Apis Capital Deep Value Fund commentary for the second quarter ended June 30, 2021.

Q2 2021 hedge fund letters, conferences and more

Dear Partners,

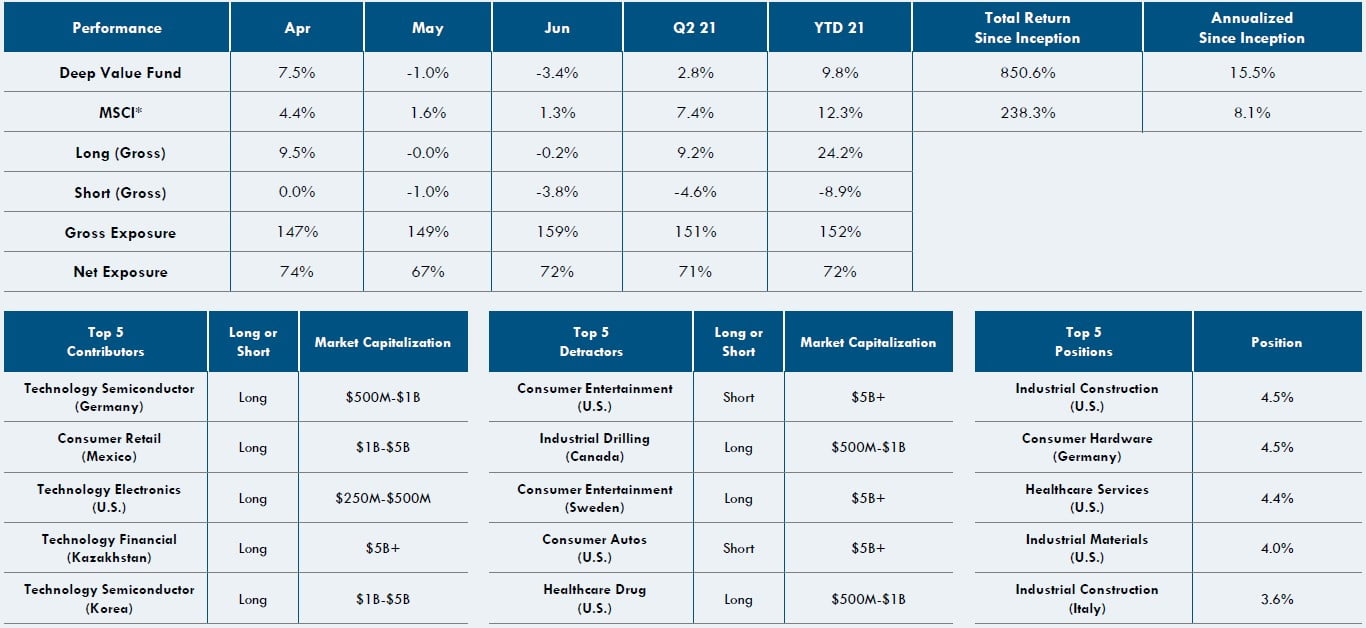

Apis Capital Deep Value Fund was up 2.8% net in Q2 2021. During the past quarter, our longs contributed 9.2% (gross), while our shorts detracted 4.6% (gross). At the end of June, the Fund was approximately 72% net long with the portfolio 115% long and 43% short.

Performance Overview (Gross Returns)

The second quarter was characterized by several feuds playing out in the market. The retail embrace of SPACs and meme stocks continued in earnest. While we were somewhat impacted on the short side, we maintain a handful of small positions. The long side was characterized by strong performances from commodity-related names offset by a pullback from other companies in our portfolio that had performed strongly last year. In general, the market is working out whether to favor growth or value stocks. As we have discussed in previous letters, our framework allows for both growth and value; moreover, we often find both elements in the same stock.

