Hayden Capital commentary for the second quarter ended June 30, 2018 can be found below

Q2 hedge fund letters, conference, scoops etc

Dear Partners and Friends,

After the fun of last quarter, US markets resumed a slow and steady climb these last few months, even while US-China trade tensions continue to intensify (for reference, the Chinese A-share markets are down almost -17% from their highs this year, but you wouldn’t know it sitting in the US).

In the second quarter of 2018, our portfolio was up +5.7% (net of fees), with our cash balance continuing to decline. Comparatively, the S&P 500 was up +3.4% and the MSCI World index was up +0.3% during the same time period. This brings our annualized return since inception to +15.2% (net of fees), vs. +10.5% for the S&P 500 and +7.6% for the MSCI World index.

Besides our new investment in iQiyi (IQ) at the end of last quarter (see our Q1 2018 letter, and discussed below), we haven’t done much with the portfolio these past few months4. There have been a few small additions / trims to existing positions here and there, but largely our portfolio has remained idle. In order to achieve the magic of compounding, it’s often best to get out of the way, and let our investments do their thing.

Under my most optimistic scenario, I’ll be able to find us a few more great companies at the right prices, to be fully invested within the next few years. At the same time, we’ll continue to upgrade the portfolio, from less attractive investments nearing the end of their business lifecycle, to those with longer and more durable runways ahead.

Lessons From Asia

Currently I’m writing this letter from Asia, where I’ve spent last couple weeks in Shenzhen, Singapore, Jakarta, Seoul, and Hong Kong. Part of the thesis when I originally started Hayden, was that as the world becomes more global, there are lessons to be learned from studying the evolution of business models abroad & applying those case studies to how businesses would develop domestically, as well as vice versa.

Few investors have the opportunity to look across borders, and thus their knowledge base is extremely siloed (for example, “US Small Cap Consumer”). I firmly believe this creates an opportunity for longer-term investors who are willing to break this mold, and be open-minded enough to recognize that sometimes the US business models & practices aren’t always best.

In particular, I’ve spent a lot of time studying China. This isn’t just because of my family background there (although it helps) – but rather because I believe successful business models are a function of evolution & adaptation – aka [survival of the fittest] X [access to capital]. My theory is the business models that can scale globally, and create astronomical wealth in the process, are those that have been battle-tested thoroughly in their domestic markets first. Think of it as a Darwinist process, where out of 1,000 startups, the weakest business models will fail, and only the strong adapt, survive & get funding5. By the time they arrive on the global stage, they’re already the best of the best in their home country, and thus have a strong chance of having evolved the best model for succeeding elsewhere too6. It’s even better if that home country was populous, entrepreneurial, had demanding customers, and formidable competitors who put up a fight7. For this reason, it’s also more likely that the best business models from a >1 Billion population market will be more durable than one from a 5 million population market.

Traditionally, this segment has been dominated by the United States – where a culture of entrepreneurship + relatively large homogenous culture (#3 population globally) + richest economy / domestic market to sell to + willing venture investors to fund startups, have created a perfect environment to nurture future global businesses.

