Apis Capital Flagship Fund commentary for the fourth quarter and the year ended December 31, 2020.

Q3 2020 hedge fund letters, conferences and more

Dear Partners,

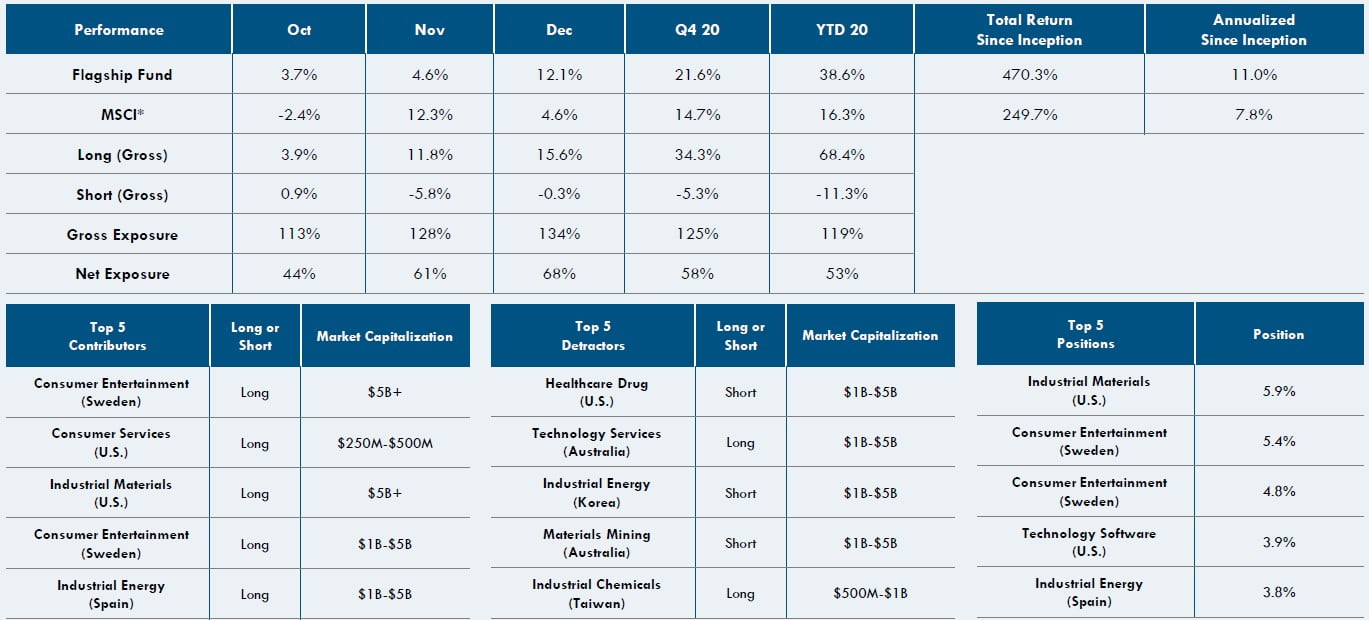

Apis Capital Flagship Fund was up 21.6% net in 4Q20. During the past quarter, our longs contributed 34.3% (gross), while our shorts detracted 5.3% (gross). At the end of December, Apis Capital Flagship Fund was approximately 68% net long with the portfolio 101% long and 33% short.

Apis Capital Flagship Fund: Performance Overview (Gross Returns)

2020 was a year to expect the unexpected and we humbly admit being surprised, not only by the market’s general strength under the circumstances, but also our ability to successfully navigate it. In the end, 2020 returns were the second best in our 17-year history with December 2020 our single-best month. The Apis Capital Flagship Fund benefited (finally!) from emerging tailwinds for small-capitalization companies as well as renewed interested in ex-U.S. and emerging markets which can hopefully sustain, given years (even decades) of relative underperformance.