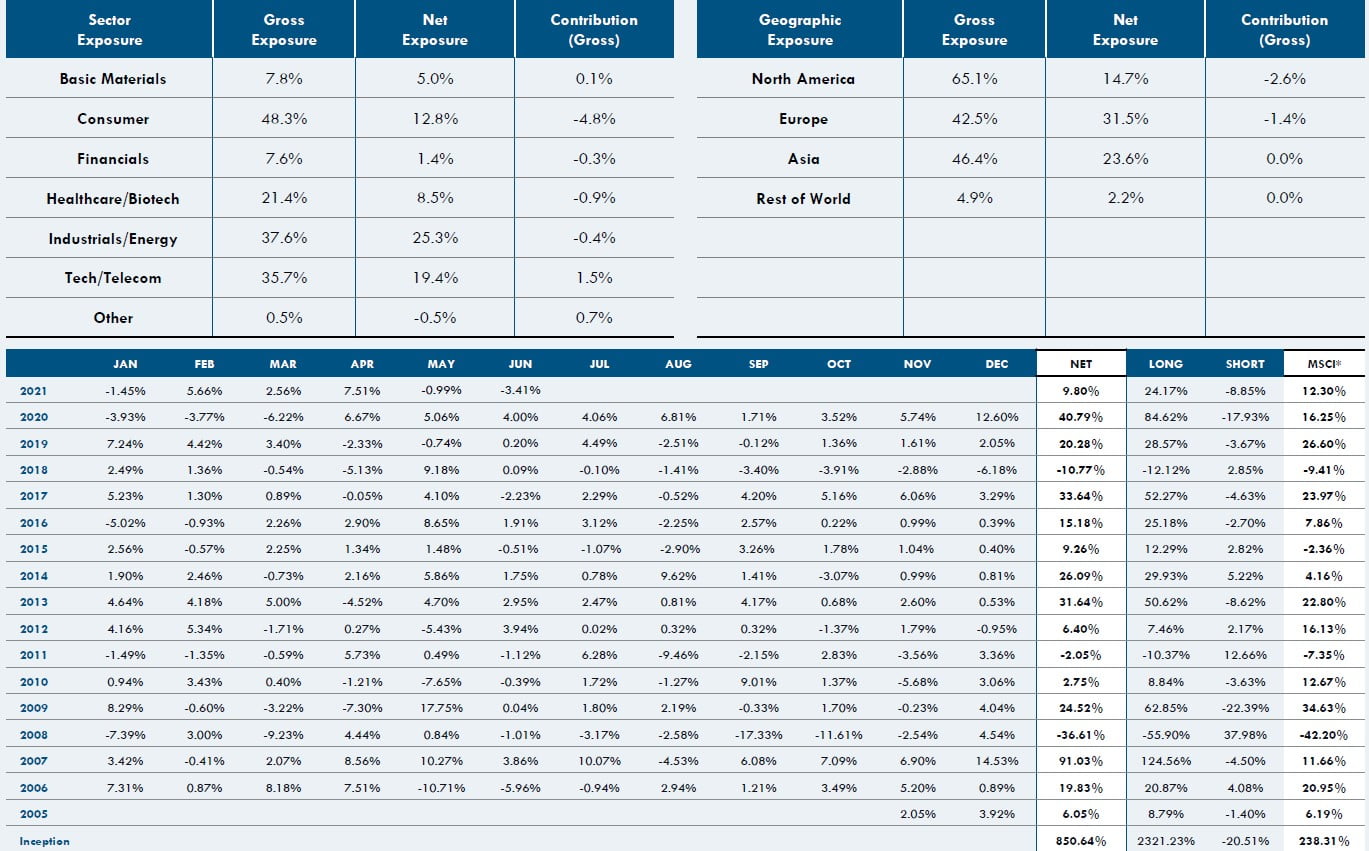

Regionally, Asia contributed the largest gains followed by Europe. North America was a slight loss as long gains were offset by shorts. By sector, Cyclicals contributed the lion’s share of gains adding over 4.6% to performance, while the remaining sectors largely offset each other.