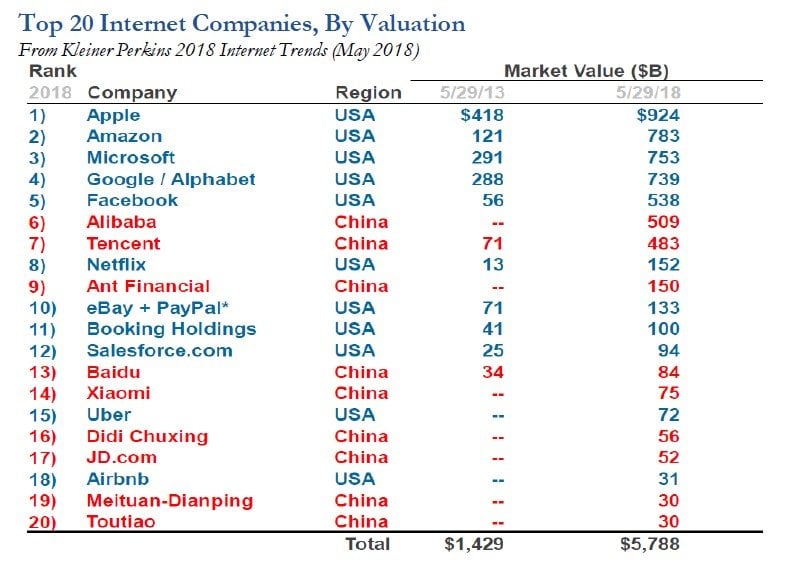

But this is starting to change. On the startup side, the rise of Chinese interest giants like Alibaba and Tencent and others, have created “role models” for wealth creation and have spurred a whole ecosystem of startups in recent years, who are all chasing the “startup dream”.

Similar to the US, China is starting to develop a culture of entrepreneurship / risk-taking + has a large homogeneous culture of 1.4 billion people + is the world’s second largest economy / domestic market + has growing ecosystem of venture capitalists. For instance, one just has to look at the number of co-working and startup incubators that have emerged in cities like Beijing, Shanghai, and Shenzhen to appreciate this trend.

On the funding side, for the first time, Chinese VC investment has surpassed that of North America in Q2 2018 – taking 47% of global VC funding vs 35% for the US. It’s important, since even if you have the heartiest plant species, it still needs to be watered (i.e. VC funding) in the early stages to grow. Granted, a large chunk of this funding was associated with the latest Alipay / Ant Financial round. But even excluding this, China still makes up a sizable 36% of global funding (and growing…).

All of this points towards a rosy outlook for China’s startup scene, and some innovative business models to emerge from the ecosystem in coming years. But don’t get me wrong, it’s still not easy to find great businesses, and there are some crucial nuances for investors (especially those sitting 10,000 miles away) to understand, that differ from the Western tech ecosystems. These are just a few, for illustration…

(Note: I don’t have time to discuss all of them in-depth here, but would be happy to dive deeper into these offline with our clients anytime).

Playing A Game of “Go”

Why would Tencent, a predominately gaming, social media, and payments platform, invest in a bike sharing platform (LINK)? Or what about JD, an e-commerce platform, investing in a real estate business?

The best analogy I’ve heard for these often seemingly puzzling moves, was that these tech conglomerates are playing a game of “Go” (LINK). Often in the game, you may put a piece far away from where the action is in order to stake your territory (for instance, placing a piece in the top left corner of the board where it’s empty, rather than continuing to place pieces in the bottom right, where you’ve been battling it out). The idea is that eventually the entire board will be filled – sooner or later, the battle will get to the other side. It’s better to stake your territory now, regardless of how far-flung it may seem, since it’s easier to defend that section later on, if you already have pieces in play.

This idea is very powerful, especially in China’s tech ecosystem, which is dominated by Tencent & Alibaba (and unlikely to have any upcoming serious competitors). On top of this, there are often exclusivity agreements attached to these investments – if Alibaba invests in a company, typically they will include a clause that the investee can’t raise money from any entities associated with Tencent (and vice versa). In fact, this even applies to investment bankers, with major banks having to choose sides (LINK). In certain cases, it may even make sense to “defensively” invest (i.e. throw away) some money on a firm, just to make sure your competitor can’t use that piece against you later on.

It’s only by understanding this dynamic, that investors can understand the rationale behind these tech conglomerate’s moves. They’re just playing a real-life game of Go.

Ads, Ads, Everywhere

There are ads everywhere in China. Everywhere you turn, there’s shining blinking lights, people yelling at you to coming into their stores… someone is always trying to get your attention. I’m even afraid of stopping to look at menu outside of a restaurant for more than 10 seconds – as I know any longer, and a waitress is going to come out and start giving me the “hard sell” about how great their menu is.

