)

As a further check, we compared IEP’s premium to NAV against all 526 U.S. based closed end funds (CEFs) and their respective premiums to NAV in Bloomberg’s database.

We found that IEP’s premium to NAV is the highest among every fund on the list and more than twice as high as the next closest fund.[5]

(Source: Hindenburg screenshot of Closed End Funds from Bloomberg. IEP manually added by Hindenburg for comparison, as it is a closed investment vehicle structured as an MLP vs. a CEF)

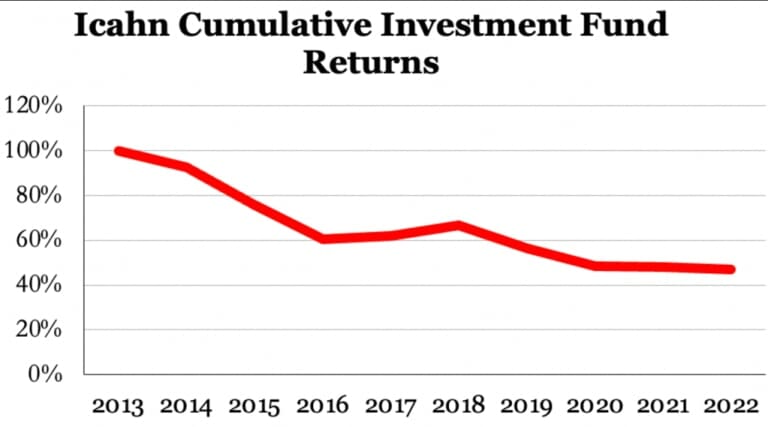

Icahn’s Last Year Of Significant Outperformance Was 2013, Coinciding With The Beginning of His Successful Herbalife Campaign

Icahn’s Investment Portfolio Has Lost 53% Since 2014. This Compares To S&P 500 Performance of 147% In The Same Period

Despite Icahn’s career of heavily publicized activist wins, his recent performance has suffered. Icahn’s last year of significant outperformance was in 2013, when Icahn’s investment fund returned 30.8%, coinciding with the beginning of his successful Herbalife campaign. [Pgs. 1 and 95]

Since 2014, Icahn’s public market investment portfolio, which comprises 45% of IEP’s gross indicative assets (i.e., excluding holding company cash & debt) has lost 53%. In the same period, the S&P returned 147%. [Slide 20]

Icahn’s Dividends Are Mathematically Unsustainable: Since 2014, $1.5 Billion In Cash Dividends Were Paid Despite Negative Free Cash Flow of $4.9 Billion, Owing To Poor Performance

Overall, IEP has posted negative $4.9 billion in free cash flow since 2014, according to FactSet data, fueled by portfolio losses and declines in IEP’s operating investments. [Pg. 46, Pg. 41, Pg. 116]

Despite its extended period of losses and negative cash flow, IEP has paid unitholders cash dividends of almost $1.5 billion during the period. [1,2,3,4,5,6,7,8,9]

During that same time frame, IEP raised its quarterly dividend 3 times, from $1.25/unit in 2013 to $2/unit starting in 2019 (a year when IEP posted negative $1.7 billion in free cash flow.)

In the past 4 years alone, IEP has paid out $980 million in cash dividends, despite cumulatively burning almost $1.6 billion in free cash flow.

The Company Has Supported Its Dividend And Declining Asset Values By Selling $1.7 Billion Through At The Market (ATM) Unit Sales Over The Past 4 Years

The Bookrunner For Unit Sales Is Jefferies, The Sole Sell Side Analyst That Covers IEP, Which Has Assumed In Its Research Notes That IEP’s Dividend Is Safe In Perpetuity

In Short, Icahn Has Been Using Money From New Investors To Pay Out Dividends To Old Investors

With a name as well-known as Icahn, one would think sell side analysts would line up to offer their unique take on publicly traded Icahn Enterprises. Instead, Jefferies is the sole sell side analyst covering the company.

Jefferies analyst Daniel T. Fannon initiated the firm’s research on IEP in April 2013 with a “buy” rating and has touted the company ever since. In Fannon’s February 28, 2023 research note, he placed a $70 price target on Icahn Enterprises, saying:

“IEP represents one of the few public vehicles for investors to access the activist investor style”.

As noted earlier, Jefferies’ research notes assume that Icahn’s dividends will be paid out in perpetuity even in a worst case scenario, despite free cash flow and investment losses that clearly evidence that the dividend is high risk.

To sustain its dividend, IEP has sold units over the last 4 years, totaling over $1.7 billion in at-the-market (ATM) offerings. [Pg. 47, Pg. 98] The sole agent of all of IEP’s offerings has been Jefferies. [1,2,3,4,5]

Once again, the very investment bank selling IEP units to investors is simultaneously drawing in additional retail investors with its “buy” rating and its unsupported assumption that IEP’s dividend is safe forever.[6]

Carl Icahn’s relationship with Jefferies & Co (“Jefferies”) goes back to the corporate raider leveraged buy-out days of the 1980’s. Several articles from the time noted Icahn’s ties to the founder of Jefferies, Boyd Jefferies, who eventually pleaded guilty to two felony counts of securities fraud and resigned from the firm he founded.

Jefferies current CEO, Richard Handler, has maintained a close relationship with Carl Icahn over the years. A 2014 article reported that Icahn helped bail out Jefferies during the global financial crisis. Jefferies now appears to be returning the favor (and collecting fees along the way through its ATM unit sales).

Read the full report here by Hindenburg Research.