Notable winners on the long side include Xpel which delivered just over 1.2% and produces a protective coating for automotive paint. HEG Ltd (Indian manufacturer of graphite electrodes) also contributed about 1.0%, as did Cornerstone Building (building supplies in the US). Long detractors were all below 1.0% each and included Intelligent Systems which we expect to have a strong catalyst in 4Q. On the short side of the book, we had one retail-driven detractor who cost us about 2.7% and a handful of others detracting between 0.3% and 0.6%. These continue to be some of the most compelling shorts we have ever seen, but we acknowledge the need to manage risk and have intentionally kept them small, generally between 0.2% to 1.0% in size. Contributors on the short side included names like Chugoku Electric Power, which managed to defy the market as Japan continues to turn away from coal, falling 26% in the quarter.

While gross exposures ticked up to 159% at the end of June (from 148% at March month-end), net exposures remained virtually unchanged from the first quarter (72% in Q2 versus 74% in Q1). A slight decrease in Consumer net exposure was offset by a slight increase in Industrials. Regional exposures also remained relatively stable versus first quarter.

Portfolio Outlook And Positioning

Markets are stressing over a big uptick in U.S. inflation. The implications for valuations are material as high inflation will meaningfully impact price-to-earnings multiples. Speculative stocks are particularly vulnerable, i.e., periods reminiscent of 1972 or 2000. With that said, debate rages as to how sustainable the recent inflation pick up will be. We are not macro experts, but one can hardly ignore the underlying context: labor shortages exacerbated by epic unemployment benefits (the snapshot below speaks volumes), closed schools/lack of childcare leading to all manner of product and service shortages.

Consider that at least half (or more) of the May core inflation figure is attributable to record spikes in rental car rates, used car prices, travel and home costs. Who knows how transitory these will be, we are not sure ourselves. For the time being, however, we are watching the data very closely and, as always, considering our overall positioning within context. Our gross exposure continues to be towards the lower-half of its historical range while our net is at the mid-to-upper end, and we continue to focus on unique, idiosyncratic ideas whose fortunes should not pivot on short-term macro considerations. We feature a few of these ideas in the “Investment Highlights” section.