In a country of 1.4 billion people though, this aggressive in-your-face style, is pretty rational. If you aren’t, good luck getting a seat on the metro, buying a house, a table at Starbucks, or convincing someone to choose your restaurant vs. the 20 others on the same block. Every day feels like a competition for resources. To survive, you have to be aggressive (which is often perceived as rude by Westerners, myself included). It’s become in-grained in the culture.

This dynamic is pervasive in the digital sphere too. Turn on the TV, and you’ll see a ton of advertisements / product placement. What may look like a distraction / turn off to Westerners (ie. “why would anyone ever want to watch a show with this many ads or brand sponsorships”) is just the norm to Chinese viewers. For example, I was watching a random Chinese reality TV show, and the entire show was basically an advertisement for Pinduoduo – the logos on the screen, the name tags, the pillows in reality show’s house, where the reality star got his deliveries… the entire show was sponsored by the company8.

As for e-commerce, I remember reading a funny quote a while back, where a JD customer described Amazon’s China website “as bland as plain water”. Instead, he preferred JD’s bright colors, pop-ups, and flashing lights, which made him “feel festive and in the mood to shop” (LINK). What seems obnoxious to those of us in the United States, is “festive” to others.

The point is, there are subtleties to the culture, which may seem counter to Western business models. It’s helpful to be aware of these.

Number of Quality Companies & Culture of Investing

Lastly, something that has surprised me on this trip, is the sheer amount of exposure Asia-based investors have chosen to US stocks. Almost consistently, when asking Singapore or Hong Kong based investors (granted my sample may be biased, since these are mostly concentrated, “quality” investors) what their portfolios look like, something like 90% of it will be in U.S. companies. Why do they choose to invest halfway around the world in a foreign market, when there are a similar number of US public companies as Chinese ones?9

The consistent answer has been that most listed companies in Asia are sh*t10. Disclosure tends to be horrible, mainly because these businesses aren’t run with the public shareholders in mind. For example, one of my clients in Singapore brought up a good point: for instance, many families (especially in small & mid cap land), list their businesses publicly. This isn’t to raise money or grow the business, but rather to have a public “currency” for their ownership stake, so that they can have better standing among their private bankers. By having a publicly traded stock which they can point a definitive value to, the family can use it as collateral to borrow more money for their outside investments, such as real estate.

Investors need to be especially wary of this for investments in conglomerates with “sum of the parts” situations – typically where the holding company’s shares trading at a significant discount to the combined value of listed subsidiaries. It’s more likely for the subsidiary values to be artificially inflated (especially if there’s no logical reason for them to be public in the first place), for alternative reasons other than “unlocking value”.

These types of issues are symptomatic of an immature market, where there’s a lack of an “investing culture”. For instance, less than 7% of Chinese households own stocks, compared to over 55% for the US11. Over 70% of trading volume is dominated by retail investors, which results in wild swings in stock prices. This creates a negative cycle, whereby:

- Few households treating stocks as a place for serious investment (rather than a place for speculation), leads to…

- High volatility, which means…

- Fewer “quality” companies wanting to list on Asian exchanges (they only list if they can’t raise money elsewhere or have alternative motives), which creates…

- A pool of lower quality public companies due to this adverse selection, leading to…

- Few households choosing to invest in stocks, and preferring real estate as the “safer” store of wealth.

Eventually, this cycle will break as the market matures, just as it did in the United States post-1930’s. I’m still trying to figure it out, but it will be interesting development to watch. We’re starting to see some signs of change happening already12.

Portfolio Updates

Amazon (AMZN): A common fear among investors, is that Amazon is getting too big and that its growth with eventually slow due to the law of large numbers. It’s already one of the most valuable companies in the world, and its boxes are omnipresent across much of the United States. At almost $900BN in market cap, it can’t possibly keep growing at 20%+ growth rates for much longer, right?

Obviously, I disagree, as illustrated by our ownership in the company – and especially in today’s world of winner-take-most type business models, where the real winner is the consumer13 (I touched upon this concept in our Q3 2017 Letter, LINK).