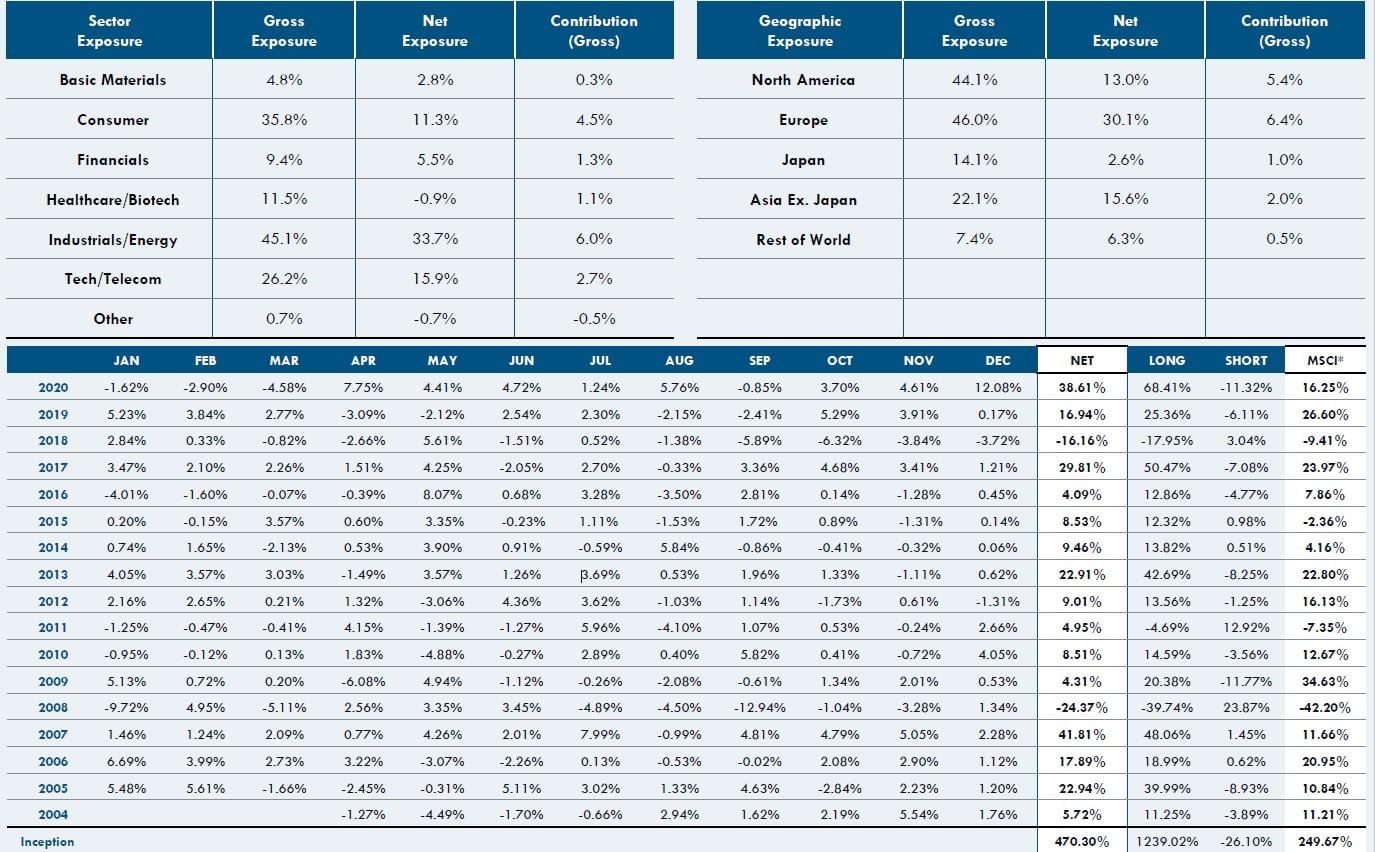

At the macro level, our best returns came from the Industrials sector (22.9% contribution), followed by Consumer (17.1%) which aligns with our long-term success in those sectors. An outlier this year, however, is the regional performance contribution from Europe, which added 19.6% to returns compared with North American and Asia (including Japan) which added 13.7% and 14.4%, respectively. 2020 marks the first time Europe has led the way.

As self-described “stock-pickers,” the most gratifying aspect of 2020 was the strength and breadth of positive contributors. Long side stock performance was outstanding, generating in excess of 68% to returns. Top names such as West Holdings (Japan) and Kambi (Sweden) each contributed more than 5.0%, but in sum there were 26 names that added more than 1.0% to returns versus 4 names that detracted over 1.0%, and all these were crystalized in the Q1 crash. While there is nothing wrong with owning Tesla or other Unicorns if that is your thing, we find it oddly satisfying there isn’t a winner in the Fund that is a household name.

For the quarter, there were 12 holdings that each added over 1.0% to returns, led by Darling Ingredients in the U.S. (2.6%) and Evolution Holdings in Sweden (2.1%). Other winners included Rush Street Interactive, Myokardia, Flatex, and Global Wafers to name just a few. Part of success is avoiding failures and the largest quarterly loser was Pexip Holding (Norway) which only detracted about 0.3%.