Shorting ‘Meme’ Stocks

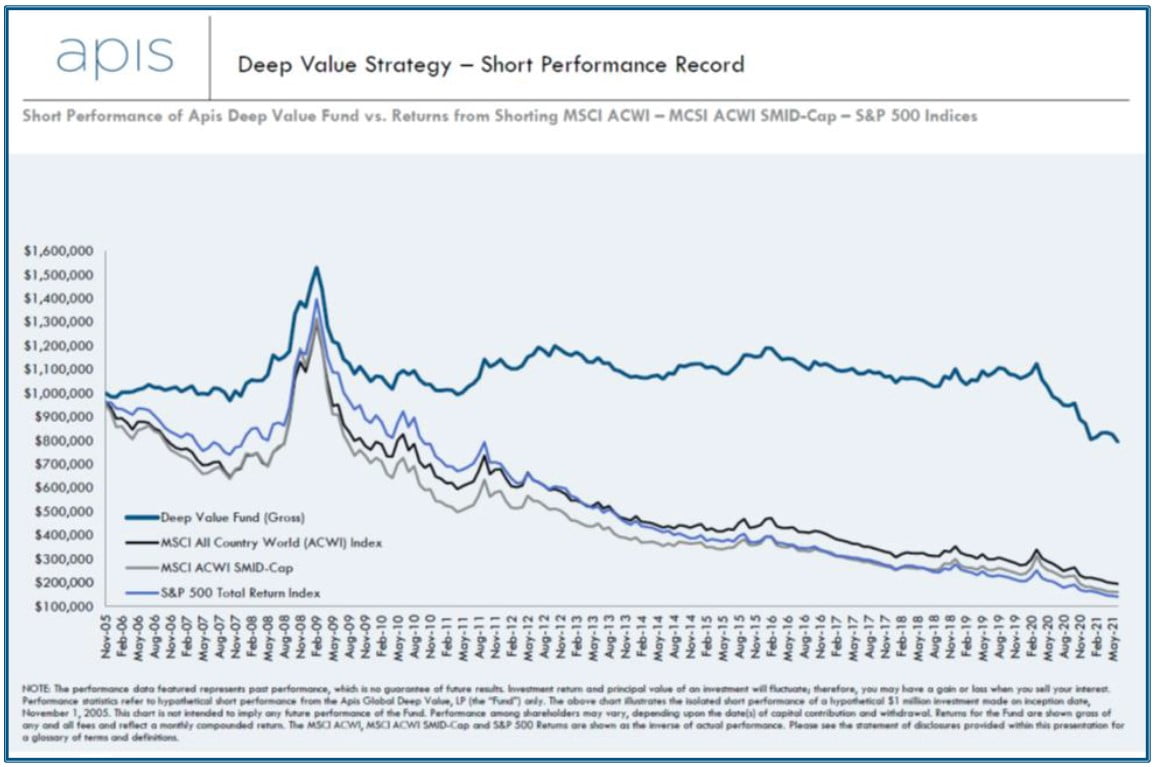

Given the unprecedented speculation it is worth spending a moment on the topic of shorting. Shorting has never been easy, but the last 18 months (for us at least) have never been more difficult. In our first 16 years, we essentially broke even on shorting, with 7 positive and 9 negative years. From the standpoint of alpha, we look much better as our shorts have relatively underperformed the market by a wide margin.

In some years such as 2008 or 2011, shorting has provided significant returns, mitigating, or completely erasing losses when markets were poor. From our global purview, no market looks as attractive today for shorting as the U.S.

There are many traditional reasons shorting stocks is difficult. Markets have a tendency to increase over time and managers/bankers are incented to push stocks higher. There are also technical challenges such as securing borrow, borrow costs and regulatory hurdles that raise the hurdle in achieving a profitable outcome. Now, in addition to these traditional challenges, there are some new reasons shorting has become more difficult. ‘Meme’ retail investors have banded together and are a new force to reckon with. Their behavior is completely irrational as they set out to destroy ‘evil’ short sellers. Shady managements band with these investors to silence critics knowing captured regulators have no intention of enforcing disclosure rules. Media (e.g., Jim Cramer) goad on retail investors, leading the unsophisticated to almost certain ruin (remember Cramer’s rant in March 2008 that Bear Stearns was “just fine,” only 5 days before it was bailed out for $2 per share by JPMorgan Chase?).

The ‘meme’ stock phenomena represents a new extreme against traditional fundamental analysis – bad news is now good. When the stock of a troubled business falls, the Reddit crowd takes offense, ganging up on short sellers in attempts to engineer a squeeze and ”stick it to the man”. When and if the stock falters, they egg each other on with “diamond-hands” emojis. It is weird and it has nothing to do with investing, but that is the current reality. Companies use this circus to issue stock (e.g., AMC went from 100 million to 500 million shares outstanding in last 18 months alone!) and executives, despite running their companies fundamentally into the ground, take advantage of the situation and pay themselves tens-of-millions of dollars in ‘compensation’. Option market makers (Wall Street) also get rich selling volatility.

One difficult aspect to rationalize is why short selling is targeted. Investors can believe a business is undervalued and worth more, so they buy it. Or they can believe a business is overvalued and worth less, so they sell it. Neither view is inherently good or bad. That money should flow toward good businesses and away from bad ones is why capitalism works. Short sellers provide a useful public good when they expose bad management or help to root out corruption. They are brave to take on the media and political forces that are closely aligned with their corporate benefactors. Ironically, meme investors prop up corruption and enrich bad managements while sending billions in premia to options desks – not exactly “sticking it to the man.”

How does Apis deal with this situation? Fundamentals will reassert themselves, but we cannot predict when. We have analyzed and, in some cases, shorted several businesses we believe are likely to fail. They are started as small positions (generally 20 bps to 50 bps in size) which we can add to when the tide turns. When it does, and even if we miss the early downside, we can add with our own “diamond” hands (okay, high conviction hands; we will never have diamond hands on anything!) when these situations become terminal. Let us not forget, in 2008 our average short fell 80%. Shorts kept us in the game under very difficult circumstances and considering the current speculative environment, they may again.