Along this vein, I recently came across a few charts from Empirical Research, which I found interesting. It’s nothing ground-breaking, but it does a good job of illustrating Amazon’s ample room to grow ARPU and market share, particularly when viewed versus case studies of its peers (especially Walmart in its glory days).

In terms of ARPU, Amazon is still far behind its archrival Walmart, at ~$800 annually per existing customer vs. Walmart at ~$1,800. The cause of this $1,000 gap, is largely explained by the significant amount of groceries Walmart sells, and explains why this is the next “battleground” for Amazon14.

For example, the average household spends $150 per week on groceries, or ~$60 per person.15 This equates to ~$3,100 per year.

Last August, Amazon bought Whole Foods for $13.7BN, and just 3 months later had already returned Whole Foods sales growth around to 4.4% y/y, vs just 0.6% the quarter before (prior to the deal closing)16. But even while these brick & mortar numbers are impressive, the real benefits of the acquisition lie online.

Today, Walmart is the “top dog” in the brick & mortar grocery market (in 2016, Walmart + Sam’s Club accounted for 21% of total US grocery sales, LINK). But online, the tables have flipped. Reports indicate Amazon is now the leader in the online grocery market, with 18% market share vs. Walmart at just half that (LINK). As of Q2 2018, Amazon already generated $650M ($2.6BN annualized) in online grocery sales17.

Although the industry is relatively nascent, Nielsen predicts online groceries to account for 20% of total grocery sales by 2025, equal to $100BN in annual sales (~9x larger than today, or a 32% CAGR)18.

**

Prior to the Whole Foods acquisition, Walmart certainly had a competitive advantage in the online grocery market. Amazon had tried for years with its Amazon Fresh initiative, with disappointing results. For example, the service first launched in Seattle in 2007 and didn’t roll out to other cities for years as Amazon tinkered (and failed) with the model (LINK).

Cold-chain logistics was a completely different infrastructure than Amazon’s traditional non-perishable market, and more of a challenge than they expected. The nature of groceries is that the items have a relatively low value-to-weight ratio, and even worse, deteriorate in quality / value rather quickly19. From the second the veggies are plucked from the ground, it’s a race against the clock.

For example, in a sign of its struggles with fresh delivery, Amazon even launched a pick-up service in early 2017 (prior to the Whole Foods deal), where customers could order their produce online and pickup via a drive-thru (versus having previously insisted on the benefits of a delivery-only model. By doing so, Amazon seemed to admit they couldn’t solve this portion of the business model).

The only solution was a highly dense network of refrigerated warehouses, which was expensive to build, and hard to justify given it had few synergies with Amazon’s core non-perishable business of selling electronics, laundry detergent, etc.

Then came Whole Foods. By acquiring the company, Amazon gained access to a network of over 400 refrigerated warehouses overnight, located within 10 miles of 80% of US population. More importantly, many Prime members are also customers of Whole Foods (both skew towards higher income households), and thus covers an even higher 95% of Prime households (LINK). By integrating Prime benefits with Whole Foods, Amazon is driving increased loyalty to the Prime & Amazon brands, while gaining a foothold in a rapidly growing market experiencing +30% growth y/y (and thus taking share from Walmart & other competitors as consumers become used to buying groceries online).

**

The potential benefits to Amazon’s financials are significant, if they’re successful. At a $100BN industry by 2025, Amazon would add an additional ~$18BN in revenues by simply maintaining a 20% market share (similar to their current online grocery market share, and also Walmart’s offline market share).

On top of this, case studies from Chinese tech-enabled grocery stores (Hema, for example) have shown that by integrating online & offline, margins can be multiples higher than the industry standard of ~1-2%. This is because close to 50% of volume for each Hema store, is actually placed online, and thus the incremental costs of delivering from an existing (sunk cost) store within 30 minutes are very low (primarily in-store picking & delivery labor).

For example, even the best grocers have a +50% cost of goods20, and industry averages for labor costs are ~10% (LINK). Using this simplistic back-of-envelope calculation, and assuming the store can handle the additional volume, we can see every incremental online order for Whole Foods is very profitable, at ~40% margins vs. the usual ~2%. Even if this analysis isn’t exact, it’s clear that the grocery business is a high operating leverage model, and that any incremental volume via online channels are very profitable.