On the short side, the 4th quarter was better, with notable winners stemming losses. The top short was Penumbra, which fell on reports that the company misled investors about its flagship products for treating ischemic stroke. Another notable winner, Beyond Meat, declined on weak Q3 results. With 3% Q3 growth valued at 20x sales for a food product company that will never achieve high margins, we think this Unicorn has considerably more distance to fall.

Portfolio Outlook And Positioning

The tendency for a “bad” year to follow an especially strong one tempers our enthusiasm for markets. Social media is rife with retail investors discussing what they are going to do with their “stimmy” (stimulus checks). Many are looking to buy more Tesla or Bitcoin. It’s insane, but it’s the world we live in currently. There are certainly many parallels with the Internet bubble of 2000 and the most heartening thing we can draw from that experience is that when the bubble pops (and it may not be this year), it should discriminate between real companies and pretenders. We are building lists of names that we believe have the potential to decline in value by 80% or more. As ever, we remain pragmatic and have no delusions of calling a top in the market but are prepared to be more active when the mood shifts. On the other side, especially in the small-cap area, we have plenty of durable, high-growth businesses on cheap valuations. Single-digit P/E multiples, strong growth and good balance sheets are plentiful in our segment of the market. Below we highlight several names we believe should perform well in the coming year.

Investment Highlights

Cornerstone Building Brands, Inc. (U.S. – $1.5bn market cap)

The homebuilding market is currently having a sharp resurgence, with prices across the nation up approximately 8% year-on-year; a level that was last touched briefly in 2013/2014 but hasn’t been sustained since prior to the housing crisis. New home building, remodeling and home sales are all very strong. As a result, the inputs to homebuilding are seeing meaningful inflation for the first time in a decade. Products ranging from doors to faucets, roofing, lumber, flooring, siding, windows and insulation are all up 5-10% or more. Demand isn’t the only driver behind this growth; supply has also been reduced by COVID-19 as labor is in short supply for manufacturing these items. While 5-10% may not sound too dramatic, consider that a company with a low, single-digit income margin could see its profits double if these price increases pass to the bottom line.

Cornerstone Building is one such company we own. Cornerstone specializes in homebuilding products where they are the dominant manufacturer in the U.S. of both vinyl siding and windows as well as corrugated steel warehouses. The company was formed through a merger in 2019 and has been quietly focused on increasing its margins and rationalizing the business. They recently posted their sixth quarter of margin expansion, a herculean feat given this past year’s economy. The stock is on 15x current earnings, but these earnings don’t yet reflect the recently announced price increases which could cut this multiple in half (or even less ). Cornerstone is a cyclical business which will naturally trade at a low multiple near the peak of its cycle, however, this cycle looks like it’s much closer to the beginning than the end. We see the potential for about 90% upside in the shares from current levels.

Impala Platinum Holdings, Ltd. (South Africa – $10bn market cap)

Most investors have never heard of the most valuable metal in the world at the moment, rhodium. Rhodium currently trades at nearly $19,000 per ounce, or 10x the price of gold. Rhodium is in severe shortage because it is used in catalytic converters for automobiles. Passing hot exhaust through a honeycomb filter coated with minute amounts of rhodium along with its sister metals of palladium and platinum causes toxic gas, notably nitrogen oxide, to separate into its much safer constituents of nitrogen and oxygen/water. Importantly, there are no substitutes for using these metals and every major country including China is ratcheting up their auto emissions requirements, thereby driving demand increases which far outstrip supply. Supply is particularly constrained as the mines are largely confined to two geographic sources: one in Russia and the other in South Africa where an oligopoly of just 4-5 companies controls most of the production.

The third largest of these producers is Impala, which is focused on a portfolio of mines in South Africa where they produce significant amounts of rhodium, palladium and platinum. Platinum has struggled to keep up with palladium and rhodium as it is primarily used in recently shunned diesel engines, however, palladium and rhodium have seen their prices rise 100% to many times that over the past few years. Impala’s share price has risen, but still reflects significant skepticism around the sustainability of these metals’ prices with the shares trading at just 3x EBITDA and 5x earnings. We think Impala is an “ugly” mining company sitting at the heart of a “green” agenda being aggressively embraced around the world. This trend is not going to be a traditionally shaped boom-bust cycle, but it could sustain much longer than the market is giving it credit for. With no debt and enormous cash flow generation, we see Impala’s shares rising 50-100% from current levels.