Investment Highlights

MaxCyte Inc. (U.K./U.S. – $1bn market cap)

We remain bullish on MaxCyte Inc (LON:MXCT), a U.K.-listed company headquartered in the U.S. focused on electroporation, a method of inserting genetic material into cells using electricity, particularly ahead of the expected near-term catalyst of a NASDAQ co-listing in the coming months. MaxCyte’s current core business is selling devices that eliminate the need for legacy viral-vector technology to develop and manufacture engineered cell therapies. MaxCyte is dominant in this segment and to date has signed 13 strategic platform licenses with leaders in the field such as Kite/Gilead, CRISPR Therapeutics, and Allogene encompassing more than 75 pipeline programs with potential developmental milestones of more than $950mm. While we estimate their current market share at a modest 2-3% of all developmental programs, their platform’s advantages over legacy viral-vector techniques give us confidence of continued penetration into a market expected to grow at 17% annually to more than $50bn by 2030. With these dynamics and assuming realistic expectations for regulatory success/approvals and conservative single-digit royalties, we estimate long-term recurring revenue potential in the hundreds-of-millions of $USD for MaxCyte.

Perhaps most important to the near-term performance of MaxCyte is the anticipated NASDAQ co-listing, which is gaining steam with the company scheduling a special meeting this month to vote on a series of proposals and amendments that will clear the path to NASDAQ registration in 2H 2021. Considering MaxCyte is a largely undiscovered name among U.S. investors with limited broker coverage as well as the historical precedent of companies that have followed a similar path to a U.S. listing, we fully anticipate the listing to be a strong share catalyst.

SUESS MicroTec (Germany – $600mm market cap)

SUESS MicroTec SE (ETR:SMHN) has been around for over 70 years and has a history of expertise in optical devices and other precision equipment. It currently provides systems used throughout the semiconductor production process and in some cases dominates with 70%+ market share. Süss has particular know-how in what has traditionally been known as the “back-end,” where processed wafers are diced and packaged. These last steps are becoming increasingly complex as semi makers try to fit more and more functionality into smaller chips, including by stacking chips on top of one another. Süss’s bonding and lithography machines enable the advanced packaging techniques that are required for 3D memory, 5G-enabled chips, and the sensor in your Apple watch that can determine your elevation and heart rate.

The company was mismanaged in the past, with numerous profit warnings and anemic sales growth even as end markets were strong. The poor track record left the stock largely orphaned with little analyst coverage. However, things started to turn around when Dr. Franz Richter took over as CEO in late 2017. Dr. Richter put out ambitious 2025 targets of reaching €400mm in sales and more than 15% EBIT margin by 2025, vs. the €167mm in sales and 8% EBIT margin that was reported in 2017. Execution to date has been good and recently the company has delivered 25% revenue growth with record profits. When we began looking at the company, Dr. Richter had already announced his early retirement, but we remained confident in the company’s ability to grow and execute on his targets.

After meeting the new CEO who took over in May, Dr. Götz Bendele, we are even more optimistic about the company’s future. Dr. Bendele previously worked in consulting with a focus on the semi industry, with his client TSMC eventually recruiting him. Immediately before taking the role at Süss, Dr. Bendele was the CEO of publicly traded LPKF Laser (ETR:LPK), leading a significant operational efficiency program over 3 years, during which time the stock price tripled. Given his past experience in both the semi industry and leading a public company overcoming operational issues, we believe Dr. Bendele can push Süss to potentially exceed the targets set by his predecessor.

As always, we encourage your questions and comments, so please do not hesitate to call our team here at Apis or Will Dombrowski at +1.203.409.6301.

Sincerely,

Daniel Barker

Portfolio Manager & Managing Member

Eric Almeraz

Director of Research & Managing Member

Apis Capital Deep Value Fund