Additionally, grocery has the added benefit of keeping the Amazon brand “top of mind”, due to the higher frequency of buying groceries (~6x per month, LINK), vs. Prime customers at our estimated ~2.5x per month.

Amazon already has the same square footage of distribution centers as Walmart, which should give it the capacity to continue taking American’s wallet share. Today, Amazon only has ~5% market share in overall US retail sales, but ~20-25% of incremental sales, implying there’s still a large opportunity to bridge that gap. Launching into the grocery vertical will help them do so, and help it fend off the “law of large numbers” to keep growth from plateauing.

The next time you see this at your local Whole Foods, you’ll know why:

iQiyi (IQ): In our last letter, I vaguely talked about a new investment we made toward the end of the first quarter, nicknamed “Undisclosed Position #1” (I’m definitely not getting any points for creativity on that name). I described why despite the company being at an earlier stage than any investment we’ve made before (it’s barely even gross profitable!), I felt it was prudent for us to build a small position in the company (LINK).

Well, we’re done building the position, and I’m happy to say that position is iQiyi (NASDAQ: IQ). At a high-level, what attracts us to the company is a combination of a strong industry tail-wind (as Chinese millennials increasingly shift leisure time to online video streaming) and a content strategy that we believe will provide a more durable moat vs. competitors, by building a core competency around niche, differentiated, original content that is hard to find through mainstream channels.

We’re starting to see early signs of this paying off. Paid subscribers are ~67M today and grew 75% y/y last quarter alone21. At over ~400M “free” monthly users, almost ~50% of China’s internet population is using the platform on a monthly basis22. While I expect the free user base growth to slow (it’s likely close to mature penetration levels), the key will be to convince these users to pay a monthly subscription fee, where they’ll have exclusive access to original content, and reduce the number of (very annoying) ads.

This will be key, as paid subscribers generate 6.5x more revenue than free users. Thus far, paid subscribers as a % of total users have rapidly increased, from only 3% in 2015 (11M paid subs) to ~15% in Q2 2018 (67M paid subs). Some industry analysts expect this to hit 40% by 2022 (~250M paid subs).

In terms of where the capital is going, the vast majority is being spent on content (72% of revenues) and marketing (13% of revenues), with both expenses geared primarily towards attracting paid subs. Our analysis indicates that the company is getting very attractive returns on these investments (for instance, a ~245% return on Rap of China’s season 1), and IRR’s of ~55% on each subscriber it converts.

We bought the shares at an average price of ~$17 in the weeks after the IPO, at a valuation of ~2.7x 2018E sales. It’s hard to know exactly where margins will shake out when the industry matures, but traditional media distributors have averaged ~20 - 30% margins and Netflix at 12.5% margins. As an example of the scalability of the business model, we estimate iQiyi’s incremental margins to be +80% for each new subscriber it signs on. At $17, it was implying a ~20x “normalized margin” multiple (or lower) for a business I expect to grow +40% a year.

Note, the stock is already up ~100% since our original purchase, and shares remain volatile. There’s fears around competition from Tencent and the ability of the business to survive a prolonged content war (which obviously I believe they will). During this time period, we haven’t sold a single share, and will likely add at the appropriate levels, and the company continues to execute (and thus de-risking the thesis).

A few weeks ago, I presented the company at the ValueX conference in Vail, Colorado. While I didn’t have time to dive into all the details of the thesis (I only had 15 minutes), I think the deck hits the key points of the investment, and illustrates the aspects of the business that I find attractive. Anyone who’s interested, can find the presentation here (LINK). Our investors can also reach out to me personally, and I’d be more than happy to walk through the case offline.