Swancor Holding Co., Ltd. (Taiwan – $500mm market cap)

Swancor in Taiwan, which we highlighted in last quarter’s letter, offers attractive growth prospects as one of the beneficiaries of the upcoming expansion in the offshore wind market, yet at a much more reasonable valuation than other, more widely recognized “green” energy stocks. Swancor generates more than 75% of its revenues from resins and carbon fiber that are used in offshore wind turbines and their blades. The company had early success supplying to Chinese wind turbine producers, but had not broken into the major international producers until recently. Helped by localization requirements in the burgeoning Taiwanese offshore wind market, Swancor signed its first supply deals with major turbine players Siemens Gamesa and MHI Vestas in 2018 and 2019, respectively, which are now starting to bear fruit. The Taiwanese market will be one of the fastest growing offshore wind markets in the next 10 years, growing installed capacity by a 55% CAGR and providing Swancor with plenty of runway for growth. In fact, Swancor should also benefit from the growth in other Asian markets like Japan and South Korea which are forecasted to expand offshore installed capacity by 10 year CAGRs of 81% and 50% respectively, compared to a CAGR of just 15% in Europe over the same time frame. Thanks to Swancor’s new customer wins and exposure to the fast-growing Taiwanese market, we forecast core earnings to grow by approximately 50% in 2021. This puts the stock on a very reasonable 15x P/E, especially compared to other renewable energy suppliers like TPI Composites (TPIC US) on 37x, CS Wind in Korea on 38x, or Gurit (GUR SW) on 27x.

Maire Tecnimont S.p.A. (Italy – €630mm market cap)

Maire Tecnimont is a well-known EPC (engineering, procurement, and construction) company based in Italy that helps its customers design and manufacture different types of production facilities across the world. Historically focused on hydrocarbon projects (oil & gas, petrochemicals, and fertilizers), it has recently been expanding into the renewable segment with projects in hydrogen, wind, railway, etc. In particular, it is starting to work on exciting projects in green hydrogen, or hydrogen produced via electrolysis.

Because of COVID-19, its working capital has been stretched and shares have become oversold. It now trades at 2x its peak free cash flow, or 5.4x trailing EPS. Interestingly, management has guided its green business to produce €50mm of EBITDA by 2023, and if you applied a 10x multiple to that (there is precedent for a much higher multiple on a green energy business, by the way!), you would get €500mm in equity value. That’s nearly the market cap of the entire company today. The core business is expected to inflect with Q4 results, and we view the green business like a “free option,” which could double the shares by itself.

Neowiz Corp. (South Korea – KW500bn market cap)

Neowiz is a Korean game developer and publisher that has been around since 1997 and was started by former employees of Nexon. Most of its sales come from popular casual games in Korea, such as Pmang Poker and Pmang Slots, but it is also one of the most well-respected publishers of 3rd party games in Japan. Neowiz is by far the cheapest stock among its gaming peers at 9x Street EPS (8x ex-cash), despite growing at an impressive 15-20% clip. Part of its valuation discount is due to its historical focus on casual games and recent loss of a publishing deal in Japan, but we think things are about to change.

The Street is modeling revenue growth deceleration in Q4 and 2021, but this is far too conservative in our opinion. Neowiz is about to release a very well-reviewed self-developed game called Bless Unleashed and has two large games it will be publishing in Japan (to replace the one it lost). Not to mention its large casual games business is getting a boost from recent deregulation in Korea and continued COVID-19 lockdowns. We anticipate these catalysts will create both better-than-expected results and multiple expansion over the next few quarters with rock-bottom valuation, creating an attractive risk-reward scenario.

Firm Update

During the 4th quarter, the firm onboarded and implemented Enfusion, which will strengthen our current infrastructure and operational processes by providing enhanced institutional methods to combine our order management & execution, portfolio management, real-time risk monitoring, and a general accounting ledger into a fully integrated, cloud-based system. We will also be using the Enfusion Managed Services offering to outsource and further support our middle- and back-office functionalities.

In addition to these updates, we continue to focus on expanding and diversifying our firm’s overall asset base by leveraging the long-term alpha generated for our partners. More specifically, we’ll seek to strengthen our investor mix by introducing new institutional clients to our successfully launched Global Discovery long-only Fund, which ended its inaugural year up in excess of +70% net.

As always, we encourage your questions and comments, so please do not hesitate to call our team here at Apis or Will Dombrowski at +1.203.409.6301.

Sincerely,

Daniel Barker

Portfolio Manager & Managing Member

Eric Almeraz

Director of Research & Managing Member

Apis Capital Flagship Fund