Conclusion

I’m constantly surprised at how many people actually read these letters, and even more surprising, in how many corners of the globe. Over the last few weeks, whether it’s Shenzhen, Hong Kong, Singapore, or Seoul, I’ve met fellow investors who are familiar with Hayden’s work and have had great conversations around local business models / trends, who are the disrupters in those markets, understanding what my misconceptions are around the country, and what local investors think are the biggest opportunities23.

I’m not writing this to brag or say Hayden Capital is ‘da shit (we’re not - and are still tiny compared to the rest of the investment world). Rather I mention it, because it’s an interesting case study of how amazing quick

information spreads nowadays (thanks to the internet), and how platforms have commoditized & democratized the way it’s spread. On top of this, as investors, we need to constantly search for our blind spots – and as business models and capital flows increasingly cross borders, filling in this knowledge gap requires us to travel globally as well.

By contrast, I recently met an investor in Hong Kong, who made some extraordinary returns investing early with several of the legendary hedge funds we know today. The only way he found these managers 30 years ago, and halfway around the world, was by going to the local library and flipping through reports (something which most people could have done, but probably didn’t take the time to, and thus giving a significant advantage vs his peers) 24.

Nowadays, we have Twitter, dedicated investing websites, FaceTime, WeChat groups, email, among other platforms. When a fund publishes a research report, it gets read in every continent at the same time. For example, Bloomberg recently ran a profile about our last quarter’s letter – which the reporter discovered simply through word of mouth (LINK).

Along these lines, an investor’s competitive advantage is no longer around “discovery” / turning over the

right rock. Every single rock has been turned over before, and looked at numerous times. Rather, what sets investors apart is having the right frameworks to be able to recognize something “great” when you see it (see our Q1 2018 Letter, LINK). Having a toolbox of “mental models” is more important today than ever.

Similarly, the good news is if you’re an entrepreneur, investment manager, or public company, is this level of transparency means you can spend more time on your core product (focusing on adding the highest value to your customers), and if you do that well, investors or new customers will naturally find you25. The bottleneck is no longer on “discovery” / worrying no one will find your amazing product.

Today, the better your product, the easier it is to convince other people to buy, due to ranking higher on peer reviews (think CNET, Amazon, Consumer Reports, etc), and unlimited shelf space online. New customer acquisition costs become lower, plus the product becomes better for existing customers, encouraging them to repurchase in the future. It’s a beautiful virtuous cycle.

I mention this, because when I started Hayden, I had a vague notion of “if we do good work, add value to our clients, and put it on the internet, people will appreciate it & eventually find us.” I wanted to create the “beautiful cycle” mentioned above, but in the investing field. Despite the still early stage of Hayden Capital as a firm (our business thesis isn’t proven yet), so far my own expectations have been exceeded, and I have to thank our partners, fellow managers, and anyone who has read our material for that.

We continue to be open to new, thoughtful partners who appreciate our investment approach. I’ve always prided myself on trying to operate Hayden Capital the way I would want it to be done if I were an outside

investor (because I am). If we can simply curate a group of such similar-minded individuals, over the life of our firm, I’ll consider Hayden a success. If you know someone who you think would be a good fit for our strategy and Hayden Capital, please have them reach out.

**

This semester, I will also be looking for an intern to join for the fall term. Preferably, the intern would have some investing experience and an international background, with an interest in our particular style of

investing. But most importantly, I’m looking for a deep thinker & voracious reader, who has an insatiable curiosity about how different frameworks & trends fit together, and ultimately with the goal of understanding how the world works. If you know a rare individual like that, please send them my way.

This week, I will also be giving a seminar at the Hong Kong Society of Financial Analysts (the local Hong Kong CFA chapter). It’d be great to have you join and meet in person, if you’re in the area (LINK).

Last quarter, I ended our letter with this lovely table. It’s such an important concept though, that I’ve decided you can bear with looking at it one more time. More importantly, it’s not just money that compounds – it’s knowledge, relationships, physical health, personal networks, evolution / innovation… many aspects of life can be explained by this simple concept.

As always, please reach out if there is anything I can help with. You probably know which coffeeshop to find me at by now.

Sincerely,

Fred Liu, CFA

Managing Partner